StartUp Health H1 2019 Report: Healthcare Services Emerge as Top Investment Focus Across 11 Medical Subsectors

2019 was defined by StartUp Health as “The Year of the Patient.” Patients have always been the soul of the healthcare revolution. In the vast healthcare landscape, patients are the true investors; our patients are weary of a care system that prioritizes quantity over quality.

This year, we have observed shifts in capital flows within the healthcare sector: Penguin Almond Group invested $250 million to enhance medical care services for patients in China and allocated $100 million to advance testing services tailored to specific patient populations. Total fundraising in the healthcare sector reached $680 million this year, with women’s healthcare recording the highest growth rate in funding during the same period, representing a 68% increase compared to last year.

All signs indicate that investors are looking to support companies that can improve care for underserved populations.

VCBeat (WeChat ID: vcbeat) has compiled the financing and investment data for 11 sub-sectors of the healthcare industry in the first half of 2019, based on StartUp Health’s semi-annual report.

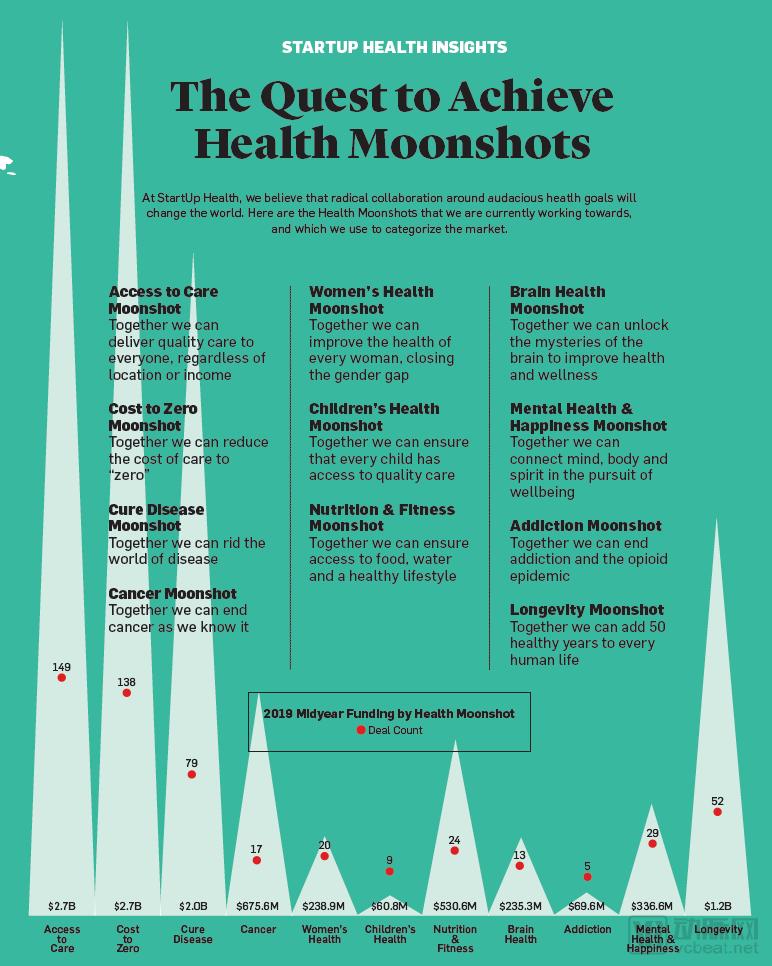

Chart of Transaction Volumes Across 11 Subsectors in the Healthcare Industry

The 11 healthcare subsectors that secured financing in 2019 were: Access to Care, Cost to Zero, Cure Disease, Cancer, Women’s Health, Children’s Health, Nutrition & Fitness, Brain Health, Mental Health & Happiness, Addiction, and Longevity.

Among these, “Healthcare Service Accessibility” and “Zero-Cost Care” recorded significantly higher transaction volumes and values than other healthcare subsectors, emerging as the top two hottest fields in the first half of the year. In the first half of 2019, the “Healthcare Service Accessibility” sector completed 149 transactions, with a total value reaching $2.7 billion; “Zero-Cost Care” saw 138 transactions, also amounting to $2.7 billion.

Among these 11 sub-sectors, the slowest performers in the first half of this year were the children’s health and addiction treatment sectors, with only 9 and 5 deals respectively, totaling $60.8 million and $69.6 million in transaction value.

