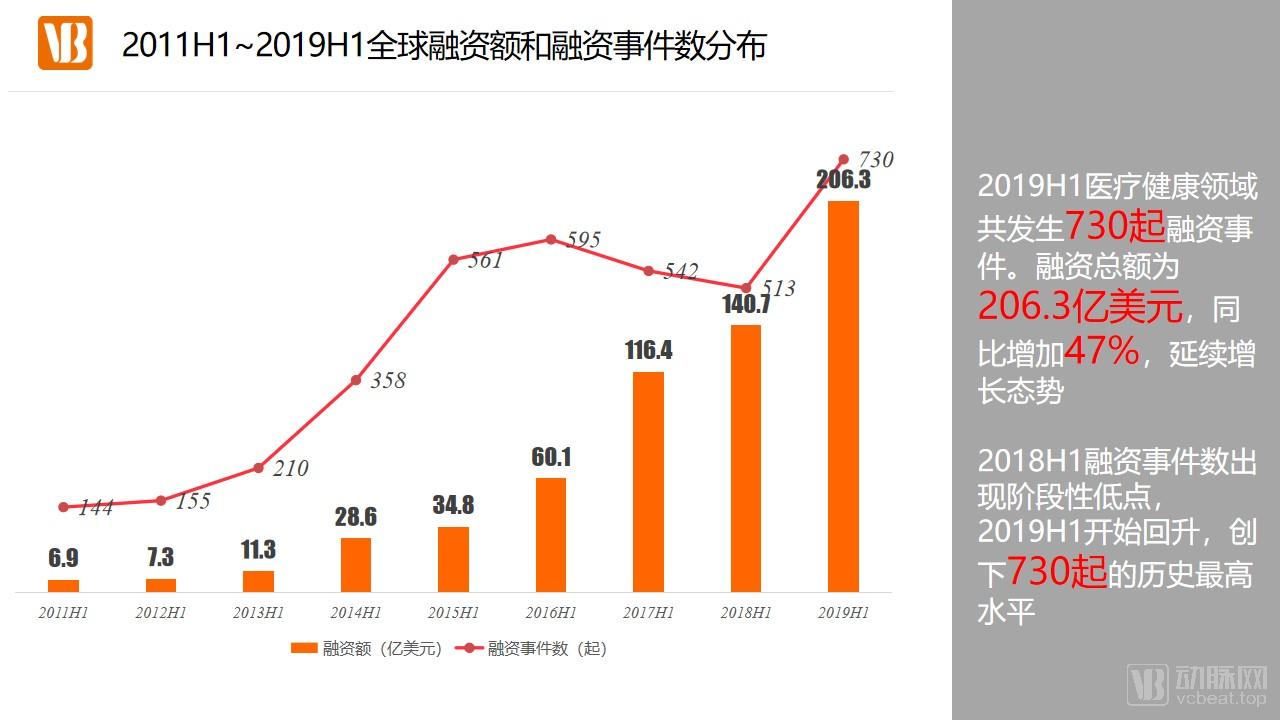

Record-Breaking H1 2019: 730 Deals Raise Over $20B in Global Healthcare Investment, Led by JD Health’s $1B+ Series A

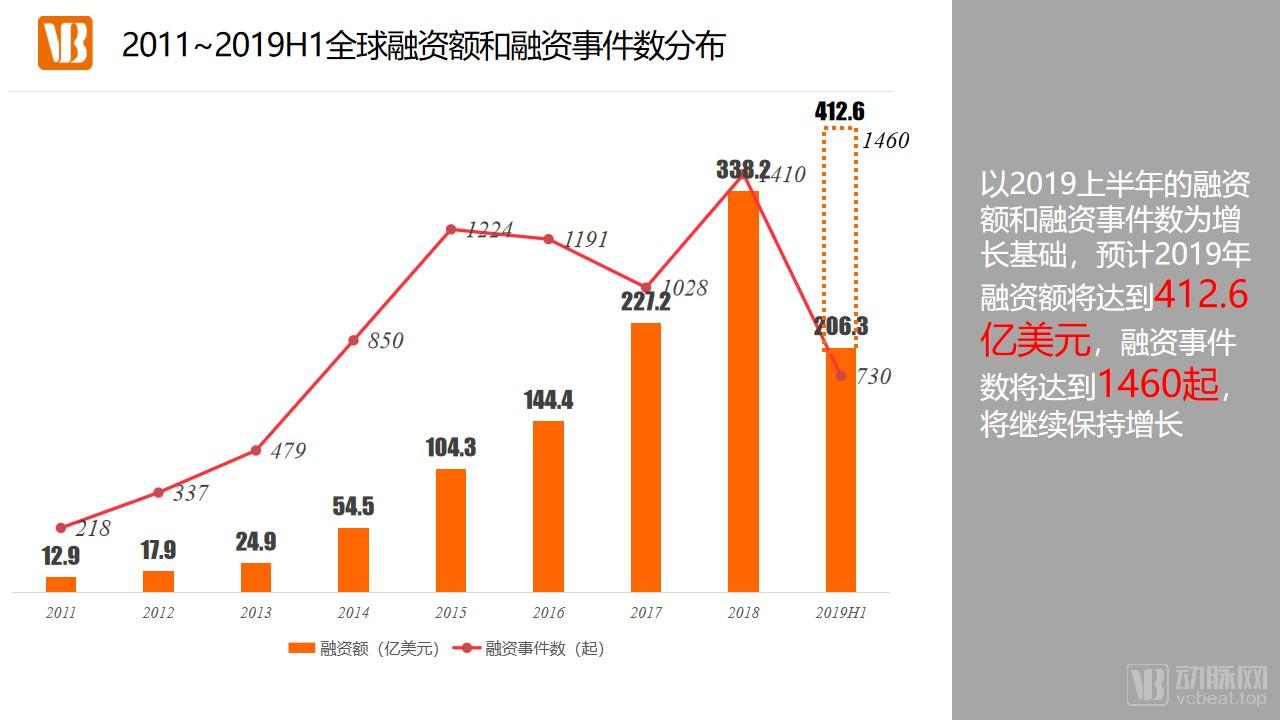

In the first half of 2019, a total of 730 financing deals occurred in the global healthcare industry, with the total financing amount reaching $20.63 billion. Based on this, the full-year financing amount for 2019 is projected to exceed $40 billion, and the number of financing deals is expected to approach 1,500, both setting new historical highs. The healthcare industry will continue to maintain a strong growth momentum. Within the specific sectors of healthcare, biotechnology and pharmaceuticals remain the areas of greatest interest to investors, with these two fields having the highest number of listed companies. Regenerative medicine, genetic engineering, and biomaterials have become representatives of innovation in the healthcare industry, driving the entire sector forward. (The scope of this financing report includes 72 undisclosed financing rounds)Financing Event, but financing events with undisclosed amounts are not included in this statistics).

As can be seen from the relevant data, the number of financing events and the total financing amount we have compiled are significantly higher than those published by other institutions. This is primarily because our statistical scope covers major countries worldwide, and the sectors included not only encompass popular areas such as biopharmaceuticals, biotechnology, and digital health, but also extend to traditional fields such as chemical pharmaceuticals, consumer healthcare, healthcare finance, and maternal and child health. Through in-depth mining of large-scale data, we have drawn the following conclusions:

(1) The pharmaceutical sector, particularly the biopharmaceutical segment, has seen the highest number of successful corporate listings.

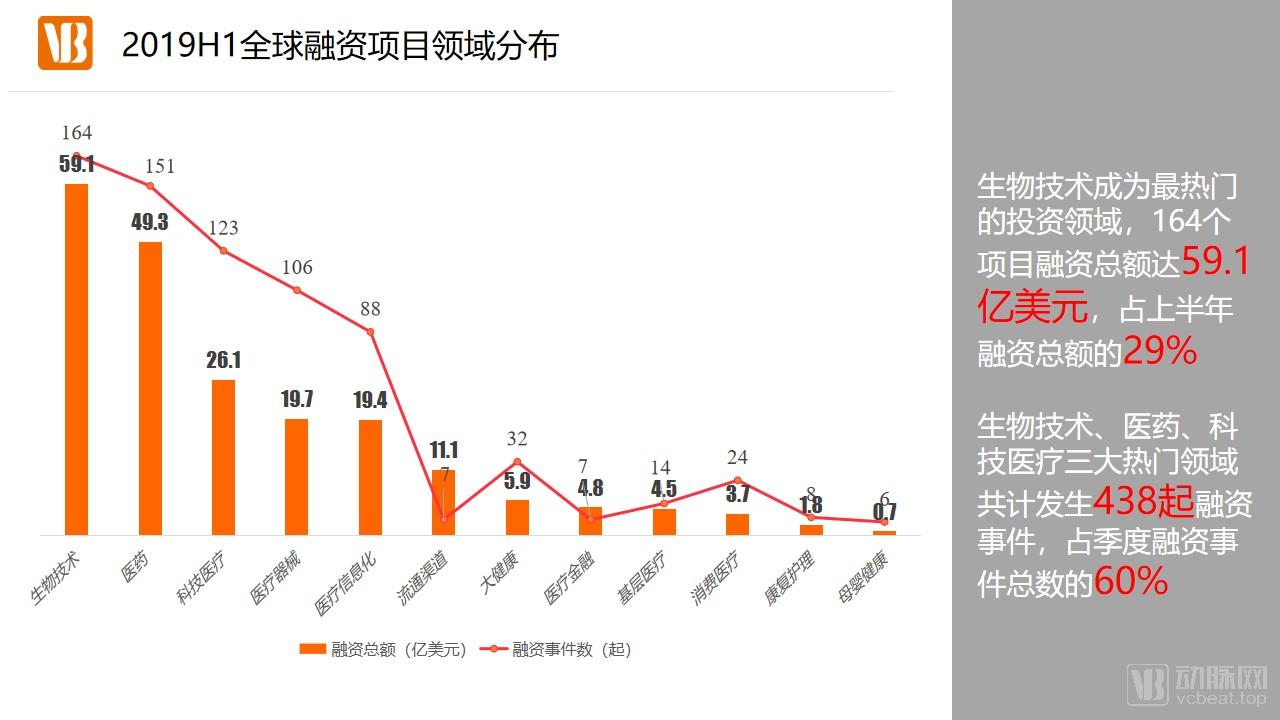

(2) The biotechnology sector, represented by regenerative medicine, genetic engineering, and biomaterials, secured $5.91 billion in investment, ranking first.

