Without a Protracted 'Tenglong Huanniao' Strategy, There Can Be No 'Big Fish in Big Waters' for Healthcare Entrepreneurship

As a top-tier investor in China’s venture capital community, Mr. Lu Gang, Partner at Legendstar Partners, began overseeing Legendstar’s operations in late 2009. He established the firm’s angel investment and incubation team and led direct investments in more than 70 healthcare projects. These include high-growth companies such as Tianjin Micro-Nano Core, Pacgen Biopharma, Kintor Pharmaceutical, Burning Rock Biotech, Ribobio, Co-Dx, ZhiKangBoYao, XinKangHe Biotechnology, Lightness Medical, Deepwise AI, and Xinyun Medical, as well as overseas companies including Axonics (which had its NASDAQ IPO in 2018), Urotronic, Abimmune Biopharma, NEUROVASC, and HiFiBio. The portfolio spans biopharmaceuticals, gene technology, medical services, intelligent technologies, and medical devices.

In 2018, Legendstar Capital completed the fundraising for its third fund, bringing its total number of managed angel investment funds to five, with a combined capital of approximately RMB 2.5 billion. In Lu Gang’s words, they are “well-stocked with ammunition” in healthcare investments.

At the “2019 Summit on Innovative Practices in Primary Healthcare,” Lu Gang delivered a keynote address titled “Empowering Primary Care: Bigger Waters, Bigger Fish.” Drawing from his extensive experience in healthcare venture capital and investment, he shared insights from both the investor and entrepreneur perspectives, clarified current trends and underlying dynamics in the healthcare sector, identified emerging opportunities, and provided strategic guidance for entrepreneurs.

This article is compiled from Mr. Lu Gang’s insightful speech, originally titled “Empowering Grassroots Healthcare: Bigger Waters, Bigger Fish.”

Mr. Lu Gang, Partner at Legendstar Capital, Delivers Speech at the 2019 Summit on Innovation and Practice in Primary Healthcare

In recent years, medical investment has experienced significant fluctuations, generating considerable buzz and leading to substantial bubbles and social fervor. As the hype subsides, skepticism has grown, particularly regarding the viability of internet-based healthcare. While primary care appears promising—backed by government funding and boasting a vast market—it remains fraught with challenges.

Today, my presentation will focus on Legendstar’s reflections and practices in response to these fluctuations. I will share three case studies from our investment and incubation portfolio, hoping to offer you some inspiration and assistance.

“No big fish in shallow waters”: What does “holding back” mean?

China’s current healthcare service structure resembles an inverted pyramid, which fails to address the pressing pain points in the sector. A substantial proportion of medical services are concentrated in tertiary Grade A hospitals. These tertiary hospitals account for approximately 50% of total patient visits, while the numerous lower-tier hospitals collectively handle the remaining 50%. In addition to disparities in patient case mix, there is also a significant gap in per capita healthcare expenditure.

Under the tiered diagnosis and treatment system, primary healthcare will undergo significant changes. Shifts in payment mechanisms are driving a substantial increase in patient volume at primary care hospitals. Building on an existing base of nearly 6 billion annual visits, patient numbers are expected to grow by an estimated 20%–30% per year. This growth, combined with changes in per-capita spending, will create a massively expanded market. Even if per-capita spending increases by just RMB 100, this would represent an incremental market worth RMB 60 billion—a considerably large market size, and this figure is a rather conservative estimate.

