178 Financing Rounds and 24 IPOs: Five Key Sectors Poised for Growth – 2019 H1 Biotech Investment Report

In many people’s forecasts, 2019 will be a difficult year, with the “chill” from the 2018 capital winter continuing to persist.

However, according to the “H1 2019 Healthcare Industry Investment and Financing Report” recently released by VCBeat, financing for 730 projects in the first half of 2019 exceeded $20 billion, setting a new historical high.

The harsh winter has long since dissipated, and the healthcare industry appears to continue maintaining a robust growth trajectory.

In the fields of biology and medicine, domestic investment in biopharmaceuticals continues to dominate, with gene testing remaining a prominent area after several years of sustained interest. In contrast, regenerative medicine, genetic engineering, and biomaterials have emerged as representatives of innovation in the healthcare industry abroad. Investment and financing trends appear to be diverging significantly between China and overseas markets.

We selected investment and financing data related to the biotechnology sector from the first half of the year, compared domestic and international figures, and sought potential new investment directions by analyzing the disparities in funding activities. As per our usual practice, we derive insights into the future from the data.

In the first half of 2019, there were 63 financing events in China’s biotechnology and pharmaceutical sectors, with a total funding amount of $1.645 billion. Among the overseas companies included in our statistics, there were 115 financing events, totaling $5.408 billion. In addition, there were 7 initial public offerings (IPOs) in China’s biotechnology sector, raising a total of $1.403 billion; abroad, there were 17 IPOs, raising a total of $1.194 billion.

Data indicate that investment trends in China during the first half of 2019 remained largely unchanged, with chemical drugs, biologics, and genetic testing continuing to be the most heavily invested sectors, attracting the highest financing amounts and frequencies. Chemical drug companies secured a total of USD 570.0337411 million in financing across 16 deals; biologics companies raised USD 481.357069 million through 16 deals; and genetic testing firms (including instruments, equipment, testing, and analysis) obtained USD 310.1688567 million via 15 deals.

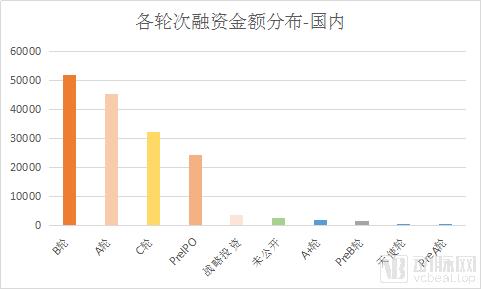

Broadly speaking, the financing landscape in China during the first half of the year remained largely unchanged, with continued investment focused on precision medicine. An analysis of the distribution of funding amounts across various rounds reveals that the majority of capital was allocated to companies at Series A and beyond. Angel and Pre-A rounds collectively raised only $10.42 million, accounting for just 0.63% of the total.

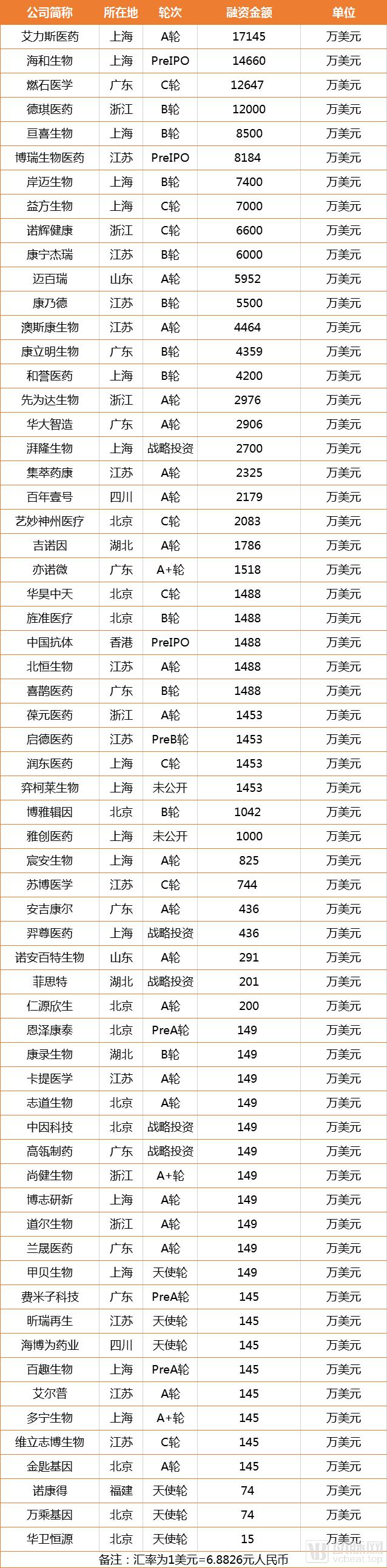

Among the top ten companies by financing amount, most are familiar names.

