"4+7" Policy’s Impact on Pharmacies Is Far from Trivial!

From the issuance of the first prescription for a drug selected under the “4+7” centralized volume-based procurement program in Xiamen on March 18 to the official launch in Guangzhou, the last pilot city, on April 1, nearly three months have passed since the implementation of the “4+7” pilot program.

Based on the results of the first batch of the "4+7" volume-based procurement, 88% of the selected drugs were generic drugs that had passed the consistency evaluation, with an average price reduction of 52%. The patent cliff for originator drugs will compel manufacturers to introduce more innovative medicines. Meanwhile, the implementation of medical insurance payment standards will leverage the market-regulating effect of price differentials to increase the market share of generic drugs.

In the future, the combined policy measures of consistency evaluation, volume-based procurement, and medical insurance payment will profoundly reshape the pharmaceutical industry ecosystem and achieve the goal of controlling medical insurance costs.

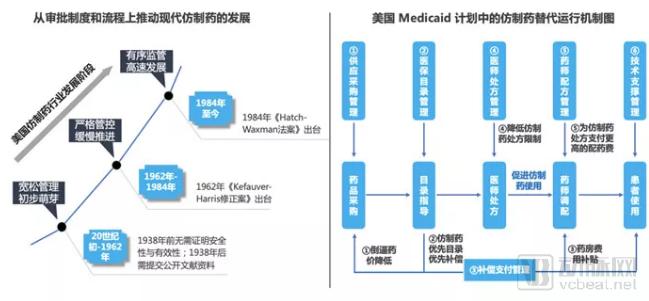

There are already international precedents for healthcare cost containment.

The U.S. Medicaid program regulates the conduct of pharmaceutical manufacturers, healthcare institutions, pharmacies, and patients through various measures, promotes the development of modern generic drugs through approval systems and processes, fully facilitates generic substitution, and achieves the policy objective of reducing pharmaceutical expenditures.

By leveraging health insurance mechanisms to regulate the use of generic drugs, generics in the United States account for nearly 85% of market volume, yet contribute only about 13% of total sales revenue, with the remaining share dominated by high-priced innovative originator drugs. Consequently, the prescription of generic drugs significantly reduces healthcare expenditures, saving the U.S. more than $300 billion annually in drug spending.

The “4+7” volume-based procurement policy was officially implemented in April this year, leading to drastic changes in the market landscape for the first batch of 25 drug varieties. As the number of drugs that have passed the consistency evaluation continues to rise, more varieties are likely to be included in the scope of volume-based procurement. By analyzing the market shifts observed in the first batch, we can make accurate predictions about future market expectations.

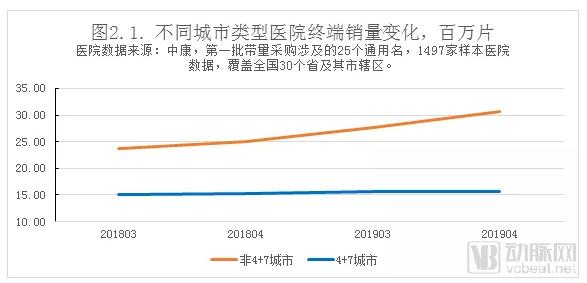

According to data from Sinohealth, the total sales volume of the 25 generic drugs included in the first batch of volume-based procurement increased significantly in non-“4+7” cities, but showed no significant growth in “4+7” cities (Figure 2.1). It is an undisputed fact that sales growth in “4+7” cities has been sluggish, while sales growth in non-“4+7” cities has been robust.

Upon careful consideration, the causes underlying the aforementioned phenomena are in fact not complex.

In the hospital markets of the "4+7" cities, products included in the volume-based procurement program may be substituted by alternatives; consequently, their sales growth is significantly lower than that in non-"4+7" cities, and the overall market size for these products in "4+7" city hospitals is likely to further shrink in the future.

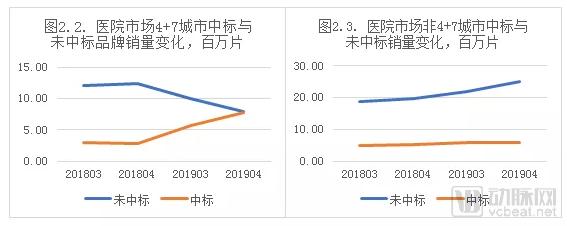

In the hospital markets of the "4+7" pilot cities, the volume-based procurement (VBP) products demonstrated a significant effect in terms of winning brands replacing non-winning brands; the sales growth of winning brands basically offset the sales decline of non-winning brands (Figure 2.2). However, in the non-"4+7" hospital markets, the total sales volume of non-winning brands increased significantly, while that of winning brands showed no substantial growth (Figure 2.3);

Currently, the incremental growth in total hospital sales for products included in volume-based procurement (VBP) is driven by the expansion of non-winning brands in cities outside the “4+7” pilot program, whereas the growth of winning brands merely represents a shift within the existing market.