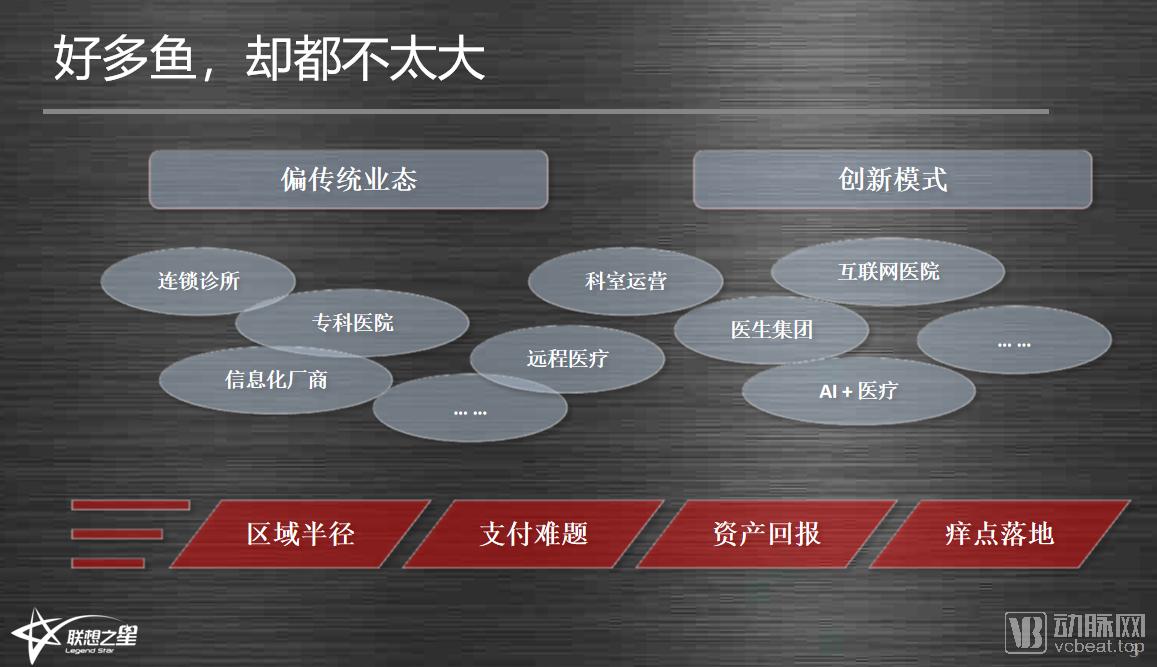

Given the vast size of this market, there is no shortage of healthcare startups. Many have introduced innovative business models, such as co-built clinical departments and integrated research-and-medical-care services. Others focus on more traditional operations, such as numerous conventional specialized hospitals. Yet, despite these extensive explorations within such a large market, few major players have emerged, if any at all. Why? I have outlined several constraining factors below.

Constraints include issues with regional radius, payment challenges, and asset return concerns. For instance, the return on investment is not high, the asset return rate is less than ideal, the overall capital investment is substantial, and the payback period is relatively long. Furthermore, the so-called solutions address only minor inconveniences (“itch points”) rather than critical pain points.

Among these, the most critical issues are payment challenges and the distinction between “nice-to-haves” and “pain points.” The payment system itself suffers from significant structural problems. Moreover, the focus has been on addressing “nice-to-haves” rather than true “pain points,” resulting in relatively low returns on assets. This has led to vigorous government promotion, yet substantial obstacles remain.

“The Cage-Swapping Strategy”: A Protracted War in Healthcare

Given our long-standing investment history in the healthcare sector, I delivered a speech in 2016 addressing the constraints facing the healthcare industry. I encourage you to review it and analyze the issues raised therein.

Startups in new medical services may rapidly heat up, but the ecosystem of this industry is extremely complex. While there are favorable driving factors, the constraining forces are also very powerful. The ecosystem chain, dominated by the “Big Four”—large tertiary hospitals, senior department heads, major pharmaceutical and medical device manufacturers, and large-scale medical insurance payers—is unlikely to change in the short term. Although there are four major shortcomings, namely “lack of information flow, lack of core physicians, lack of incentive mechanisms, and lack of payment power,” their influence remains very weak.

The healthcare industry requires a protracted war; do not expect quick victories or rapid, explosive returns. The future is bright, but the path is tortuous. Without the mindset for a long-term struggle, you may falter midway. Do not approach a marathon with the mentality of a sprinter.

