Premium Healthcare Market Report: 2.29 Million High-Income Consumers Drive Rapid Growth, Nearly 100 Brands Compete

Upgraded demand inevitably drives supply-side reform, and the growing number of high-income individuals has fueled the development of the premium healthcare market. Driven by consumption upgrades, policy liberalization, and capital investment, the premium healthcare market has entered a growth phase. By 2018, the number of premium healthcare brands had reached nearly 100, with services covering first-tier cities and selected second-tier cities across China; Beijing, Shanghai, and Guangzhou have emerged as their primary markets.

High-end healthcare and primary care differ in market positioning, leading to variations in the content and quality of medical services provided. What are the characteristics of high-end healthcare users? How do medical service institutions operate? And what roles can third-party consultation platforms play?

VCBeat, in collaboration with Yiguo Doctor, jointly released the “Report on the Development of the High-End Medical Market in the Context of Consumption Upgrading,” aiming to clarify the aforementioned issues through the analysis and organization of relevant data from the high-end medical market.

The data in this report are primarily derived from field research conducted at select high-end medical institutions, the VCBeat database, and the backend database of Yiguo Doctor. We believe that, supported by these data, the current state and future trends of the high-end healthcare market can be reflected and discussed with greater accuracy and authority.

High-end medical care differs from primary care in that it provides personalized, high-quality medical services tailored to higher-income individuals. It is characterized by distinct personalization, higher fees, thorough doctor-patient communication, and extended consultation times. Services are delivered exclusively by senior physicians, most of whom have prior experience at large tertiary Grade A hospitals.

According to Deloitte’s 2017 survey on medical satisfaction among Chinese consumers, only 21% of respondents expressed satisfaction with the current healthcare service system. When price sensitivity is low or when covered by high-end commercial health insurance, consumers are willing to shift toward premium healthcare services that offer superior quality, including those provided by private medical institutions and special-needs outpatient clinics or international departments at public Grade 3A hospitals.

It can effectively address the “three long waits and one short visit” issue in basic medical services (long registration times, long queueing times, long medication dispensing times, and short consultation times), create a comfortable healthcare environment and high-quality patient experience, and meet the medical service needs of individuals across different income levels.

Comparison Between Premium Healthcare and Primary Care

Data Source: VCBeat · VBInsight

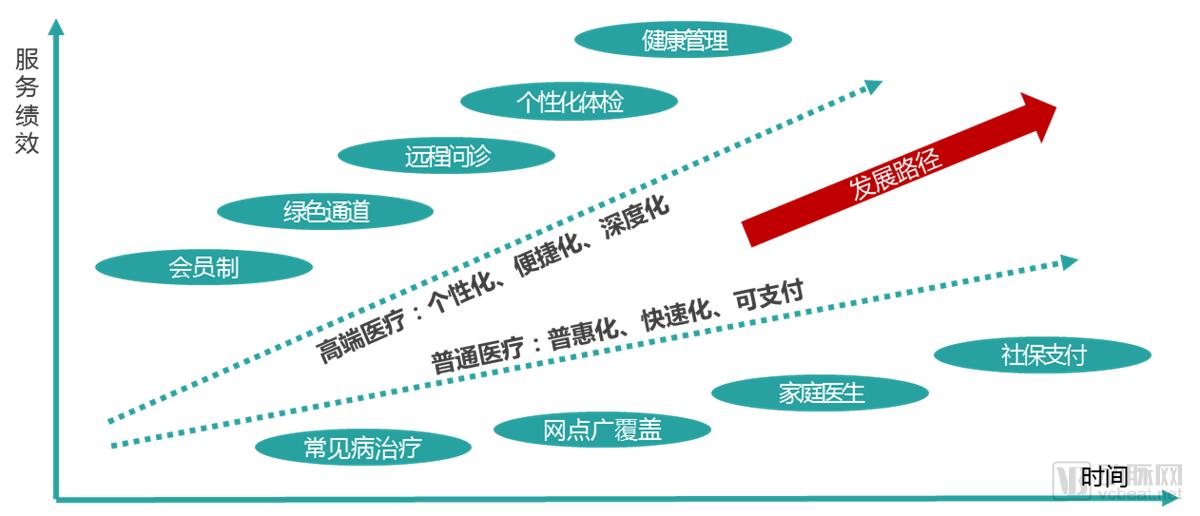

Due to the differing positioning of high-end healthcare and primary care, their development paths are also distinct. Primary care will evolve along the lines of universal accessibility, efficiency, and affordability, with a focus on the treatment of common diseases.

Primary healthcare should expand its network coverage as much as possible to serve more patients, while improving the quality of grassroots medical services through the family doctor system. Considering the affordability for ordinary residents, it is also necessary to include more medical expenses in the social insurance reimbursement system.

Meanwhile, premium healthcare is evolving toward personalization, convenience, and depth. By implementing membership-based management, it establishes green channels for patient registration, appointment scheduling, and consultations, thereby making medical care more accessible. Moreover, for high-income individuals, disease treatment represents only a basic need; their primary focus lies in disease prevention and health management.

Therefore, it is essential to deepen medical services by expanding into high-value-added offerings such as remote consultations, personalized health screenings, and health management, while developing tailored health management plans for individual patients.

Comparison of Development Paths Between High-End Healthcare and General Healthcare

Image source: Chart by VCBeat·VCBeat Research Institute

Compared with primary care, premium healthcare demands higher standards in service content and quality; therefore, it must demonstrate its distinctiveness in service workflows, service teams, medical equipment, and clinical processes.

Commercial Healthcare Institutions Possess Five Key Value Points

Image source: VCBeat · Eggshell Research Institute

The consultation process in premium healthcare is highly patient-centric. Professional staff communicate with patients regarding appointment scheduling, physician profiles, and procedural workflows. Furthermore, certain institutions provide dedicated companions throughout the entire visit to address any patient needs promptly.

Most physicians providing diagnostic and treatment services are affiliated with large tertiary hospitals, hold senior professional titles, and include many renowned experts in their respective fields, thereby ensuring high-quality medical care. Some high-end medical institutions offer services in foreign languages such as English, Japanese, and French, or directly employ foreign specialists to address language barriers for international patients.

High-end medical institutions are willing to introduce the latest medical equipment, which is fully functional, highly intelligent, and offers high detection accuracy. In addition, the entire medical service process is highly standardized, with strict adherence to protocols in every step—including consultation, registration, diagnosis, examination, treatment, medication dispensing, and payment—thereby providing patients with a novel healthcare experience. High-end medical services encompass not only basic services such as disease treatment but also extended services like health management and overseas medical care, thereby meeting the diverse healthcare needs of patients.

High-end medical services in China mainly come from two major sources: commercial healthcare institutions and special-needs medical services provided by public hospitals. Special-needs medical services in public hospitals primarily refer to medical service activities conducted to meet specific healthcare demands, on the basis of ensuring basic medical needs. These services include designated surgeries, overtime surgeries, comprehensive nursing care, special-needs wards, and expert outpatient clinics, which initially mainly served foreign guests and high-ranking officials.

Public hospitals have established specialized VIP outpatient clinics or International Medical Departments (Centers) to provide the aforementioned services, such as the Peking Union Medical College Hospital International Medical Center and the China-Japan Friendship Hospital International Medical Department. In May 2015, the General Office of the State Council issued the “Guiding Opinions on Pilot Comprehensive Reform of Urban Public Hospitals,” which explicitly stipulated that the scale of special-needs services in public hospitals should be controlled, with the proportion of such services not exceeding 10% of total medical services. This means that the development of special-needs medical care in public hospitals will be strictly restricted.

Unlike public special-needs services, commercial healthcare institutions face no scale restrictions. In recent years, their numbers have grown steadily, with various private hospitals and clinics being established in succession, thereby becoming the dominant force in high-end healthcare.