(3) The proportion of repeat investors in fields such as pharmaceuticals and medical devices is higher than that of new investors, indicating that these sub-sectors are gradually entering a mature stage.

(4) The number of projects with domestic financing amounts exceeding USD 100 million increased by 80% year-on-year; these projects are highly likely to become future unicorns in the healthcare industry.

(5) The number of Series A financing rounds has become a key indicator for hot sectors, with the top four hottest sectors in China all having the highest number of Series A deals.

(6) The continuous rise in the amount of single-round financing for domestic projects indicates that corporate innovation costs are increasing, necessitating greater capital investment to drive innovation initiatives.

VCBeat collected data on 163 healthcare companies listed over the past five years on the A-share, Hong Kong Stock Exchange, U.S. stock markets, and other securities exchanges. The analysis revealed that pharmaceutical companies accounted for the largest number of listings, with a total of 78 firms, representing nearly 50% of the sample.

IPO Landscape of Healthcare Companies (2015–H1 2019)

Among them, there are as many as 60 biopharmaceutical companies, a growth primarily driven by policy incentives within China. The Hong Kong Stock Exchange’s new regulations introduced in 2018 stated that “biotechnology and life sciences companies could go public even without revenue,” which prompted a wave of biopharmaceutical and biotech firms—including Innovent Biologics, Hua Medicine, Ascletis Pharma, Fosen Pharmaceutical, and Junshi Biosciences—to complete their listings in Hong Kong in 2018. Under the continued influence of these new policies, the Hong Kong Stock Exchange saw additional biopharmaceutical listings in the first half of 2019, including CStone Pharmaceuticals, CanSino Biologics, Viva Biotech, Mabpharm, and Hansoh Pharmaceutical.

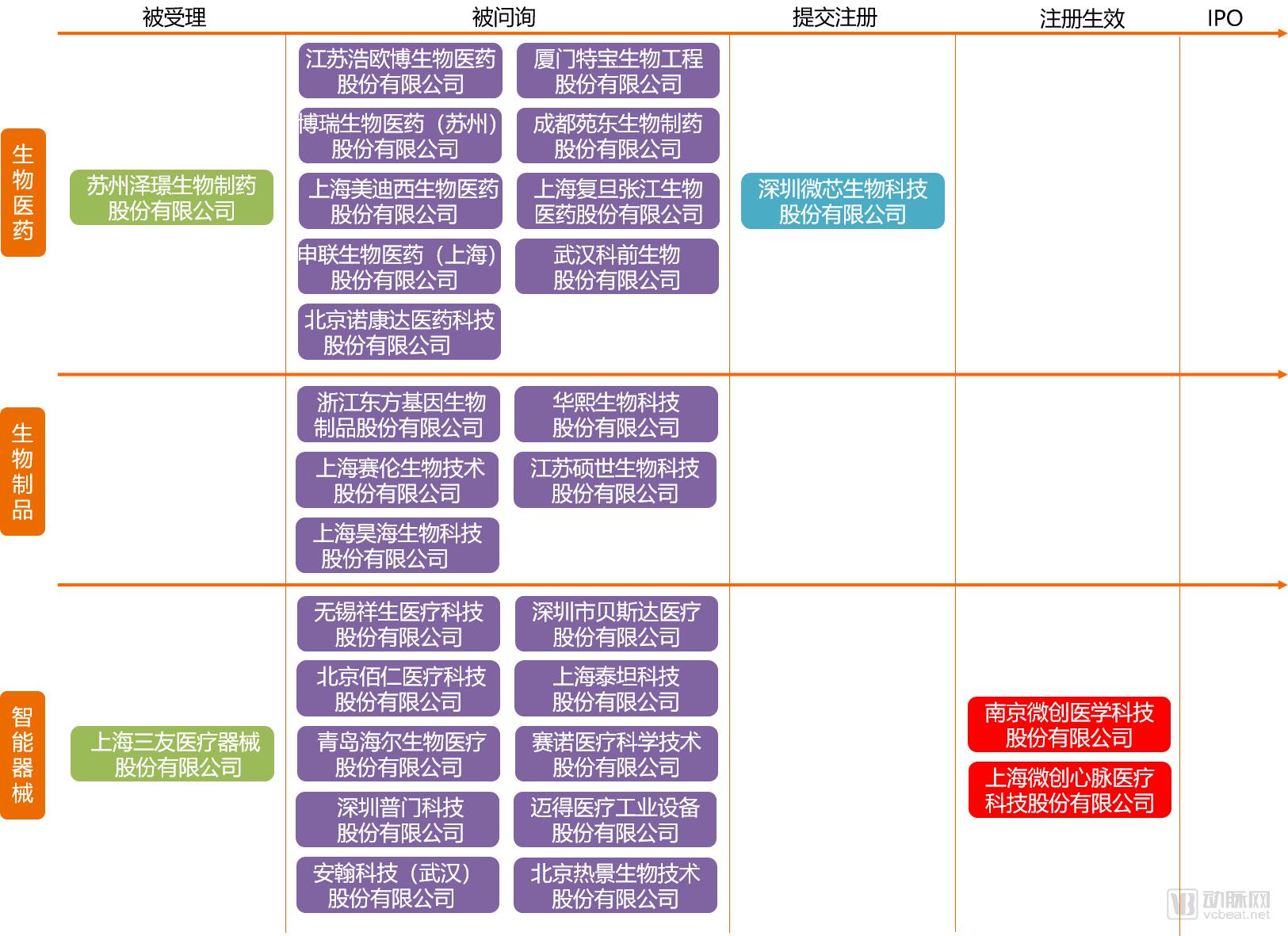

Furthermore, on January 30, 2019, the China Securities Regulatory Commission (CSRC) released the “Implementation Opinions on Establishing the STAR Market on the Shanghai Stock Exchange and Piloting the Registration-Based IPO System.” As a priority sector for the STAR Market, the biopharmaceutical industry has seen an accelerated pace of related companies seeking listings on this board. VCBeat has compiled the IPO application status of these companies on the STAR Market (as of July 3, 2019).

STAR Market Application Status of Healthcare Companies

Based on the dynamics of STAR Market projects, 16 companies engaged in biopharmaceuticals or biological products have entered the approval pipeline for the STAR Market. Shenzhen Chipscreen Biosciences Ltd. has submitted its registration application and is poised to receive listing approval.

Chipscreen Biosciences, established in 2001, is primarily engaged in the research and development of innovative small-molecule drugs. Its core technology features an integrated drug innovation and early evaluation system based on chemogenomics, which has successfully led to the discovery and development of three first-in-class novel drugs and a series of new molecular entity candidates. Its Class I first-in-class novel drug, Chidamide (brand name: Epidaza), has been launched for the treatment of peripheral T-cell lymphoma and is the world’s first subtype-selective histone deacetylase (HDAC) inhibitor. Prior to submitting its listing application to the STAR Market, the company completed seven rounds of financing, with investors including Lilly Asia Ventures, CCB Capital, Shenzhen Capital Group, China Merchants Bank International, and other prominent investment institutions.

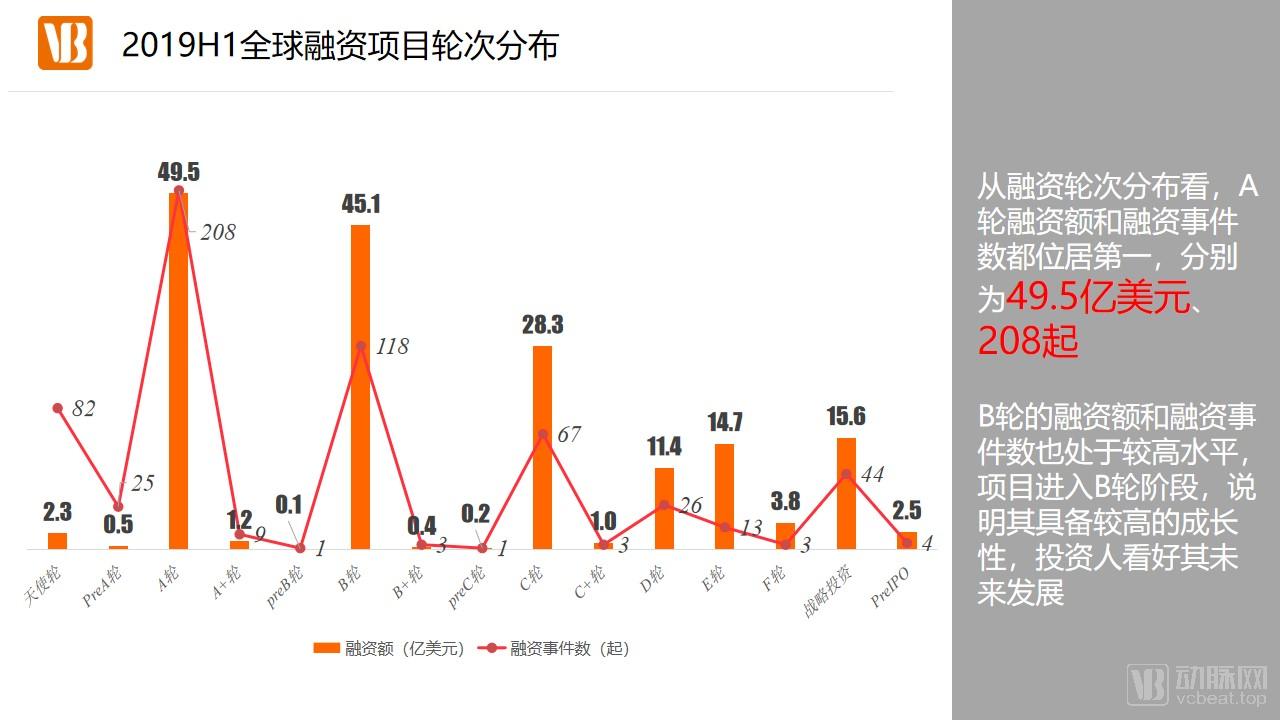

In terms of funding rounds for projects in the first half of 2019, Series A had the highest number of deals, accounting for 2%, and the total funding amount for Series A projects reached $4.95 billion, making it the round with the highest total funding.