Abroad, biologics and small-molecule drugs remain the mainstream investment focus. A total of 36 biologic companies secured $1,631.67612 million in financing, making it the sector with the highest total funding, while 19 small-molecule drug companies raised a combined $986.9042 million. Although these two sectors have maintained their popularity for decades, another emerging therapeutic area deserves attention by comparison.

In the first half of 2019, a total of 13 companies in the gene therapy sector secured financing, with the total amount reaching $1,247.862982 million, second only to biopharmaceuticals. However, the average financing amount per gene therapy company was $95.98946015 million, twice that of biopharmaceutical companies.

Among the top 10 companies in financing rankings, four are gene therapy firms. Undoubtedly, gene therapy is currently the star player in overseas biotechnology venture capital investment.

Biologics and small-molecule chemical drugs have long remained perennial investment hotspots. Investment enthusiasm in these two sectors has persisted abroad for nearly three decades, while in China, investment in drug innovation began around 2012. Continuous technological iterations, from small-molecule targeted therapies to antibodies, have consistently revitalized these fields. In the antibody space (e.g., PD-1), the early-stage layout phase has concluded, and the sector has entered a harvest and commercialization stage. However, beyond PD-1, numerous inhibitory pathways remain to be explored. Although the next “PD-1” has not yet emerged, scientific breakthroughs are merely a matter of time.

As for early-stage investments in the pharmaceutical sector, RNA therapeutics may warrant attention. In 2018, the approval of two RNA-based drugs marked a breakthrough in this field, subsequently sparking increased investor interest and financing activity.

In April 2019, Panorama, a company focused on drug development related to RNA regulation, secured $3.7 million in seed funding. Its investors included WI Harper Group, Delian Capital, ZhenFund, and the Sino-US United Fund-Luxin Venture Capital Fund.

Arrakis also closed its $75 million Series B financing round in the same month. The round was co-led by venBio and Nextech Invest, with participation from WuXi AppTec, Omega Funds, HBM Healthcare Investments, GV, Alexandria Venture Investments, and Arrakis’s Series A investors. With this funding, Arrakis will advance the development of its product pipeline based on its innovative small-molecule drug platform targeting RNA, accelerating the progression of its drug candidates into clinical trials.

In May, Twentyeight-Seven Therapeutics secured an additional $17.75 million in funding from prominent venture capital firms Sofinnova Partners and Osage University Partners. Earlier, in its Series A financing round in September 2018, the company received a total of $65 million from MPM Capital, Novartis Venture Fund, Johnson & Johnson Innovation (JJDC), Vertex Ventures HC, Longwood Fund, and Astellas Venture Management. To date, the total amount raised in its Series A round has reached $82.75 million.

The rising prominence of RNA therapies can be attributed to 2018, a year rightly hailed as the inaugural year of RNA therapeutics. In August, Alnylam’s Onpattro received approval from the U.S. Food and Drug Administration (FDA), becoming the first RNA interference (RNAi) drug to reach the market in the two decades since the discovery of the RNAi phenomenon—a milestone of significant importance. In December, Moderna Therapeutics, an RNA therapy company, raised $604.3 million through its initial public offering (IPO), setting a record for the largest biotechnology IPO in history.

In early July 2019, Skyhawk Therapeutics announced a research and development collaboration agreement with Merck & Co. (MSD). Skyhawk will leverage its SkySTAR technology platform to assist Merck in developing innovative small molecules targeting RNA splicing as potential novel therapies for certain neurological disorders and cancers. To date, Skyhawk has entered into collaboration agreements with multiple major pharmaceutical companies, including Biogen, Takeda, Celgene, and Merck, demonstrating significant industry interest in its small-molecule drug development platform targeting RNA splicing.

According to a report published by Grand View Research, the global market size for antisense RNA and RNAi therapeutic drugs is projected to grow at a compound annual growth rate (CAGR) of 8.6% from 2018 to 2025, reaching $1.81 billion by 2025, indicating strong momentum in RNA drug research and development in the coming years.