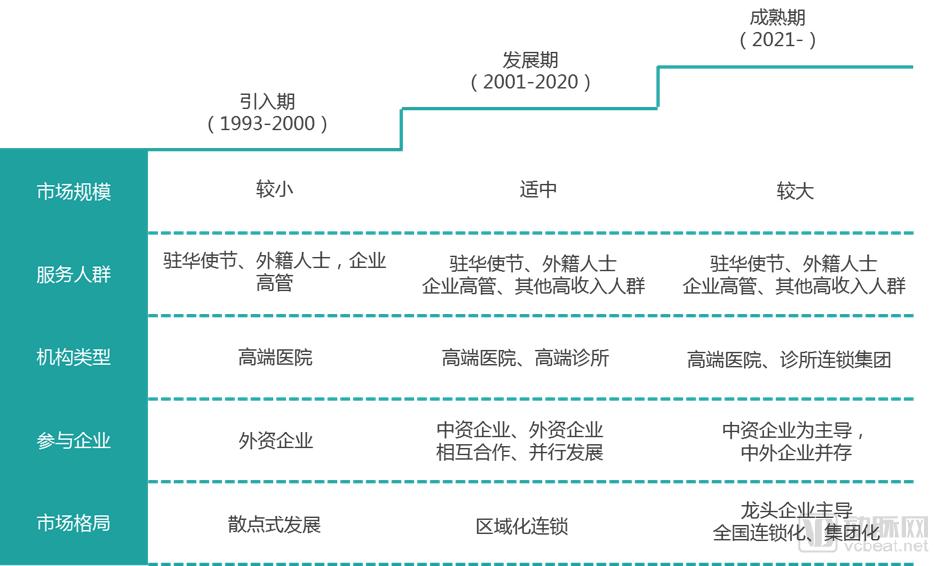

The development of high-end healthcare in China is primarily divided into three stages: the introduction phase, the growth phase, and the maturity phase. Currently, it has entered the second phase. Each stage exhibits distinct characteristics in terms of market size, target population, types of medical institutions, participating enterprises, and market landscape.

(1) Introduction Phase (1993–2000)

High-end medical services were introduced from Hong Kong and abroad. In 1993, Dr. Fang Xinrang, a medical expert hailed as the “Father of Rehabilitation,” jointly established with the former Ministry of Health the first high-end medical institution in mainland China—the Beijing-Hong Kong International Medical Clinic (now known as the Beijing Hong Kong-Macao International Medical Clinic)—to meet the healthcare needs of expatriates in Beijing.

In 1997, United Family Healthcare, a renowned high-end medical institution in the United States, established its first premium private hospital in Beijing—Beijing United Family Hospital, primarily providing medical services to diplomatic envoys stationed in China, expatriates working in China, and affluent individuals.

In 2000, Vista Clinic was established, providing international diagnostic and treatment services. During this phase, high-end healthcare was primarily concentrated in Beijing, serving a limited population with very few medical institutions.

(2) Development Phase (2001–2020)

During this phase, China saw the emergence of high-end healthcare brands represented by ParkwayHealth, New Century Healthcare, Amcare, HarmonyCare, and Aiyuhua Healthcare.

In 2005, ParkwayHealth opened the Shanghai Parkway Huaying Outpatient Clinic in Shanghai, bringing international high-quality healthcare services to the city.

In 2006, Beijing New Century Children’s Hospital officially commenced operations, followed by the establishment and launch of Beijing Shengbao Obstetrics and Gynecology Hospital, Beijing Hemei Women’s and Children’s Hospital, Honghua Clinic, and Jiahui Clinic. To date, New Century Healthcare Group has established multiple facilities in Beijing.

In addition to Beijing United Family Hospital, United Family Healthcare has opened multiple satellite clinics and established United Family Hospitals in Shanghai, Tianjin, and Qingdao.

Furthermore, Chinese and foreign enterprises have strengthened their cooperation. Fosun Pharma acquired a stake in China-USA United Medical Imaging Healthcare (CUMIH), with both parties jointly promoting the development of United Family Healthcare in China. Lenovo Group partnered with the U.S. investment firm Warburg Pincus to establish Amcare USA Medical Group, which has opened multiple medical institutions in cities such as Beijing, Tianjin, Shenzhen, and Hangzhou.

It is evident that during this phase, Chinese and foreign brands developed in parallel, with some brands achieving regional chain operations. The patient demographics served by these medical institutions included not only expatriates but also corporate executives and other high-income groups.

(3) Maturity Stage (2020–Present)

A key indicator of an industry entering its maturity phase is the emergence of leading enterprises and a stabilizing market landscape. According to forecasts by Deloitte, China’s high-end healthcare market was expected to enter a mature stage after 2020, during which leading companies would leverage their advantages in capital, technology, talent, and management to establish nationwide chain operations, thereby further increasing market concentration.

China's High-End Healthcare Has Entered a Growth Phase

Image source: Chart by VCBeat·VCBeat

China’s high-end healthcare market is in a phase of development. What are the driving forces behind this growth, and how are these factors propelling the advancement of China’s high-end healthcare sector?

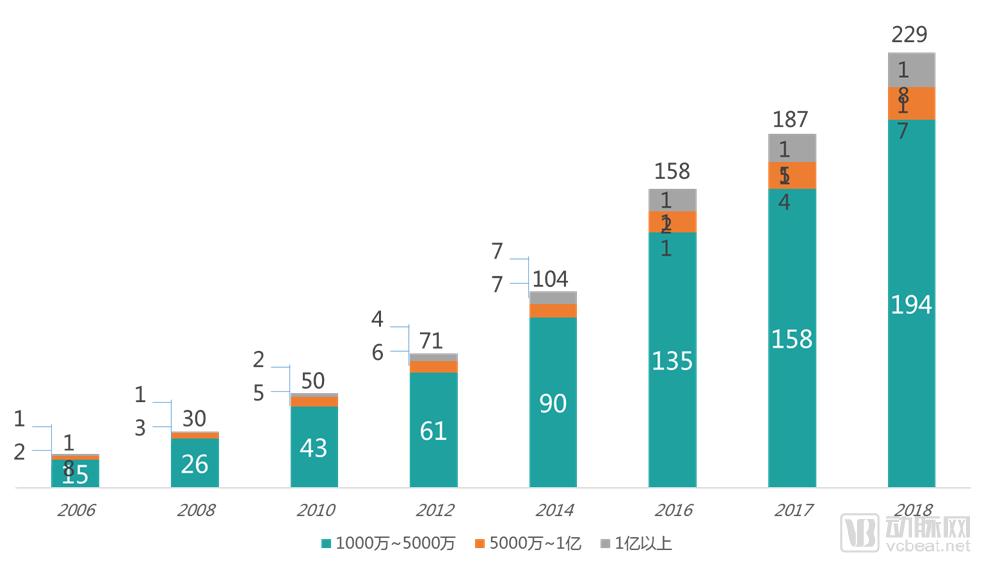

In 2018, the number of high-net-worth individuals in China reached 2.29 million.

Note: High-net-worth individuals refer to those with disposable assets exceeding RMB 10 million. Source: Bain & Company

High-net-worth individuals constitute a significant portion of the high-income population. As income levels in China continue to rise, the number of high-net-worth individuals has been growing steadily. In 2018, this group reached 2.29 million, with a compound annual growth rate (CAGR) of 22.3% over the past decade, indicating that the scale of China’s high-income population is expanding year by year.

High-income individuals report low satisfaction with existing public healthcare services, seeking superior private medical care and demonstrating a willingness to pay higher premiums for it. Furthermore, beyond basic disease treatment, they desire personalized ancillary services such as health management, disease prevention, and screening—offerings that the public healthcare system fails to adequately provide. Consequently, rising income levels, particularly the expansion of the high-income demographic, have generated market demand conducive to the development of premium healthcare services.

Income levels determine consumption levels, and rising incomes inevitably drive consumption upgrades. As healthcare constitutes a significant component of household consumption expenditure, income growth also alters the nature of people’s healthcare spending.

