The Truth of Early-Stage Healthcare Investment and China's Acceleration

FreeS Fund

Venture Capital Firms

Editor’s Note: This article is reprinted from FreeS Fund, authored by Wang Lei. VCBeat has been authorized to republish it.

On June 25, the 120-year-old MIT Technology Review released its 2019 list of “50 Smartest Companies” (TR50). Life sciences emerged as a prominent highlight on this list, with ten companies featured across fields including gene editing, new drug development, pharmaceutical professional services, medical devices, and medical equipment.

On May 24, the U.S. FDA officially approved Zolgensma, the first gene therapy developed by Novartis for the treatment of spinal muscular atrophy (SMA) in children under two years of age. Prior to this approval, most infants with this condition would not survive beyond the age of two due to respiratory failure. The approval of Zolgensma marks a milestone in the use of gene and cell therapies for disease treatment.

On May 14, GRAIL, a U.S. company known as the “Tesla” of early cancer detection, announced that its multi-cancer blood test had received Breakthrough Device Designation from the FDA, marking a significant step toward approval.

In recent years, there have been numerous examples of technology demonstrating its allure, unleashing its potential, and transforming medicine. Of course, we have also witnessed the shattering of technological ideals. On May 27, IBM Watson Health, the AI healthcare giant, announced large-scale layoffs, sparking a debate: In the digital era, how far away is the realization of “AI + Healthcare,” and how can we fully unleash AI’s potential to transform medicine? This article will address the following questions one by one:

1. Returns on Biomedical Investments in Mature Markets (the U.S.) Far Exceed Expectations

2. Turning to China, is now a good time for early-stage investment in tech-driven healthcare?

2.1 Three Major Drivers of the Development of China's Biomedical Industry

2.2 Five Opportunities Drive the “China Speed” in Tech-Enabled Healthcare

3. Summary: How Do We Position Ourselves in Early-Stage MedTech Investments?

I hope this offers you some new perspectives.

Investing in early-stage healthcare projects has long been a subject of controversy. The most common criticisms center on the high capital requirements, elevated risks, and prolonged return horizons, which seem to make profitability elusive. However, this is not the case. Let us examine the returns on biopharmaceutical investments in mature markets such as the United States.

First, biotech venture capital delivers strong returns in mature markets.

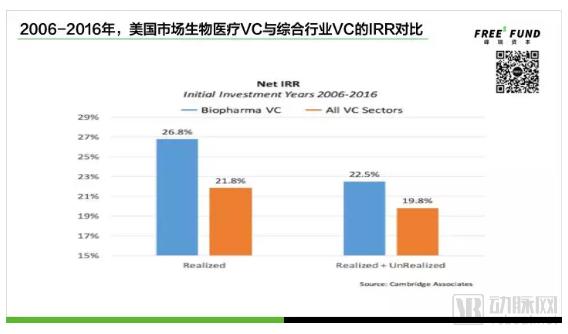

The data below are sourced from the blog of a partner at a prominent U.S. healthcare venture capital firm. The first chart compares the internal rate of return (IRR) of healthcare VC investments with that of generalist VC investments in the U.S. market from 2006 to 2016. Based solely on data from this period, we observe that healthcare VC returns—both realized and unrealized—are significantly higher than those of generalist VC funds.

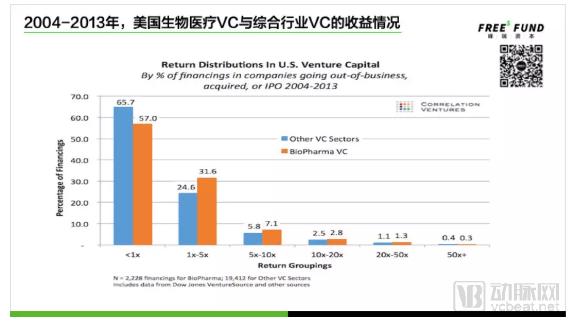

The second chart compares the returns of U.S. healthcare venture capital (VC) and general-industry VC from 2004 to 2013. It shows that, except in the range where returns exceed 50x—where healthcare VC underperforms general-industry VC—healthcare VC delivers higher returns than general-industry VC across the 0–50x return range.