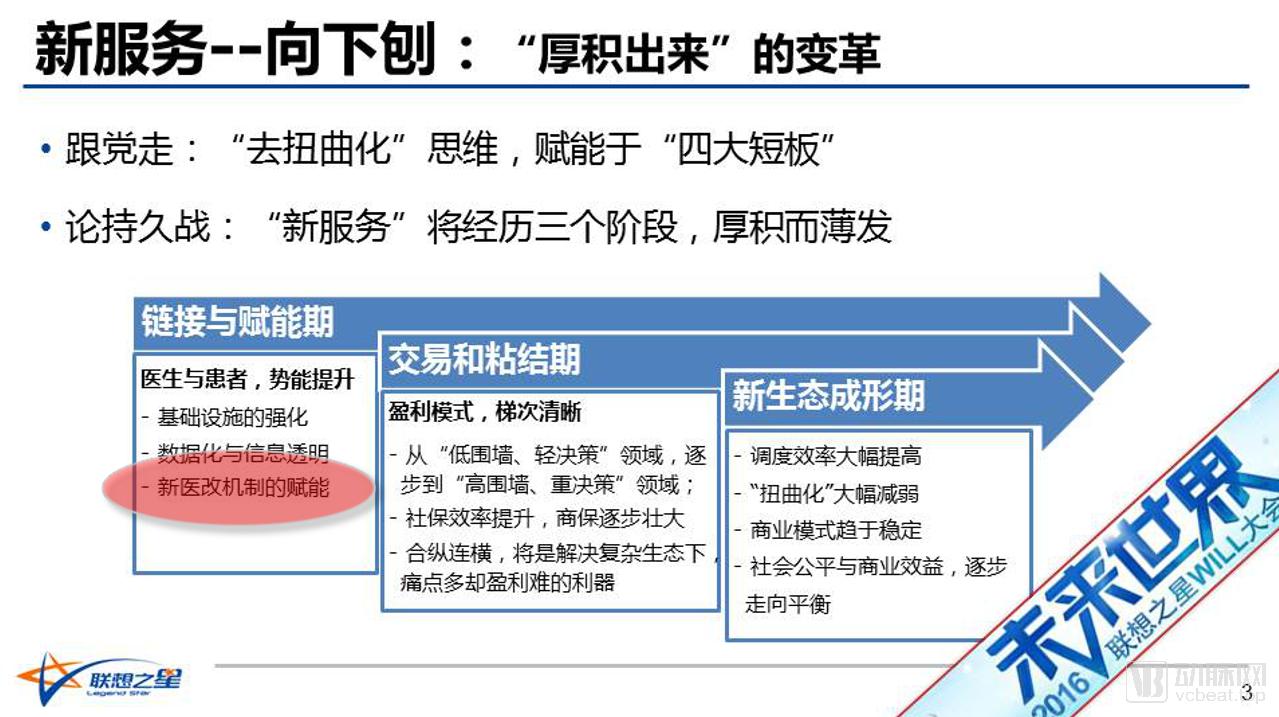

In 2016, we conducted an analysis that divided the healthcare sector into three approximate phases: I. Connectivity and Empowerment Phase; II. Education and Stickiness Phase; III. New Ecosystem Formation Phase. Only after these three phases are completed will the overall healthcare landscape reach maturity, and significant entrepreneurial and commercial opportunities will emerge during this transitional process. We are currently still in the first phase. The duration of this first phase depends primarily on the empowerment driven by new healthcare reform mechanisms; other factors are secondary. Without progress in healthcare reform, it is difficult for other aspects to gain momentum. (See details in“Legendstar Capital’s Lu Gang: Healthcare Investment May Shift from Defensive to Offensive”)

Payment reform is the “key link,” where a single move affects the entire system. With the changes in payment mechanisms, the first phase can be said to be nearing its end, marking the transition between Phase I and Phase II.

Following the launch of tiered diagnosis and treatment in 2015, the model of “subsidizing healthcare through drug sales” began to phase out, inevitably giving way to a system where healthcare is sustained by service revenues. The introduction of the “4+7” policy in July 2018 sent shockwaves through the industry, sparking widespread wait-and-see attitudes and controversies. Coupled with the establishment of the National Healthcare Security Administration and a series of resolute, incisive reform measures, what did this signal? It signaled the end of the era of “subsidizing healthcare through drug sales.” This is a positive development, as the previous model had caused significant distortions—not only in drug pricing but also throughout the entire medical service fee structure. Those who fail to recognize this shift and continue to operate under outdated mindsets and rules are destined to be eliminated.

Traditional market forces are still in a phase of strategic maneuvering and have not yet rapidly evolved to a model where medical services sustain healthcare providers. Therefore, I believe the endgame must inevitably be one where medical services fund healthcare delivery; this is not something to challenge, or you risk becoming an obsolete force. However, having identified this endgame does not mean the world has changed overnight. The strategic interplay during this transition is quite complex, involving continuous “structural replacement” (teng long huan niao), making a tortuous path the new normal.