Series A funding is generally regarded as the watershed moment for a project’s entry into the maturity stage. A large number of Series A projects indicates that an increasing number of ventures are transitioning into maturity, significantly reducing the risk of early failure and making them more likely to attract capital interest in later stages.

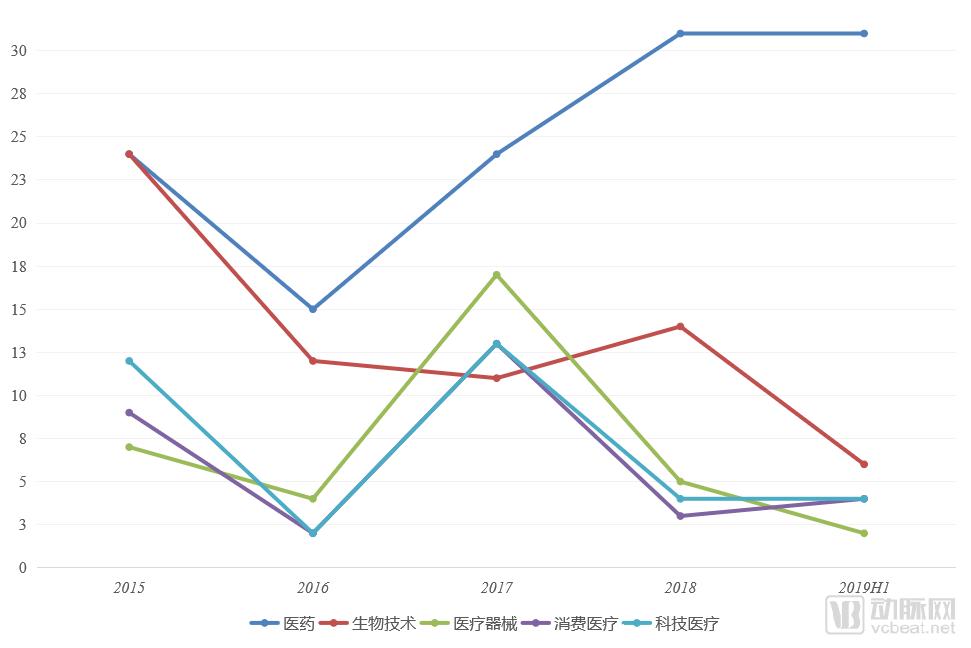

Biotechnology remains the hottest investment sector in the capital market. Unlike in the past, regenerative medicine has emerged as a highlight within the biotechnology field, giving rise to representative companies such as Kerecis, Orthocell, and TissueTech. Regenerative medicine refers to medical practices that restore or establish original functions by replacing or regenerating human cells, tissues, or organs, with a strong emphasis on the “3Rs”: replacement, repair, and regeneration. The four key components of regenerative medicine are cells, biomaterials, signaling molecules, and bioreactors.

Kerecis, founded in 2009 and headquartered in Reykjavik, Iceland, is a medical technology company dedicated to tissue regeneration therapies using fish skin. Orthocell, an Australian company, is a medical enterprise committed to improving the lives of patients with tissue injuries, providing innovative approaches for the regeneration of tendons, cartilage, and soft tissues. TissueTech, headquartered in Florida, USA, is an innovative company focused on delivering novel tissue regeneration solutions for the treatment of ophthalmic conditions, musculoskeletal injuries, wound care, and other diseases.