This blog reviews nearly 16,000 healthcare investment cases, revealing that only one biopharma unicorn with a return multiple exceeding 50x emerges for every 300 deals on average. From this perspective, biopharma projects may appear less dazzling than star investments in the consumer sector. However, in terms of overall returns, healthcare-focused funds have consistently maintained their own distinct performance dynamics and have been validated over long cycles in mature markets.

Secondly, in mature markets, biomedical projects have shorter exit cycles and lower investment losses.

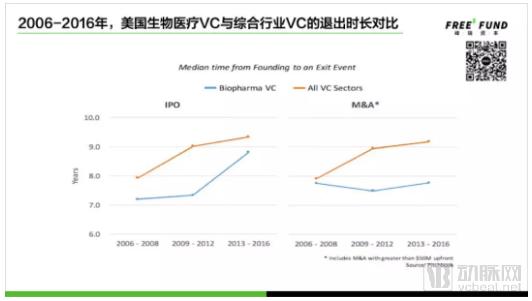

The chart below reflects the average exit duration for U.S. healthcare venture capital (VC) firms versus generalist VC firms between 2006 and 2016. It can be seen that the average exit time for healthcare VC is shorter than that for generalist VC.

A key reason is that, generally, the cycle from drug and medical device development to commercialization is lengthy. Neither venture capital (VC) firms nor large private equity (PE) funds can easily sustain the substantial expenditures required for drug and device R&D after Phase II or Phase III clinical trials. Consequently, major VC investors typically exit at relatively early stages, making secondary markets and large-scale mergers and acquisitions (M&A) the primary exit routes for such projects.

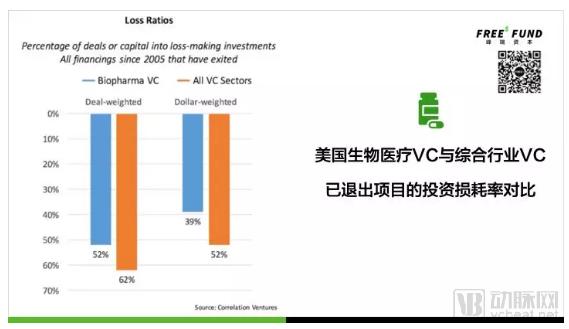

Let’s examine the investment loss situation. The chart below reflects the investment losses of exited projects in U.S. healthcare venture capital (VC) versus general-industry VC since 2005. Whether measured by deal count (deal-weighted) or investment amount (dollar-weighted), healthcare VC has experienced lower investment losses compared to general-industry VC.

Moreover, mature secondary markets are favorable to biomedical stocks.

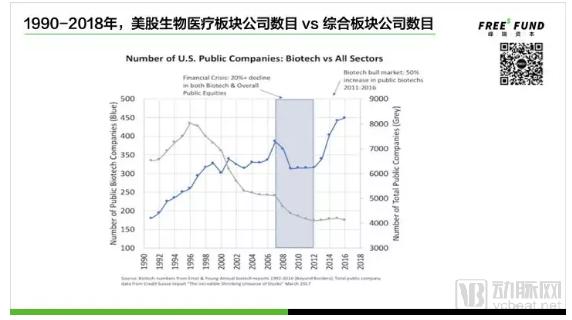

The number of newly listed biopharmaceutical companies continues to grow. In the chart below, the blue line represents the number of biopharmaceutical companies listed on U.S. stock exchanges, while the gray line represents all companies listed on the secondary market. Although these sectors differ, the overall trend for biopharmaceutical stocks is clear: a continuous increase in new listings coupled with very few delistings, indicating strong popularity in the secondary market.

Biomedical venture capital has become a significant component of venture investment in mature markets, primarily the United States. In terms of return on investment, exit timelines, and investment losses, biomedical VC demonstrates outstanding performance in these mature markets.

Diversified and standardized exit channels have yielded substantial returns for biomedical projects. The trend of technology-driven medical innovation has also endowed biomedical projects with strong scalability and liquidity in the secondary market.

Having covered the mature markets, how is biopharma investment performing in emerging markets? Let us turn our attention to China, the second-largest market for global healthcare investment.