With these insights, we may gain a clearer understanding of our future direction. Whether from an investment or entrepreneurial perspective, how can we identify the “big fish” amid such opportunities? Currently, the “small fish” lack growth potential, while the “flying fish” remain all talk and no action, unwilling to come down to earth.

How to Become a “Big Fish”?

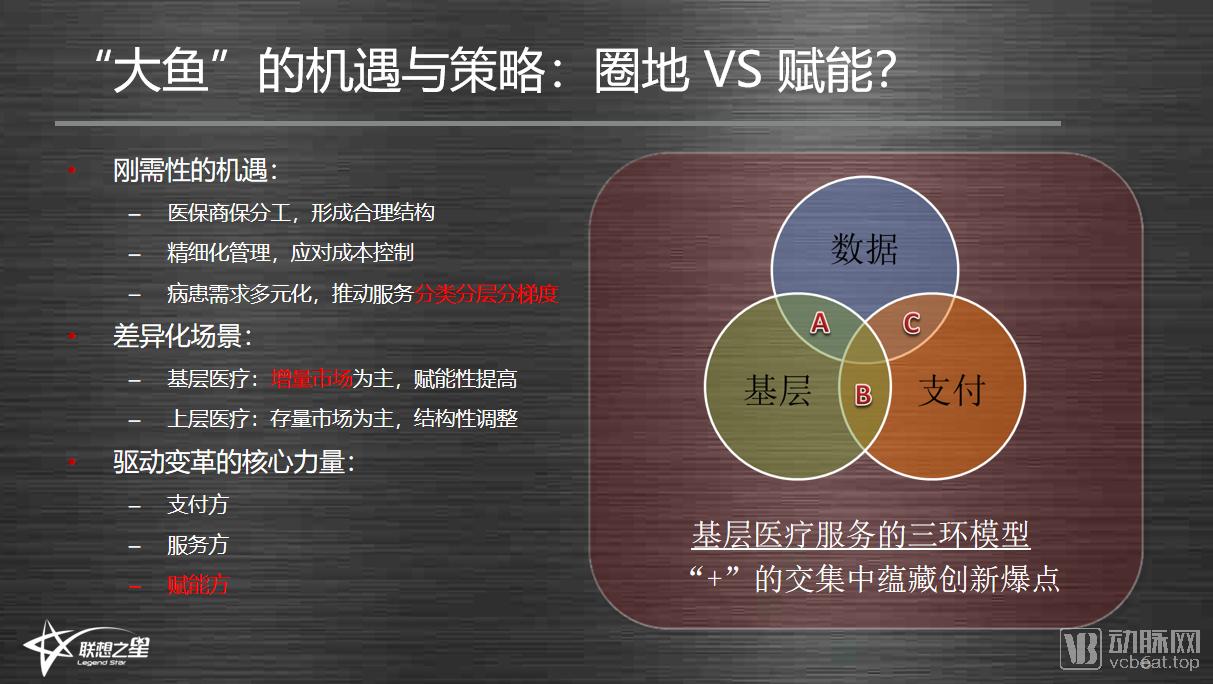

Seeking Opportunities to Become Industry Giants: Two Current StrategiesSome large healthcare groups are engaging in territorial expansion, acquiring and strategically positioning hospitals. They adopt a land-grab mindset for entrepreneurship, aiming to emerge as industry giants. Another approach focuses on “empowerment” initiatives at this stage. We do not judge which strategy is superior; however, as early-stage investors, we believe that prioritizing the empowerment strategy at present is more likely to foster the emergence of additional industry leaders.

Why adopt such a strategy? Because China’s healthcare challenges are fundamentally supply-side issues, and empowerment is undoubtedly an essential means to address them. In terms of empowerment, the ability to facilitate it—determining who can provide empowerment, through what methods, and in which areas—constitutes the foundational condition for becoming a “major player.” I have listed some typical elements below:

First, there are rigid-demand opportunities in the market. These rigid-demand opportunities can be further categorized by type, tier, and gradient. How exactly are these tiers defined? For instance, tier-1 and tier-2 cities versus tier-3 and tier-4 cities; tertiary hospitals versus secondary and primary hospitals, down to clinics. How are these gradients delineated? Only through such granular segmentation can one identify opportunities within the unique context of China’s healthcare environment.

