Philips' Three-Year Transformation: 18 Medical Technology Acquisitions and Strategic Focus on Four Key Healthcare Domains

Philips Healthcare

Integrated service provider in healthcare, quality living, and lighting fields

Transformation is not an easy undertaking, especially for large enterprises that have long been listed among the Fortune Global 500.

Pull one hair, and the whole body moves.

In 1891, Philips started its lighting business in the Netherlands. After growing and expanding, it mainly focused on two major businesses: lighting and health technology. In 2016, the revenue proportions were 29% for lighting and 71% for health technology. In September 2014, Philips announced its strategic implementation plan, with key measures including establishing two independent companies to focus respectively on healthcare technology and lighting business.

To achieve this goal, an independent structure for the lighting business was established within the Philips Group in February 2016. On May 27, 2016, Philips Lighting was listed on the Euronext Amsterdam stock exchange under the ticker symbol “LIGHT,” and it was renamed Signify in 2018.

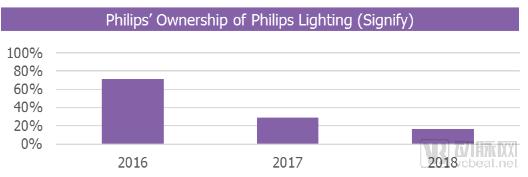

Philips’ Stake in Philips Lighting (Signify) Is Rapidly Declining

After the listing of Philips Lighting, Philips still held a 71.23% equity stake in the company. Subsequently, Philips continued to reduce its holdings in Philips Lighting/Signify, and as of December 31, 2018, its shareholding ratio had decreased to 16.5%.

Philips, by contrast, focuses primarily on healthcare. In the past, Philips offered a wide range of medical product lines with limited interconnectivity. Over the past two to three years, however, the company has been rolling out themed solutions that are more closely aligned with the needs of hospitals, healthcare institutions, consumers, and patients, while continuously increasing solution complexity.

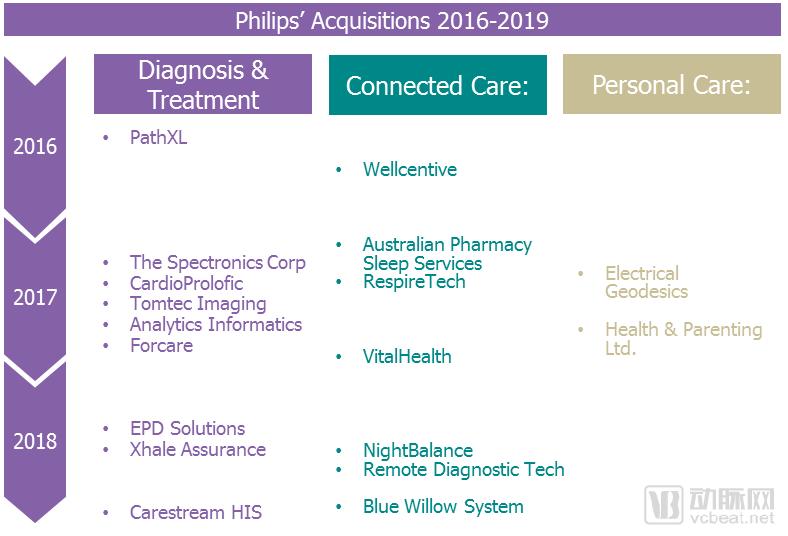

Since early 2017, Philips has completed 18 acquisitions in medical technology, signaling its transformation into a technology provider in the healthcare sector. This transformation is characterized by three key aspects. First, Philips has gradually consolidated and integrated its product lines around thematic focuses, making operations more holistic and efficiency-driven by aligning them with these core themes. Second, the company has reduced its interest in non-healthcare businesses and is now fully recognized by the industry as a health technology enterprise. Third, Philips has evolved from a manufacturer focused primarily on devices and hardware into a solutions-oriented company that leverages its advanced equipment to provide comprehensive care throughout the patient journey and disease lifecycle.