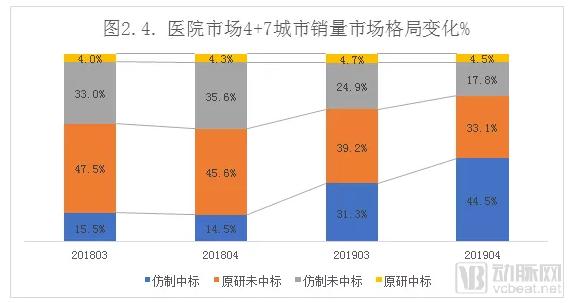

The overall sales volume share of winning generic brands increased from 14.5% in April 2018 to 44.5% in April 2019, while that of non-winning originator brands decreased from 45.6% to 33.1% over the same period, and that of non-winning generic brands declined from 35.6% to 17.8% (Figure 2.4).

It is evident that the market landscape of hospitals in the "4+7" cities is undergoing a dramatic transformation.

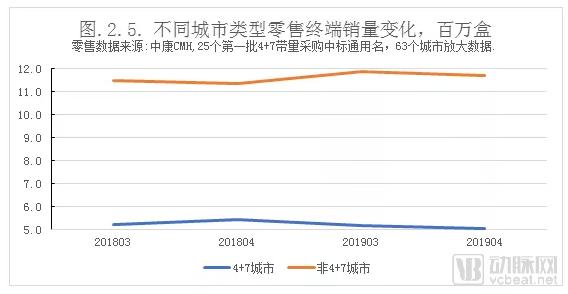

From the perspective of the retail market, there has been no significant growth in the overall sales volume of volume-based procurement (VBP) products. This trend holds true for both the “4+7” pilot cities and non-“4+7” cities, with month-on-month sales even showing a suspected downward trend (Figure 2.5).

Industry insiders believe that the existing hospital market volume has not significantly shifted to the retail sector due to volume-based procurement (VBP); in fact, there may even be a flow back from the retail market to hospitals. Meanwhile, these “4+7” VBP-listed products have likely been substituted with alternative products in the retail channels of the “4+7” pilot cities.

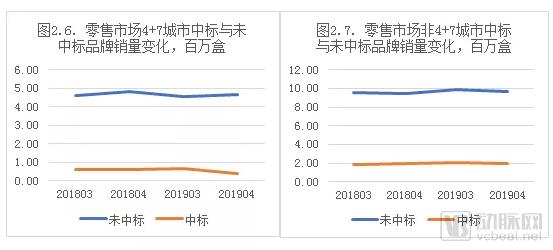

Due to the significant price disparity between hospital and retail channels, some winning brands in the “4+7” city retail market were delisted, resulting in an approximate 42.4% year-on-year decline in sales volume for winning brands in April, while non-winning brands saw a 2.5% decrease (Figure 2.6). In contrast, in non-“4+7” city retail markets, sales volume for winning brands increased by 4.7% year-on-year in April, whereas non-winning brands experienced a 1.5% decline (Figure 2.7).

It is worth noting that among the products included in the volume-based procurement program, only the winning brands have seen a slight growth in retail markets in non-"4+7" cities; the market shift of non-winning brands to the retail channel has not yet been reflected.

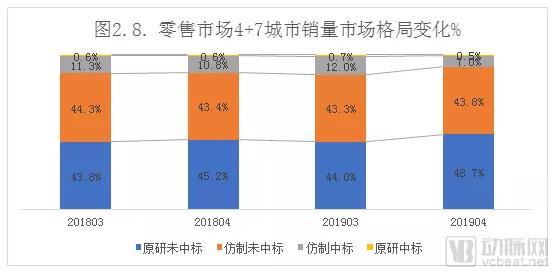

Non-winning originator brands are eroding the sales volume share of winning brands in the retail markets of the “4+7” cities. Currently, changes in the retail market landscape are primarily evident in these “4+7” cities. The overall sales volume share of non-winning originator products increased from 45.2% to 48.7% year-on-year in April, while that of winning generic products decreased from 10.8% to 7.0% over the same period.

Following the implementation of the “4+7” volume-based procurement program, it is expected that a substantial share of high-priced generic drugs will be squeezed out, while the market share of originator drugs also faces erosion and revenue losses due to price reductions.

Generic Drug Manufacturers Face Survival Challenges After Failing to Win Bids.

