Comprehensive Analysis of 32 Medical Companies on STAR Market: Two Debut with Over 200% Peak Gains

After a wait of more than half a year, the STAR Market finally began trading this morning, with the first batch of 25 stocks officially listed.

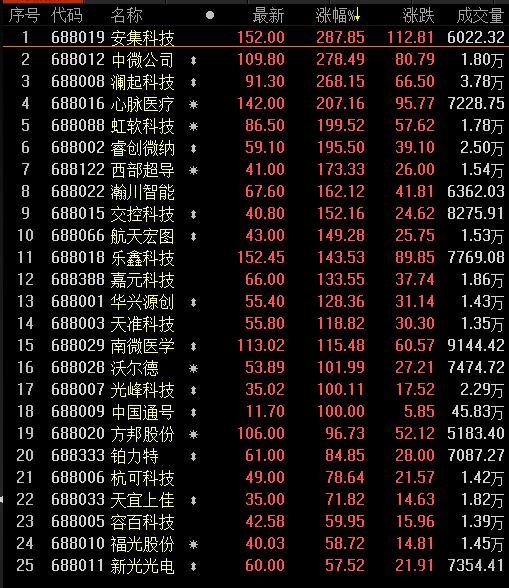

Starting from the call auction at 9:15 a.m., the prices of all 25 stocks surged significantly. At 9:16 a.m., Montage Technology posted the highest gain of 266.94%, while Xinguang Optoelectronics, with the lowest gain among the group, still rose by 30.01%. Subsequently, by 9:25 a.m., there were no major changes in the call auction results, as the gains for all 25 stocks continued to expand gradually.

At the opening, Anji Microelectronics Technology posted the highest gain, surging 287.85% or CNY 112.81, while XinGuang Optoelectronics recorded the lowest gain among those listed, up 57.52% or CNY 21.91. Two medical stocks, MicroPort Endovascular and NanWei Medical, ranked fourth and fifteenth, respectively, on the gainers’ list.

July 22, 9:29 a.m., the opening price of STAR Market stocks—a historic moment.

Trading officially commenced at 9:30 a.m. By the time VCBeat published this article (9:35 a.m.), the gains had moderated somewhat, with the peak increase reaching 203.34%. Notably, two healthcare stocks, MicroPort Endovastec and Nanwei Medical Technology, were both trading above their IPO prices. MicroPort Endovastec was priced at 118 yuan, up 155.25%, while Nanwei Medical Technology stood at 99.01 yuan, reflecting an 88.77% increase.

As of July 22, a total of 149 companies had submitted applications for listing on the STAR Market, with 28 having completed registration. Among the registered companies, three were in the medical sector, two of which went public today. VCBeat has reviewed the 149 applicant companies and identified 32 that are related to healthcare (excluding veterinary pharmaceutical products). We have downloaded the prospectuses of these 32 companies and extracted their operational data for analysis in the following sections.

Data Interpretation of the First 25 Listed Companies on the STAR Market

Starting in early July, the first batch of 25 companies listed on the STAR Market, which will make their debut on July 22, have successively completed their price inquiries. The highest issue price was RMB 62.60 for Espressif Systems, while the lowest was RMB 5.85 for China Railway Signal & Communication Corporation.

IPOs on the STAR Market are priced through market-based bidding, with the previous 23x P/E ratio cap removed, thereby moving valuation and pricing toward marketization. Although regulators have urged institutional investors to submit rational bids during the issuance process, they have refrained from administrative intervention. The registration-based IPO system is functioning effectively, allowing market investors to determine offering prices, which enables high-quality and high-potential companies to secure higher valuations.

The 25 companies in the first batch of listings had planned to raise RMB 31.089 billion, while the actual total amount raised reached RMB 37.0179 billion. For most companies, the funds raised based on the determined offering prices exceeded their originally planned funding requirements. The highest price-to-earnings (P/E) ratio was 170.75x for AMEC, and the lowest was 18.8x for CRSC. Meanwhile, CRSC was also the company that raised the most capital, totaling RMB 10.53 billion. The P/E ratios of most companies fell within the range of 35–50x, which is considered relatively reasonable.

Five companies have price-to-earnings (P/E) ratios exceeding 60x: Raytron Technology (79.09x), Advanced Micro-Fabrication Equipment Inc. China (AMEC, 170.75x), ArcSoft Corporation (74.41x), Western Superconducting Technologies (67.8x), and BLT (68.4x). The industries they operate in are optoelectronic devices, semiconductor equipment, visual artificial intelligence, titanium alloy manufacturing, and metal additive manufacturing (3D printing), respectively.

In the past, IPO pricing on the main board was relatively low, making subscription to new shares a virtually risk-free profit opportunity. However, on the STAR Market, market-oriented pricing has aligned valuations more closely with market consensus. As a result, consecutive daily limit-ups are no longer expected after listing, and there is even a possibility of shares falling below their issue price on the first trading day. As of press time, although the P/E ratios of these 25 companies have reflected higher valuations under the market-based pricing mechanism, investor enthusiasm remains high on the STAR Market’s inaugural trading day, driving share prices upward.