Second, differentiated scenarios. When we started our venture, we were reluctant to compete in saturated markets. Under the current payment reforms, do you consider the growth potential for patient volume and revenue at tertiary hospitals to be incremental or existing? Is the primary care sector an incremental or existing market? My perspective is to prioritize incremental opportunities and avoid competing in saturated markets as much as possible. Primary care represents an incremental market, but it requires empowerment. Those who can provide such empowerment will be the ones to succeed.

In incremental markets and stock markets, the business models that can become dominant players also differ. The stock market should undergo structural adjustments to help improve efficiency; while the incremental market is an empowering market, where helping others enhance their capabilities is key. These are actually two different scenarios that must be distinguished, as they represent entirely different business logics.

Business Innovation Requires a Different “+” Approach

Here, I have consistently emphasized empowerment. But what exactly is empowerment?

The three-ring model illustrated in the figure addresses the various “+” models that have been prevalent in the past, yet none have been particularly well executed. Models such as “Primary Care + Data” exhibit moderate monetization potential. The model with the strongest practical monetization capability is “Payment + Primary Care.” Currently, favorable policies from the payment system are supporting primary care, making this area the most effective for monetization, although it has the weakest explosive growth potential. Industrial institutions favor investing in this sector primarily because the revenue streams are clearly visible.

Regarding the topic of “+,” it was mentioned at VCBeat’s “2018 Top 100 Future Healthcare Forum.” Over the years, despite all the efforts to integrate various elements through this “+” approach, why have we failed to address the pain points in the healthcare market? Why have we been unable to generate revenue across all segments? I have reached a conclusion: the business logic was flawed. The “+” strategy was misapplied; it merely added tools without addressing the essence of business. (See details“Chaos, Heroes, and the Sword: A Guide to Healthcare Entrepreneurship in the Age of Warlordism”)

Why is the business logic flawed? It is evident that many “Internet + Healthcare” companies are now establishing offline clinics and hospitals, shifting their focus to physical operations in a model known as online-offline integration. Why is this integration necessary? Because a purely online model cannot resolve the underlying issues; it is essential to encompass the surrounding ecosystem. Ultimately, these companies find themselves reverting to an offline model, returning to traditional practices.

“AI + Healthcare” is inherently an asset-light sector. AI companies have flocked to develop applications for pulmonary nodule detection, breast cancer screening, and fundus examination, among others. As a result, their diagnostic performance has become largely homogeneous, reducing AI to mere software and transforming AI firms into software vendors. Hospitals procure such software primarily based on price competitiveness, rather than adopting a per-capita fee model. Whether hospitals purchase the software outright or integrate it with hardware, AI companies ultimately revert to the status of traditional enterprises, making it unsustainable to justify their previously high valuations.

Therefore, if one aspires to become a major player and seize significant opportunities, achieving this within a single segment of the ecosystem presents considerable challenges. At a minimum, two segments must be integrated: either “Primary Care + Payer” or “Primary Care + Data.” Only through the synergy of these two segments can substantial commercial growth potential be unlocked, with the “+” symbolizing the true catalyst for innovative breakthroughs.

Within this “+” framework, the primary focus should be on opportunities driven by essential needs. Secondly, healthcare services constitute a complex market that will inevitably undergo stratification, with the two most significant tiers being the primary care sector and the high-end sector. The primary care segment represents an incremental growth market; however, it remains relatively weak at present and requires empowerment-driven enhancement. Thirdly, there are core driving forces. Regardless of whether in the primary care or high-end sector, the core drivers consist of three parties: payers, providers, and enablers. Payers include basic medical insurance, commercial insurance, and individuals whose consumption is upgrading. Providers refer to physicians and medical institutions, while enablers pertain to those supporting the activities undertaken by these stakeholders.

Sharing Three Cases: Which Disease Types Are Suitable for Primary Care?

A notable case that has prompted significant reflection and drawn the attention of regulators is the grassroots ophthalmology project. Ophthalmology addresses a critical pain point well-suited for primary care settings, but this business model has been severely undermined. Why? Because excessive greed among investors led to over-exploitation and unrealistic growth expectations, thereby damaging the entire industry and this specific niche sector. Indeed, some directors of grassroots hospitals now immediately reject any proposals involving similar models.