First, the most significantly affected are pharmaceutical companies whose generic drugs failed to win bids in the centralized procurement. The current impact is primarily reflected in the hospital markets of the “4+7” pilot cities. For example, Shuaitai (clopidogrel) held approximately 10.5% of the clopidogrel market share in hospitals across the “4+7” cities in April 2018, which dropped to 0.4% by April 2019, effectively exiting this market segment and being replaced by Taikai, the winning brand. Such non-winning generic brands, as well as those that have not passed the consistency evaluation, face substantial survival risks. In the short term, they can still operate in non-“4+7” cities and non-procurement markets; however, as the pilot program expands to more cities, their only viable market in the future will be the non-procurement segment.

Furthermore, original brands that failed to win bids in the centralized procurement have also been significantly impacted. This impact is currently most evident in the hospital markets of the “4+7” pilot cities. For instance, Lipitor’s sales volume share in these markets dropped from approximately 64% in April 2018 to 39% in April 2019, being replaced by Ale (Atorvastatin), the winning bid brand. The greatest challenges faced by such brands are channel migration and price maintenance management.

For generic drug manufacturers that won the bid, the primary impact lies in managing market chaos caused by significant price disparities; in some cases, products were forced to be withdrawn from retail channels in the "4+7" pilot cities due to an inability to cover the price difference, resulting in a decline in their retail market share.

Commercial companies, facing significant price reductions, would need to distribute larger volumes if delivery fees remain calculated based on transaction amount. Consequently, these companies are confronted with the challenges of managing high-cost inventory and balancing distribution costs against profit margins.

For pharmacy chains, the current impact is limited to winning brands associated with the “4+7” volume-based procurement program, with minimal effect on the overall product mix of these chains. In the short term, these brands are facing significant pressure from substantial price differentials. Although some manufacturers provide partial backend price subsidies, a considerable gap remains between the subsidized prices and the winning bid prices. Chains are clearing inventory through promotions, delisting certain winning brands, which has damaged their value-oriented brand image. Some patients may return to hospitals or community health centers for medications, leading to an overall decline in profitability. However, in the long run, more pharmaceutical manufacturers, particularly originator companies, will allocate greater resources to the retail channel. Meanwhile, as hospital drug prices continue to decrease, the gross margins for prescription drugs will become increasingly thin.

Following the implementation of volume-based procurement (VBP), hospitals have employed various measures to guide and require physicians to prioritize the use of winning bid generic brands in order to strictly meet procurement volume targets. This has inevitably impacted prescription volumes for originator products. Since originator drugs typically have a larger base of long-term patients, switching these patients to the winning generic brands in the initial phase requires considerable effort in patient communication and entails risks associated with medication changes. Current market feedback and data trends indicate that the rate of medication switching is particularly high in lower-tier hospitals. Physicians in these institutions have limited autonomy in decision-making; consequently, their prescribing habits for chronic disease medications have been significantly affected.

Industrial Response

In the short term, the pharmaceutical industry needs to adjust its resource allocation, channel structure, pricing system, and promotional strategies. Winning brands should focus on supplying hospitals in the "4+7" cities, maintain their presence in non-"4+7" city markets, closely monitor price linkage trends in non-"4+7" cities, assess the risk of product delisting in the retail market, and make strategic choices accordingly. Non-winning generic brands should exit the hospital market in "4+7" cities, downsize their hospital sales teams, consider entering non-standard markets such as the third-terminal retail sector, evaluate return on investment, and potentially adopt the Contract Sales Organization (CSO) model. Non-winning originator brands should prepare for the transfer of existing hospital channel volumes, prioritize layout in non-standard markets such as retail, and temporarily maintain their current pricing system.

In the long run, strategic choices involve either exit, innovation-driven growth, or low-cost leadership. Companies should assess the extent of policy implementation and their own capabilities, particularly in product lines, to decide whether to follow through or exit. If they choose to stay, they must strategically build core competencies driven either by innovation or by low cost, ensuring a continuous pipeline of new products.

Chain Response

In the short term, stabilize customer traffic. Manage inventory of winning bid brands; temporarily delist them if necessary, and adjust the product mix. Stabilize customer flow by strategically introducing non-winning brands, particularly originator drugs, and offset profit losses by promoting categories unaffected by the "4+7" volume-based procurement policy.

In the long term, it is essential to optimize the structural layout of store types and refine product portfolios. Professional pharmacies and Direct-to-Patient (DTP) pharmacies located near hospitals are both prescription-driven; therefore, they must strive to secure more medical insurance resources. However, any utilization of public healthcare resources will be subject to strict regulatory control. The prescription-driven nature also limits the gross margin potential for pharmacy chains, making these outlets primarily significant for strategic positioning and establishing a professional brand image. In contrast, community pharmacies rely more on advertising and sales promotion to drive demand. Their product structures feature a higher proportion of traditional Chinese medicine (TCM) proprietary drugs and general health products, offering relatively higher gross margins. Meanwhile, it is necessary to balance the mix of customer traffic-driving items and profit-generating categories, while exploring differentiated services and value propositions that distinguish them from community hospitals.