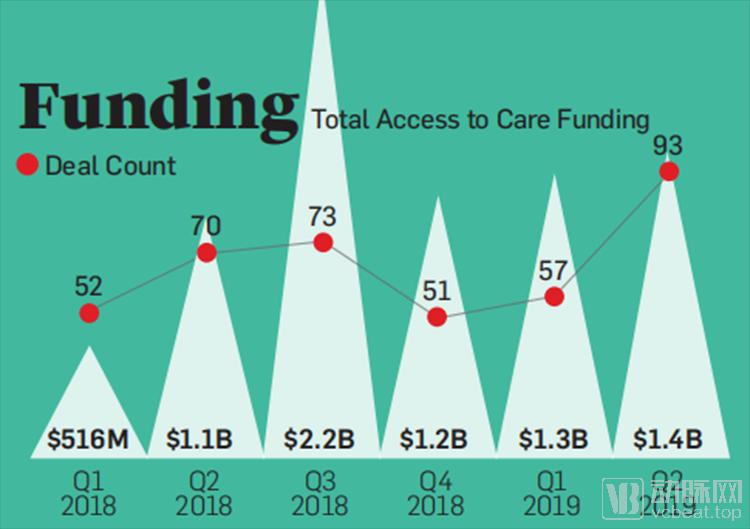

Domain of Access to Care

Transaction Value and Volume in the Field: Four Quarters of 2018 to Two Quarters of 2019

In the field of "healthcare service accessibility," financing increased by 67% and the number of transactions rose by 23% from the first half of 2018 (2018 Q1, 2018 Q2) to the first half of 2019 (2019 Q1, 2019 Q2).

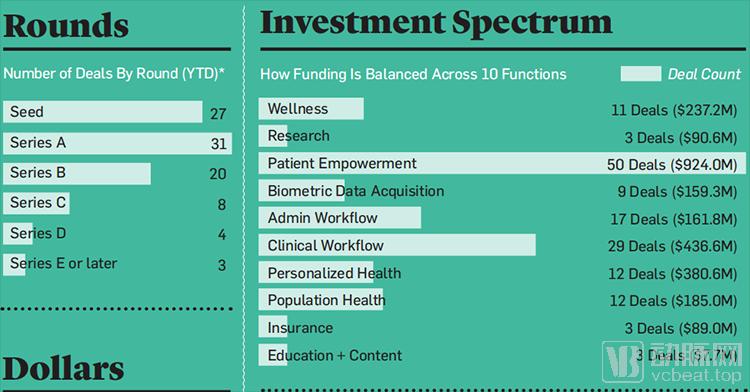

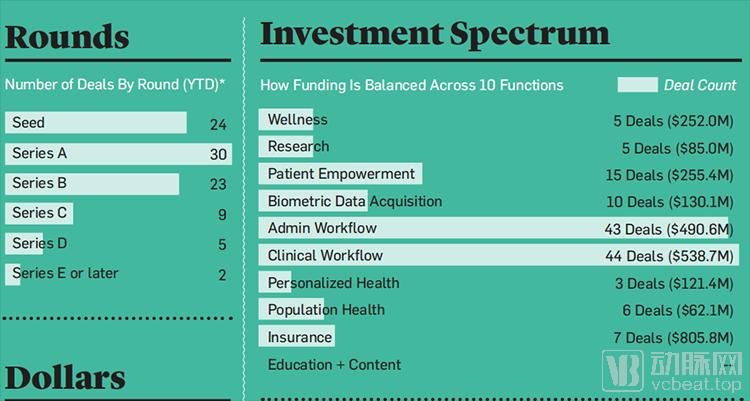

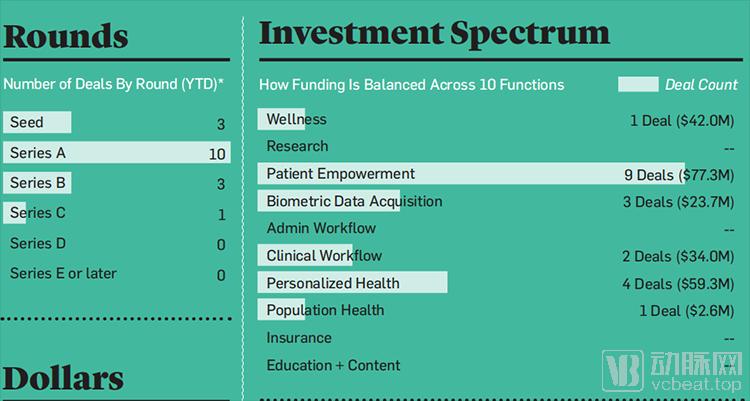

Distribution of Financing Rounds and Investment Frequency in This Sector During the First Half of 2019