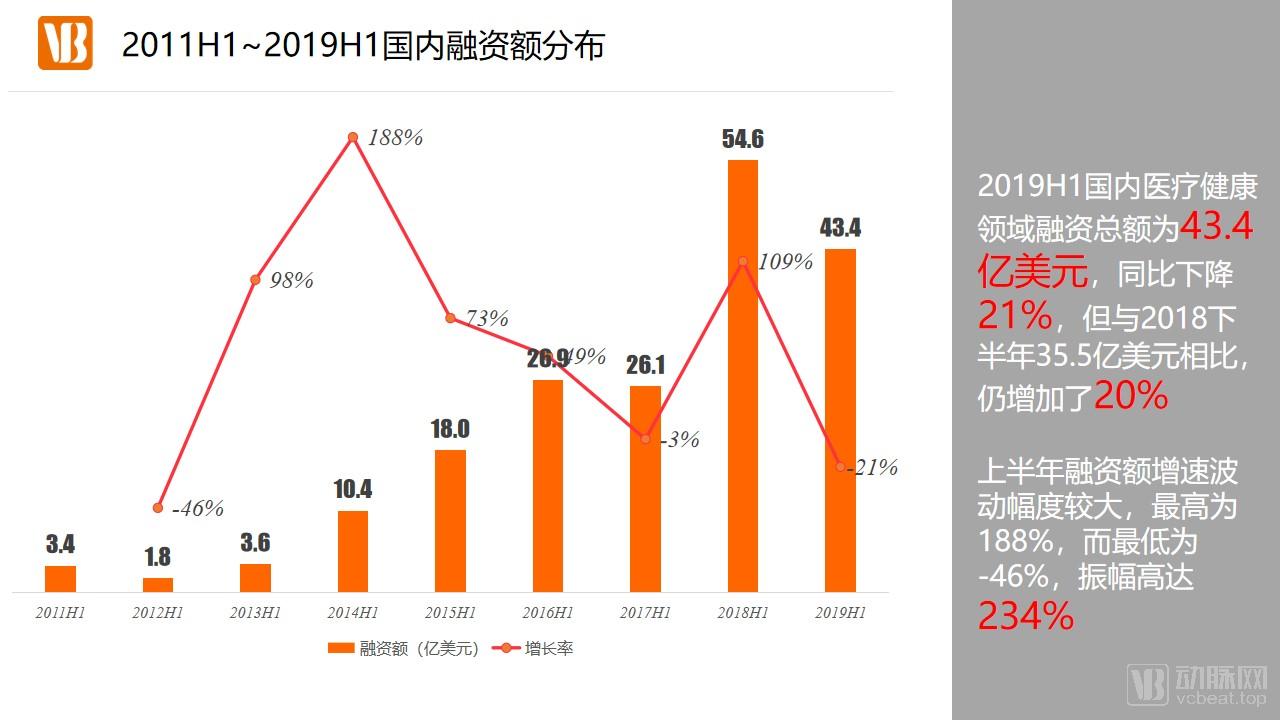

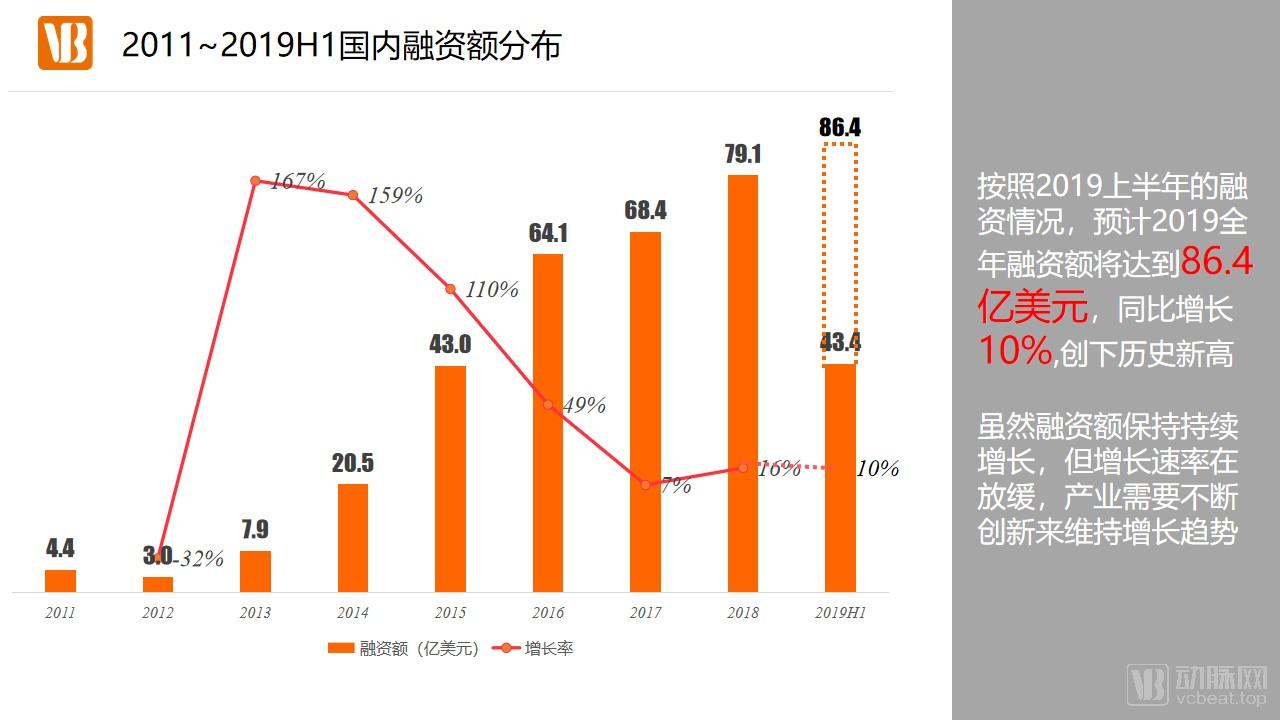

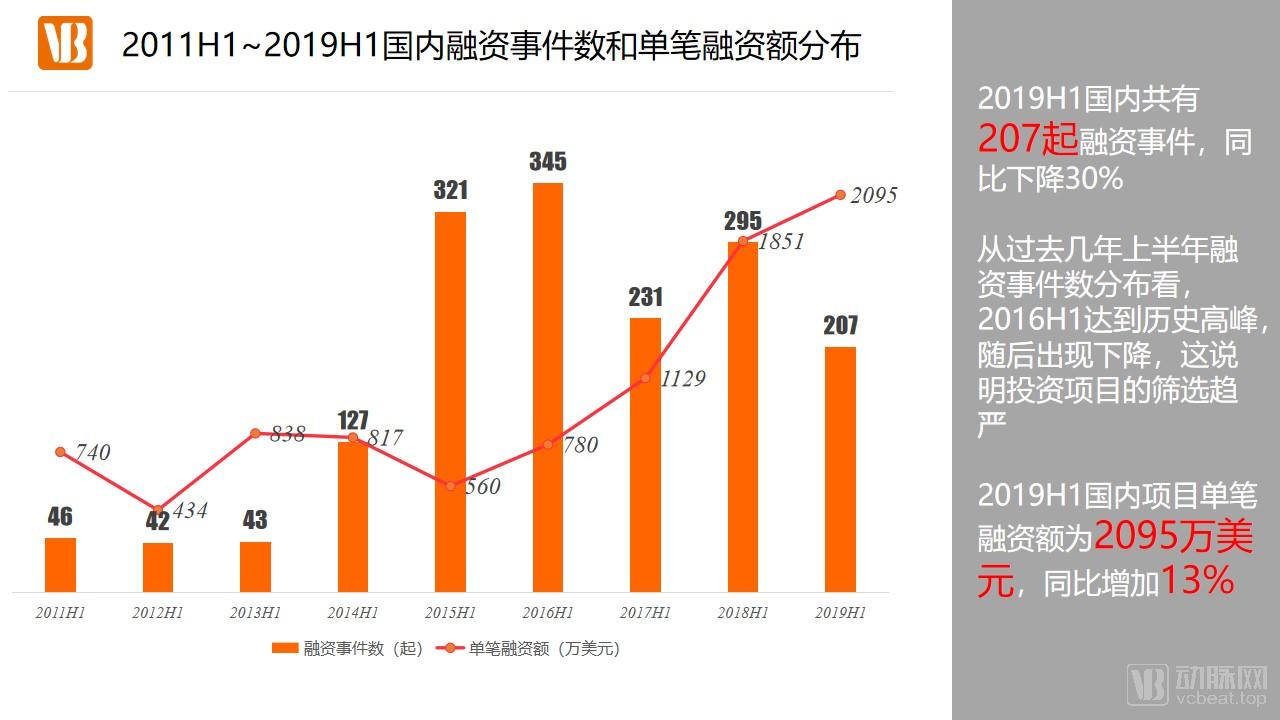

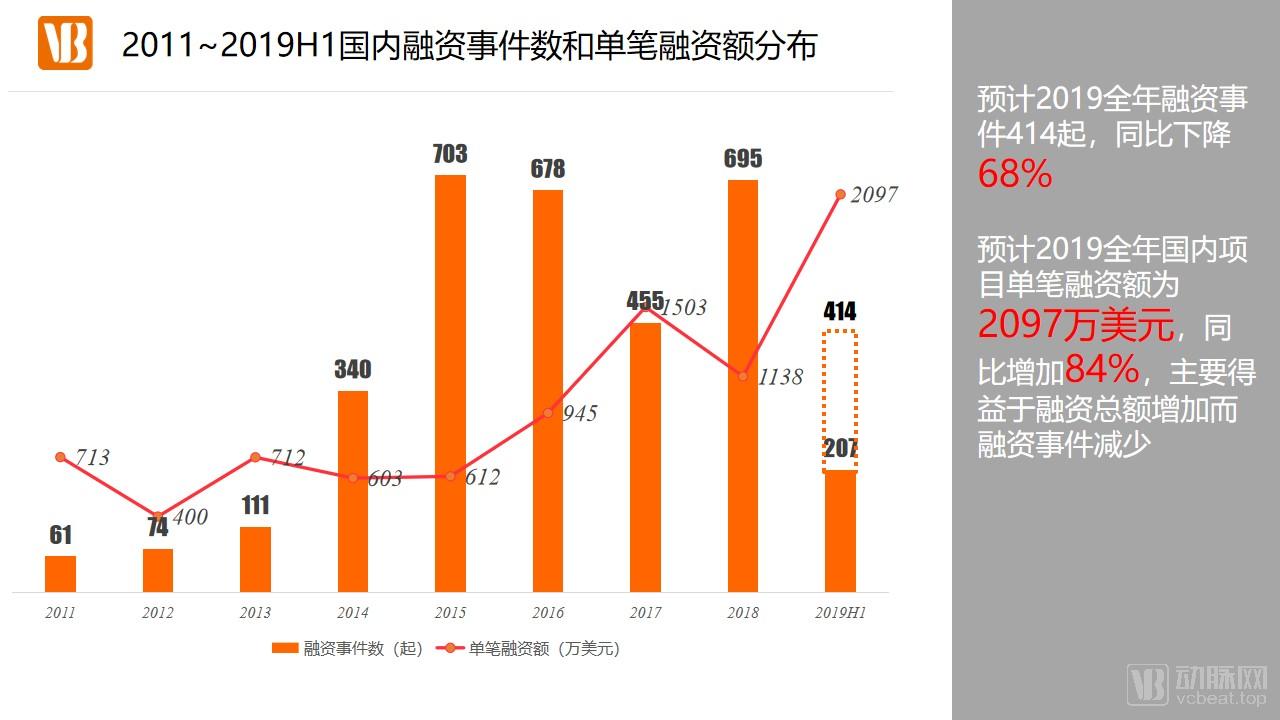

In the first half of 2019, there were a total of 207 financing events in China, with a total financing amount of $4.34 billion. Based on this, the full-year financing amount for 2019 is projected to reach $8.64 billion, representing a 10% year-on-year increase and setting a new historical high. This indicates that the investment and financing market for China’s healthcare industry is aligned with global trends and continues to grow.

In terms of single-round financing amounts, 2019 is set to hit a record high. This is partly due to the decline in the number of financing deals, but also attributable to the emergence of large-scale financing rounds, such as JD Health (over $1 billion) and Penguin Almond Group ($250 million).

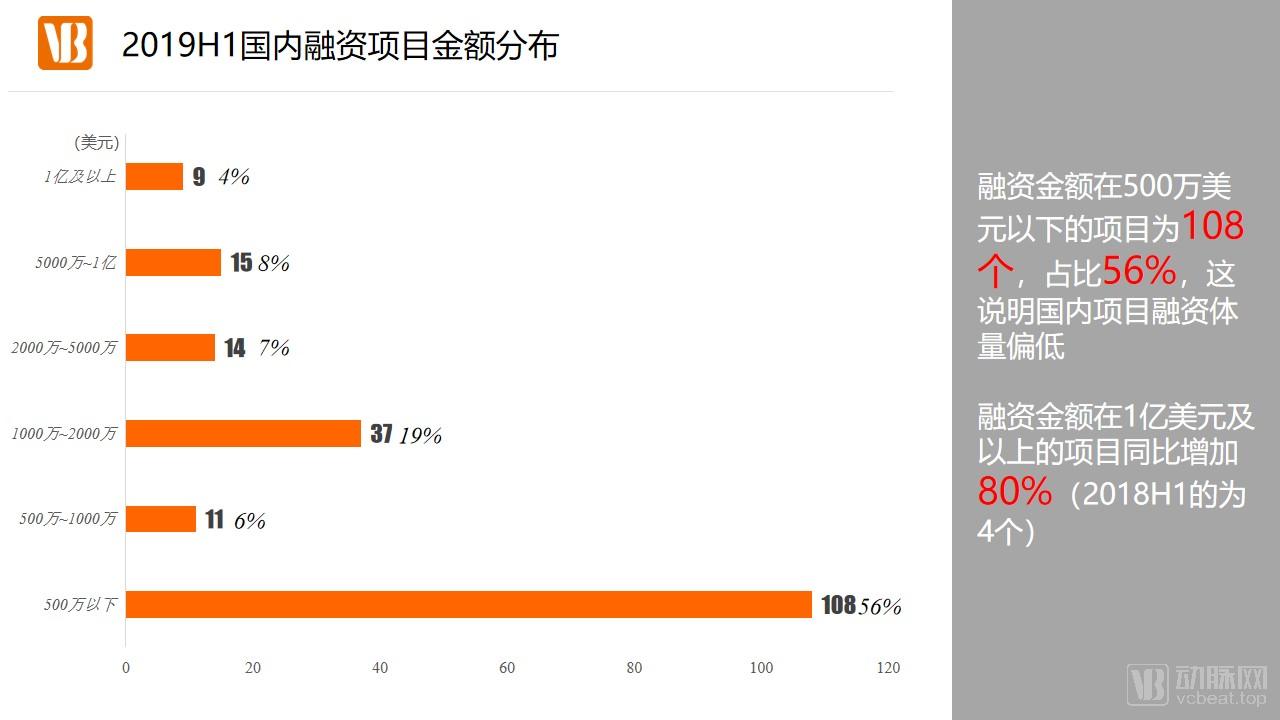

Domestic projects generally have relatively low financing volumes, with 56% of them raising less than $5 million. Startups need to enhance their technological innovation and business model innovation capabilities to demonstrate significant market potential and superior investment returns to investors, thereby securing substantial funding.

Encouragingly, the number of projects in China that secured over $100 million in financing during the first half of the year increased by 80% year-on-year, indicating the emergence of star enterprises in certain niche sectors. These companies are poised to join the ranks of healthcare unicorns and become a core force driving medical innovation.