The product portfolio continues to expand, affecting nearly 20% of the terminal pharmaceutical market.

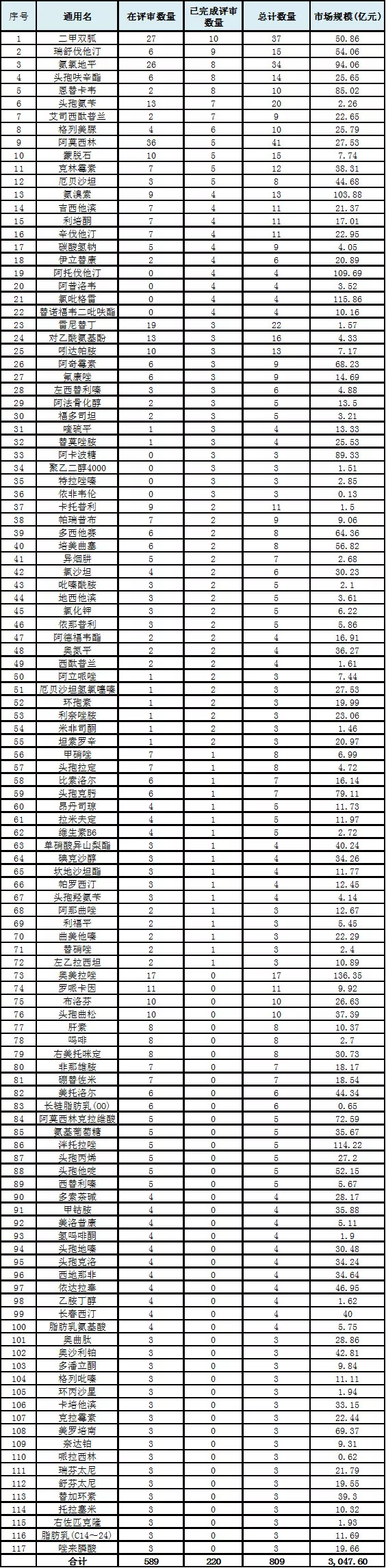

Based on the current policy implementation progress and environmental analysis, the continued expansion of the “4+7” drug varieties is essentially certain. Future candidates for inclusion in volume-based procurement are primarily those with the potential for multiple manufacturers to pass the consistency evaluation. As of June 26, we retrieved 1,137 drug applications for consistency evaluation from the Sinohealth KINGS system. Temporarily excluding drugs deemed equivalent to having passed the consistency evaluation by virtue of being marketed in the United States, Europe, or Japan, there are 117 generic names with three or more cumulative approvals or ongoing reviews (Table 4.1). The total terminal market size for drugs under these generic names amounts to approximately RMB 300 billion, accounting for about 18.4% of the overall market (Sinohealth CMH data, 2018).

Table 4.1. List of Generic Drug Names with More Than Three Approvals or Cumulative Review Passes

Brands that fail to win bids are unable to access the primary healthcare market, leaving the retail sector as their last resort.

Currently, drug revenue from tertiary hospitals still accounts for more than 50% of the entire market. However, with the gradual implementation of tiered diagnosis and treatment, the share of drug revenue in the primary healthcare market has risen significantly, increasing from 17% in 2013 to 19% in 2017. This proportion is expected to continue expanding. Meanwhile, based on the current implementation of the “4+7” volume-based procurement program, the proportion of winning bids in primary healthcare procurement far exceeds that in tertiary hospitals. Products that failed to win bids will have to withdraw from the primary healthcare market, making the retail channel the core competitive arena for these non-winning products in the short term.

With declining foot traffic, retail pharmacies need to return to the essence of value and enhance consumer stickiness through professional services.

Data from Zhongkang’s receipt records indicate that the number of retail orders continued to decline in 2018, while overall retail growth was driven by increases in both average transaction value and average item price. As pilot programs for medical insurance payment pricing are progressively deepened, the profit margins gained from price hikes will gradually diminish. For retail pharmacies, enhancing professional capabilities is imperative. A pressing challenge for retail pharmacies is to determine how to boost consumer stickiness through specialized services, while also strengthening collaboration with upstream brand suppliers and selecting branded medications that enjoy consumer recognition.

The impact of the “4+7” volume-based procurement policy has already become evident across various channels within just a few months of its implementation. As the rollout accelerates, overall market changes are becoming increasingly pronounced. We await further developments with keen interest.