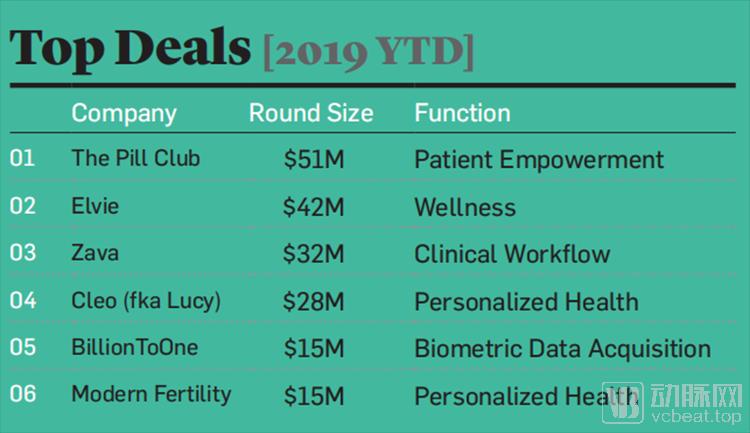

In terms of financing rounds and investment frequency, Series A rounds accounted for the largest proportion, with 31 transactions. Patient Empowerment received the highest number of investments, totaling 50 deals, with a cumulative investment amount reaching $924 million. The largest individual investments in this sector are illustrated in the figure below.

Penguin Almond Group Secures $250 Million in Funding, Ranking First on the List

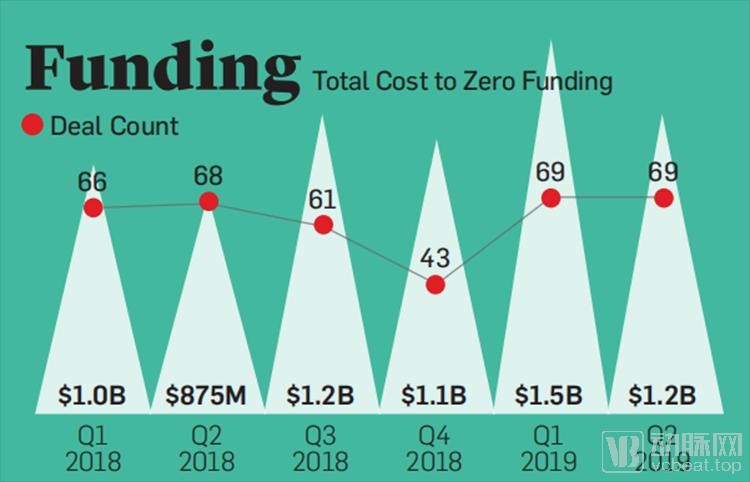

Zero-Cost Care (Cost to Zero) Sector

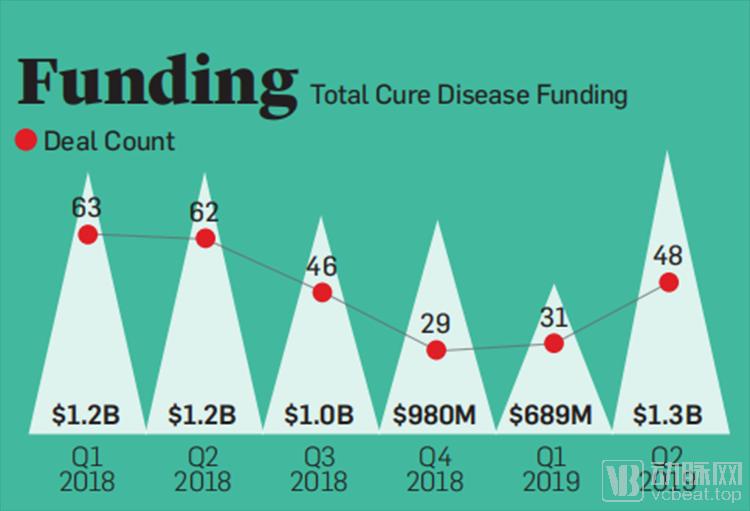

Transaction Value and Volume in the Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “zero-cost care” sector, transaction volume saw almost no growth from the first half of 2018 (Q1 and Q2 2018) to the first half of 2019 (Q1 and Q2 2019), but transaction value in the first half of this year reached $2.7 billion, a 45% increase.

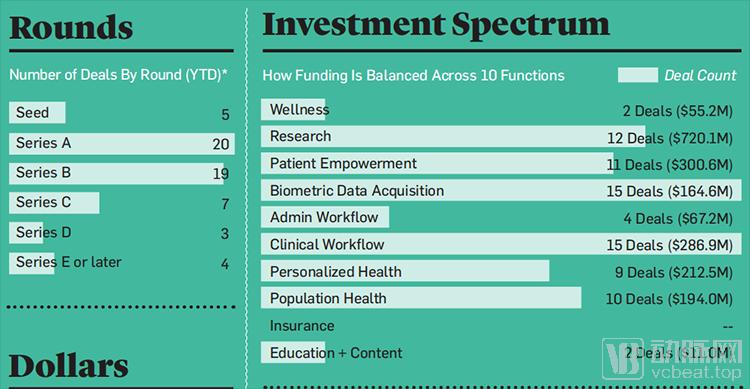

Distribution of Financing Rounds and Investment Frequency in the Field During the First Half of 2019

In terms of financing rounds and investment frequency, Series A accounted for the largest proportion, with 30 deals. Clinical Workflow and Admin Workflow ranked first and second in the number of investments received, with 44 and 43 deals respectively, and total investment amounts reaching $538 million and $490 million respectively. The largest investments in this field are shown in the figure below.