Previously, healthcare consumption by residents was primarily concentrated in high-medical-necessity scenarios, such as appointment scheduling and disease treatment. Currently, however, resident healthcare spending has expanded beyond these core medical services to include scenarios with significant consumer attributes, such as disease screening, health management, obstetrics and gynecology hospitals, dental clinics, plastic surgery centers, and postpartum care facilities. These areas constitute the key service offerings of premium healthcare. Consequently, consumption upgrading has driven the rapid development of the premium healthcare sector.

Consumption Upgrading Drives the Rapid Development of Consumer-Oriented Healthcare

Image source: VCBeat chart

Against the backdrop of deepening healthcare reform, encouraging private investment in medical services has become an inevitable trend in the development of the healthcare industry. The state has lowered market entry barriers for foreign-invested and privately funded medical institutions, and its access policies for their entry into the healthcare service sector have undergone a process of continuous deepening and refinement, evolving from macro-level to micro-level frameworks.

Policies have relaxed restrictions on foreign and private capital establishing medical institutions.

Data Source: VCBeat Database

(1) Relax restrictions on foreign investment in healthcare institutions

The establishment of foreign-funded medical institutions is highly complex, with government policies shifting from strict restrictions to gradual liberalization.

In April 1997, the former Ministry of Foreign Trade and Economic Cooperation issued the Supplementary Provisions on the Establishment of Foreign-Invested Hospitals, which stipulated that foreign-funded medical institutions entering China must engage in joint investment and joint operations with Chinese medical institutions or other entities.

In July 2000, the former Ministry of Health and the former Ministry of Foreign Trade and Economic Cooperation jointly issued the Interim Measures for the Administration of Sino-Foreign Equity Joint Venture and Cooperative Medical Institutions, which further stipulated that the Chinese party’s equity share or interests in such institutions shall not be less than 30%, and the term of the joint venture or cooperation shall not exceed 20 years.

Ten years later, the Notice on Forwarding the Opinions on Further Encouraging and Guiding Social Capital to Establish Medical Institutions, issued by the General Office of the State Council, proposed piloting and gradually relaxing restrictions on qualified foreign capital establishing wholly foreign-owned medical institutions within China. This marked the first policy signal released in favor of wholly foreign-owned medical institutions.

Subsequently, the Interim Measures for the Administration of Wholly Foreign-Owned Medical Institutions in the China (Shanghai) Pilot Free Trade Zone and the Notice on Launching Pilot Programs for Establishing Wholly Foreign-Owned Hospitals explicitly permitted overseas investors to establish wholly foreign-owned hospitals in seven provinces and municipalities—Beijing, Tianjin, Shanghai, Jiangsu Province, Fujian Province, Guangdong Province, and Hainan Province—through new establishment or mergers and acquisitions, thereby further expanding the geographic scope for the establishment of foreign-funded hospitals.

Therefore, policies governing wholly foreign-owned hospitals will become increasingly lenient in the future, further promoting the development of high-end foreign-funded medical institutions.

(2) Relaxing Market Access Conditions for Private Capital

The state has consistently provided strong support for privately run healthcare institutions, and restrictions on private capital entering the medical sector have been progressively relaxed.

The “Several Opinions on Accelerating the Development of Socially Run Medical Institutions,” issued in January 2014, explicitly stipulates that non-public medical institutions possessing the requisite qualifications shall be approved in accordance with regulations, with expedited processing of approval procedures, streamlined approval processes, and enhanced approval efficiency.

In May 2017, the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services,” which provided specific guidelines for opening medical service institutions to social capital in areas such as market access, approval services, investment cooperation, and opening-up. The policy supports privately run medical institutions in introducing strategic investors and partners, and attracts overseas investors to establish high-level medical institutions in China through joint ventures and cooperation.

High-End Healthcare Is Poised for an Investment Surge

Data source: Guangzheng Hengsheng; chart by VCBeat · VBInsight

High-end medical institutions, given their premium service positioning and higher fee structures, have no need to participate in the national health insurance network. As disposable incomes rise and the high-income population continues to expand, growing health awareness among this demographic is driving increasingly robust demand for premium healthcare services.

However, the limited availability of premium wards in public hospitals and the extreme difficulty in securing appointments with top specialists have created opportunities for the development of high-end healthcare. In particular, specialized fields with relatively lower policy and technical barriers—such as dentistry, obstetrics and gynecology, and ophthalmology—are able to gain recognition from the capital market more readily, becoming the primary investment targets in the early stages.

From a medium-term perspective, the continued growth of the high-income population will further drive the development of premium healthcare. Geographically, this expansion will gradually extend from first-tier megacities such as Beijing, Shanghai, Guangzhou, and Shenzhen to second-tier cities, thereby broadening its coverage. Specialties will evolve from early-stage areas with lower entry barriers to those requiring higher technical expertise, with premium clinics and premium hospitals developing in parallel.

For example, United Family Healthcare has begun establishing a presence in select cities such as Beijing, Shanghai, and Tianjin, with plans to gradually expand into Wuhan, Chengdu, Chongqing, and other urban centers. In addition to general hospitals, the group will establish more specialized medical institutions in high-tech fields, including oncology hospitals and rehabilitation hospitals, to serve a broader segment of China’s high-income population.

As one of the largest foreign-funded medical institutions in Shanghai, Parkway Healthcare has a network spanning downtown Shanghai, Pudong, Hongqiao, and Xintiandi, with service outlets including Shanghai Huixing Jinpu Outpatient Department, Shanghai Parkway Huaying Outpatient Department, and Shanghai Ruixiang Outpatient Department.

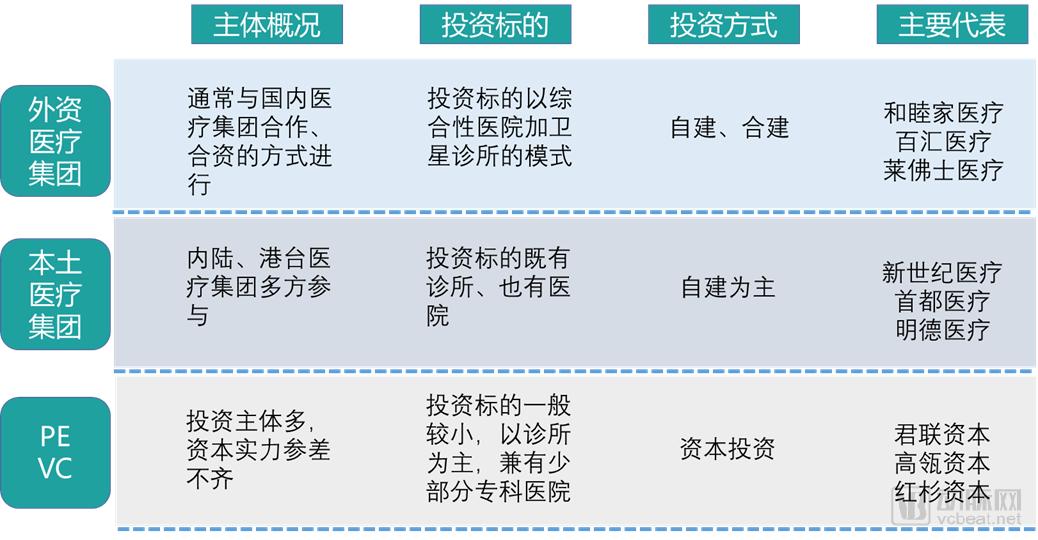

# Major Investors in High-End Healthcare

Image source: VCBeat · Eggshell Research Institute

Currently, the main investors in China's high-end medical institutions include foreign medical groups, domestic medical groups, and PE/VC firms.

Foreign medical groups have entered the market through joint ventures and collaborations with local medical institutions, primarily adopting a layout model of general hospitals supplemented by satellite clinics. For instance, United International Healthcare Group partnered with Fosun Medical Group to expand the presence of United Family Hospitals and clinics across major Chinese cities, while Parkway Pantai has established a network of high-end clinics in China through its acquisition of Shanghai Ruixin Medical Group.