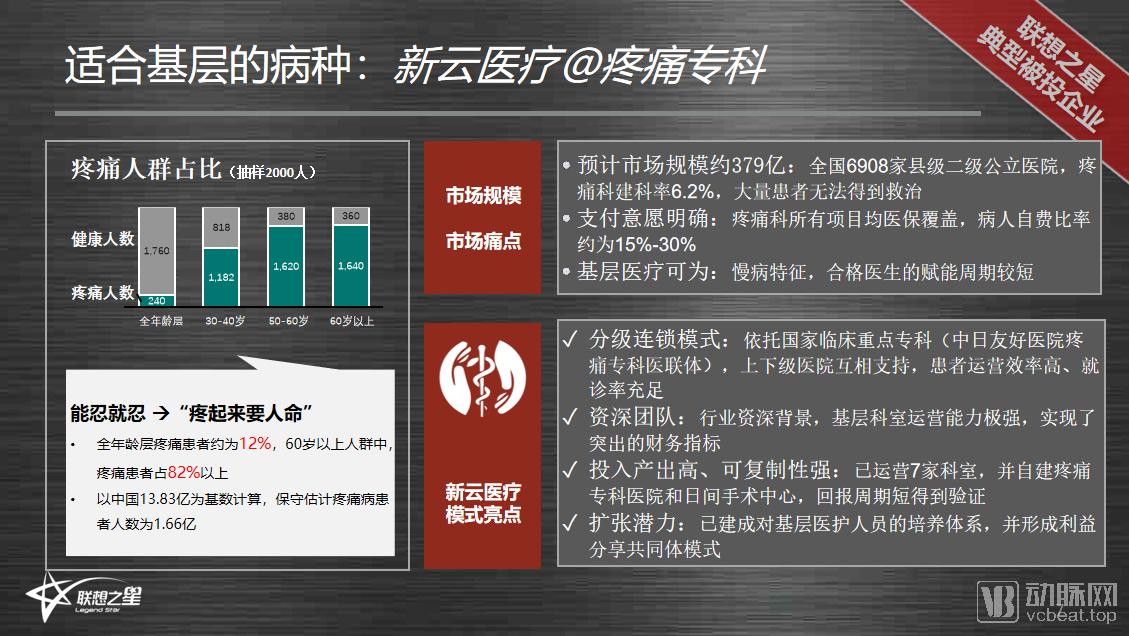

In addition to ophthalmology, many other medical conditions are well-suited for primary care settings. For instance, pain management represents a growing market with inelastic demand. Middle-aged and elderly patients demonstrate a strong willingness to pay for pain-related treatments. Pain-related conditions are covered by healthcare reforms, meaning there are no significant structural barriers to reimbursement, and payment willingness is driven by the urgent need to alleviate suffering. However, what are the challenges? The primary issue lies in the clinical efficacy of specialized pain management. Can high-quality service outcomes be delivered to ensure patient satisfaction at the primary care level? Furthermore, it remains questionable whether primary care hospitals and physicians have the capability to launch such specialty services and whether they can be adequately empowered to do so.

Xinyun Medical has precisely identified disease conditions that are well-suited for primary care settings.

Patients with pain issues cannot visit top-tier or Grade 3A hospitals every one to two weeks, as the cost and logistical burden are prohibitive; therefore, their care needs to be addressed at the primary care level. Xinyun Medical has adopted a tiered chain model, leveraging the nation’s most prominent specialized medical consortia to enable mutual support between upper- and lower-level institutions. Through exploration, this approach has ensured adequate patient consultation rates. Xinyun boasts an experienced team with strong industry backgrounds and has achieved solid financial performance, with healthy metrics for individual clinics—a crucial prerequisite. Furthermore, Xinyun demonstrates high replicability. It currently operates seven clinical departments, has established its own pain specialty hospital and ambulatory surgery center, and has validated its return-on-investment cycle.

If a project merely achieves these points, it remains a “small fish.” To survive in the market and grow into a “big fish,” it must possess expansion potential. This requires establishing a training system for primary care healthcare professionals that truly empowers them—not only by enhancing their capabilities but also by aligning their financial incentives, thereby creating a closed-loop benefit structure. When patients seek care, they receive effective treatment, while primary care institutions and physicians also generate profits, fostering sustainable development through combined profitability and capability growth. As further expansion becomes necessary, the project will have stronger reserves and lower costs associated with scaling up.

