Ten Healthcare Companies Listed in Hong Kong in H1 2019: BeiGene-Style Biotechs Like CStone and JinXin Gain Attention, Vaccine Stocks Lead Market Performance

Since 2018, Hong Kong stocks have witnessed an IPO boom. The streamlined procedures, lenient listing requirements, high success rate, and short waiting period have become the primary reasons why companies are keen on listing in Hong Kong. According to statistics from securities firms, over the past four years, companies that filed for IPOs in the Hong Kong market took an average of only 114 days from the submission of IPO application materials to their initial public listing.

With the new amendments to the Listing Rules of The Stock Exchange of Hong Kong Limited taking effect last year, which permit pre-revenue biotechnology companies to list, a wave of biotech firms that have not yet achieved commercialization has joined the IPO boom in the Hong Kong stock market. Last year, four pre-profit biotechnology companies—Ascletis Pharma, BeiGene, Innovent Biologics, and Junshi Biosciences—went public in Hong Kong following the implementation of the new regulations.

Which healthcare companies went public via IPOs in Hong Kong in the first half of this year? How many of them were pre-revenue biotech firms? What was their performance? VCBeat (WeChat ID: vcbeat) has compiled an overview.

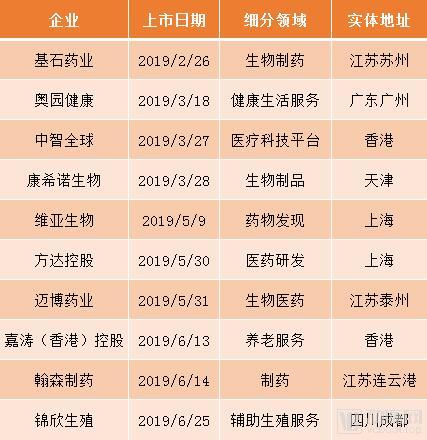

Overview of Healthcare Companies’ IPOs on the Hong Kong Stock Exchange in the First Half of 2019

Source: The Stock Exchange of Hong Kong, corporate websites

VCBeat statistics show that a total of 10 healthcare companies were listed in Hong Kong during the first half of 2019. These enterprises are primarily located in the Yangtze River Delta region, with three from Jiangsu Province and two from Shanghai.

Jiangsu is a major pharmaceutical province, home to a large number of leading enterprises in their respective niches, such as Hengrui Medicine, Yangtze River Pharmaceutical Group, and WuXi AppTec. It also hosts key pharmaceutical industry clusters, including the Suzhou BioBAY, Taizhou China Medical City, and the Lianyungang Economic and Technological Development Zone. Local pharmaceutical companies benefit from substantial technological and policy advantages.

In November 2018, the Shanghai Municipal People's Government issued the "Notice on the Action Plan for Promoting High-Quality Development of Shanghai's Biopharmaceutical Industry (2018-2020)," proposing to build a globally influential source of biopharmaceutical innovation and a biopharmaceutical industry cluster. This has enabled local pharmaceutical companies to receive greater policy support and access more resources along the industrial chain.

In terms of business distribution, these 10 companies are involved in fields such as drug discovery, biopharmaceuticals, assisted reproductive services, and elderly care services, among which six are pharmaceutical R&D and manufacturing enterprises. The specific business focuses of each company are as follows:

Profile of Healthcare Companies Listed via IPO on the Hong Kong Stock Exchange in the First Half of 2019

Source: Company website

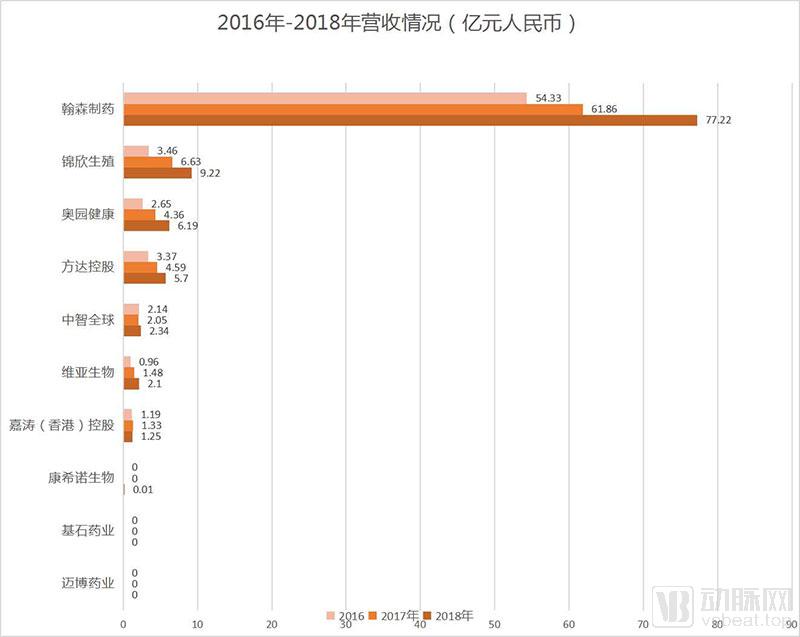

Revenue Performance of Healthcare Companies That Went Public in Hong Kong via IPO in the First Half of 2019