Domestic healthcare investment groups have primarily entered the high-end medical market through self-built facilities, such as New Century Healthcare’s establishment of Beijing New Century Children’s Hospital and Beijing New Century Women’s and Children’s Hospital, Capital Medical’s development of Beijing Aiyuhua Women’s and Children’s Hospital, and Mindray Medical’s creation of Beijing United Family Hospital.

Private equity (PE) and venture capital (VC) firms have primarily targeted clinics for investment, with notable examples including Legend Capital, Sequoia China, and FenXiang Investment. For instance, Legend Capital invested in Usmile Dental and Happy Dentistry; Sequoia China invested in Zhibei Pediatrics; and FenXiang Investment invested in Mommy Knows. VCBeat has collected and organized information on various investors in the high-end healthcare market in recent years (see the table below for details).

Overview of Investment Entities in the High-End Healthcare Market

Data Source: VCBeat Database

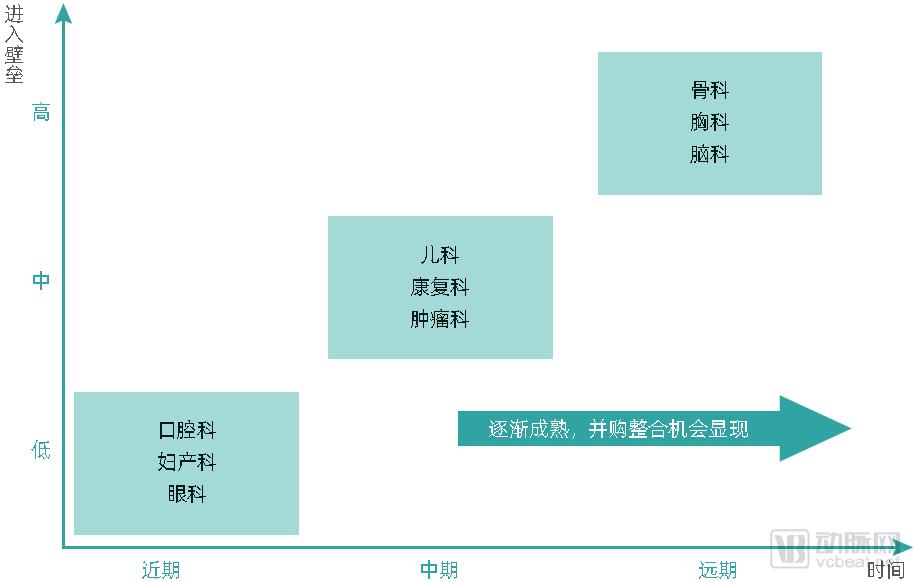

Capital is profit-driven and selects high-quality sectors for investment based on internal and external environments. Fields such as dentistry, obstetrics and gynecology, and ophthalmology have recently become hotspots in the capital market due to their low technical and policy barriers and controllable risks. In contrast, public hospitals have shown limited willingness to develop pediatrics and rehabilitation medicine due to factors such as minimal medication use, fewer diagnostic tests, and high clinical complexity. This has created opportunities for differentiated development in high-end healthcare. Given the substantial market demand in these areas, the capital market has begun to increase investment allocations, suggesting they may well become the next wave of investment hotspots.

Dentistry and Obstetrics & Gynecology Emerge as Investment Hotspots; Pediatrics and Rehabilitation Show Promising Futures

Image source: VCBeat · VCBeat chart

China’s commercial health insurance sector has entered a phase of development, driven by consumption upgrades, policy support, and strong investor interest. What are the key pain points and demands of the major players in the premium healthcare market? How is the competitive landscape structured, and how do various stakeholders interact? We will address these questions by systematically analyzing the relevant entities.

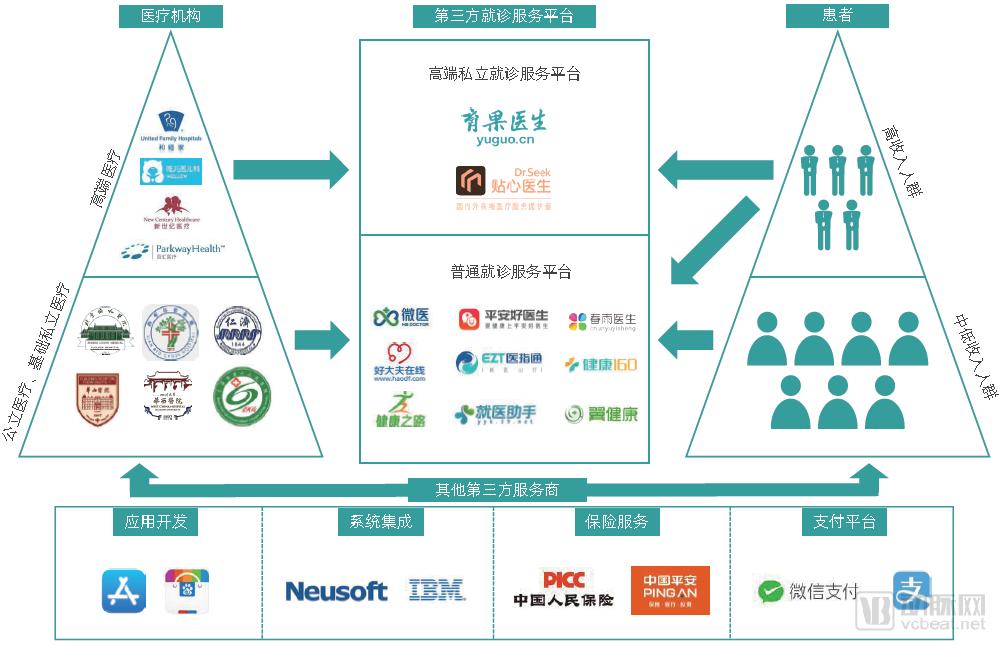

The medical services market primarily comprises healthcare institutions, patients, third-party appointment platforms, and other third-party service providers. It is evident that the overall medical consultation services market exhibits a balance-scale distribution: there is a large number of primary care institutions and a substantial patient population, whereas high-end medical institutions are few in number and serve a smaller patient base.

Healthcare institutions, as providers of medical services, are primarily categorized into two types based on patient positioning:

① Public medical institutions and basic private medical institutions mainly provide basic medical services to low- and middle-income populations;

② High-end medical institutions, which primarily provide premium healthcare services to high-income individuals. As the demand side of medical services, patients choose different levels of care based on their income levels; high-income individuals have a broader range of options and show a stronger preference for premium healthcare services.

Third-party medical consultation service platforms serve as an intermediary bridge connecting the supply and demand sides of healthcare services. Based on their market positioning, these platforms are categorized into two main types: premium and standard. There is a larger number of platforms focused on basic medical services, such as WeDoctor, Haodf Online, and Ping An Good Doctor.

However, there are currently few platforms dedicated to high-end medical services, with Yiguo Doctor and Tiexin Doctor being representative examples. Other third-party service providers mainly offer ancillary services aimed at facilitating disease treatment, including software services, information services, insurance services, and payment services.

The Market Landscape of Medical Consultation Services Exhibits a Libral Distribution Pattern

Image source: VCBeat · VBInsight

As a vital component of the healthcare services market, high-end medical care exhibits distinct characteristics among its supply side, demand side, and third-party consultation platforms.

