Rock Health: Digital Health Sees $4.2B in H1 2019 Funding, Introduces NLO Metric to Assess Investment Bubble Risks

Rock Health

Digital Health Investment Fund

By the end of the first half of 2019, a total of $4.2 billion had been invested in the digital health sector. Although Rock Health had predicted that investment in digital health would slow down this year, current industry investment data suggest that the sector is poised to set a new record this year.

VCBeat (WeChat ID: vcbeat), citing Rock Health’s latest report, has compiled a summary of investment activities in the digital health sector during the first half of 2019 and analyzed investment trends in this field with a focus on “investment bubble” and “net liquidity oversupply (NLO).”

In the first half of 2019, the growth rate of investment capital in the digital health sector was largely consistent with the growth trend observed since 2011. Despite fluctuations in certain years, the overall funding environment in recent years has remained relatively stable.

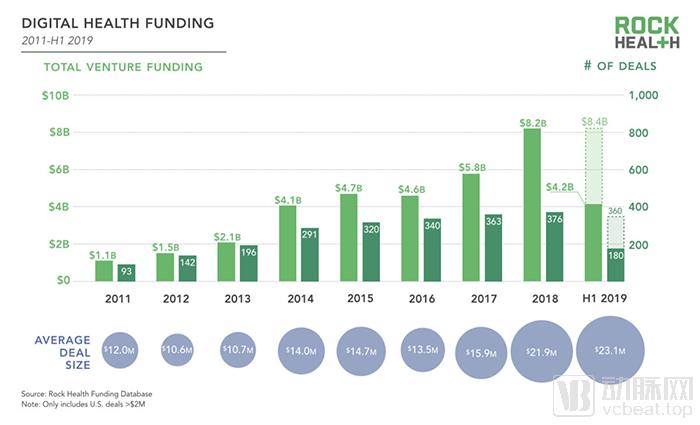

As shown in the figure below, a total of 180 deals were closed in the digital health sector during the first half of 2019, raising $4.2 billion in capital. If this steady growth rate continues, investment in the sector is projected to reach $8.4 billion by the end of 2019, with 360 investment transactions completed. This will surpass the total investment amount of $8.2 billion recorded in 2018.

Annual Total Investment and Transaction Volume from 2011 to the First Half of 2019 (Image Source: Rock Health)

In investment transactions during the first half of 2019, approximately 69% of investors were repeat investors. Furthermore, out of a total of $4.2 billion in invested capital, roughly 30% came from large deals (acquisitions or financings) exceeding $100 million each. Sean Day, a researcher at Rock Health, stated in the report that these few large transactions, each surpassing $100 million, are driving the development of the entire industry.

According to a Rock Health report, the digital health sector has already completed 43 mergers and acquisitions (M&A) this year, making M&A the most common exit strategy for digital health companies. However, if the M&A pace observed in the first half of the year continues, the total number of deals for the full year is projected to decrease by 25% compared to last year, reaching approximately 86 transactions by the end of 2019.

Nevertheless, Rock Health remains relatively optimistic, predicting that more non-healthcare companies will acquire startups in the digital health sector in the future. The report’s researchers wrote: “As an increasing number of non-healthcare companies enter the digital health space, we expect acquirers from other sectors to become more active in the coming years. Furthermore, technology companies and non-healthcare companies have consistently ranked as the second and third most active acquirers in the digital health sector.” Companies within the digital health sector itself rank first in acquisition activity.

With the wave of mergers and acquisitions, a significant number of IPOs have been withdrawn this year. Initial public offerings in the digital health sector are rare; however, five digital health companies—Livongo, Health Catalyst, Change Healthcare, Phreesia, and Peloton—are expected to go public this year, breaking the streak of zero IPOs in this sector since 2016.

In early 2019, Rock Health explored the question: Is digital health in a bubble?

Investment bubbles are a type of economic cycle in which asset prices in a particular sector rise far beyond the actual value of the real economy in that sector. When investors encounter a “bubble,” new investment halts, causing prices to plummet and thereby bursting the bubble. In such scenarios, startup valuations crash dramatically, creating an urgent need for fresh venture capital funding to maintain solvency.