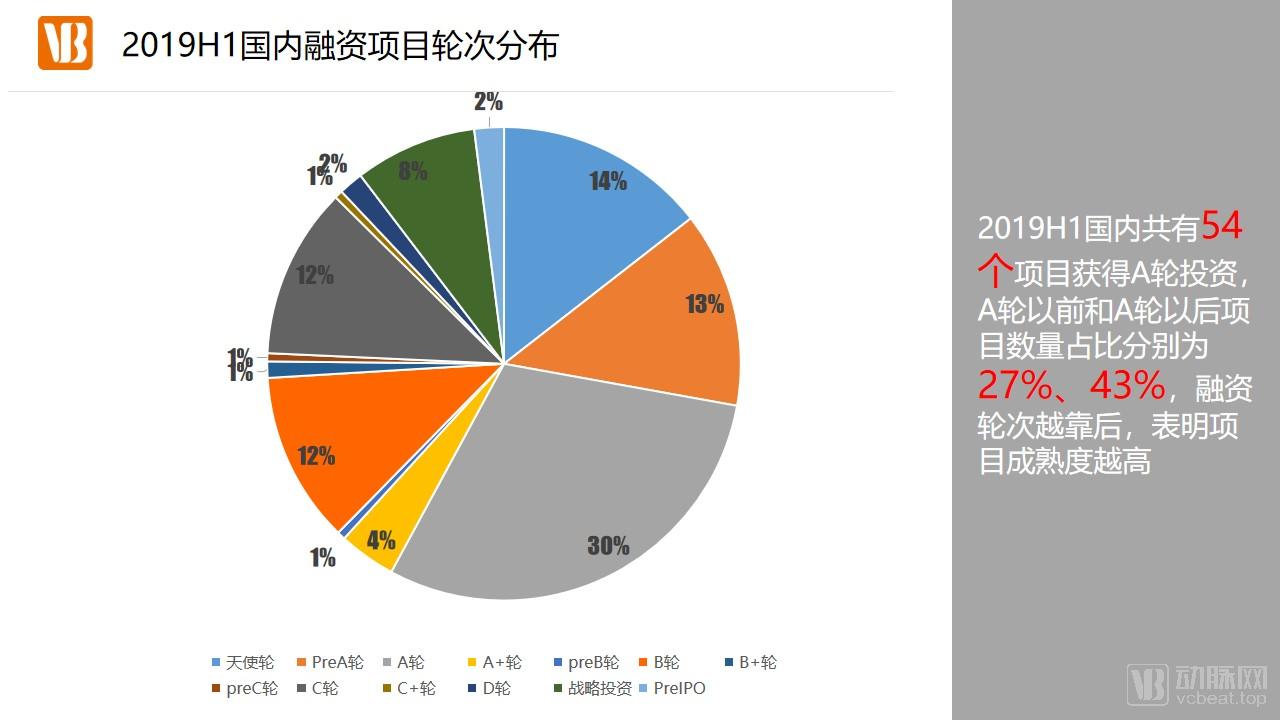

The distribution of project financing rounds in China is converging with global trends, with Series A rounds being the most frequent. This also indicates that the scale of projects entering the mature stage in China is expanding. JD Health’s Series A financing round, exceeding $1 billion, became the focal point of the healthcare industry in the first half of the year.

In addition, the proportion of Series B and Series C financing events each exceeds 10%. Early-stage financing rounds are primarily driven by venture capital (VC) firms, while later stages are predominantly led by private equity (PE) firms. These investors focus on the company’s later-stage development and become more actively involved in management and operations to accelerate corporate growth.

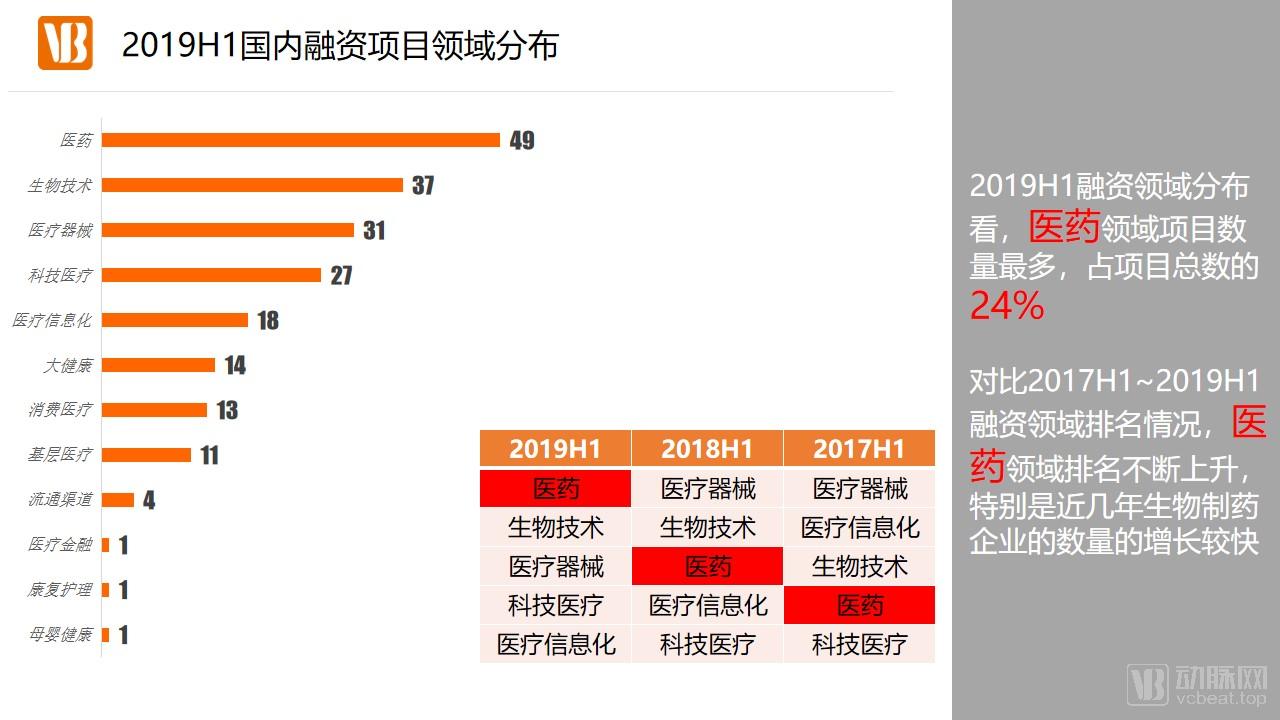

A comparison of the top five hot sectors over the past three years reveals a steady rise in the ranking of the pharmaceutical industry, which became the sector with the highest number of domestic financing deals in the first half of the year. This trend is primarily driven by heightened investment enthusiasm in the pharmaceutical sector, spurred by financing activities among biopharmaceutical companies.

As traditional methods for new drug development become increasingly challenging, with rising R&D costs and declining success rates, many pharmaceutical companies are actively entering the field of biopharmaceuticals. By leveraging biotechnologies such as genetic engineering, cell engineering, fermentation engineering, enzyme engineering, and biochip technology, these companies are advancing biomedical research and development to treat complex and diverse cancers and rare diseases. According to the “Report on the Epidemiology of Malignant Tumors in China” released by the National Cancer Center, there are 3.929 million newly diagnosed cases of malignant tumors in China each year. The development of biopharmaceuticals will undoubtedly bring significant benefits to cancer patients.

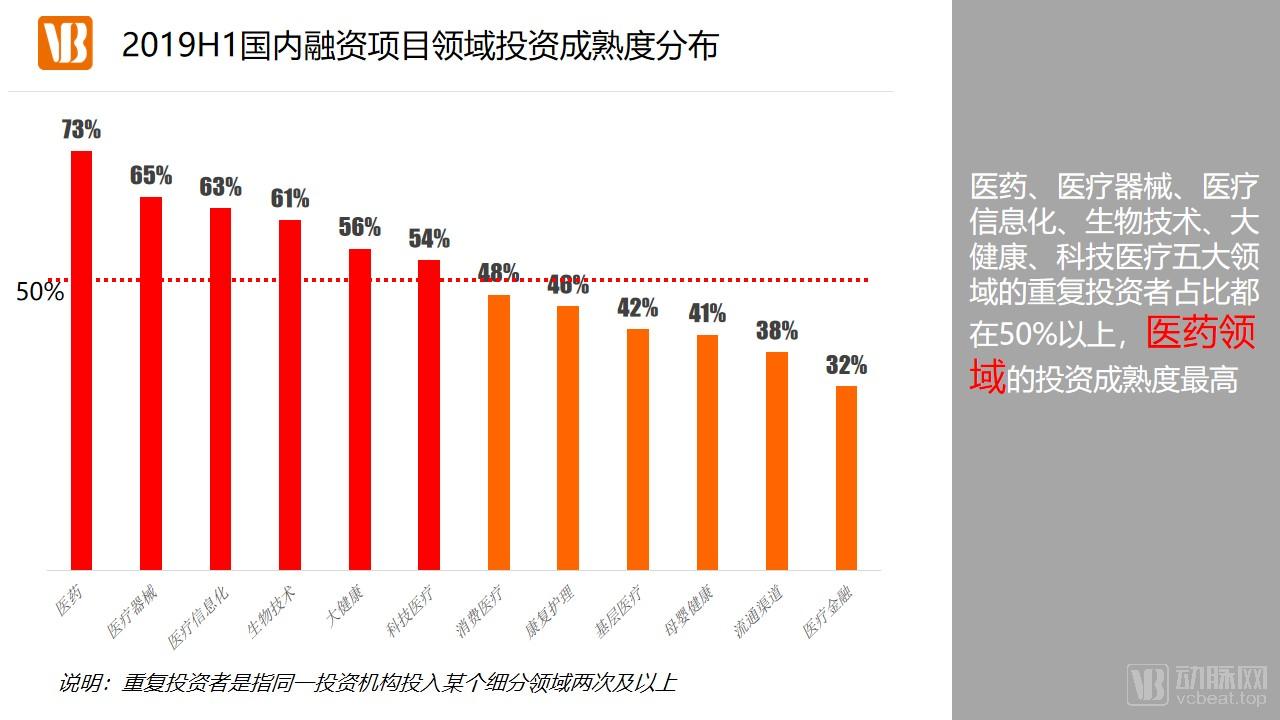

Unlike previous investment and financing reports, we have added an analysis of the investment maturity in each sub-sector. By calculating the proportion of repeat investors in each sub-sector, we use this as an indicator to judge its investment maturity. That is, the higher the proportion of repeat investors in a certain sub-sector, the higher the investment maturity of that sector.

The proportion of repeat investors exceeds 50% across six sectors: pharmaceuticals, medical devices, healthcare informatization, biotechnology, general health, and tech-enabled healthcare. In the pharmaceutical sector, in particular, the share of repeat investors reaches as high as 73%. This is primarily because the pharmaceutical industry chain is highly mature, with relatively clear timelines for each stage. Consequently, compared to other subsectors, the payback period and return on investment in the pharmaceutical field are more predictable, thereby encouraging institutional investors to engage in repeated investments.