In this round of new stock listings, the online lottery success rate has remained basically at around 0.05%. Investors participating in online IPO subscriptions have shown great enthusiasm, suggesting that attention to the STAR Market may be increasing. However, after the listing on the STAR Market, investors have found that returns from IPO subscriptions have decreased, and losses may even occur. As a result, enthusiasm for IPO subscriptions will inevitably decline gradually in the future, leading to an increase in the lottery success rate.

STAR Market Prioritizes Tech Innovation Enterprises in Seven Key Sectors

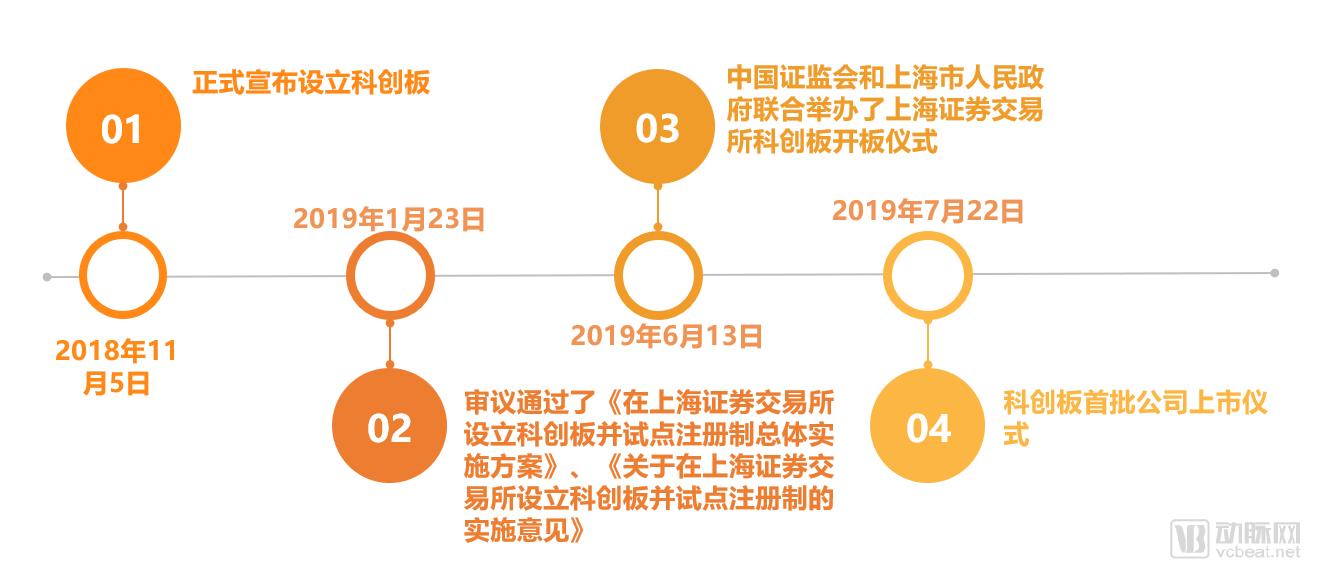

A review of the timeline for the launch of the STAR Market shows that it took just over eight months from the initial proposal to establish the board to the listing of the first batch of 25 companies, creating a miracle in the capital market.

On November 5, 2018, President Xi Jinping announced the establishment of the “STAR Market” at the opening ceremony of the first China International Import Expo. The STAR Market is designed to serve technology-driven enterprises that align with national strategies, possess core proprietary technologies, and enjoy broad market recognition.

On January 23, 2019, the Sixth Meeting of the Central Committee for Comprehensively Deepening Reforms reviewed and approved the Overall Implementation Plan for Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System, as well as the Implementation Opinions on Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System. On the 30th of the same month, the China Securities Regulatory Commission (CSRC) publicly solicited comments on the Measures for the Continuous Supervision of Companies Listed on the STAR Market (Trial) and the Administrative Measures for the Registration of Initial Public Offerings on the STAR Market (Trial). Relevant policies, laws, and regulations concerning the STAR Market were subsequently introduced.

On June 13, 2019, at the opening ceremony of the 11th Lujiazui Forum, the China Securities Regulatory Commission and the Shanghai Municipal People’s Government jointly held the launch ceremony for the STAR Market of the Shanghai Stock Exchange, marking a new first step for China’s capital market.

On July 5, 2019, the Shanghai Stock Exchange announced that, after more than eight months of efficient, orderly, and meticulous preparations, the initial batch of companies on the STAR Market had basically met the listing requirements and the timing was ripe; therefore, the listing ceremony for the first cohort of STAR Market companies would be held today (Monday, July 22, 2018).