Clover Health Tops the List with $500 Million in Funding

Disease Treatment (Cure Disease) Field

Transaction Value and Volume in This Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “disease treatment” sector, both funding and transaction volumes had declined for several quarters before increasing in June 2019, with quarterly funding rising by 90% and transaction volume up by 55%.

Distribution of Financing Rounds and Investment Frequency in the Field During the First Half of 2019

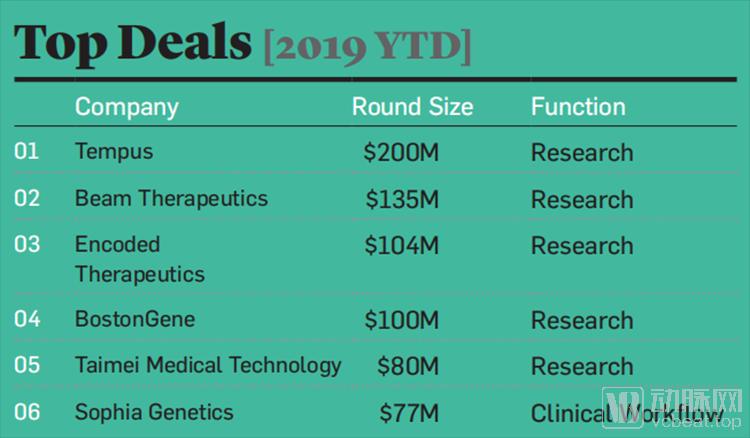

In terms of funding rounds and investment frequency, Series A and Series B financings ranked first and second, with 20 and 19 deals, respectively. Biometric Data Acquisition and Clinical Workflow tied for the highest number of investments, each receiving 15 deals, with total investment amounts reaching $164 million and $286 million, respectively. The largest individual investments in this field are shown in the figure below.

Tempus Ranks First with $200 Million in Funding

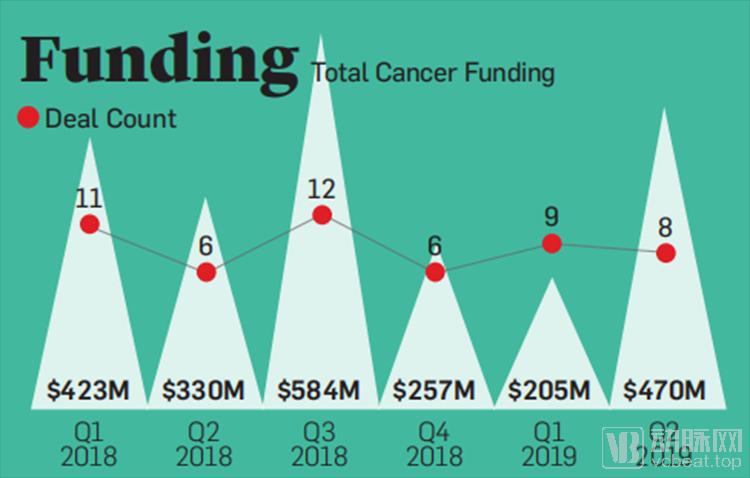

Cancer Field

Transaction Value and Volume in the Field: Four Quarters of 2018 to Two Quarters of 2019

In the "cancer" sector, funding rebounded in Q2 of this year after a continuous decline through the end of 2018, surging by more than 120% compared to Q1 of the same year, with a median deal size reaching $14 million.

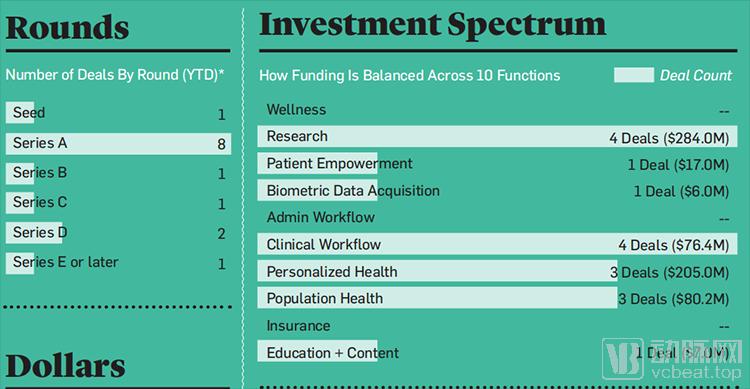

Distribution of Financing Rounds and Investment Frequency in This Sector in the First Half of 2019

In terms of funding rounds and investment frequency, Series A accounted for the largest share, with eight deals. Research and Clinical Workflow tied for the most frequent investment categories, each receiving four investments, with total investment amounts reaching $284 million and $76.4 million, respectively. The largest individual investments in this field are shown in the figure below.