Major Acquisitions by Philips’ Business Groups Over the Past Three Years

Overview of Philips' Key Acquisitions in the Past Three Years

Diagnosis and Treatment, and Healthy Living account for the majority of Philips' revenue.

Philips organized its internal business units into three core healthcare technology sectors: the Personal Health Business Group, the Diagnosis and Treatment Business Group, and the Care and Nursing Business Group. In January 2019, Philips restructured its business architecture again, adjusting it to Diagnosis and Treatment, Connected Care and Health Informatics, and Healthy Living.

Philips’ 2018 Annual Report Discloses Revenue and Growth for Its Three Business Groups Over the Past Three Years

In Philips’ 2018 Annual Report, operating revenue was disclosed by new business groups. The Diagnosis & Treatment and Health Living segments constitute Philips’ core businesses, with revenues of EUR 7.245 billion and EUR 7.228 billion, respectively, showing a negligible difference.

Diagnosis and Treatment is the most important segment, comprising two major businesses: Precision Diagnosis, led by Luo Kai, and Image-Guided Therapy, led by Bert van Meurs. The Diagnosis and Treatment segment achieved a nominal growth of 5.1% compared to 2017, primarily driven by double-digit growth in Philips’ Image-Guided Therapy and Ultrasound businesses, as well as low single-digit growth in the Diagnostic Imaging business.

In 2018, the Connected Care and Health Informatics business generated total revenue of €3.084 billion, representing a nominal 2% decrease compared to 2017. Within this segment, the Health Informatics business saw slight single-digit growth, while the Monitoring & Analytics and Therapy & Care businesses remained flat year-over-year. Growth in the Therapy & Care business was impacted by significant expenses related to settlement agreements. The Sleep & Respiratory Care business was transferred from the Personal Health segment to the newly renamed Connected Care segment. Philips’ Connected Care portfolio comprises “Monitoring & Analytics and Therapy & Care,” “Sleep & Respiratory Care,” and “Population Health Management.” It aims to connect pre-hospital, in-hospital, and post-discharge settings by providing intelligent, integrated data management and analytics solutions. By capturing and integrating comprehensive patient data, it enables healthcare professionals to make diagnosis and treatment decisions based on data-driven insights and deliver personalized care services.

The Healthy Living business generated total revenue of €7.228 billion in 2018, representing a 1% nominal decrease compared to 2017. Excluding the negative currency effects and consolidation impacts totaling 4%, comparable revenue increased by 3% year over year. The Sleep & Respiratory Care business achieved high single-digit growth but has since been reclassified into a different business segment. The Personal Health & Home Appliances business recorded modest single-digit growth, while the Health & Wellness business remained flat year over year.

Philips' Four Key Strategic Directions for the Future

A few weeks ago, Philips held its annual industry analysis forum in Boston, where it showcased its evolving business portfolio. At the conference, Philips highlighted four strategic directions for the future of healthcare:

- Imaging Diagnostics Field

- Radiology AI

- Virtual Care and Remote ICU

- Population Health Management

Imaging Diagnostics Field

First, Philips plans to expand its Diagnosis and Treatment business and strengthen its influence in the field of imaging diagnostics. In March this year, the U.S. FDA approved the Philips Intellisite Pathology Solution (PIPS), which is the first whole slide imaging (WSI) system that can assist physicians in interpreting digital pathology images, and also the first WSI system approved by the FDA for this purpose. Philips aims to extend its business into oncology through the Intellisite platform, encompassing areas such as digital pathology and radiation oncology.

In the field of radiation oncology, Philips has established partnerships with Elekta and Radiation Oncology. The world’s first high-field magnetic resonance radiotherapy system—Elekta Unity—incorporates Philips’ innovative MRI technology, seamlessly integrating a state-of-the-art radiotherapy accelerator, a 1.5T high-field diagnostic-grade MRI system, and online adaptive radiotherapy workflow software into a single platform. This platform enables real-time acquisition of MRI images of tumors and surrounding normal tissues during treatment, online adjustment of treatment plans, and real-time assessment of treatment outcomes.