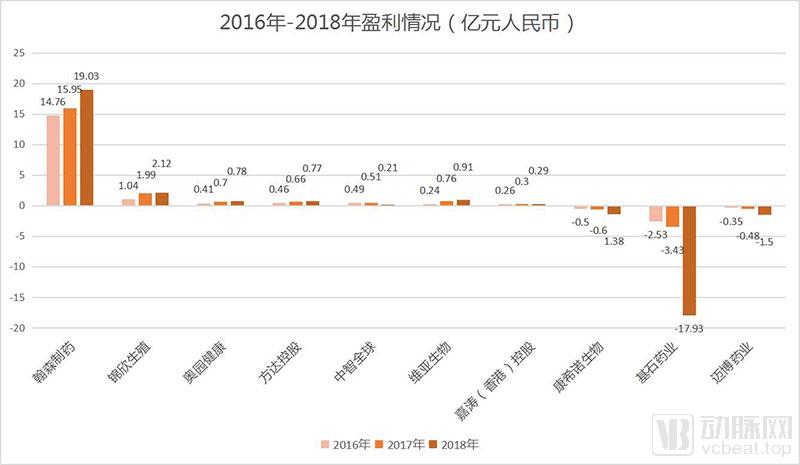

Profitability of Healthcare Companies That Went Public in Hong Kong via IPOs in the First Half of 2019.

Source of revenue and profit data: Prospectuses and 2018 annual reports of the respective companies; compiled by VCBeat.

Based on the revenue and profitability performance of 10 companies over the past three years, VCBeat has roughly categorized these 10 companies into three tiers:

Tier 1: Mature-Stage Enterprises

Hansoh Pharmaceutical, with annual revenue exceeding RMB 5 billion and annual net profit surpassing RMB 1 billion, has achieved steady year-on-year growth.

Hansoh Pharmaceutical, established 24 years ago, is a leading R&D-driven pharmaceutical company in China. The company focuses on six therapeutic areas: central nervous system disorders, oncology, anti-infectives, diabetes, gastrointestinal diseases, and cardiovascular diseases. It boasts an extensive, diversified, and leading drug portfolio, with a strategic emphasis on the research, development, and commercialization of Class 1.1 innovative drugs and first-to-market generics.

Since 2002, Hansoh Pharmaceutical has been developing Class 1.1 innovative drugs. Currently, two new molecular entity (NME) Class 1.1 innovative drugs have been developed and launched, while six Class 1.1 innovative drugs under development have entered Phase II clinical trials or later stages of research, with four of them scheduled for launch before 2020.

Furthermore, Hansoh Pharmaceutical has developed various proprietary technologies, including its exclusive PEGylation modification technology, which has enabled the company to develop a series of Class 1.1 innovative long-acting drugs.

To date, Hansoh Pharmaceutical has launched more than 30 first-to-market generic drugs in China, including Oulanning and Amening for central nervous system disorders; PulaiLe, Zefei, Xinwei, and Xintai for oncology; Zetan, Hengjie, and Hengsen for anti-infective therapy; Fulaidi for diabetes; and Ruibote for gastrointestinal diseases.

Another noteworthy statistic is that Hansoh Pharmaceutical has had 30 drugs included in the National Reimbursement Drug List, 13 of which are its key products. From 2016 to 2018, revenue from these 13 key products accounted for 83.4%, 85.7%, and 89.5% of total revenue during the respective periods.

Second Tier: Growth-Stage Companies

Growth-stage companies have established stable profitability, driven either by R&D capabilities or business models. This cohort includes Fangda Holdings, Viva Biotech, Jinxin Fertility, Aoyuan Health, and CIIC Global.