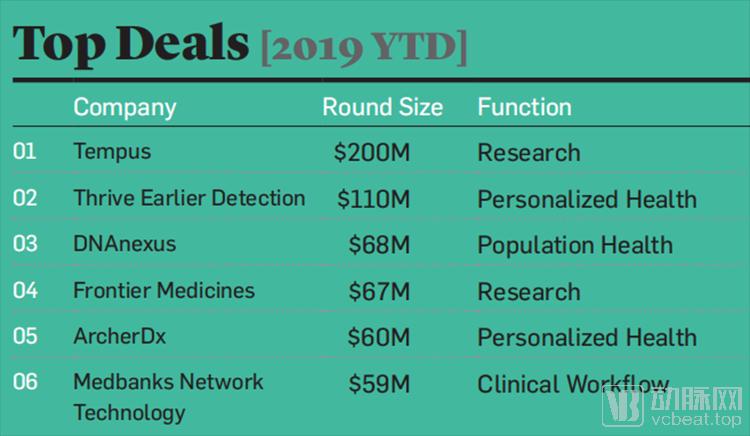

Tempus Tops the List with $200 Million in Financing

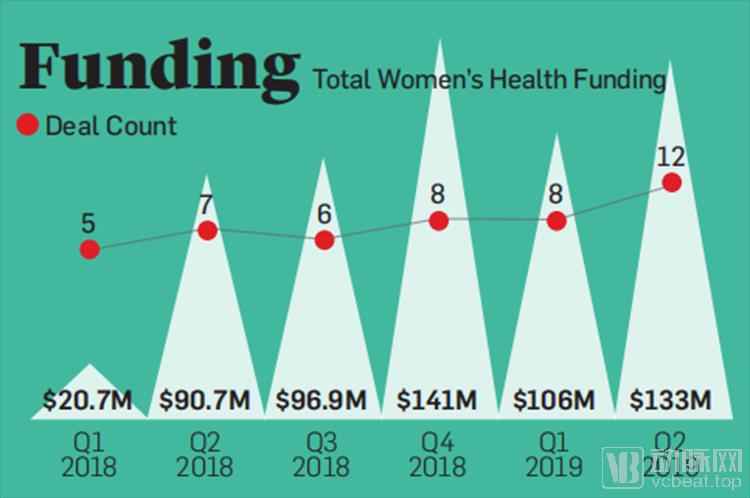

5. Women’s Health

Transaction Volume and Quantity in This Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “Women’s Health” sector, funding amounts and deal counts saw the largest growth from the first half of 2018 to the first half of 2019. The sector is still in its early stages, with 76% of funding coming from seed and Series A rounds. The median transaction amount was $6.8 million.

Distribution of Financing Rounds and Investment Frequency in the Sector During the First Half of 2019

In terms of financing rounds and investment frequency, Series A accounted for the largest proportion with 10 deals. Patient Empowerment received the highest number of investments, totaling 9 deals, with a total investment amount reaching $77.3 million. The largest investments in this field are shown in the figure below.

The Pill Club Ranks First on the List After Completing a $51 Million Financing Round

Children’s Health

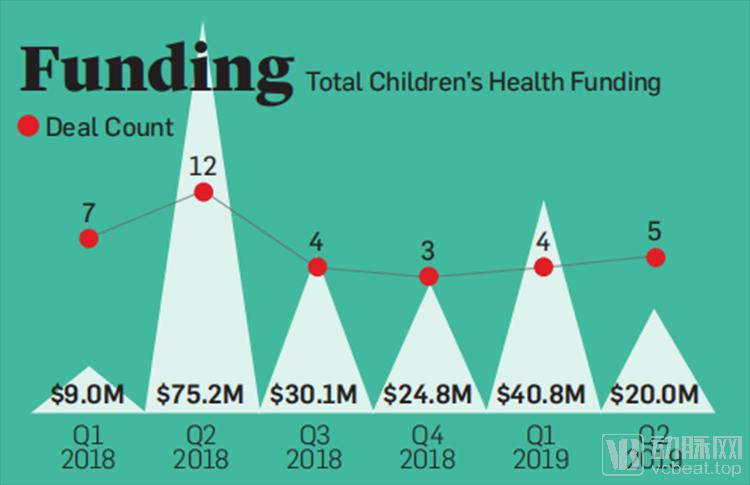

Transaction Volume and Value in This Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “Child Health” sector, fundraising increased by $24 million this year, while future funding trends in this area remain unpredictable. Since 2015, funding in this sector has been on the rise, but capital flows have been confined to the branches of population health and personalized health.