Rock Health has summarized the following six common characteristics of investment bubbles:

Unclear Exit Market

It also analyzed whether the digital healthcare industry is at risk of an investment bubble from these six perspectives. VCBeat has briefly summarized some of the key insights and case studies from the report to examine the investment landscape in this sector.

1. Hype Replaces Core Business

Conclusion: Since 2018, there has been no “bubble” in this regard.

Smart investors are pursuing companies with tangible value. Virta Health, a portfolio company of Rock Health, recently announced the results of a nearly two-year clinical trial, in which 18.8% of patients achieved complete or partial remission of diabetes within two years—a rate far exceeding that seen in conventional care. Based on these impressive clinical outcomes, Virta Health is able to set drug prices commensurate with therapeutic efficacy.

2. High Cash Burn Rate

Conclusion: At this point, 2019 saw some additional “bubble” compared to 2018.

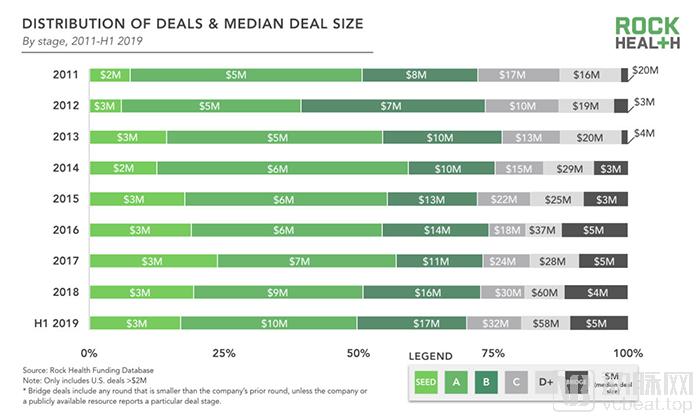

To date, the median Series A financing amount in the digital health industry in 2019 was $10 million, representing an 11% increase from the 2018 median of $9 million and doubling the 2011 Series A median (as shown in the figure below). Series B financing has seen similar growth, with the 2019 median reaching $17 million, 2.1 times the 2011 Series B median.

Median Funding Amounts by Round, 2011–2019 (Image source: Rock Health)

For companies that raised early-stage financing between 2014 and 2016, the average interval between funding rounds was approximately 20 months. Companies with high cash burn rates face a crisis when venture capital levels decline or when they operate in an environment with limited capital access.

3. High Valuations Decoupled from Reality

Conclusion: As in 2018, the “bubble” is not pronounced.

Investors minted three new unicorns in the digital health sector in the first half of 2019: Zipline, Gympass, and Hims. Zipline completed a $190 million financing round in the first half of this year, reaching a valuation of $1.2 billion; Gympass secured $300 million in funding led by SoftBank Vision Fund, with an estimated valuation exceeding $1 billion; Hims raised $100 million at a $1 billion valuation, achieving unicorn status less than a year after its founding in 2017.

4. Cash Surge from New Investors

Conclusion: There will be no "bubble" on this front in 2019.

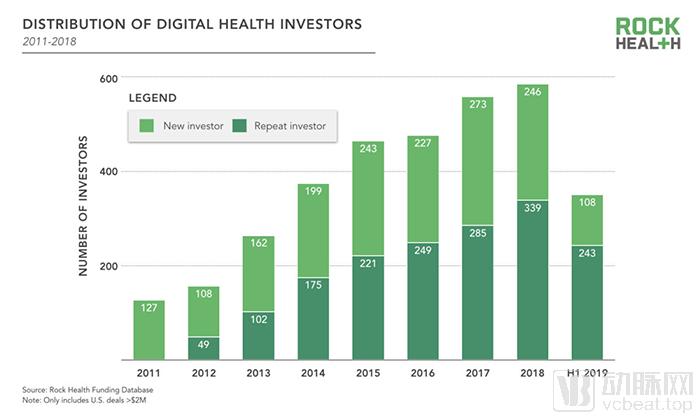

Repeat investors are a hallmark of a mature investment landscape in the digital health sector. Since 2016, repeat investors have outnumbered new investors annually, a trend that has become even more pronounced: among the 351 disclosed investors, 69% had previously invested in a digital health company. (See chart below)

Proportion of New and Existing Investors, 2011–2019 (Image source: Rock Health)

5. Fraud or Misuse of Funds

Conclusion: Less of a "bubble" than in the past; at least, no "bubble" exists at present.