Fangda Holdings is a contract research organization (CRO). From 2016 to 2018, its revenues were RMB 337 million, RMB 459 million, and RMB 570 million, respectively, with bioanalytical services spanning the entire drug development process constituting its largest revenue source. In recent years, driven by regulatory policies such as the guidelines on consistency evaluation for generic drugs, outsourcing opportunities in drug research and analysis have increased. Fangda Holdings seized this opportunity, resulting in a substantial increase in revenue.

WuXi Biology, also a CRO, is a new drug discovery technology institution with multiple globally leading technologies. It has provided drug discovery services to nine of the top ten pharmaceutical companies worldwide, and its business extends to hundreds of biotechnology firms and research institutes around the globe.

While providing technical services, WuXi Biologics also makes strategic investments in biotech startups with high growth potential, combining its traditional Cash-for-Service (CFS) model with its proprietary Equity-for-Service (EFS) model. Under the EFS model, WuXi Biologics provides drug discovery and incubation services to clients in exchange for equity or economic interests in those clients, thereby capturing the upside potential of their intellectual property value. Meanwhile, the CFS model ensures the company maintains a stable cash flow.

From 2016 to 2018, WuXi Biology’s revenue amounted to RMB 96 million, RMB 148 million, and RMB 210 million, respectively, with net profit also increasing substantially. The growth was primarily driven by increases in fair value and gains from the disposal of equity interests in certain incubated portfolio companies.

Jinxin Fertility is an assisted reproductive technology (ART) medical institution. From 2016 to 2018, its total revenues were RMB 346 million, RMB 663 million, and RMB 922 million, respectively. According to a Frost & Sullivan report, the national average success rate for ART services provided by medical institutions in China was 45% in 2018, whereas Jinxin Fertility achieved a significantly higher rate of 54%. In addition to its technological advantages, Jinxin Fertility has expanded its industrial coverage through acquisitions. Currently, the group owns multiple institutions, most of which were acquired, including Chengdu Xinan Gynecology Hospital, Shenzhen Zhongshan Urology Hospital, the Reproductive Science Center (RSA) in the United States, and the PGS laboratory NexGenomics.

Aoyuan Health is a property management and commercial operation service provider, with revenues of RMB 265 million, RMB 436 million, and RMB 619 million in 2016, 2017, and 2018, respectively. Its prospectus indicates that businesses related to the healthcare industry have not yet generated revenue, with main earnings still coming from advantageous sectors such as property management and commercial operations. Aoyuan Health is exploring businesses including beauty training, traditional Chinese medicine services, and elderly care services.

In addition, CIIC Global is a service provider of qualification certification platforms for the healthcare industry. Its revenues from 2016 to 2018 were RMB 214 million, RMB 205 million, and RMB 234 million, respectively. With its primary business located in the United States, the company derives most of its revenue from annual fees paid by members for supplier qualification certification solutions. Kato (Hong Kong) Holdings is a long-established operator of elderly care homes in Hong Kong, having built well-known branded facilities such as Kato and Fai TO. It achieved revenues of RMB 119 million, RMB 133 million, and RMB 125 million in 2016, 2017, and 2018, respectively.

Tier 3: Unprofitable Companies

On April 30 last year, the newly revised Listing Rules of The Stock Exchange of Hong Kong Limited came into effect, allowing pre-revenue biotechnology companies to list. The new rules have prompted a wave of unprofitable biotech firms to pursue initial public offerings (IPOs) in Hong Kong to secure sufficient funding for drug research and development and commercialization. Several unprofitable biotechnology companies listed in Hong Kong this year include CanSino Biologics, CStone Pharmaceuticals, and Mabwell Bioscience, with their respective details as follows:

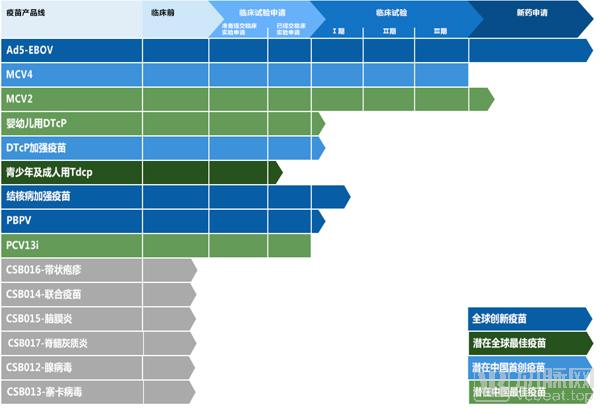

CanSino Biologics is dedicated to the research and development, production, and commercialization of high-quality, innovative, and affordable vaccines. Currently, it is developing 15 vaccine candidates across 12 disease areas. In addition to three products for the prevention of meningococcal infection and Ebola virus disease that are nearing commercialization, CanSino has six vaccines in clinical trials or under clinical trial application review, and another six vaccines in preclinical development.