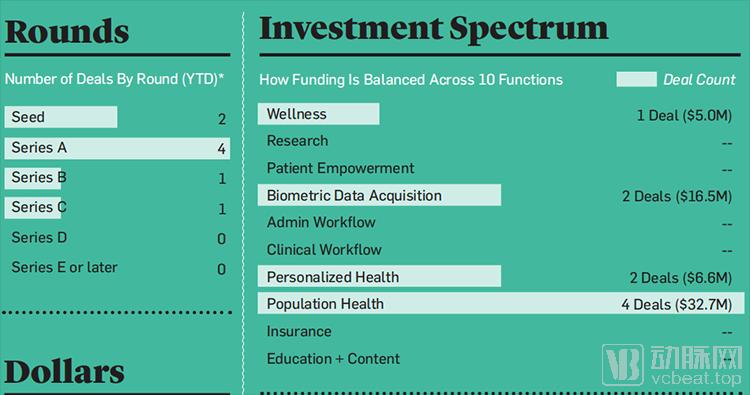

Distribution of Financing Rounds and Investment Frequency in the Field in the First Half of 2019

In terms of funding rounds and investment frequency, Series A accounted for the largest share, with four transactions. Population Health received the highest number of investments, also totaling four, with a cumulative investment amount of $32.7 million. The largest individual investments in this sector are illustrated in the figure below.

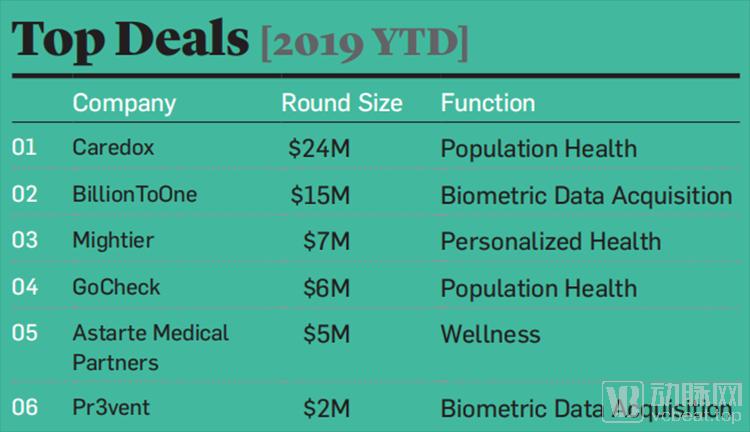

Caredox Completes $24 Million Financing, Ranking First on the List

Nutrition & Health (Nutrition & Fitness) Field

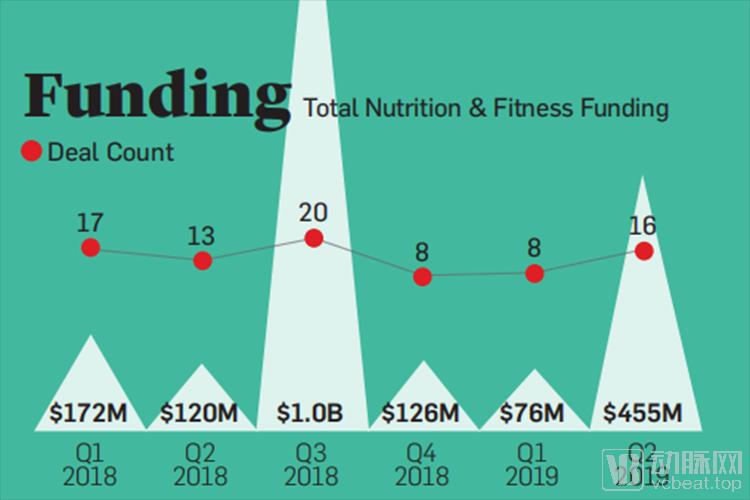

Transaction Value and Volume in the Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “Nutrition and Health” sector, funding growth from the first half of 2018 to the first half of 2019 ranked second only to that in the Women’s Health sector, representing an 82% year-over-year increase. In this year’s transactions, the median deal size reached $13.3 million, with 36% of deals exceeding $60 million.

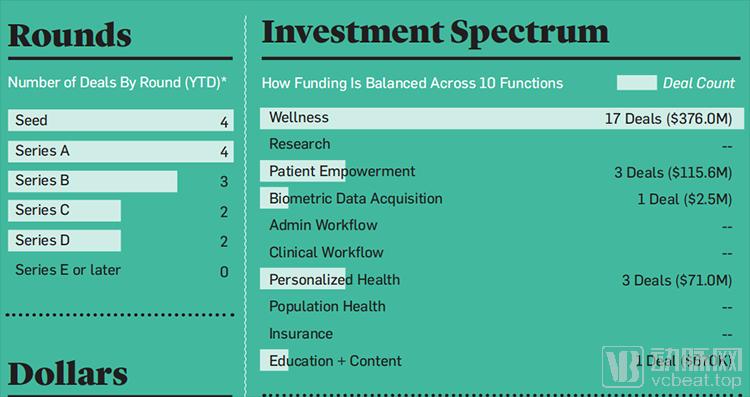

Distribution of Financing Rounds and Investment Frequency in This Sector During the First Half of 2019

In terms of financing rounds and investment frequency, Series A and seed rounds accounted for the largest proportion, with four investments each. The Wellness sector received the highest number of investments, totaling 17 deals, with a cumulative investment amount of $37.6 million. The largest investments in this sector are shown in the figure below.