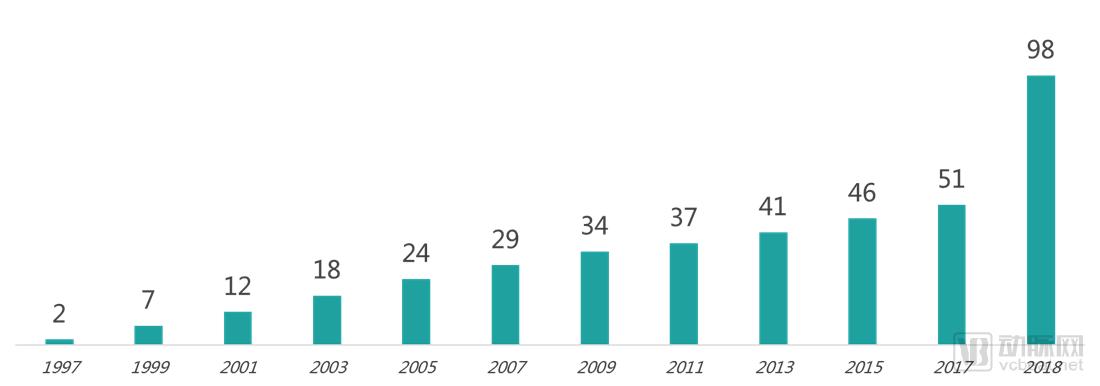

(1) Increase in the Number of Brands and Diversified Development of Institutions

High-end healthcare in China has entered a phase of development, with an increasing number of medical brands. The number of brands has grown from two in 1997 to 98 in 2018, including well-known international brands such as United Family Healthcare, Parkway Pantai, and Raffles Medical, as well as prominent domestic brands like New Century Healthcare and Shengbao Medical. The rise in the number of brands indicates that more enterprises are entering the high-end healthcare market, which will help accelerate market growth and expand the scale of medical service supply.

In 2018, China had nearly 100 high-end medical brands.

Source: Bain & Company; compiled by VCBeat

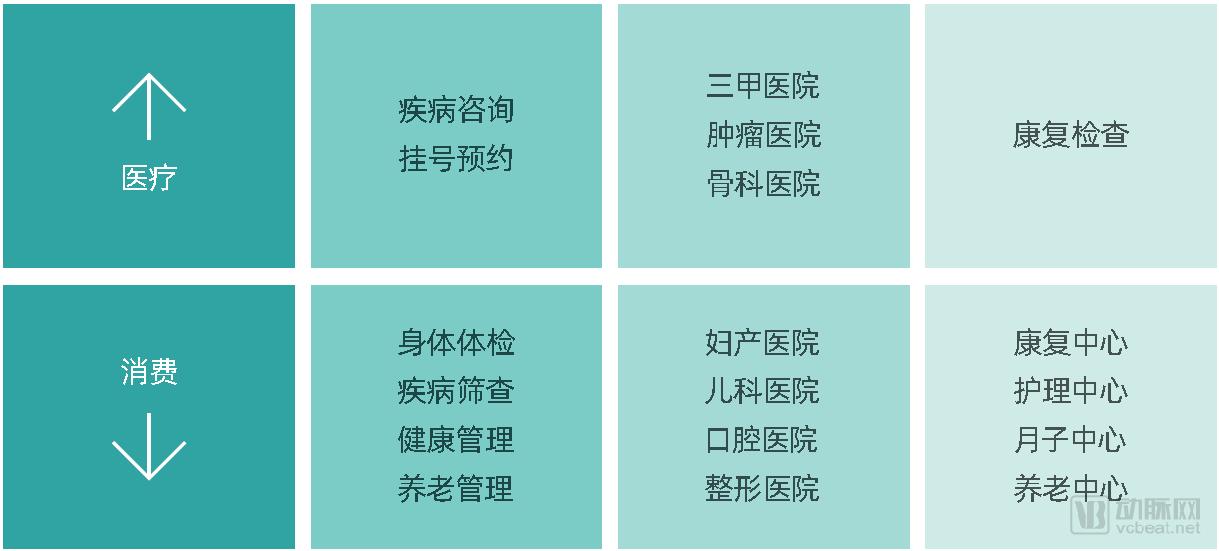

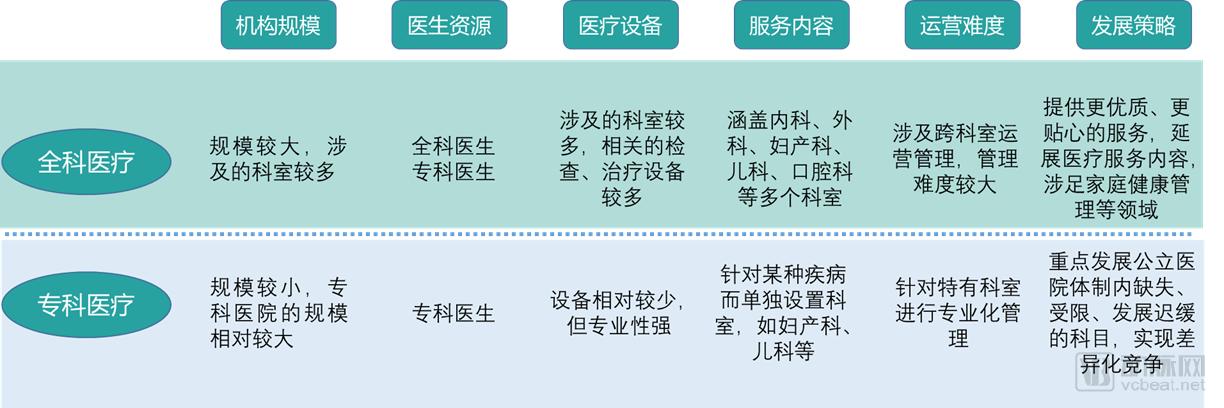

High-end healthcare primarily comprises two major categories: general practice and specialized care. General practice includes general hospitals and general clinics, while specialized care encompasses specialized hospitals and specialized clinics. General practice operations are typically larger in scale and involve a wider range of departments, usually covering internal medicine, surgery, obstetrics and gynecology, pediatrics, dentistry, and other service areas. In contrast, specialized care focuses on providing professional diagnosis and treatment services for specific types of diseases, such as maternity hospitals and pediatric clinics.

Key Differences Between General Practice and Specialist Care

Data source: Public information

General Practice and Specialty Care Differ Significantly in Institutional Scale, Physician Resources, Service Offerings, and Development Strategies

Specialized medical care primarily involves expert services across various fields, with more professional medical equipment and services. It can achieve differentiated competition by focusing on developing areas that are lacking or restricted in public healthcare.

Distribution Map of High-End Medical Institution Types

Image source: Chart by VCBeat·VCBeat

General hospitals are primarily represented by United Family Healthcare, which has established multiple facilities in Beijing, Shanghai, Tianjin, Qingdao, and other cities. General practice clinics are mainly represented by Beijing Hong Kong International Medical Clinic and Raffles Medical, with a primary presence in the three major cities of Beijing, Shanghai, and Guangzhou, providing general practice medical services. There are numerous specialized hospital brands, predominantly focused on obstetrics, gynecology, and pediatrics, with New Century Healthcare and Amcare USA as representative examples.

(2) Prominent specialization and personalization, with high-quality services covering the entire process

Premium Medical Services Covering All Aspects

Image source: Chart by VCBeat

Unlike conventional healthcare, premium healthcare places special emphasis on professional, patient-centered, and customized services to meet the medical needs of high-income individuals.

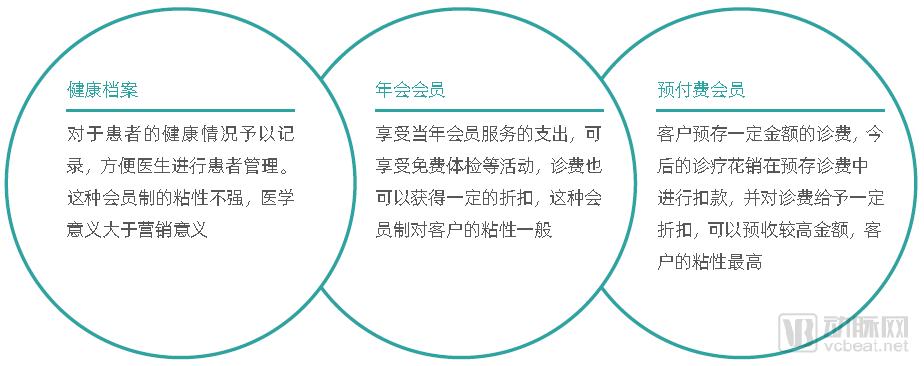

Consultation Session

Premium healthcare services provide one-on-one consultations with professionals, who conduct detailed inquiries into patients’ physical conditions and medical histories, establish individual patient records, and offer membership-based services.