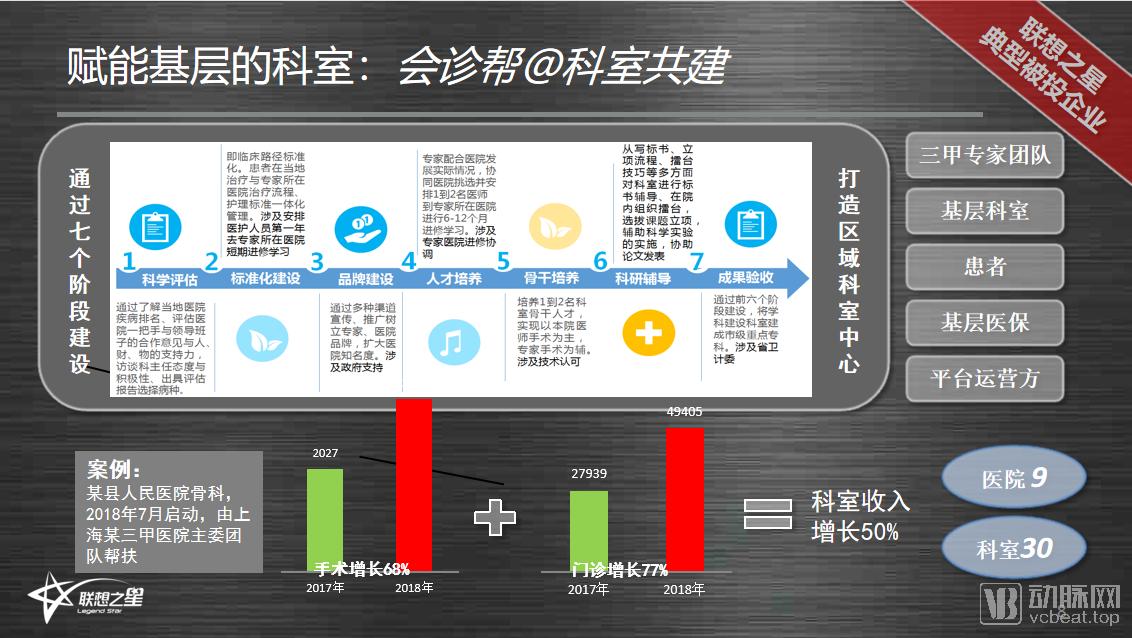

The second case involves empowering primary-care departments, using a co-construction model similar to that employed with individual departments.

“Flying knife” procedures are also empowering grassroots departments, as are joint department-building initiatives between higher-tier and lower-tier hospitals. However, such empowerment is extractive in nature; for instance, the primary goal is simply to earn a fee per surgery, without transferring capabilities to grassroots institutions, making it a short-term endeavor. In conversations with many hospital presidents, they have noted that while these political mandates must be fulfilled, the lack of enthusiasm among doctors and departments often results in implementation that addresses only “nice-to-have” issues rather than “pain points,” failing to evolve into a sustainable, long-term initiative.

Our investment in Huizhenbang also focuses on co-building medical departments, with the goal of establishing regional specialty centers and strengthening their capabilities. In this process, it has formed a community of stakeholders—including tertiary Grade A hospitals, primary-care departments, and patients—and achieved a more equitable distribution of benefits among them. This approach not only reinforces core value but also ensures that all parties benefit through this shared-interest community, enabling the platform to achieve sustainable growth. Huizhenbang is currently experiencing strong performance growth, with many hospitals partnering with it. Where once they were turned away at the door, they are now welcomed as honored guests, primarily because Huizhenbang helps hospitals deliver greater value and enhance their capabilities.

AI + Healthcare: Not only was it a hot topic in the past, but its current momentum has also remained strong. The greater challenge now lies with platform-based AI solutions. Significant differences exist across various disease categories, and there is little cross-specialty patient flow or data sharing, resulting in numerous barriers and making implementation difficult. Consequently, vertical AI solutions are easier to deploy. Their revenue models are more secure, as they have already secured approvals for medical service pricing and national health insurance reimbursement. This sector offers sustainable entrepreneurial opportunities, with the primary question being the height of the growth ceiling.