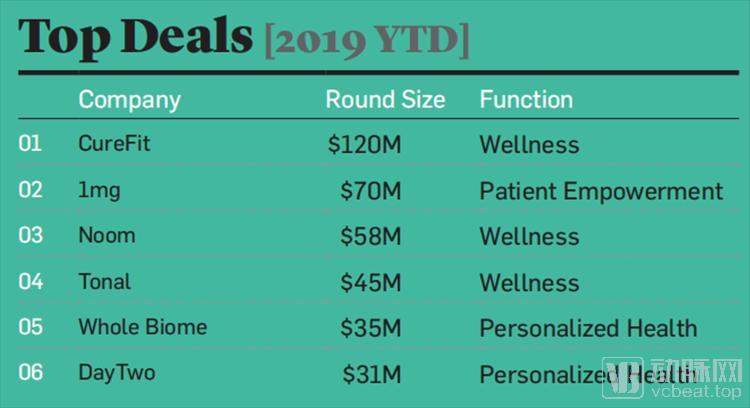

CureFit Tops the List with $12 Million in Funding

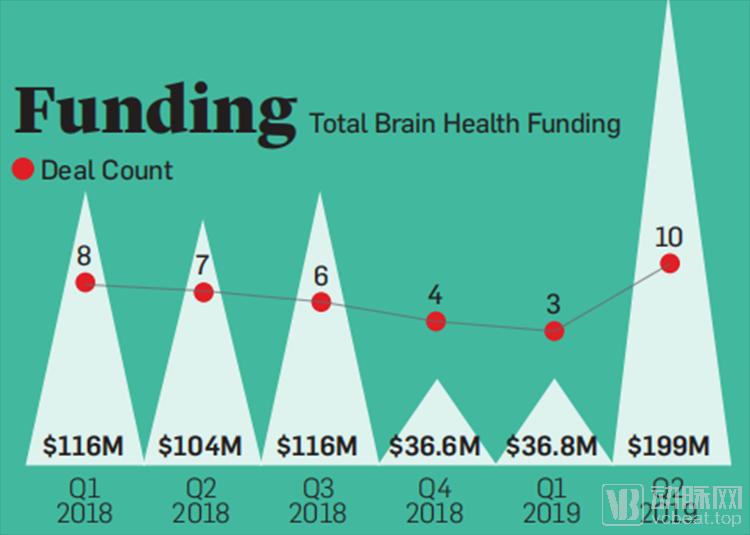

Brain Health Sector

Transaction Value and Volume in This Sector: Four Quarters of 2018 to Two Quarters of 2019

In the “Brain Health” sector, funding had been lagging almost continuously since the fourth quarter of 2018, only rebounding in the second quarter of this year. From BlackThorn Therapeutics’ development of neurological drugs to Savonix’s digital neurocognitive testing, the sector completed a series of financing rounds totaling $200 million.

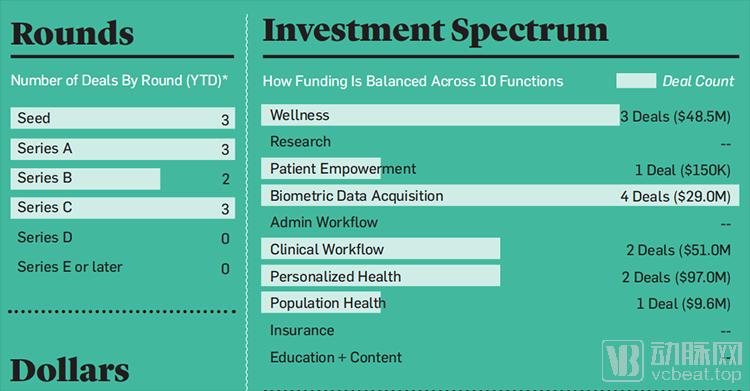

Distribution of Financing Rounds and Investment Frequency in This Sector in the First Half of 2019

From the perspective of investment rounds and investor frequency, there is no distinct distribution pattern in the number of investment rounds within this field; Seed, Series A, and Series C rounds each saw 2–3 investments. Biometric Data Acquisition received the highest number of investments, with four deals totaling $2.9 million. The largest individual investments in this sector are shown in the figure below.