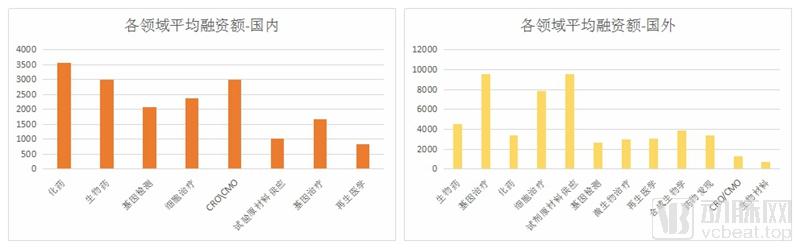

Beyond this, which other sectors warrant attention? We have also calculated the average financing amount across various sectors.

The distribution of average investment amounts differs significantly between China and other countries, yet a convergence emerges in the field of cell therapy, where average financing amounts in both regions rank among the highest.

The cell therapy industry in China secured a total of USD 166.2058772 million in financing, with an average of USD 23.74369675 million per deal, ranking fourth; the international cell therapy industry raised a total of USD 788.581 million, with an average of USD 78.8581 million per deal, ranking third.

The cell therapy industry has garnered significant attention, largely due to the sequential approvals of cell therapy products from Novartis and Kite. However, since their market launch, these two products have failed to deliver impressive sales figures. Their exorbitant pricing has remained highly controversial, and long-standing efforts to secure reimbursement through national health insurance ultimately came to naught.

So, why does cell therapy continue to attract significant attention? VCBeat believes that a key factor is that the two currently marketed products have yet to meet genuine clinical needs, leaving the market largely untapped. High costs and limited indications represent the current bottlenecks faced by the two approved cell therapy products. Startups that can achieve breakthroughs in these two areas are well-positioned to stand out.

Moreover, in this field, pharmaceutical giants and startups are almost on the same level. For startups, whether going public independently or eventually being acquired by major pharmaceutical companies, both are favorable exit strategies.

Moreover, the approval of existing products in the market demonstrates that the mechanisms and safety of cell therapy have been validated, and the regulatory approval framework has been well-established. For companies seeking to enter this field, there is no need to be concerned about uncertainties stemming from regulatory mechanisms or safety issues.

In China, although no company has yet officially initiated clinical trials for cell therapy, the National Medical Products Administration (NMPA) is poised to establish corresponding clinical trial standards, given that such products have already been launched in the United States. Shortly after Novartis brought its product to market, the NMPA began soliciting public comments on relevant guidelines, and several cell therapy products have since entered the clinical approval stage.

Currently, the majority of cell therapy products in China are centered on CAR-T therapies, with nearly all companies submitting product applications targeting the CD19 antigen for hematologic malignancies. This trend is likely driven by the fact that CD19 remains the only approved target for CAR-T therapies to date, providing a reference framework for both clinical trials and regulatory approval processes.

In fact, most domestic cell therapy companies are also laying out allogeneic therapy and solid tumor therapy products. These two directions will be the barriers to competition for CAR-T therapy in the next step. Most companies hope to rely on CD-19 to gain a leading market position, but they also need to prepare early for the next breakthrough.

Reagent raw materials include animal models, cell models, and culture media for plant and animal cells. Although the average funding amount in this sector has not ranked among the top domestically, we can see that the average funding amount abroad reaches as high as $95.9 million.

Reagent raw materials constitute the upstream sector of the biotechnology industry; however, the majority of products currently used in China are imported. Taking mice, the most commonly used laboratory animals, as an example, the world’s largest resource center for model mice and rats is The Jackson Laboratory in the United States, which provides approximately 10,000 strains of model mice. At the beginning of this century, there was a significant gap between China and developed countries in the overall level of mouse model development and application.

For basic research projects of this kind, the availability of high-quality domestically produced products will make import substitution a prevailing trend. Gaps in the domestic market also present opportunities for companies with high technological barriers. For instance, as previously reported by VCBeat, GemPharmatech, leveraging its self-established Chinese Laboratory Animal Resource Center for Genetic Engineering, developed China’s first conditional mouse strain and established a mouse application and industrialization base that aligns with international standards, promotes shared standards, and adheres to high-quality requirements.

On June 3, 2019, GemPharmatech completed its Series A financing round of RMB 160 million, with investors including CDH Investments and Sinopharm Group. Currently, GemPharmatech ranks first in Asia and second globally in scale.

Microbial therapy is a relatively underdeveloped field in China, whereas research on microbial-based treatments has long been flourishing abroad. It should be noted that the term “microbial therapy” here does not refer to antibiotic products, but rather to disease intervention achieved through the modulation of gut microbiota.