The number of Series A financing rounds has become a hallmark of hot sub-sectors, with the top four hottest sub-sectors in China all ranking highest in Series A deal volume. As previously noted, Series A financing serves as a watershed moment for projects entering the maturity stage. Securing Series A funding indicates that institutional investors have validated the project’s commercial viability. This endorsement from institutional investors inevitably attracts greater attention from other investors to the sector, thereby fueling its status as an investment hotspot.

Beijing remains the top city for capital attraction, accounting for 26% of the total with 54 financing events in the first half of the year. However, there is a mismatch between popular cities and popular sectors: pharmaceutical financing activities mainly occurred in Shanghai and Jiangsu rather than Beijing, which is related to local industrial development policies and the growth of key industrial parks. In the fields of biotechnology and medicine, Zhangjiang in Shanghai and Suzhou in Jiangsu have become domestic hubs for development.

For instance, as early as 2009, Shanghai proposed the establishment of six major biopharmaceutical industry development bases: constructing biopharmaceutical R&D, clinical research organization (CRO), and industrial bases in Pudong’s Zhangjiang–Zhoukang area, Minhang, and Xuhui; and building biopharmaceutical industrial bases in Fengxian, Jinshan, and Qingpu. After ten years of development and operation, these areas have attracted a large number of innovative biopharmaceutical companies.

Jiangsu has also prioritized the biopharmaceutical industry as a key development focus. A number of industrial parks, including the Nanjing Medical and Health Industrial Park, Jiangsu Binhai Pharmaceutical Industrial Park, Suzhou BioBAY, and Changshu Suyu Biopharmaceutical Industrial Park, have attracted a large number of biopharmaceutical enterprises, thereby driving the growth of Jiangsu’s biopharmaceutical sector.

On May 10, 2019, JD.com announced its first-quarter 2019 financial results and formally established JD Health as a subsidiary group. As the sole subsidiary under JD.com dedicated to comprehensive health-related businesses, JD Health will leverage the parent company’s capabilities and resource advantages. Building on its existing core strengths in medicine and pharmaceuticals, and based on four key business segments—pharmaceutical retail, pharmaceutical wholesale, internet healthcare, and Healthy Cities—JD Health will further expand and deepen its footprint in the “Internet + Healthcare” industry through data- and technology-driven smart healthcare solutions. JD Health is also poised to become the third mega-unicorn cultivated by JD.com, following JD Digits and JD Logistics.

As a leading non-public healthcare service platform in China, Penguin-Almond Group has established the country’s largest network of high-quality chain clinics following the merger of its two major brands, Penguin Doctor and Almond Doctor, in August 2018. Its offline footprint comprises nearly 50 clinics across eight cities—Beijing, Shanghai, Shenzhen, Chengdu, Shenyang, Guangzhou, Hong Kong, and Nanjing—covering various formats including general practice clinics, ambulatory surgery centers, and specialty clinics. The online platform boasts resources connecting over 440,000 certified physicians and 10 million patients, while linking to more than 30,000 hospitals. This round of financing was co-led by Country Garden Venture Capital, Tencent, and Gaw Capital Partners, with participation from CMB International, Harvest Wealth Management, the China-Russia Investment Fund, Sequoia China, Shengshijing Group, and AVIC Trust. The funds raised will be primarily dedicated to continuously building an integrated online-to-offline (O2O) one-stop comprehensive healthcare service platform and health management system under the Penguin-Almond brand.

Allist Pharmaceuticals, founded in 2004 and headquartered in the Zhangjiang Hi-Tech Park in Shanghai, has established R&D pipelines in major disease areas including hypertension, diabetes, and oncology. The company has filed more than 50 patent applications domestically and internationally and submitted multiple new drug applications. This round of financing was led by Shiyu Capital, with participation from Zhengxingu Innovation Capital, Sifanghe, Gongqingcheng Hanren, Yuansheng Venture Capital, Gaoke Xinjun, Gaoke Xinchuang, SDIC Chuanghe, Deyi Capital, Huaxin Century Investment, and Qianlong Capital. The funds raised will be primarily used to advance the subsequent clinical development of the core product furmonertinib mesylate, accelerate its commercialization, and promote overseas collaborations.

Haihe Biopharma, founded in 2011 in Zhangjiang Science City, Shanghai, is dedicated to the discovery, development, and commercialization of innovative oncology drugs. On February 11, 2019, the company announced the completion of a $146.6 million financing round, led by Huagai Capital, with participation from Yingke Capital, CSPC Pharmaceutical Group, Hillhouse Capital, CAS Venture Capital, Liansheng Venture Capital, Boyuan Capital, Caijin Capital, and Dalian Pharma. The company has established a preclinical drug evaluation technology platform and a clinical research system encompassing units for drug synthesis, quality research, formulation studies, pharmacological and efficacy evaluation, biomarker discovery and validation, medical strategic planning, and clinical trials. It currently has 10 compounds in clinical development and 5 in preclinical stages, nine of which are novel original drugs.

Shuidi Inc. was founded in 2016 by Shen Peng, co-founder of Meituan Waimai. Currently, Shuidi has over 600 million registered users and 250 million independent paying users. Leveraging the WeChat ecosystem, it has established three core business segments: Shuidi Chou (crowdfunding), Shuidi Huzhu (mutual aid), and Shuidi Bao (insurance). This round of financing was led by Boyu Capital, with participation from prominent investors including Tencent, CICC Capital, and Gaorong Capital. The company will vigorously expand its health insurance and health protection businesses, such as the Shuidi Insurance Mall and Shuidi Mutual Aid, to create a service model for health insurance and health protection that offers a superior user experience.