Currently, there are three main types: health record-based, annual membership, and prepaid membership. Due to the highest customer stickiness, prepaid membership has become the primary membership type for high-end medical institutions, such as New Century Healthcare’s Panda Card and Ai Yuhua Women and Children’s Hospital’s Dolphin Card.

Major Types of Membership Systems

Image source: Chart by VCBeat·VCBeat

Appointment Registration Process

Premium healthcare institutions not only provide online appointment registration services at this stage but also arrange consultations with specialists in relevant fields based on patients’ conditions. Customer service representatives coordinate schedules with patients in advance, allowing patients to proceed directly to the specialist’s clinic at the appointed time, thereby eliminating the hassle of waiting in line.

The standard hospital appointment process involves detailed communication with the patient, followed by relaying the relevant information to the back-end system. The back-end then schedules an appropriate specialist based on the patient’s condition and confirms the appointment time with the patient. Upon arrival for the visit, offline nurses provide triage and guidance services.

For medical platforms represented by Yiguo Doctor, there is an additional preliminary comprehensive comparison step. Based on the patient’s condition, location, schedule, budget, and insurance coverage, these platforms provide tailored recommendations for the most suitable hospitals and specialists, thereby enhancing the patient experience while reducing costs and saving time.

Diagnosis Phase

Disease diagnosis is a critical component of medical care, with the professionalism and accuracy of the diagnosis directly influencing the formulation of treatment plans. To enhance diagnostic accuracy and mitigate the risk of misdiagnosis for major diseases, premium healthcare institutions often arrange multidisciplinary consultations involving multiple specialists in relevant fields, and may even facilitate second opinions from authoritative international experts.

Examination Process

High-end medical institutions are equipped with the most advanced imported diagnostic and testing devices, feature specialized laboratories staffed by professional laboratory technicians, and provide tailored examination protocols for different patient populations. Throughout the entire examination process, professional nurses provide full-process accompaniment, offering guidance to patients and assisting them in obtaining their test results.

Some hospitals have launched breast examination and cervical cancer screening programs targeting common female diseases, providing comprehensive and accurate detection of gynecological threats such as breast cancer and cervical cancer to facilitate early diagnosis and reduce disease incidence.

Treatment Phase

Physicians will determine the appropriate treatment plan based on examination results. For common conditions, treatment is provided through prescribed medications; for severe cases, hospitalization will be arranged. High-end medical institutions prioritize the advancement and intelligence of therapeutic equipment to enhance treatment efficacy and alleviate patient suffering.

For instance, Beijing United Family Hospital introduced the da Vinci Surgical Robot, manufactured by the U.S.-based Intuitive Surgical, in 2015. It has been widely applied in general surgery, urology, cardiovascular surgery, thoracic surgery, gynecology, head and neck surgery, and pediatric surgery, thereby improving surgical outcomes and reducing surgical risks.

Payment Process

The healthcare payment process is closely intertwined with high-end medical insurance. High-end medical services and high-end medical insurance complement each other: high-end medical services (provided by private hospitals, international departments, and international clinics) stimulate the market for high-end medical insurance, while high-end medical insurance drives patient traffic to high-end medical institutions, thereby expanding their customer base.

Moreover, several relatively mature companies in the high-end medical insurance market, such as the well-known BUPA, Cigna & CMB, MSH, AXA, and GBG, have established partnerships with numerous healthcare providers. These arrangements enable policyholders to receive “cashless” treatment at network hospitals—simply signing off before leaving—with subsequent settlement of expenses handled directly between the hospitals and the insurers.

Quality medical services deliver a superior customer experience for this type of insurance, while the safety net provided by coverage alleviates patients’ concerns about seeking care at private hospitals. High-end medical insurance offers four major benefits to premium healthcare institutions:

First, customer referral. High-end clinics charge high fees and have relatively low patient traffic, while insurance companies maintain their own directories of recommended healthcare providers. By integrating with commercial health insurance, high-end medical institutions can gain access to referred customers.

Second, it facilitates medical access for patients. When choosing direct-billing medical institutions, policyholders are not required to make cash payments; instead, patients simply swipe their insurance cards, and the insurer settles directly with the medical provider. Patients only need to verify the bill. This offers considerable convenience to customers, eliminating out-of-pocket payments and the hassle of navigating complex reimbursement procedures.

Third, trust endorsement. Like public health insurance, commercial health insurance serves to enhance trust. If high-end medical institutions are endorsed by insurance companies, patients will perceive these clinics as more standardized, thereby increasing their sense of trust.

Fourth, enhance quality. Commercial insurance clients are typically high-income individuals who generally have higher expectations for medical services and technology, thereby providing reverse incentives for clinics to continuously improve their service standards.

Compared with social insurance, commercial health insurance covers a broader range of diseases and also includes non-disease-related services such as health check-ups and medical assessments. It offers higher reimbursement rates, with 95% of commercial insurance products providing up to 100% coverage. Moreover, reimbursement is not limited to mainland China but also extends to medical institutions in Hong Kong, Macao, Taiwan, and selected countries in Europe and the United States.

Commercial insurance offers broad coverage, high reimbursement rates, and strong convenience.

Image source: VCBeat·VCBeat

As the primary suppliers, high-end medical institutions are becoming increasingly numerous and diverse in type. To ensure the quality of medical services, most physicians are specialists recruited from large tertiary Grade A hospitals, medical equipment consists of the most advanced imported devices, and strict operational protocols are enforced at every stage of care. In terms of payment, high-end medical insurance services have been introduced, offering broad disease coverage, extensive geographic reach, high reimbursement rates, and greater convenience.

High-income individuals’ demand for medical services has transcended mere disease treatment. They seek convenient access to care, comfortable medical environments, personalized diagnosis and treatment, comprehensive disease screening, long-term health management, end-to-end overseas medical accompaniment, and rapid commercial insurance payment processing. They are willing to pay a premium for superior medical services.

However, the existing healthcare system is primarily oriented toward disease treatment. Issues such as the difficulty in securing appointments with specialists and for premium services, brief consultation times, poor effectiveness of disease screening, overcrowded hospital environments, substandard service attitudes among medical staff, and the inability to provide long-term health management services have become significant pain points for high-income individuals seeking medical care.

High-end healthcare precisely addresses the shortcomings of public healthcare by developing personalized disease treatment and health management plans based on patient needs, thereby effectively resolving the medical access pain points faced by high-income individuals.

Unmet Healthcare Service Needs Among High-Income Populations

Image source: Chart by VCBeat

Green Channel

Currently, seeking medical care at hospitals involves time-consuming processes such as queuing for registration, scheduling appointments with doctors, and waiting for consultations, with no guarantee of securing an appointment with a preferred specialist. Premium healthcare services offer an end-to-end solution covering registration, appointment scheduling, and consultation. Patients simply need to specify their requirements, and the hospital will arrange the physician’s availability accordingly, allowing patients to receive care directly at the scheduled time.

One-on-One Service

Public hospitals are overcrowded, with each physician consulting dozens of patients daily. The high patient volume results in shortened consultation times, thereby compromising the quality of care. In contrast, premium healthcare offers one-on-one services, where each physician dedicates specific time slots exclusively to individual patients. This model ensures ample time for doctor-patient communication, enabling meticulous and comprehensive diagnosis and treatment.

Comfortable Environment

Public hospitals face bed shortages, with multiple patients sharing rooms and common living facilities. In contrast, high-end private hospitals offer private rooms with refined decor and comprehensive amenities, providing patients with personal space and a quiet environment conducive to recovery.