From 2016 to 2018, CanSino Biologics incurred net losses of RMB 50 million, RMB 64 million, and RMB 138 million, respectively, while its R&D expenses increased year by year, amounting to RMB 50 million, RMB 68 million, and RMB 114 million, respectively.

CanSino Biologics Product Pipeline, Source: Official Company Website

CStone Pharmaceuticals is a biopharmaceutical company focused on the development and commercialization of innovative immuno-oncology therapies and molecularly targeted drugs. From 2016 to 2018, CStone Pharmaceuticals reported net losses of RMB 253 million, RMB 343 million, and RMB 1.793 billion, respectively. The company expects to incur significant expenses and operating losses in the coming years, primarily driven by research and development activities.

Currently, CStone Pharmaceuticals has established an oncology drug pipeline comprising 15 candidate drugs, five of which are late-stage candidates currently in or approaching pivotal trials.

CStone Pharmaceuticals’ Product Pipeline, Source: CStone Pharmaceuticals Official Website

Mabwell Therapeutics focuses on the research, development, and manufacturing of novel drugs and biosimilars for cancer and autoimmune diseases. Its candidate drug pipeline includes nine monoclonal antibody drugs, three of which are core products in Phase III clinical trials. From 2016 to 2018, Mabwell Therapeutics reported net losses of RMB 35 million, RMB 48 million, and RMB 150 million, respectively.

In addition to all being unprofitable, the aforementioned three companies share the following three commonalities:

These three companies have relatively short operating histories and have not yet successfully launched any new drugs. *Nature Reviews Drug Discovery* published an article analyzing drug development timelines, with data showing that the average time from preclinical target screening to final market approval is at least 13.5 years (excluding the target validation phase). Preclinical development takes an average of 5.5 years, while clinical development averages 8 years. A study published in the *Journal of Health Economics* also noted that the average drug development timeline is approximately 10 years, with average R&D costs reaching about $2.87 billion.

Although statistical estimates of drug development timelines and costs vary across studies due to differences in the therapeutic areas targeted, they consistently highlight prolonged development cycles and substantial financial investments; vaccine development is similarly a lengthy process.

All three companies possess gap products within their respective fields, indicating significant potential for future market growth.

For example, CMAB007 from Mabpharm is the only monoclonal antibody therapy for asthma developed by a domestic Chinese company in China to have reached Phase III clinical trials; CanSino’s Ad5-EBOV is China’s first approved Ebola virus vaccine, authorized for emergency use and national stockpiling; Antibody inhibitors targeting immune checkpoint proteins have become successful cancer treatments, with a recent trend toward combination therapies using backbone products of tumor immunotherapy: PD-1, PD-L1, and CTLA-4 antibodies. CStone Pharmaceuticals is the only company in China whose three backbone antibodies for tumor immunotherapy have all entered clinical stages.

These three companies boast outstanding R&D capabilities and a robust pipeline, which will further bolster their future growth potential.

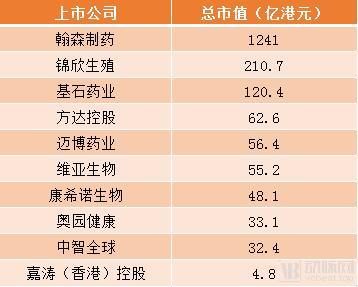

An analysis of the market capitalizations of these three companies reveals that CStone Pharmaceuticals’ market cap is more than double that of the other two. In addition to the substantial valuation potential within the oncology sector where its drugs operate, multiple drug candidates have advanced to late-stage clinical trials. CS1001, China’s first fully human, full-length anti-PD-L1 monoclonal antibody, initiated Phase III clinical trials in November 2018. Another product, Ivosidenib, indicated for the treatment of relapsed or refractory acute myeloid leukemia (AML) with an IDH1 mutation, received marketing approval from the U.S. FDA in July 2018.