2018 was a landmark year for healthcare investment in China. Consider the following figures to get an intuitive sense of the fervor in last year’s healthcare investment market:

In 2018, the total global investment and financing in the healthcare industry amounted to $38.801 billion, with a total of 1,410 financing events, of which 930 were concentrated in the four hot sectors of biotechnology, medical devices, pharmaceuticals, and healthcare informatics;

In the same year, the total investment and financing volume in China’s healthcare industry reached RMB 82.585 billion, marking the highest level in the past five years, with a year-on-year growth rate of 78.64%. A total of 695 transactions were recorded, with an average investment amount of approximately RMB 119 million per deal.

Favorable national policies, technology-driven innovation, and rising demand from an aging population have combined to create a powerful synergy, driving the “China speed” of development in the healthcare industry in 2018.

Why Did China’s Healthcare Investment Boom Only Arrive in 2018? Let’s Turn the Clock Back Four Years.

In 2015 and 2016, global healthcare investment was booming. This period coincided with the initial completion of electronic health record (EHR) adoption in the United States, as well as the amplifying effects of mobile internet, giving rise to many business model innovations such as telemedicine, chronic disease management, and healthcare big data.

During those years, the imbalance between supply and demand and low efficiency were the prominent contradictions in China’s healthcare industry. However, the talent pool and policy framework across the entire market were insufficient to support the launch of technology-driven healthcare startups. As a result, venture capital investments in the early to mid-stages of the healthcare sector at that time were predominantly focused on business model innovation. At that time, some established, traditional professional healthcare funds in China mainly invested in generic drugs or later-stage projects. Yet, opportunities in these areas have become scarce today.

Since mid-2016, technology-driven healthcare investment has gained momentum, with advanced diagnostic technologies, biotechnologies, and various platforms supporting these innovations emerging to establish a foothold in the healthcare startup ecosystem. These developments laid the foundation for the surge in healthcare investment in 2018.

More than three years ago, at the inception of FreeS Fund, we invested in a number of early-stage healthcare projects focused on business model innovation. These ventures have withstood the tests of time, market dynamics, and regulatory policies as they progressed from initial concepts to the implementation of products and services; some have even secured new growth opportunities after overcoming challenges.

We believe that for projects with light service components, entrepreneurs’ learning agility and stress resilience are crucial. As the healthcare industry is vital to public welfare and highly sensitive to policy changes, founders must continuously adapt to the evolving regulatory environment to drive their ventures forward. Entrepreneurs who start with the right intentions and possess determination will ultimately persevere until they see the light at the end of the tunnel.

Since 2016, we have observed a trend: innovation is increasingly cross-disciplinary, with breakthrough innovations often occurring at the intersections of different fields. This holds true in the healthcare sector as well. The convergence of biology with data and computing, biology with electronics (automation, sensors), AI with drug discovery, and biology with materials science is reshaping the industry. Deep technologies, including single-cell technology and synthetic biology, are becoming key drivers of development in the healthcare sector.

This means that we need a multidisciplinary team with diverse know-how—spanning technology, application, and consumer sectors—to jointly evaluate projects. To this end, in 2016, we established a tech-healthcare team composed of members from multidisciplinary backgrounds, shifting our focus toward technology-driven early-stage healthcare investments and striving to identify promising early-stage ventures in the tech-healthcare sector.

Three Major Drivers of the Development of China’s Biomedical Industry

The current moment presents an excellent opportunity for venture capital in China’s biopharmaceutical sector, with the potential to achieve investment expectations comparable to those in the U.S. market. This section analyzes the key drivers currently shaping China’s biopharmaceutical industry to explain why we are in a relatively favorable window.

The driving factors are mainly divided into three aspects: one is the dividends of national policies, another is the demand growth brought about by changes in the aging population structure, and the last is deep technology represented by artificial intelligence, cellular immunotherapy, and gene editing.