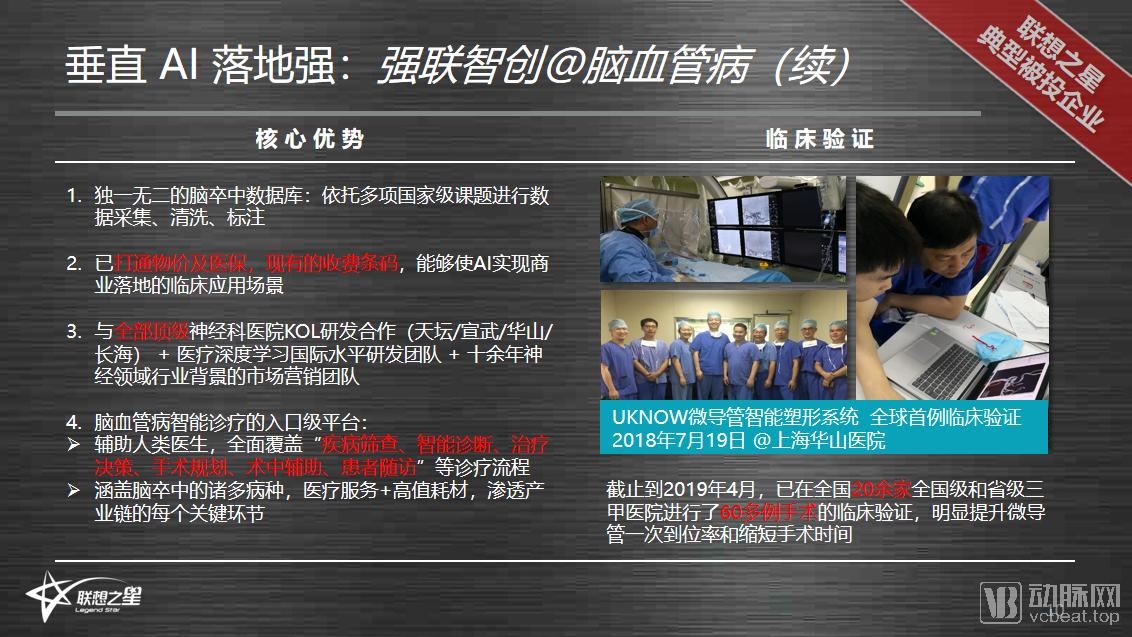

The final case I will share is QiangLian ZhiChuang, which leverages AI-powered intelligent diagnostic services to address challenges in the field of stroke.

QiangLian ZhiChuang has established R&D collaborations with key opinion leaders (KOLs) at top-tier neurology hospitals, including Tiantan Hospital, Xuanwu Hospital, Huashan Hospital, and Changhai Hospital. The company boasts an internationally competitive R&D team specializing in medical deep learning, as well as a marketing team with over a decade of experience in the neurology field. Furthermore, it has built an entry-level platform for the intelligent diagnosis and treatment of cerebrovascular diseases, assisting physicians across the entire clinical workflow—including disease screening, intelligent diagnosis, treatment decision-making, surgical planning, intraoperative assistance, and patient follow-up. Future offerings will also encompass various value-added services and consumables.

By delivering medical value across multiple layers—from top to bottom and from front to back—StrongLink AI has established robust collaborations with over 20 hospitals in intraoperative planning and intraoperative assistance.

Medical entrepreneurship requires a broad-minded vision that embraces the world.

The grassroots market holds immense potential; avoid adopting an aloof attitude and instead identify critical pain points characterized by significant disparities in service accessibility or resource distribution. Within specialized domains, practitioners should further refine their positioning to find the best fit. Unwavering commitment to this strategy is essential for securing a promising future.

Regarding the pace of development: Does slower growth make it harder to attract investors? Investment requires returns, and mindsets differ between fast- and slow-growth strategies. What are the core metrics driving rapid growth? Is it revenue and profit, or patient reputation? Entrepreneurs need to understand the growth logic of grassroots medical services and thereby adjust their mindset regarding growth pace.

Finally, a broad strategic perspective is essential. Within the “+ Healthcare” model, services exhibit strong regional characteristics, leading to a fragmented market landscape dominated by local players—a situation likely to persist in the long term. Nevertheless, we must maintain a nationwide vision. Another key aspect is the “high-density, high-frequency” development strategy. Many tasks, such as managing individual patients’ consultation times and providing pre- and post-consultation care, are either beyond the capacity or willingness of tertiary (Grade III) hospitals due to time constraints. In contrast, primary care institutions can deliver these services more comprehensively. When expanding business models, we need to increase service density and frequency to genuinely enhance the quality of primary healthcare services.

Thank you all!