Market Capitalization of Companies Listed on the Hong Kong Stock Exchange; Data Source: Hong Kong Exchanges and Clearing Limited; as of market close on July 2

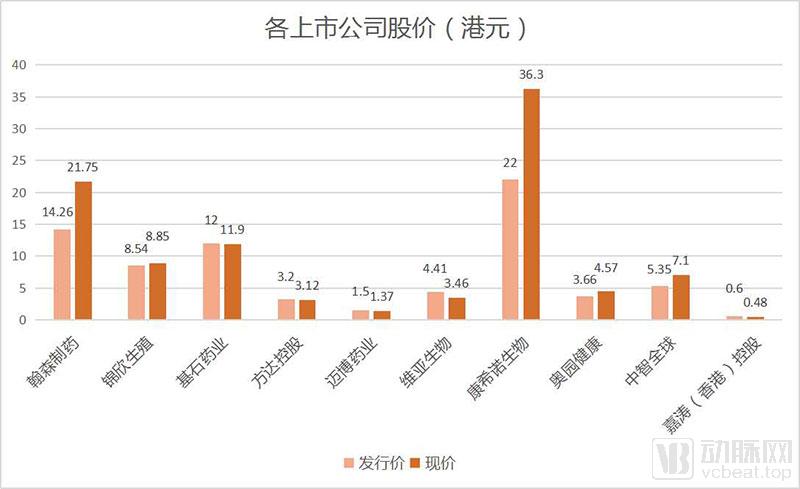

Comparison of IPO Price vs. Current Price for Each Company, Data Source: Hong Kong Stock Exchange, as of the close on July 2

In terms of stock prices and market capitalization, Hansoh Pharmaceutical has seen significant gains.

As a mature pharmaceutical company with steady growth in both revenue and profits, Hansoh Pharmaceutical’s financial performance has far outpaced that of its peers listed during the same period, earning investor recognition and pushing its market capitalization beyond RMB 100 billion.

In March 2016, the General Office of the State Council issued the “Opinions on Carrying out Quality and Efficacy Consistency Evaluation for Generic Drugs.” Following the issuance of this document, generic drugs that passed the consistency evaluation enjoyed several advantages, including preferential treatment in centralized bidding procedures. Hansoh Pharmaceutical’s three major products—Oulanning, Xinwei, and Fulaidi—were the first generic versions of olanzapine, imatinib mesylate, and repaglinide tablets, respectively, to pass the consistency evaluation in China, thereby gaining certain advantages in centralized bidding procedures.

In the preliminary list of winners for last year’s “4+7” volume-based procurement program, Hansoh Pharmaceutical had two drugs selected. Based on the officially announced procurement volumes and winning bid prices, this equated to a one-time order worth as much as RMB 229 million. Furthermore, Hansoh Pharmaceutical plans to expand its coverage in county-level and community hospitals to broaden its sales network and drive sales growth for new products, leveraging the tiered diagnosis and treatment system and the government’s increasingly favorable policies for smaller hospitals.

As the only vaccine R&D and manufacturing enterprise among the ten companies, CanSino Biologics recorded the highest stock price increase. Data from the Hong Kong Stock Exchange shows that its share price reached a high of HK$45.75. China is the world’s largest producer of human vaccines. According to data disclosed by the National Institutes for Food and Drug Control (NIFDC), the annual volume of vaccine batch releases in China ranges from 700 million to 1 billion doses, ranking first globally. In 2018, the volume of vaccine batch releases declined significantly year-on-year, primarily due to the production halt at Changchun Changsheng Bio-technology following the Changsheng Biological incident, which led to delays in batch release approvals for certain vaccines. As the impact of these industry incidents subsides, the domestic volume of vaccine batch releases is expected to gradually return to normal levels.

Furthermore, on June 29 of this year, the Vaccine Administration Law of the People's Republic of China was promulgated and will come into effect on December 1. As China’s first vaccine administration law, it fully embodies the core principles of raising entry standards for the vaccine industry, optimizing the competitive landscape, rectifying industry irregularities, increasing industry concentration, promoting industrial mergers and acquisitions as well as the development of leading enterprises, and encouraging innovative research and development, thereby enhancing certainty within the industry.

As a result, investor confidence in vaccine companies has also risen significantly.

In summary, mature companies have achieved gratifying results from their Hong Kong IPOs, securing both capital and enhanced influence; pre-profit biotechnology firms have been able to raise more funds to support further R&D and commercialization, with each type of company meeting its specific needs.

In recent years, Chinese-funded shares and mainland capital have accounted for an increasingly large proportion of the Hong Kong market. A company’s choice of listing venue is influenced by factors such as listing rules, market valuations, and IPO queue times. With the imminent launch of the STAR Market, many companies are also shifting their IPO targets to the Chinese mainland.

Next, how many healthcare companies planning an IPO, especially pre-profit biotech firms, will embark on the path to listing in Hong Kong? Will the number of healthcare companies listing on the STAR Market surpass those on the HKEX? Let us wait and see in the second half of 2019.