IDC Report: China's Healthcare Cloud Spending Reached RMB 5.05 Billion in 2018

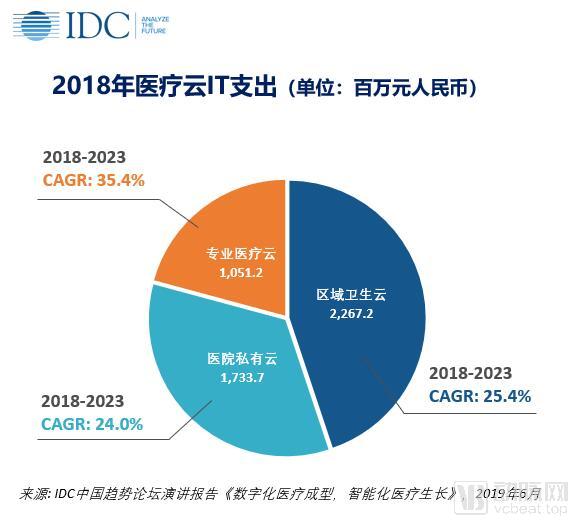

Beijing, July 18, 2019 — After years of continuous healthcare system reform and technological innovation, a distinctive Chinese model of innovative healthcare service delivery is taking shape. China’s digital transformation in healthcare is flourishing, with smart medical solutions blossoming across the board and the initial framework of smart hospitals beginning to emerge. Within this new healthcare service ecosystem, medical cloud computing serves as the foundational pillar. According to IDC research, total IT spending on medical cloud in China reached RMB 5.05 billion in 2018 and is projected to reach RMB 16.88 billion by 2023, representing a compound annual growth rate (CAGR) of 27.3% from 2018 to 2023.

“IDC MarketScape: China Healthcare Cloud, 2019 Vendor Assessment” report was officially released recently against this backdrop. The report indicates that public cloud providers and healthcare IT vendors offering construction and operation services for private healthcare clouds are the two main types of vendors in the current healthcare cloud market. The report selected 11 market-recognized healthcare cloud enterprises for analysis and assessment, providing a reference for hospitals, local health commissions, and various emerging healthcare service institutions when selecting suppliers.

Medical cloud computing is reflected not only in the adoption of cloud-based IT infrastructure by hospitals and the use of cloud services for medical information systems, but also serves as a platform supporting the application of new technologies, such as medical AI, medical extended reality (XR), and medical robotics. Furthermore, medical cloud computing will support the innovative transformation and operational execution of comprehensive health-related businesses, including medical insurance payments, pharmaceutical distribution, drug research and development, and population health management. From the perspective of health economics, medical cloud computing will enhance the efficiency of healthcare informatization, ensuring that it keeps pace with the broader transformation of the healthcare sector.

Based on this study, IDC believes:

1. Hospitals have largely and comprehensively adopted cloud computing technologies and their applications.

Hospitals have not only begun to adopt cloud computing capabilities such as cloud storage, cloud disaster recovery, big data, and scientific computing, but are also migrating their application systems to cloud computing platforms. Some hospitals in small and medium-sized cities have even proposed comprehensive cloud strategies, leveraging public or private clouds to fully support all hospital operations. The adoption of hybrid cloud models by hospitals is gradually becoming a trend, making multi-cloud management an emerging requirement for healthcare institutions.

2. In addition to providing IaaS capabilities such as cloud storage and cloud disaster recovery for hospitals, public clouds have also begun to offer PaaS services to medical institutions and healthcare IT vendors.

Including network databases, big data processing platforms, and artificial intelligence development platforms, these infrastructures support hospitals in deploying application systems on cloud platforms and developing new applications. Public cloud providers will leverage their respective strengths to compete; enterprises with abundant cloud computing resources deployed across China hold a competitive advantage, enabling them to more efficiently replicate successful experiences from individual hospitals to other regions nationwide. Some public cloud providers have gained a first-mover advantage by leveraging their extensive cloud resources to build dedicated clouds for hospital clients in multiple locations.

3. The delivery of healthcare services exhibits strong geographic characteristics, a feature that has fostered the development of private medical clouds.

Medical private clouds based on specific regions or cities are rapidly developing. These private clouds support various services, including internet-based healthcare, medical consortia, family doctor programs, health insurance payments, prescription sharing, and health management. They also host emerging systems such as artificial intelligence to enable telemedicine and regional healthcare services. Established vendors in traditional healthcare IT hold certain advantages in the medical private cloud sector, leveraging private cloud infrastructure not only to facilitate hospital upgrades and development but also to expand into diverse health and medical service offerings.

4. The future development of healthcare cloud computing will feature the simultaneous advancement of public and private clouds.

Public cloud services have gradually expanded from offering Infrastructure as a Service (IaaS) to Platform as a Service (PaaS), and further to Software as a Service (SaaS), enabling emerging application services such as imaging cloud platforms, telemedicine, and artificial intelligence. In contrast, private healthcare clouds initially took root by delivering SaaS-based application systems, then gradually expanded to provide IaaS services to healthcare institutions across entire regions, along with PaaS platforms that enable these institutions to develop and deploy more diverse application systems.

5. Competition between public cloud and private cloud vendors is currently still characterized by each party carving out its own territory, but the rivalry has already begun.

As the digital transformation of healthcare continues to advance, competition between the two is expected to intensify. In the early stages, competitors will be evenly matched; however, as the rivalry evolves, companies that make continuous progress in both “capabilities” and “strategy” will gain a competitive edge. Beyond competition, collaboration between public and private cloud vendors is also emerging as a trend. Such partnerships allow both parties to leverage their respective strengths, thereby securing a more advantageous position in the market.

“Xiao Hongliang, Senior Research Manager at IDC China’s Industry Research and Consulting Services Department, stated, ‘The importance of medical cloud in building the future healthcare service system has been recognized by hospitals, healthcare IT vendors, and various cloud providers. Medical cloud not only supports the development of new healthcare service systems but also promotes the application of emerging technologies such as healthcare big data and medical artificial intelligence.’”

Public cloud providers will continue to intensify their efforts in expanding medical cloud services, striving for greater initiative in supporting hospitals’ business transformation. Meanwhile, health IT vendors offering medical cloud solutions will accelerate the cloud-based deployment of their solutions, aiming to secure a stronger advantage as the entire healthcare sector migrates to the cloud. In future development, regardless of vendor type, continuous enhancement of cloud application capabilities and ongoing optimization of strategic planning will be essential to gaining a competitive edge.

Source: IDC