Drivers from national policy dividends can be assessed using three indicators:

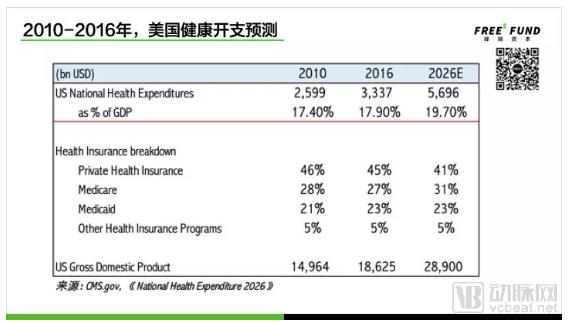

National Healthcare Expenditure as a Percentage of GDP: In 2016, China’s total health expenditure accounted for only about 6% of its GDP, whereas in the same year, U.S. healthcare spending represented approximately 18% of its GDP. The U.S. healthcare sector has experienced accelerated growth in recent years, and is projected to reach around 20% of GDP by 2026. By that time, the U.S. healthcare industry is expected to employ 14% of the nation’s workforce (17 million people), underscoring the indispensable role of the healthcare sector in the U.S. national economy.

Although China’s healthcare expenditure has been rising year by year, it remains relatively low in comparison. Since 2012, the proportion of healthcare spending to GDP in China has steadily increased. The government has also introduced a series of favorable policies related to biomedical investment, which have become the core driving force for future economic growth in China’s healthcare industry.

Government Fiscal Spending on Healthcare: According to statistics, China’s healthcare expenditure accounted for only about 7% of its total fiscal spending in 2017, a significant gap compared to the United States’ 27% in the same year. The U.S. figure is projected to reach approximately 30% by 2028, meaning that nearly three-tenths of the government’s fiscal budget will be allocated to covering medical costs for the elderly and low-income populations. In this regard, China may need to increase financial support from the Ministry of Finance in the future.

Out-of-Pocket (OOP) Expenditure Ratio: Currently, the proportion of out-of-pocket payments in China’s healthcare payment system remains high, necessitating medium- to long-term structural improvements.

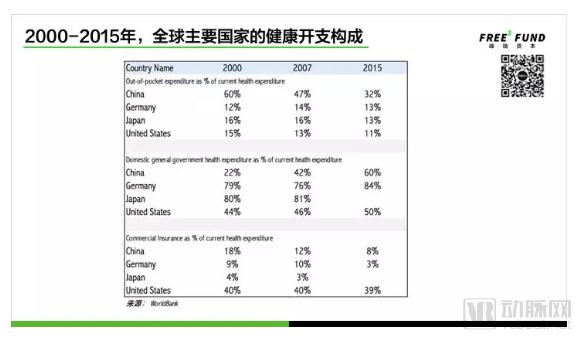

The World Bank collected data on the composition of health expenditure in major countries worldwide from 2000 to 2015. The data show that in 2015, out-of-pocket payments accounted for 32% of total health expenditure in China. This means that, on average, 32% of medical costs for each healthcare visit were paid directly by individuals. Compared with countries such as Japan, Germany, and the United States, this proportion is undoubtedly very high.

In Japan and Germany, a major direction in the current healthcare structure is to continuously strengthen public health insurance funds to achieve universal coverage. Under this model, the state bears the majority of medical costs, significantly reducing out-of-pocket expenses for individuals. However, this approach leads to increased fiscal pressure, as well as growing challenges in cost containment and management of the health insurance system.

The United States is the only country in the chart where health insurance has been commercialized. However, even though commercial insurance covers approximately 50% of healthcare costs, the government still bears the bulk of the remaining 40%, with minimal out-of-pocket expenses for individuals. While over-treatment and insurance waste have long been widely criticized within the U.S. healthcare industry, American citizens can access relatively comprehensive medical coverage without bearing excessive financial burdens, which reflects a hallmark of an advanced society.

In recent years, the United States has continuously promoted the development of commercial health insurance. Its sustainable growth will depend in the short to medium term on whether the commercial health insurance industry can rationally leverage big health data and engage in deep collaboration with healthcare institutions to transition into a managed care model. In the medium to long term, it will hinge on whether public health insurance funds and commercial health insurance can assume greater expenditure responsibilities to help middle-class families and residents in remote areas share the financial risks associated with illness. Concurrently, it is essential to improve the supply of medical resources and establish a robust primary care physician system.