At ESTRO 2019, Philips launched IntelliSpace Radiation Oncology, an intelligent patient management solution for radiation oncology and the latest addition to its portfolio of radiation oncology systems and software suites. The new product lineup, unveiled for the first time at ESTRO, includes Pinnacle Evolution treatment planning software, Big Bore RT, a dedicated oncology computed tomography (CT) simulator, as well as the Ingenia Elition 3.0T MR-RT and Ambition 1.5T MR-RT magnetic resonance (MR) systems.

Through the imaging equipment, oncology treatment devices, and information system integration and solutions launched in collaboration with its partners, Philips leverages the respective advantageous resources of both parties to jointly promote new technologies, thereby enhancing their capacity to serve radiation oncologists and cancer patients. Given that multidisciplinary team involvement is required throughout the entire cycle of radiation oncology treatment, Philips’ new strategic direction is clearly a wise move.

Radiology AI

Artificial intelligence is a recurring theme in Philips’ medical imaging business, with its Personal Health, Connected Care, Precision Diagnosis, and Image-Guided Therapy (IGT) business lines all revealing plans to leverage AI in their respective products. It is evident that AI will play a pivotal role as Philips transitions from a hardware vendor to a solutions provider.

As early as five years ago, Philips incorporated digital innovation and artificial intelligence into its corporate development strategy. The company invests €1.8 billion annually in research and development. Currently, Philips employs more than 400 data scientists worldwide, focusing on research topics related to big data and AI, with close integration into clinical scenarios and workflows.

Currently, the core of this strategy is a cloud-based platform, the HealthSuite Digital Platform (HSDP), which provides seven domain-specific platforms for its key business areas, including HealthSuite Consumer, HealthSuite Acute Care, and HealthSuite Imaging.

In the field of radiology, Philips’ AI platform is IntelliSpace Discovery 3.0, positioned as an end-to-end solution. This software platform facilitates the development and deployment of radiology AI algorithms in clinical research and is scheduled for launch in the fourth quarter of this year. It will initially integrate Philips applications, with third-party applications to be added later. With integrated AI capabilities, AI-generated results can be directly sent to the PACS, allowing radiologists to accept, edit, or reject the AI’s recommendations.

By supporting radiologists in clinical and translational research, Philips has positioned itself as a one-stop provider for radiology AI. Philips is still exploring business models for its radiology AI marketplace, striving to offer broader applications. These applications can be integrated not only into customers’ clinical workflows but also into their billing and administrative workflows—a common challenge faced by competitors. It may encourage third-party developers to promote their applications using standardized licensing models, such as annual subscriptions or pay-per-click, and may adopt tiered pricing depending on the functionality of the applications. Most major medical imaging companies have entered the AI marketplace and are likely to offer similar content. The key differentiators lie in how workflows are integrated and how charges are structured.

Virtual Care and Remote ICU

Tele-ICU was a key topic at Philips’ industry analyst event. The Tele-ICU capabilities of the Philips Acute Care Suite were demonstrated during the conference, with partners such as Partners HealthCare and Emory Healthcare highly praising the solution for its process improvements and enhanced efficiency.

Philips entered the Tele-ICU market more than a decade ago through its acquisition of Visicu. At that time, the solution was serving approximately 9% of ICU beds in the United States, an achievement Visicu accomplished in less than five years of commercial operations. However, growth remained sluggish compared to the early years; by early 2019, only about 20% of U.S. ICU beds were being monitored using Tele-ICU technology.

For most markets (such as smaller hospitals with fewer than 40 ICU beds), the commercial viability of launching centralized TeleICU solutions is relatively low. However, these smaller hospitals still have the potential to adopt Tele-ICU. Philips sells its TeleICU solutions to multiple telehealth service providers and also offers outsourced TeleICU monitoring services to many small hospitals. For example, Advanced Care ICU partners with Philips to provide services for nine virtual hospitals, monitoring nearly 1,000 ICU beds across the United States.