In 2018, only one digital health company was flagged for “fraud and misappropriation of funds.” The company undermined trust between customers and investors by manipulating relevant data.

As of 2019, one company is under investigation by the Federal Bureau of Investigation for alleged improper billing practices; it has suspended two clinical trials and terminated employees.

6. Unclear Exit Market

Conclusion: Although there were IPOs this year, the number of acquisitions was lower than in 2018. In this regard, a small “bubble” will emerge.

Based on the above analysis, Rock Health ultimately concluded that there was essentially no investment bubble in the digital health industry during the first half of 2019.

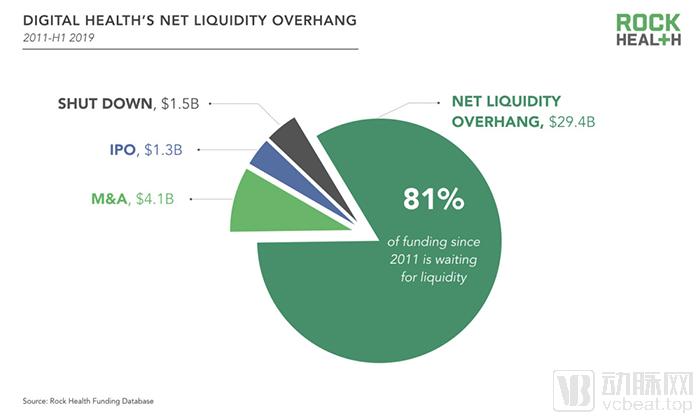

Rock Health has established a formula for Net Liquidity Overhang (NLO), namelyNLO = Total Capital Invested - Divested Investments. This parameter can measure the capital status of the entire digital health sector and explore more questions related to time and returns through NLO.

From 2011 to July 1, 2019, $36.3 billion in capital flowed into 1,274 companies in the digital health sector. During the same period, 170 companies in this sector were acquired, with a total historical financing amount of $4.1 billion; 10 companies went public, excluding the $1.3 billion raised through IPOs; and 5 companies shut down, having raised $1.5 billion on their own.

NLO Share Diagram (Image Source: Rock Health)

Currently, the NLO stands at $29.4 billion ($36.3B - $4.1B - $1.3B - $1.5B = $29.4B), indicating that 81% of assets in this sector remain “waiting on liquidity.” If the five planned IPOs for this year proceed as scheduled, the NLO will reach $31.9 billion by year-end.

Of the five companies planning to go public this year, four have raised an average of $425 million from investors, totaling $1.7 billion in investment (Change Healthcare is excluded as it was formed through a corporate merger and spin-off). According to PitchBook data, the combined valuation of these four companies stands at approximately $6.4 billion. Excluding additional capital raised through the IPOs, this represents a 3.8x multiple on the $1.7 billion in invested capital and accounts for 22% of the current net liquidation value (NLO) of the digital health sector.

In other words, at the current growth rate, companies in the digital healthcare industry will reach a break-even point with a net loss of $29.4 billion within the next four years.

This $3.5 trillion healthcare market represents one of the key pathways for future growth for many large non-healthcare companies, including giants such as Amazon and Google. These companies are high-quality acquirers, willing to pay higher premiums to ensure that digital health companies achieve their financial targets and meet their strategic needs. For example, Amazon acquired the online pharmacy PillPack for as much as $753 million, a price significantly higher than Walmart’s offer. This acquisition also demonstrates Amazon’s ambitions in the digital health sector.

Notably, JPMorgan Chase acquired healthcare payment technology company InstaMed for $500 million to enter the digital health sector. Apple and Google are also entering the digital health market; Google acquired health monitoring developer Senosis Health, and Apple acquired Tueo Health. Apple is leveraging apps and sensors to help parents manage their children’s asthma symptoms.

In summary, the current venture capital landscape for digital health remains robust, showing relatively few signs of an investment bubble. The IPO market is poised for near-term gains, supported by $29.4 billion in active venture capital (NLO). Although mergers and acquisitions (M&A) remain common in the digital health sector, acquisitions by large healthcare and non-healthcare corporations will become a significant source of liquidity and returns for digital health investors.