Demand Growth Driven by Demographic Shifts. The most prominent demographic shift is the acceleration of population aging. According to United Nations data, the proportion of China’s population aged 65 and above will rise from 10% in 2015 to 26% by 2050. In absolute terms, given China’s large population base, the current total number of people aged 65 and older in China already exceeds that of Japan and the United States. There are many reasons for the accelerating aging of China’s population, such as the baby boom in the 1970s and improvements in healthcare conditions in recent years.

Furthermore, advancements in medical technology have increased supply across the entire healthcare industry and optimized resource allocation. As a result, this has effectively extended life expectancy while simultaneously exacerbating population aging.

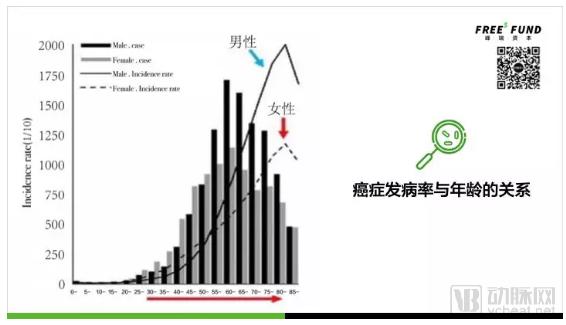

As people age, the prevalence of disease rises, generating greater demand in the healthcare market, particularly for chronic conditions such as cancer, diabetes, and hypertension. The chart below provides supporting evidence: between the ages of 30 and 80, there is a positive correlation between advancing age and cancer incidence; however, after age 80, various cellular metabolic processes in the human body slow down relatively, cancer cells become less active, and the incidence rate actually declines.

Ultimately, the sector is driven by deep technologies represented by artificial intelligence, cellular immunotherapy, and gene editing. For a long time, technology and healthcare have formed a positive feedback loop: growing healthcare demand coupled with insufficient supply has spurred advancements in medical technology; meanwhile, new technologies have introduced better treatment methods and higher cure rates, which in turn have generated new healthcare demands. For example, as medical technology continues to advance and major life-threatening diseases such as cancer and diabetes are increasingly conquered, new health demands may shift toward anti-aging and longevity extension.

Currently, the dual forces of information technology and biotechnology are simultaneously driving the upgrading of the medical and healthcare industry. Benefiting from advancements in information technology, hospital information systems have been upgraded, while mobile health and telemedicine, propelled by government policies, are dedicated to promoting health and chronic disease management and addressing the challenge of uneven distribution of medical resources. The leapforward development of biotechnology has made precision medicine possible, shifting the entire healthcare system upstream so that prediction and prevention become the focal points of healthcare. Its commercialization has the potential to reshape the future landscape of the healthcare industry.

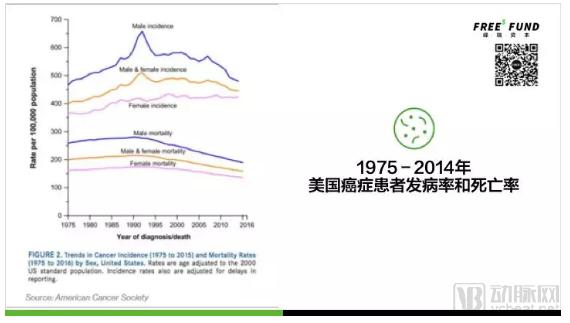

The benefits these two technological forces have brought to the healthcare industry can be seen in the annual report titled “Cancer Statistics 2017,” published by the American Cancer Society in a leading oncology academic journal. The report indicates that over the past two decades, the overall cancer mortality rate in the United States has declined by 25%. Notably, both the incidence and mortality rates for several common cancers—lung cancer, breast cancer, prostate cancer, and colorectal cancer—have decreased significantly.

The two primary drivers behind the decline in the number of cancer patients in the United States are advances in medical technologies, such as tumor detection and treatment, and the government’s stringent control over tobacco. Dr. Otis Brawley, Chief Medical Officer of the American Cancer Society, stated that approximately 30% of cancer-related deaths are attributable to tobacco use, and the decline in tobacco consumption has effectively contributed to the reduction in cancer incidence.