For Philips and the broader market, the international landscape for TeleICU deployment also varies slightly. The vast majority of Philips’ TeleICU business is driven by the United States; however, it has also successfully sold its solutions in the United Arab Emirates (Ministry of Health), India (Medica Hospital, Advanced Care ICU, INTeleICU), the United Kingdom (Guy’s and St Thomas’ NHS Foundation Trust), and Japan (Showa University Hospital). Subsequently, Philips has been promoting its Tele-ICU technology at HIMSS Europe in Helsinki, clearly indicating that it sees market opportunities beyond the United States.

Philips is one of the very few vendors offering a centralized Tele-ICU platform; therefore, despite market growth falling short of expectations, Philips has maintained the largest market share. It faces several competitors providing decentralized solutions, such as American Well (through its acquisition of Avizia) and InTouch Health. However, there are few competitors in the centralized model segment. In the future, remote monitoring is also likely to secure a position within the patient monitoring market by leveraging the deployment of its acute care suites to expand into other hospital settings, such as emergency departments or remote training—two telehealth areas expected to achieve rapid growth over the next five years.

Population Health Management

At an industry analyst event covering all of Philips’ business units, one thing has become increasingly clear: its focus has shifted to patients. Population health management is a key business segment within Philips’ Connected Care division, dedicated to providing comprehensive solutions for the healthcare ecosystem. This effort supports the gradual extension of healthcare services into lower-cost settings such as homes and communities, thereby driving the transformation of healthcare systems toward a “value-based model.”

Although Philips’ Population Health Management (PHM) division accounts for only a small fraction of the company’s overall business line revenue (as shown in the chart above), its outcomes measurement solutions have opened up a new market beyond its existing business. The trend toward vendor consolidation has led to engaged healthcare networks that encompass not only hospitals but also clinics, care facilities, communities, and homes.

Carla Kriwet, CEO of Philips’ Connected Care business unit, outlined Philips’ strategy in this field. Health systems can leverage existing solutions on Philips’ HealthSuite Digital Platform (HSDP) to create an ecosystem.

Since acquiring Wellcentive in 2016 and VitalHealth in late 2017, Philips has been implementing a plan to integrate these legacy solutions and its Remote Patient Monitoring (RPM) products into a single platform, Philips Engage, which will be hosted on the HealthSuite Digital Platform (HSDP). The addition of VitalHealth has strengthened Philips’ population health management portfolio, enabling Philips to better serve the healthcare ecosystem—including hospitals, care providers, patients, and insurance companies—and accelerate the transition of healthcare systems toward a “value-based model.” VitalHealth’s solutions seamlessly integrate patient measurements, patient engagement, care coordination, and medical analytics into electronic health records (EHRs), connecting in-hospital and out-of-hospital settings to serve both healthcare professionals and patients. Its platform allows for the configuration of interconnected care applications tailored to specific disease types, accessible simultaneously on desktop computers, tablets, and smartphones, thereby connecting and coordinating all stakeholders involved in care delivery to create a comprehensive, internet-based professional care service.

Philips’ acquisition strategy over the past two years has undoubtedly presented challenges in product integration, while Population Health Management (PHM) has remained one of the areas where Philips has made significant progress through its Engage platform and the HealthSuite Digital Platform (HSDP). However, revenue growth was constrained during the integration phase; as technical hurdles are now being overcome, the focus will shift to how Philips scales this business.

From technical, strategic, and financial performance perspectives, Philips’ rapid transformation—driven by its strategic focus on healthcare technology and significant acquisitions in recent years—has undoubtedly presented numerous challenges. During its analyst event in Boston, Philips demonstrated that it has achieved several milestones in product integration, although considerable work remains in this area. The overall strategy outlined for its three business divisions is clear, focusing on areas poised to become central to the healthcare market in the coming years, such as artificial intelligence, value-based care, telehealth, and the consumerization of health.

The company’s comparable growth rate in 2018 was 5% (2% on a nominal basis), with the Diagnosis and Treatment business segment achieving a comparable growth rate of 7% (5% on a nominal basis), outperforming Philips’ competitors in this field. The challenge facing Philips in the future will be to continue leveraging its acquisitions, technological achievements, and clear strategy to expand its new businesses and drive additional growth.