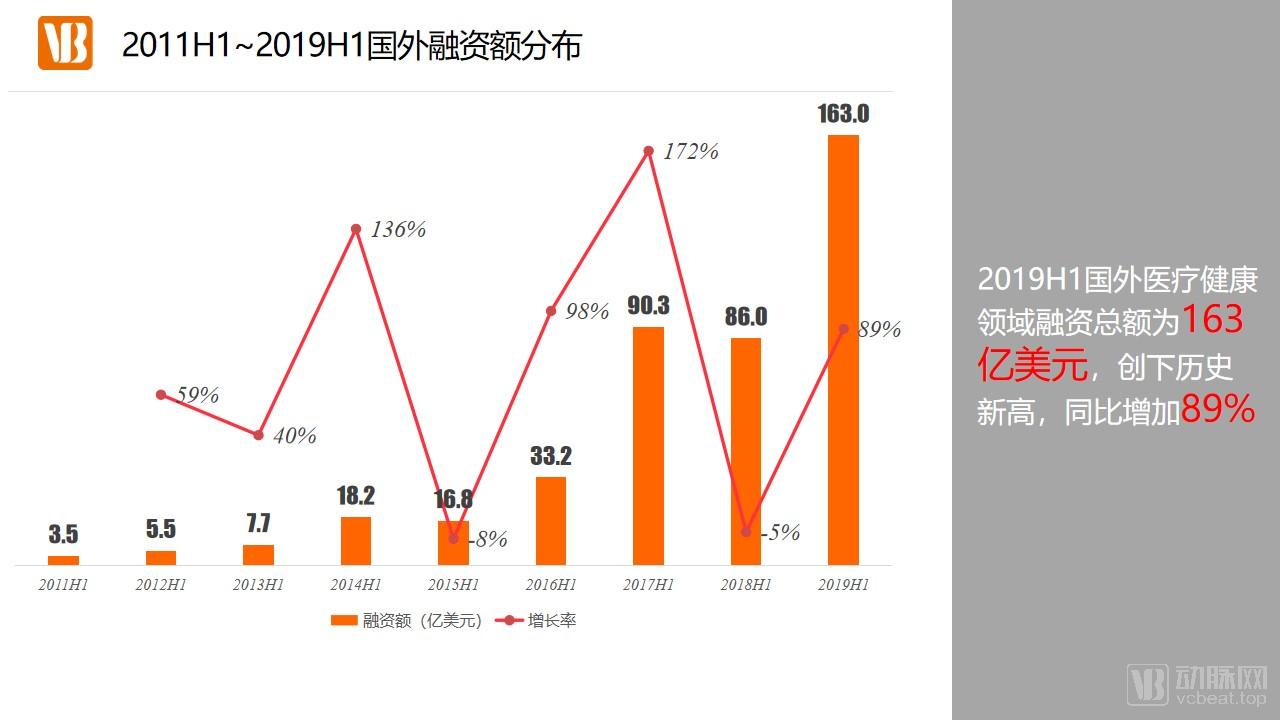

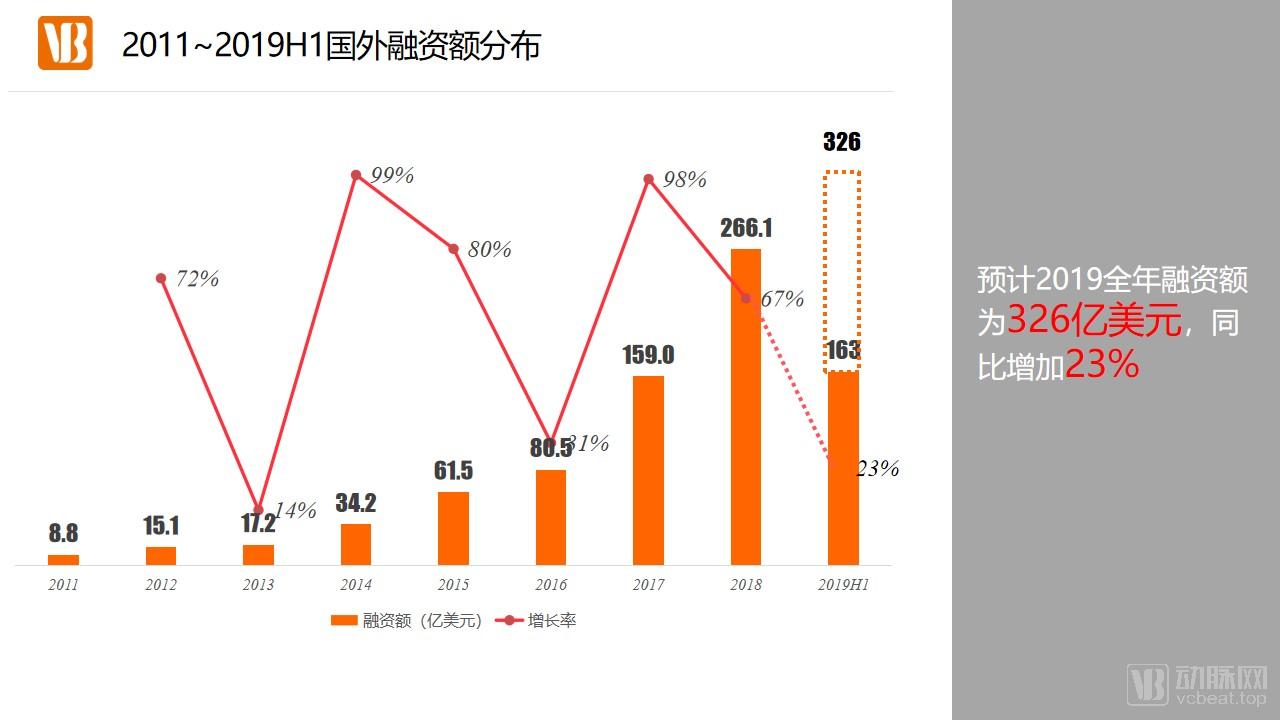

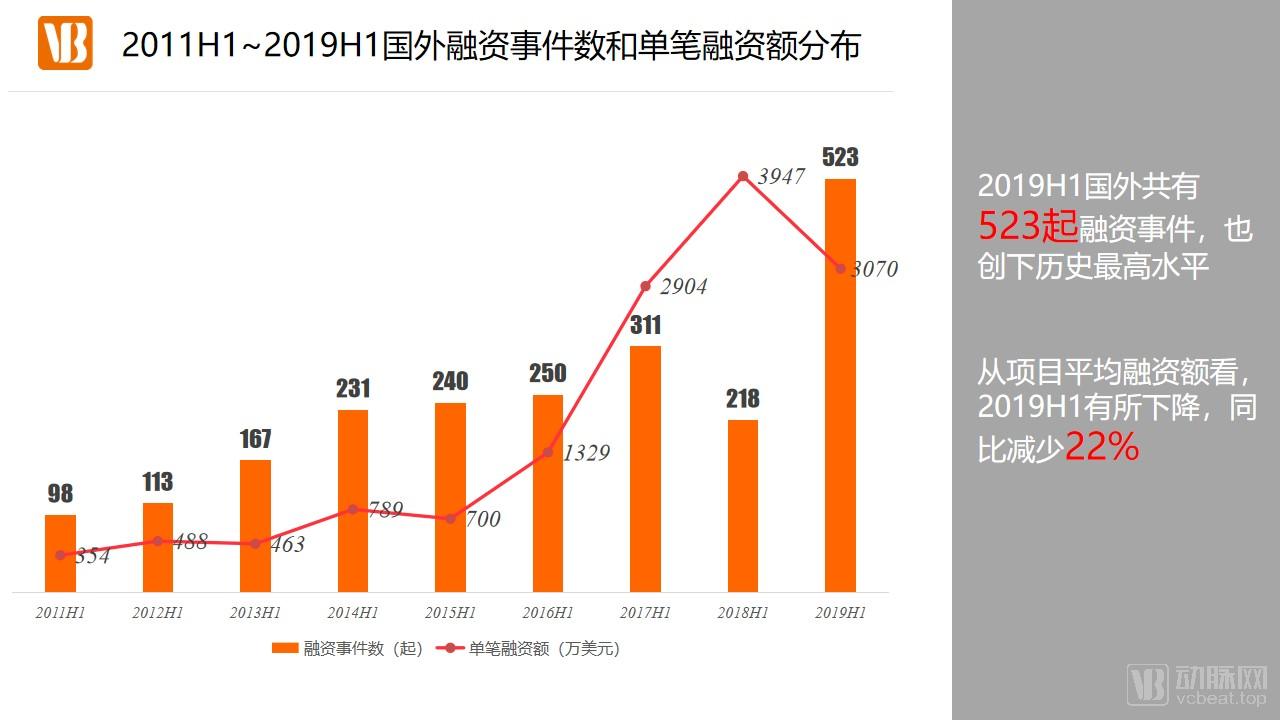

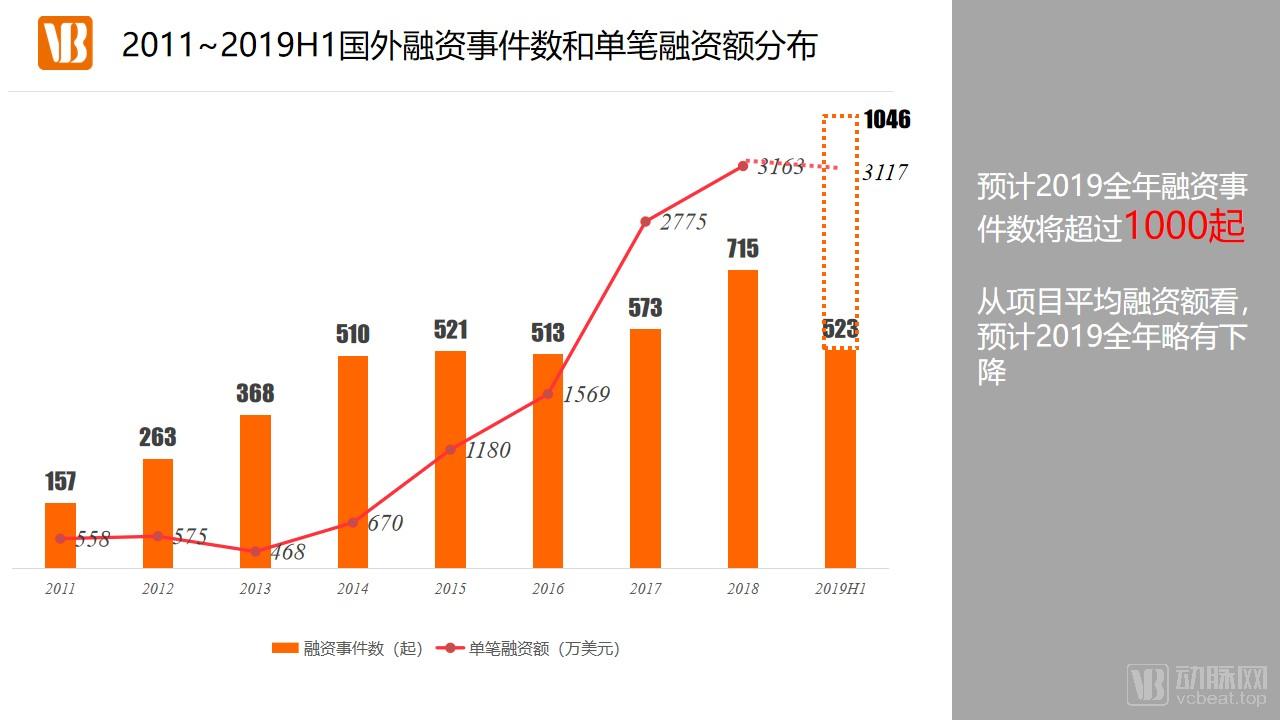

In the first half of 2019, overseas financing reached $16.3 billion, a year-on-year increase of 89%. For the full year of 2019, it is projected to rise by 23% year-on-year to $32.6 billion, indicating that the global healthcare industry will maintain sustained growth.

In the first half of 2019, there were 523 financing deals in the overseas healthcare and medical industry, indicating a high level of investment and financing activity. The total number of financing deals for the full year of 2019 is projected to exceed 1,000. Despite a cooling global venture capital environment, investment and financing in the healthcare and medical sector remained robust. These 523 financing deals reached a new high of $16.3 billion, demonstrating that the healthcare and medical industry continues to be favorably viewed by institutional investors as a long-term opportunity, with increased investment commitments even amid unfavorable macroeconomic conditions.

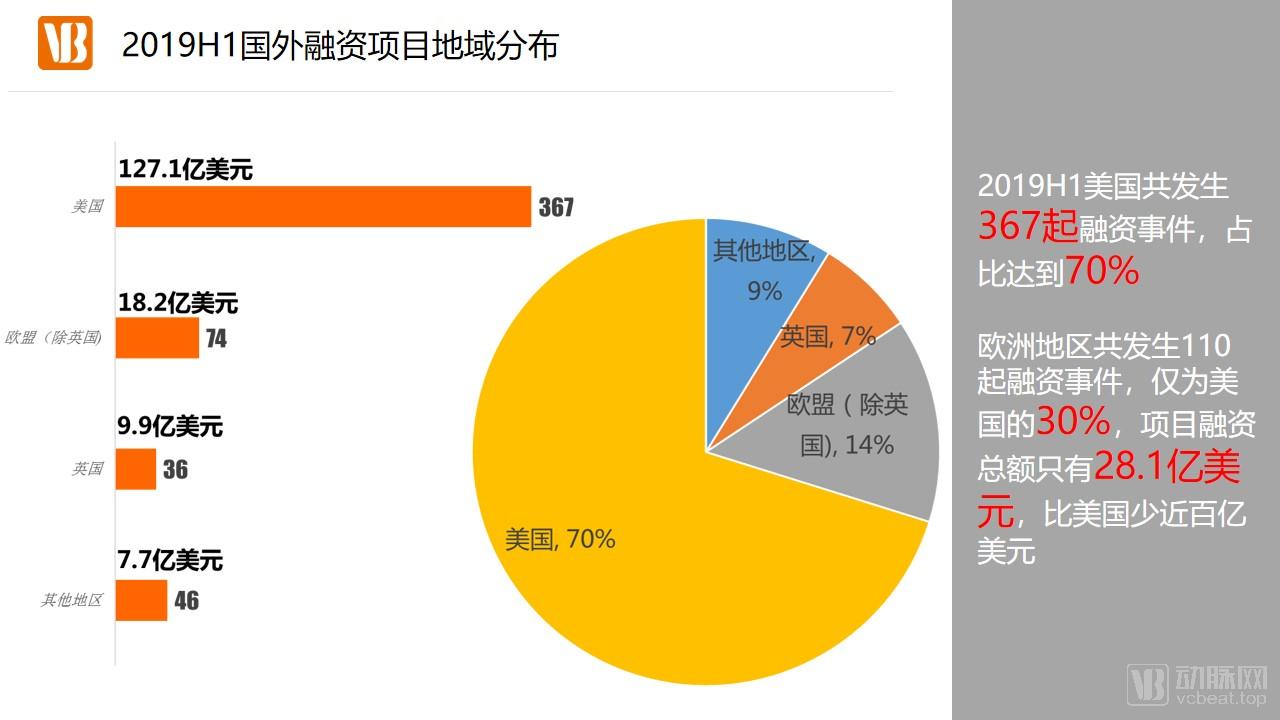

Global healthcare investment and financing remain active, with the United States playing a pivotal role. In the first half of the year, the U.S. accounted for 367 financing deals, representing 70% of the total. As a hub for innovative enterprises and venture capital firms, the U.S. sees the emergence of numerous outstanding startups annually, driving the growth of the venture capital market. Although Europe recorded fewer financing deals than the U.S., its deal count increased by 86% year-over-year, sustaining strong investment momentum in the healthcare sector.