The advent of second-generation sequencing technology has greatly propelled the development of microbiomics. Among the most classic achievements are a series of discoveries linking the human gut microbiota to human health, including tumor immunology, metabolic diseases, neurological disorders, and autoimmune diseases. Nearly all diseases related to metabolism and immunity are associated with the human gut microbiota.

In the selection of indications for microbial therapy, tumor immunity has become a highly contested frontier. *Science* has sequentially published its fifth research article on how gut microbiota influence cancer immunotherapy. Taken together, these five landmark studies have virtually confirmed the correlation between cancer immunotherapy and gut microbiota.

Among the five companies that secured financing abroad in the first half of the year, four had oncology immunotherapy products in their pipelines. Notably, Bristol-Myers Squibb (BMS) and Vedanta Biosciences have entered into a clinical trial collaboration to evaluate the efficacy of combining BMS’s PD-1 immune checkpoint inhibitor Opdivo with Vedanta’s microbiome-based candidate drug VE800 for the treatment of advanced or metastatic cancer. BMS also plans to make a financial investment in Vedanta.

In addition to tumor immunology, metabolic diseases are also a current research hotspot in microbiome-based therapeutics. Second Genome’s product for non-alcoholic steatohepatitis (NASH) has already entered Phase I clinical trials. In a previous study on the microbiome industry, VCBeat found that in addition to venture capital firms such as OrbiMed and Seventure Partners, a number of pharmaceutical giants—including Roche, Johnson & Johnson, Takeda, Eli Lilly, Pfizer, and BMS—are also participating in this field.

Although no products have yet reached the market, successive discoveries in the scientific community have illuminated the industry prospects for microbiome-based therapies. Conditions such as cancer immunotherapy, Alzheimer’s disease, diabetes, and obesity either face significant therapeutic gaps or represent markets of enormous scale. Consequently, investment enthusiasm for microbiome therapeutics is heating up in tandem with research breakthroughs.

Gene therapy has been saved for last, as this sector is too significant to overlook. In the first half of 2019, two companies in China’s gene therapy sector raised a total of $33,697,434.28, with an average financing amount of $16,848,717.14. These figures may not appear particularly attractive. However, let us hold off on judgment and examine the data from overseas markets.

In the first half of 2019, a total of 13 gene therapy companies abroad completed financing rounds, raising a combined $1,247.862982 million, with an average financing amount of $95.98946015 million per company. This sector recorded the highest average financing amount in the first half of the year.

Furthermore, a series of acquisitions by major pharmaceutical companies has further fueled the momentum in gene therapy research. In March 2019, Biogen announced its $877 million acquisition of Nightstar Therapeutics, aiming to expand Biogen’s clinical-stage ophthalmology portfolio. Approximately ten days earlier, Roche acquired gene therapy pioneer Spark Therapeutics for $5 billion.

Notably, the two acquired companies feature ophthalmic disease treatments as their flagship products. In April 2018, Novartis acquired AveXis and obtained its gene therapy product Zolgensma, which was approved for market launch in May 2019. As the first gene therapy approved for treating pediatric spinal muscular atrophy (SMA), it is priced at $2.12 million.

The development of gene therapy and cell therapy shares similarities, with the earliest clinical trials dating back to the 1990s. Due to early technological limitations and an incomplete understanding of diseases, the progress of gene therapy was initially unsatisfactory. However, with advancements in foundational technologies such as gene editing and viral vectors, along with improved understanding of diseases and tissues, the safety and efficacy of gene therapy have matured. The approval of Luxturna and Zolgensma has provided significant encouragement to the industry.

After three decades of setbacks, gene therapy is advancing rapidly, emerging as a powerful tool for overcoming various hereditary and acquired diseases. Genetic immune disorders, hematologic diseases, and neurodegenerative conditions represent areas where current biological and chemical drug research has struggled to make significant breakthroughs.

According to the “2018 Global Gene Therapy Research Report” by the leading international think tank Jain PharmaBiotech, more than 183 companies worldwide are engaged in gene therapy research—more than four times the number in 1995—with over 2,000 clinical projects underway.

Among the aforementioned sectors, microbial therapy and gene therapy stand out as particularly distinctive. Innovation in these two fields has already gained momentum abroad, yielding notable achievements; by contrast, the domestic market remains in its early stages, presenting an opportunity for rapid follow-up. For companies with strong technical capabilities, these areas offer relatively easier entry points (though this does not imply low technological barriers), as industry competitors are few or still operate at a very small scale. For investors, although investing in early-stage technologies carries substantial risk, it may well be the optimal time for investment firms accustomed to making early-stage bets to establish their positions.