BlackThorn Therapeutics Completes $76 Million Financing, Ranking First on the List

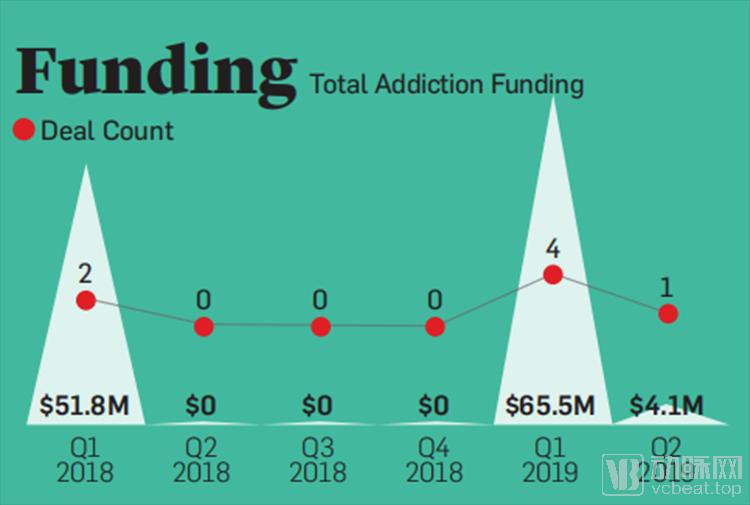

Field of Addiction Treatment (Addiction)

Transaction Volume and Value in the Sector: Four Quarters of 2018 and Two Quarters of 2019

The field of “addiction treatment” is a relatively “weak” sector, showing a significant quarter-on-quarter decline (-94%) from the first half of 2018 to the first half of 2019.

In the first half of 2019, a total of five financing rounds were completed in this sector, with three investments focused on Patient Empowerment, amounting to a total of $65.5 million. The largest financing round in this sector was secured by the drug development company Pear Therapeutics, which closed a $64 million Series C funding round.

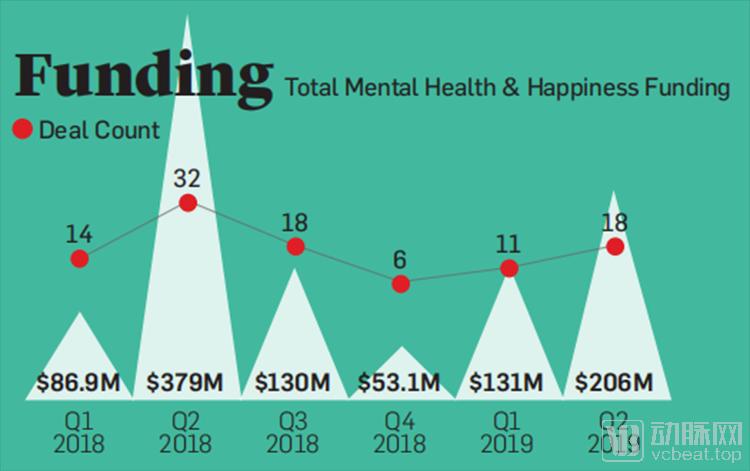

Mental Health & Happiness

Transaction Value and Volume in the Field: Four Quarters of 2018 to Two Quarters of 2019

In the "mental health" sector, the median transaction volume was $4 million, with financing rounds concentrated in the seed stage, totaling six deals. Furthermore, in the first half of this year, the sector saw five Series A financings, two Series B and Series C financings each, and three Series D financings. Calm raised the most capital this year, securing $88 million in funding.

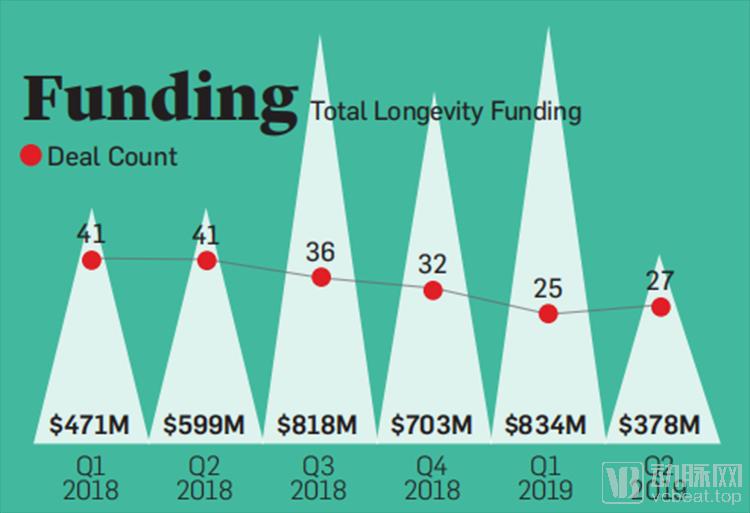

Longevity Sector

Transaction Value and Volume in This Sector: Four Quarters of 2018 to Two Quarters of 2019

From Q1 to Q2, funding and transaction volume in the longevity sector declined in 2019. Financing rounds were concentrated in seed-stage deals, with 12 transactions, followed by 10 Series B rounds and 6 Series A rounds. In the first half of this year, Clover Health secured the largest amount of financing in the sector, raising $500 million.