China has seen a downward trend in cancer prevention and treatment due to the introduction of certain advanced drugs and technologies; however, there is still a long way to go to catch up with the United States.

New technologies, growing demand, and policy support—the three major drivers—propelled the development of China’s biomedical sector in 2018.

FreeS Fund places particular emphasis on the transformative impact of emerging technologies on the healthcare industry and has participated in angel and Pre-A round investments in multiple tech-driven healthcare ventures. Singleron is dedicated to applying its breakthrough single-cell analysis technology to clinical diagnostics, health management, and drug development. Xtalpi, a world leader in computation-driven innovative drug R&D, has established collaborations with pharmaceutical giants such as Pfizer and Roche. In the field of synthetic biology, Bluepha, our portfolio company, is the world’s only provider of full-spectrum PHA bioplastics.

Five Opportunities Made 2018 a Breakout Year for Biomedical Investment in China

2018 became a breakout year for biopharmaceutical investment in China, primarily driven by the following five opportunity areas, which collectively underscored the new pace of China’s strategic deployment in the biopharmaceutical sector:

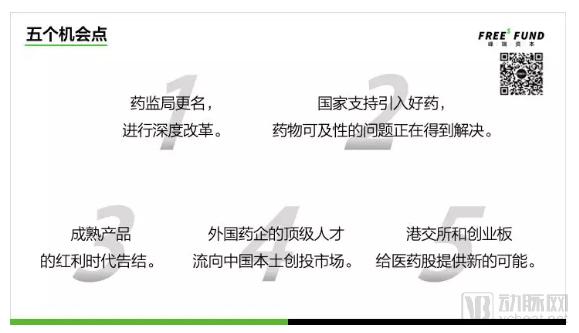

First, the drug regulatory authority was renamed and underwent in-depth reforms. In June 2018, the agency approved 71 drugs in a single batch. In September, it was officially renamed the National Medical Products Administration (NMPA) and recruited extensive talent from institutions including the U.S. FDA. The signal was clear: to standardize, professionalize, and accelerate the registration of new drugs in China.

Second, the state supports the introduction of high-quality medicines, and the issue of drug accessibility is being addressed. In 2018, both the National Essential Medicines List and the National Reimbursement Drug List were significantly expanded, with 17 oncology drugs added. Currently, most conventional oncology drugs are basically available in China. Following the release of the film “Dying to Survive,” the issue of drug accessibility garnered national attention, prompting the government to become more willing to introduce higher-priced medications for certain difficult-to-treat and serious diseases. For biomedical venture capital firms, investment in pharmaceuticals has always been a rigid demand. Coupled with current policy support, this sector holds even greater investment potential in the future.

Third, the era of dividends for mature products has come to an end. Mature products manufactured by foreign pharmaceutical companies that have passed their patent protection periods are beginning to face challenges in the Chinese market. Take cefaclor (Ceclor from Eli Lilly and Company), a commonly used antibiotic, as an example. The drug was approved in the United States in 1979, and its patent expired in 1993. In the U.S., generic versions typically become available immediately after a brand-name drug’s patent expires, allowing for virtually seamless, zero-cost market entry.

However, since Ceclor entered the Chinese market in 1993, it has remained a best-seller, generating hundreds of millions in annual sales on average. Interestingly, Ceclor is not an exception. Medicines produced by foreign pharmaceutical companies and registered in China typically remain actively marketed for more than 15 years.

Recently, the National Medical Products Administration (NMPA) introduced the “4+7” policy—a centralized drug procurement program involving four municipalities directly under the central government and seven provincial capitals or cities with independent planning status. The policy aims to encourage domestic pharmaceutical companies to produce and sell locally manufactured alternatives to Ceclor at lower costs, provided these alternatives are of equivalent quality. This initiative is designed to incentivize local manufacturers to independently develop high-quality medicines, posing a significant challenge to multinational pharmaceutical corporations. The crisis facing mature products signals greater opportunities and room for growth for Chinese pharmaceutical enterprises in the future.