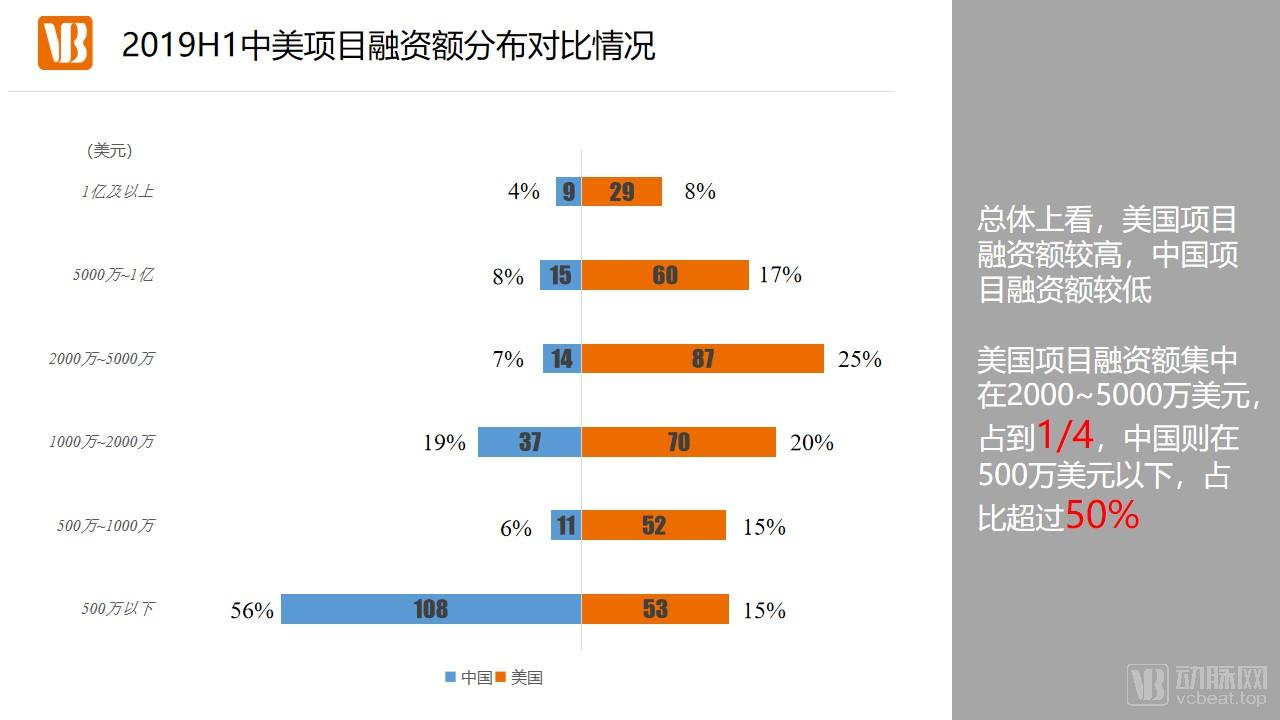

A significant gap remains in the scale of project financing between China and the United States. In the U.S., financing amounts are predominantly concentrated in the $20–50 million range, whereas in China, they are mostly below $5 million. Moreover, the number of projects with financing exceeding $100 million is twice as high in the U.S. as in China.

The size of a project’s financing depends not only on the project’s own circumstances but also on the investment style of the investing institutions. Foreign investment firms typically have longer investment horizons than their domestic counterparts, generally exiting only when the company goes public or is acquired. In contrast, domestic investment firms tend to have shorter holding periods; those participating in early-stage funding rounds often choose to cash out in later rounds.

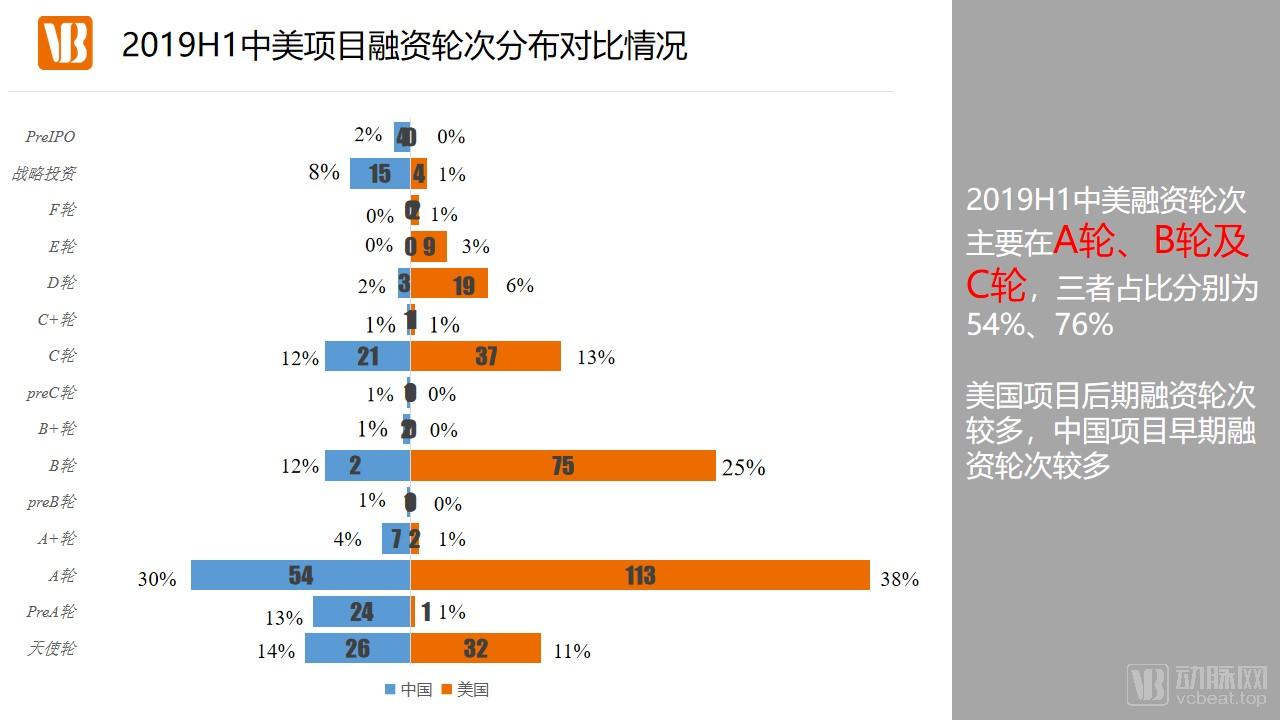

The concentration of financing rounds for projects in China and the United States is consistent, primarily distributed across Series A, Series B, and Series C. However, from an overall perspective, U.S. projects have more late-stage rounds, involving Series E, Series F, and beyond, while Chinese projects have more early-stage rounds, such as Pre-A, Pre-B, and Pre-C. This also indicates that domestic investment institutions are more focused on early-stage investments, whereas U.S. investment institutions, in addition to early-stage investments, also value participation in late-stage project investments.

The Top 5 hottest sectors in China and the United States are identical, dominated by pharmaceuticals, biotechnology, medical devices, digital health, and healthcare informatics. This reflects the mainstream development direction of the global healthcare industry and the flow of venture capital investment. However, biotechnology is the hottest sector in the United States, whereas pharmaceuticals command the highest level of interest in China.

The hottest sectors in the two countries differ, primarily due to different emphases in sector classification. In China, most biotechnology companies have drug development pipelines and launch corresponding biologics; therefore, they are categorized under the broader pharmaceutical sector. In contrast, the United States has a large number of biotechnology service providers that specialize in offering biological technical services for pharmaceutical R&D without directly manufacturing drugs; thus, they are classified under the biotechnology sector.

An analysis of investment and financing data in the healthcare industry for the first half of 2019 reveals that, against the backdrop of a cooling global venture capital market, enthusiasm for investing in the healthcare sector has not waned but instead intensified. The relatively large number of listed companies in the biopharmaceutical sector is primarily attributable to its representation of the development direction of the healthcare industry and its broad market prospects; increased government support has further sustained capital market attention to this field. Biotechnology companies specializing in regenerative medicine, genetic engineering, and biomaterials are poised to become the future stars of the venture capital market, with the potential to emerge as unicorns in the healthcare industry under the impetus of capital investment.

However, the healthcare industry has maintained a high level of investment enthusiasm in recent years, attracting substantial venture capital. Whether an “industry investment bubble” will emerge and inflict damage on the growing healthcare sector remains to be seen; we will await further developments and validate our assessment with data.

Long-press to scan the QR code of the mini-program below to receive the “2019 H1 Healthcare Industry Investment and Financing Report” free of charge.