In contrast, cell therapy has already entered the next phase. While foreign products have been launched on the market, no domestic products have formally entered clinical trials in China yet; however, the number of companies involved has surged exponentially, and competition is poised to become intensely fierce. A few companies have already obtained clinical trial approvals, gaining a temporary leading advantage as their applications enter the review process.

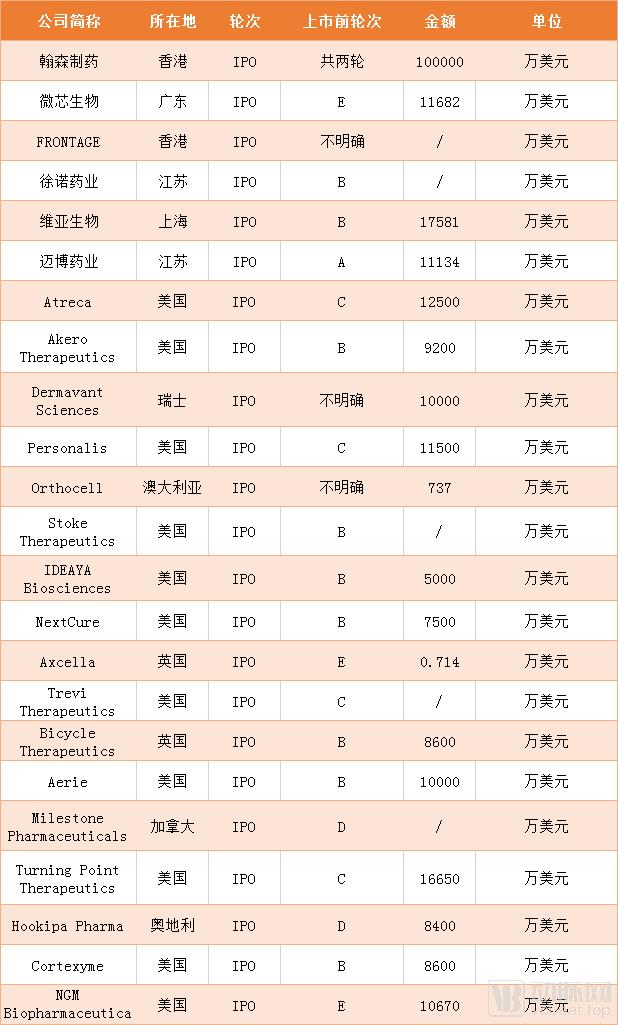

In the first half of the year, driven by the benefits brought about by the opening of the STAR Market and the Hong Kong Stock Exchange, the number of initial public offerings (IPOs) among domestic biotechnology companies was impressive. Seven companies went public, raising a total of $1.403 billion, with an average of $200 million per company. Of these seven companies, five listed on the Hong Kong Stock Exchange, undoubtedly demonstrating that the opening of the Hong Kong market has provided significant advantages to biotechnology firms. On the morning of June 13, 2019, the long-awaited STAR Market officially launched, with Chipscreen Biosciences successfully becoming the first biopharmaceutical company to list on the board. The opening of both the Hong Kong Stock Exchange and the STAR Market has enabled domestic biopharmaceutical companies to achieve a breakthrough in IPO numbers. With the launch of the STAR Market, biotechnology companies are poised to see another surge in listings, supported by the dual-platform advantage of the Hong Kong Stock Exchange and the STAR Market.

IPO Company Profile

Looking abroad, 17 companies went public in the first half of the year, with most concentrated at Series B and C stages. These 17 companies raised a total of $1.194 billion, averaging $70 million per company. Although Nasdaq has a longer development history compared to the Hong Kong Stock Exchange and the STAR Market, IPO fundraising amounts in China are more substantial.

Although the once-booming genetic testing sector has cooled abroad, funding in China remains relatively robust, driven by policy support and the exploration of new application areas. It is also evident that more capital is flowing into disease treatment research, focusing on unmet medical needs.

Whether in diagnosis or treatment, it is evident that these medical solutions are increasingly moving toward precision. Beyond oncology, the concept of precision medicine should be applied across the entire healthcare ecosystem in the future. Noteworthy areas will include disease-specific therapeutic interventions tailored to meet clinical needs, precise diagnosis and subtyping based on various diseases, and targeted treatments for specific conditions.