Fourth, top-tier talent from foreign pharmaceutical companies is flowing into China’s local venture capital and startup market. Five years ago, China had a relative scarcity of healthcare innovation projects and talent; the professionals recruited were primarily focused on CMC (Chemistry, Manufacturing, and Controls) and CRO (Contract Research Organization) sectors. Today, healthcare entrepreneurship is booming, and the war for talent has begun. Senior executives from the Top 10 multinational pharmaceutical companies are leaving these large foreign firms to dive into the wave of healthcare startups in China. For example, the former President of Sanofi’s Asia-Pacific R&D Headquarters announced in 2016 that he would join CStone Pharmaceuticals as CEO, and a former Vice President of AstraZeneca joined Zai Lab after departing in 2018. A similar migration trend is evident among mid-to-senior and middle-level managers from multinational corporations, spanning various functional departments including R&D and clinical operations. Their management expertise and industry networks will prove beneficial to the development of healthcare startup enterprises.

Fifth, the Hong Kong Stock Exchange and the STAR Market are creating new possibilities for biopharmaceutical stocks. Although China’s secondary market is far less receptive to biopharmaceutical companies than mature markets such as the United States, privatization models are generally ill-suited to support firms in this sector. Consequently, seeking additional capital through public listings has become an inevitable path, with a growing trend toward earlier entries into the secondary market. In the future, the development of biopharmaceutical enterprises on China’s ChiNext board or the Hong Kong stock market will largely follow this trajectory.

The Hong Kong Stock Exchange (HKEX) is highly receptive to biopharmaceutical companies with no revenue statements. Overall, the total capital raised by Chinese biopharmaceutical startups still lags significantly behind that of their U.S. counterparts, whether in terms of government support or backing from venture capital (VC) and private equity (PE) firms. Although VC and PE support has increased substantially since 2015, the industry will continue to advance driven by capital inflows. While some believe the current market boom is accompanied by a bubble, it has not yet reached that stage.

2018 was a pivotal year for healthcare entrepreneurship and investment in China, with numerous favorable factors converging. On one hand, the state deepened reforms and encouraged domestic innovation; on the other, mature products from foreign pharmaceutical companies lost their dominance in the Chinese market, while top-tier talent from multinational corporations joined Chinese healthcare startups. Coupled with increasingly diverse and investor-friendly exit channels, we believe this is a golden era for early-stage healthcare investment.

The healthcare entrepreneurship value chain is extensive, with high barriers to entry at every stage—from initial concept to productization and ultimately commercialization. This means that founders must possess deep industry expertise. We are optimistic about healthcare industry veterans embarking on entrepreneurial ventures, particularly those with extensive experience in pharmaceutical management.

Our macro-level strategy primarily focuses on projects that integrate early-stage innovation with technology, offer market and pricing potential sufficient to justify the associated risks, and possess an appropriate pool of innovative talent.

Moreover, projects involving related technologies and interdisciplinary fields will also present new opportunities, as the innovation process of any industry that appears massive today is entirely cross-disciplinary, with breakthrough innovations often occurring at the intersections of different disciplines. Examples include biology + data and computing, biology + electronics (automation, sensors), chips + algorithms, biology + materials, chips + consumer scenarios, and consumer + data.

Outstanding healthcare projects invested in by FreeS Fund in recent years, such as XtalPi, Bluepha, and Singleron, are typical examples of interdisciplinary ventures. XtalPi integrates cloud computing, AI, and pharmaceuticals; Bluepha combines AI, computation, and biology; and Singleron merges biology, chip technology, and computation.

At the micro level, we primarily focus on the following areas: first, in vitro diagnostics (IVD), particularly opportunities arising from the rapid development of molecular diagnostics and immunoassays; second, innovative biologics and platforms, including monoclonal antibodies, protein therapeutics, and other large-molecule drugs; third, differentiated small-molecule chemical drugs; fourth, disruptive biotechnologies; and fifth, medical devices and consumables featuring incremental innovation that drive import substitution.

Finally, thank you for your patience in reading this in-depth analysis of the biomedicine industry. I hope it offers some inspiration and that you find valuable insights in the healthcare sector, the most enigmatic waters for venture capital.