Localization in China

At the 2019 China International Medical Equipment (Spring) Fair held in May this year, Philips also made its appearance with solutions, showcasing its latest information-based and intelligent innovative solutions covering the business segments of “Precision Diagnosis,” “Image-Guided Therapy,” and “Connected Care.” In addition to the solutions consistent with Philips’ global offerings, VCBeat also gained insights into Philips’ strategic layout in China at the exhibition.

The Chinese market plays a vital role in Philips’ global strategy. Notably, within the Diagnosis and Treatment business segment, the Chinese market achieved double-digit growth in 2018. Growth across various market segments was primarily concentrated in China, ASEAN countries, the Middle East and Turkey, as well as Central and Eastern Europe.

Given the differences between the Chinese and global markets in terms of demand areas, demand intensity, and level of informatization, Philips has adopted a targeted approach to its solution layout. For instance, in February 2019, Philips signed a letter of intent with CITIC Pharmaceutical to jointly promote the domestic implementation of VitalHealth, a cloud-based population health management platform. The first step in the collaboration between Philips and CITIC Pharmaceutical involves developing and operating applications based on the VitalHealth platform’s runtime environment, including a health examination follow-up and health management system for high-end clientele, a prototype internet hospital system for assisted reproduction, and a prototype interconnected care system for out-of-hospital stroke rehabilitation. In the future, both parties will also jointly invest in the secondary development of VitalHealth to tailor it to China’s specific application environment.

At CMEF, Philips announced its collaborations with Shenzhou Medical and Ping An Good Doctor, and launched “Shenfei Cloud 2.0.” Built upon the cloud-based “Philips IntelliSpace” image post-processing platform already implemented in version 1.0, Shenfei Cloud 2.0 is an integrated solution developed specifically for the practical application scenario of early lung cancer screening. It provides end-to-end services to enable precise lung cancer screening at primary-care hospitals, encompassing intelligent equipment, information software systems, and professional services. These include a 16-slice CT scanner tailored for primary healthcare settings, medical consortium services, and lightweight imaging centers. The solution delivers comprehensive support across data acquisition, image reconstruction, image post-processing, result analysis, and assisted diagnosis and treatment, thereby helping physicians enhance diagnostic confidence, achieve early detection of small nodules and accurate follow-up, and ultimately improve the accuracy and efficiency of clinical diagnosis.

Philips has launched the “Integrated Cardiovascular Solution” for the Chinese market. This solution includes the Philips IntelliSpace Cardiovascular system, the EPIQ 7C intelligent cardiovascular ultrasound system, and echocardiography-guided interventional therapy solutions, among others. Also showcased within the “Philips Integrated Cardiovascular Solution” are two informatics solutions specifically tailored to meet the unique needs of China’s healthcare system: the one-stop IntelliSpace Care Management (ISCM) system, developed to address the direct reporting requirements for quality control data in the construction of “Chest Pain Centers” and “Stroke Centers.”

In the Chinese market, beyond public Grade-A tertiary hospitals, primary care facilities and private medical institutions require more convenient, affordable, and high-value medical services. If the real-world shortage of diagnostic physicians at the primary care level can be addressed while significantly improving physicians’ work efficiency, greater success is expected in the Chinese market. Meanwhile, Philips’ collaboration with other domestic healthcare enterprises to further enhance its integrated solution offerings will serve as the main thrust for future product promotion.

References:

Philips 2017 Annual Report

Philips 2018 Annual Report

Analysis: Philips’ Evolution to a Pure-play Healthcare Technology Vendor

https://hitconsultant.net/2019/07/02/analysis-philips-evolution-pure-play-healthcare-technology-vendor/#.XSavAugzZaR

€1.8 Billion in Annual R&D Investment: Philips Presents Five-Year Digital Transformation Report Card at CMEF

https://vcbeat.top/NTM5MzUxYjFiYTc0NmFkYmI2YmFkYmE4ODhmYTg1MTM=