Disease Screening

High-end medical services can provide patients with comprehensive health checkups and disease screenings, particularly cancer screenings, to detect potential health risks early and reduce the likelihood of major diseases.

Health Management

Public healthcare focuses primarily on the consultation phase, with an emphasis on disease treatment, while offering little to no services for pre-consultation prevention or post-consultation management. In contrast, premium healthcare provides patients with comprehensive health management services, including guidance on diet, exercise, and rest. It also offers targeted rehabilitation management plans tailored to specific disease types, ensuring long-term protection of patients’ health.

Meanwhile, internet healthcare platforms such as Haodafu and Yuguo Doctor have emerged to provide customer health management services. These platforms integrate services including telephone consultations, video consultations, medical appointment scheduling, and customized health check-ups, offering one-stop health management solutions for individuals across all demographics.

The greatest advantage of healthcare platforms launching health management services is their ability to transcend medical brand boundaries, delivering the most effective health management solutions through a service matrix that encompasses the entire network, all channels, and all clinical departments.

Commercial Insurance Payment

Social insurance covers a limited range of diseases, reimbursing only a certain percentage of costs within the covered scope after deducting out-of-pocket expenses, and the reimbursement process is cumbersome. In contrast, commercial high-end medical insurance offers broader coverage and provides personalized insurance products for prenatal checkups, childbirth, dental care, and ophthalmology. Regarding reimbursement limits, most plans cover 100% of eligible expenses and support direct billing.

Overseas Medical Treatment

High-end medical services also provide overseas medical treatment assistance. For patients seeking medical care abroad, these services include hospital selection, physician appointment scheduling, passport processing, and medical accompaniment, ensuring that patients receive high-quality medical care while their personal safety is safeguarded.

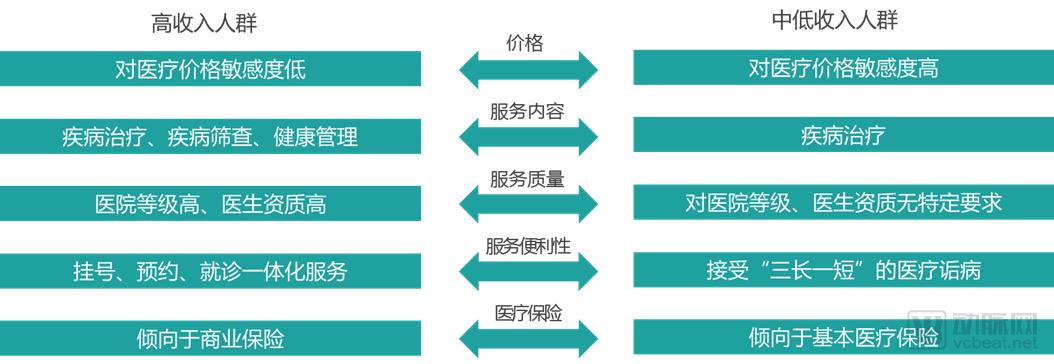

Meanwhile, high-income individuals possess strong purchasing power and have higher expectations regarding the content, quality, and convenience of medical services. They also tend to purchase commercial health insurance with broader coverage and higher reimbursement rates.

In contrast, low- and middle-income individuals, constrained by limited financial resources, exhibit high price sensitivity toward medical services. Their primary need is disease treatment, with a strong preference for higher reimbursement rates under basic medical insurance, while placing no particular emphasis on service quality or convenience. Thus, high-income groups are quality-oriented, and premium healthcare services align well with their medical demands.

Differences in Healthcare Services Between High-Income and Middle-to-Low-Income Populations

Image source: Chart by VCBeat

(1) Pain Points of Key Market Participants

The main participants in the high-end healthcare market include the government, medical institutions, physicians, and patients.

Government: Primarily on the basis of meeting the public’s basic healthcare needs, encourage the development of high-end medical institutions to satisfy the diversified healthcare service demands of high-income groups, and provide policy support.

Healthcare Institutions: High-end medical patients are primarily from high-income groups, who face significant challenges in accessing preference information regarding medical services, healthcare institutions, and physician selection. Purely offline marketing efforts have limited reach among this demographic, resulting in low brand penetration; therefore, third-party platforms are required to enhance promotional efficiency and expand brand coverage. Additionally, integration with commercial health insurance is necessary to address the payment of medical expenses for high-income individuals.

Doctor: Hoping to achieve higher income and improve personal financial conditions. Hoping to attract patients commensurate with one's professional expertise, thereby better demonstrating medical service capabilities.

Patient: There are numerous high-end medical brands, with various institutions actively promoting their medical services to patients. Due to regulatory differences between public and private healthcare sectors, private providers are permitted to set their own prices, resulting in significant price disparities in the high-end medical market and making it difficult for patients to differentiate among options. Moreover, there is a lack of independent third-party evaluation platforms for assessing the effectiveness of medical services; the objectivity and impartiality of existing assessments are often questioned, leaving patients without reliable references for decision-making.

Needs of Key Stakeholders in High-End Healthcare

Image source: VCBeat · Eggshell Institute

(2) Third-Party Medical Consultation Service Platforms Address Market Pain Points

To address the pain points of key stakeholders in the high-end healthcare sector, an independent third-party medical consultation service platform is needed as an intermediary to connect patients, healthcare institutions, and insurance providers, thereby reducing information asymmetry and improving the operational efficiency of the high-end healthcare market.

Core Features of the Premium Medical Consultation Service Platform

Image source: VCBeat · VBInsight

The core functionalities of the healthcare consultation service platform are primarily categorized into two groups: basic functions and extended functions. The basic functions mainly address the information asymmetry between medical institutions and patients, helping patients transcend the boundaries of medical departments and brands to identify the optimal medical institutions and physicians across all online platforms and channels.

Extended functions primarily address the personalization of medical services by providing personalized healthcare, insurance, and other value-added services tailored to patients’ individual needs, thereby delivering a high-quality medical experience.

First, address information asymmetry. Provide service information from major medical institutions and conduct comprehensive online comparisons, including areas of expertise, key departments, renowned physicians, service pricing, and patient satisfaction ratings. This enables patients to select medical institutions and schedule appointments based on their specific conditions, thereby reducing the randomness in healthcare decision-making.

For example, the same doctor may have different consultation schedules and fees at different practice locations. For patients, collecting and comparing such information across hospitals incurs prohibitively high costs. In this regard, healthcare platforms can help users address these challenges by quickly identifying doctors who offer suitable appointment times, are located closer, charge lower fees, and better match individual needs.

Second, addressing the personalization of medical services. High-income individuals have increasingly higher demands for the quality of medical care. By offering value-added medical services beyond core clinical care—such as overseas medical treatment and multidisciplinary team (MDT) consultations—the accuracy of disease diagnosis can be improved.

For high-income individuals who are accustomed to seeking diagnosis and treatment at private hospitals, follow-up insurance and other value-added services represent one of the personalized offerings that the platform can provide.

Furthermore, the healthcare service demands of high-income individuals extend beyond disease treatment to include disease prevention and health wellness. They also seek comprehensive, family-oriented health management plans achieved through integrated services. Platforms can meet these needs by offering holistic service packages, such as health management consultations.

Third, address institutional brand promotion. Provide an information display platform for medical institutions to assist in brand promotion, thereby enhancing brand satisfaction and improving user reach efficiency.

Promotional campaigns for high-end medical institutions also target high-spending consumers. However, due to the unique nature of the healthcare industry, widespread, standardized mass marketing is not feasible. In this context, the professional media attributes of healthcare platforms and the collective attributes of medical institution groups play a significant role.

(3) Operational Mechanisms of Third-Party Medical Consultation Service Platforms

Acquiring resources from medical institutions, doctors, and patients is the foundation for the development of healthcare consultation service platforms.

Image source: VCBeat · VCBeat chart

Third-party healthcare service platforms act as intermediaries between medical institutions and patients. On one hand, they provide medical institutions with information display and patient referral services; on the other hand, they offer patients online consultations, appointment scheduling, online payments, and medical discounts, thereby enhancing the overall patient experience.

Therefore, the key to the platform’s operation lies in simultaneously securing hospital appointment slots and patient resources. By establishing partnerships with both public and private medical institutions, the platform exports relevant information such as departmental structures and physicians’ consultation schedules, enabling comprehensive cross-network and omni-channel matching.

Patients can select departments and physicians based on their individual needs to make online appointments. Healthcare institutions and physicians can gain patient traffic through the platform. Meanwhile, the platform can also recommend the most suitable hospitals and physicians according to patients’ needs—taking into account multiple factors such as professionalism, distance, availability, and cost—to help patients make optimal choices.

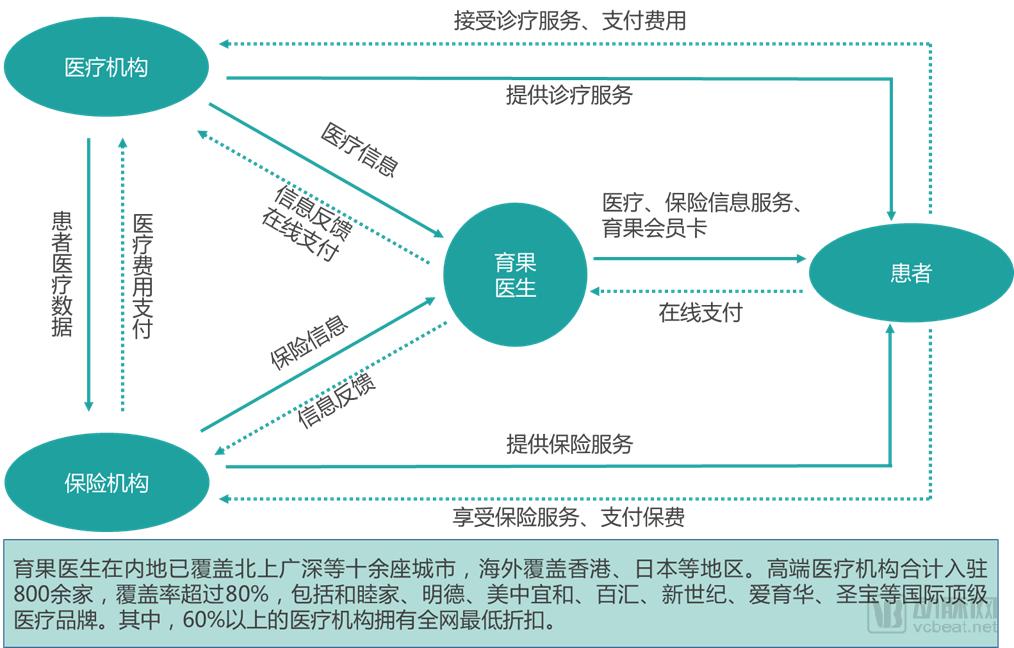

Moreover, patients can access additional services through the platform, such as disease prevention, health management, and commercial insurance integration. This not only enhances the convenience of seeking medical care but also provides more comprehensive medical services, making patients more willing to use platform-based products. For instance, Yiguo Doctor, a brand under Meituan-Dianping dedicated to the high-end private healthcare sector, effectively integrates multi-party resources to enable users to enjoy premium medical services at minimal cost.

Yuguo Doctor integrates third-party resources to create the Meituan-Dianping of the high-end healthcare sector.

Data source: Yiguo Doctor; Chart by VCBeat

Yuguo provides C-end patients with information on medical institutions and doctor-related services, enabling comprehensive cross-hospital and cross-brand comparisons of experts across the entire network.

By booking appointments with partner medical institutions through Yugu, cash-paying patients can enjoy the lowest outpatient and inpatient discounts available online during the same period. Insurance users can link their insurance plans with a single click before making an appointment to view reimbursement rates. Additionally, leveraging Yugu’s nationwide expert recommendation feature, they can comprehensively select the most suitable medical institution and physician based on factors such as greater specialization in the required treatment area, higher reimbursement rates, closer proximity, and more convenient scheduling.

In addition to routine consultations, purchasing medical packages such as health check-ups, prenatal examinations, and childbirth services through the platform entitles users to discounted rates. Furthermore, Yugu Doctor connects B-side medical institutions with C-side patients by providing healthcare providers with data on patient appointment and registration demands, disease-related inquiries, and satisfaction evaluations of medical services.

Conversely, B-side medical institutions provide Yugu Doctor with service-related information such as departments, physicians, consultation schedules, and discounts, using Yugu as the service entry point; B-side insurance institutions provide Yugu Doctor with relevant information on insurance products, direct-billing hospitals, and premiums.

As a connectivity platform, Yuguo facilitates B2B and B2C integration by providing insurance solution consultations, displaying claims information from insurance-linked hospitals, and enabling users to bind their insurance policies for one-stop access.

The above constitutes part of the report. The report also provides a detailed data-driven analysis of patient sources, healthcare preferences, departmental configurations, and consultation fee structures for high-end medical services. Below is the overall structure of the report:

I. Industry Insights: Market Positioning Determines the Development Path

1. Target the high-income demographic as the primary market

2. Personalization, convenience, and depth have become the main characteristics of the development path

3. Private sector as the primary provider, public sector as supplementary

4. Entering the Development Phase: Parallel Growth of International and Domestic Brands

II. Macro Environment: Consumption Upgrading, Policy Support, and Capital Favoritism as Key Drivers

1. Rising income levels have led to increasingly high demands for the quality of medical services among high-income groups

2. Policy Liberalization Has Driven the Development of High-End Healthcare

3. Capital Markets Provide Financial Support for the Development of High-End Healthcare

III. Market Landscape: The medical consultation services market exhibits a balanced distribution, with high-end healthcare and primary care advancing in tandem.

1. Supply Side: Diversified Development of Institutions, with High-Quality Services Covering the Entire Medical Process

2. Demand Side: Unmet Needs for Medical Services, with High-Quality Care Becoming the Core Demand

3. Third-party medical consultation service platforms: Building an intermediary bridge to enhance institutional operational efficiency and improve patients’ healthcare experience

IV. Data Insights: Beijing, Shanghai, Guangzhou, and the Jiangsu-Zhejiang Region Emerge as Hubs for High-End Medical Demand, with Dentistry and Pediatrics Becoming Popular Specialties

1. Medical Expenses—Healthcare accounts for 16% of wealth distribution among high-income individuals

2. Patient Sources – Large population base in Beijing, Shanghai, Guangzhou, and the Jiangsu-Zhejiang region; high acceptance rates among professionals in the finance and IT sectors

3. Healthcare Preferences—Chinese-funded high-end medical brands are gaining increasing trust, with medical facilities and physician qualifications becoming the primary factors in healthcare choices

4. Department Setup—Stomatology and Pediatrics are the most prevalent, with Pediatrics holding the largest market size

5. Physician Credentials – Rigorous Selection; 38.2% of Physicians Have 30 or More Years of Clinical Experience

6. Consultation Fee Structure – 50% of institutions charge over RMB 800, with foreign-funded institutions charging more than Chinese-funded ones

7. Number of Patient Visits—Beijing Has the Highest Number of Patient Visits Among High-End Medical Institutions

V. Future Trends: The Influx of New Patients Brings Dividends, with Health Management and Medical Tourism Emerging as Key Growth Areas

1. High-End Private Healthcare Reaps the Dividends of Patient Growth, with Market Size Continuously Expanding

2. Family Health Management Will Become a Key Service Focus in the Future of High-End Healthcare

3. Deep Integration of High-End Healthcare and Insurance

Long-press to recognize the mini-program below and get the full version of “Report on the Development of the High-End Medical Market in the Context of Consumption Upgrading” for free.

Report Description:

High-Income Population: Refers to individuals with an annual income of RMB 500,000 or more, or total assets of RMB 10 million or more.