The CSRC’s “Implementation Opinions” emphasize the establishment of a new Science and Technology Innovation Board (STAR Market) on the Shanghai Stock Exchange, adhering to the orientation toward the global technological frontier, the main battlefield of economic development, and major national needs. The board primarily serves technology-driven enterprises that align with national strategy, have achieved breakthroughs in key core technologies, and enjoy high market recognition.

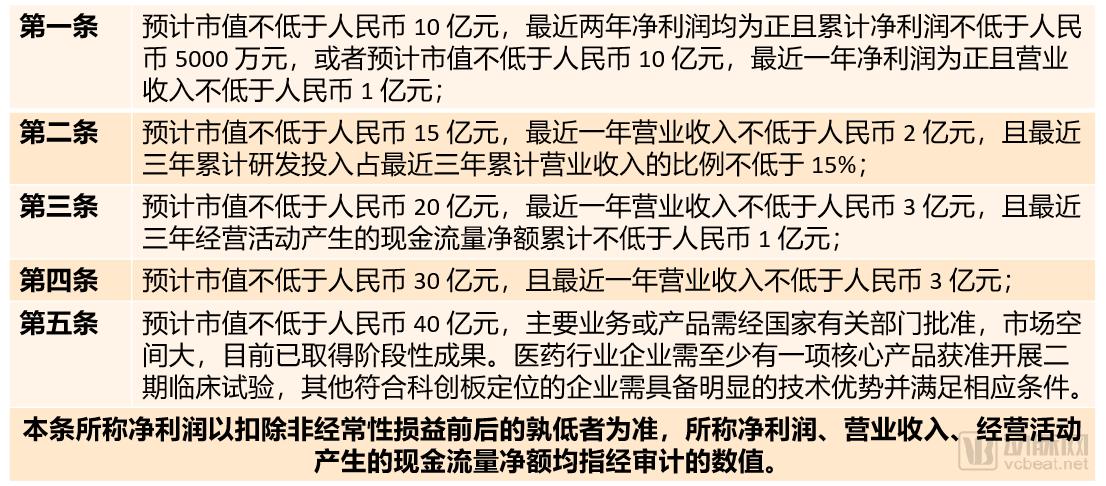

The STAR Market is required to provide key support for technological innovation enterprises in seven major fields of high-tech and strategic emerging industries, namely next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, and biomedicine, and has established five listing standards.

Listing standards incorporate market capitalization, with higher market cap corresponding to lower profitability requirements for companies.

The five listing standards of the STAR Market are established with company market capitalization as the core, combining market capitalization with corporate financial indicators such as revenue, cash flow, profitability, and R&D investment to form a set of inclusive listing conditions. Issuers applying for listing on the STAR Market must meet at least one of the five standards in terms of market capitalization and financial indicators. The prospectus and the listing sponsorship letter issued by the sponsor shall clearly specify the particular listing standard selected.

For companies with a market capitalization of RMB 1–1.5 billion, focus on profitability (higher than that of ChiNext/Main Board listings); for those valued at RMB 1.5–2 billion, prioritize R&D capabilities and investment; for firms in the RMB 2–4 billion range, emphasize market size; and for those exceeding RMB 4 billion, concentrate on core products and market potential, without imposing profitability requirements.Meanwhile, the STAR Market has also established reference financial standards for Red Chip companies and those with dual-class share structures.

Among these, the fifth set of listing criteria has drawn the most attention, as profitability is no longer a barrier to initial public offerings (IPOs). However, for pharmaceutical companies, additional requirements regarding R&D progress have been introduced, mandating that at least one core product must have received approval to initiate Phase II clinical trials. To date, Zeltalab and Bio-Thera Solutions have both chosen to go public under the fifth set of criteria; both are companies in the pharmaceutical manufacturing sector.

Overall, the STAR Market adopts the following requirements for enterprises:"The greater the market capitalization, the lower the profitability requirement."

Under the framework of the STAR Market, reasonable valuation remains the core of investment, whether in the secondary market or the primary market.

VCBeat primarily focuses on companies listed on the STAR Market within the healthcare and medical sectors; therefore, this article mainly analyzes the IPO performance of these enterprises. Among the first batch of 25 companies, two were medical firms: MicroPort Endovascular and Nanwei Medical.

MicroPort CardioFlow (688016)

MicroPort Endovascular, spun off from the Hong Kong-listed MicroPort Scientific Corporation, is primarily engaged in the research and development, manufacturing, and sales of interventional medical devices for arterial vessels. With a comprehensive product portfolio and strong market competitiveness, its flagship product is the thoracic endovascular stent graft system. The company has also actively expanded into the peripheral vascular intervention sector, leveraging years of deep expertise to offer products such as peripheral vascular stent systems and balloon dilation catheters. Notably, it possesses the only stent system approved for marketing in China that can be used in surgical procedures for type A aortic dissection.

MicroPort Endovascular’s performance has maintained rapid growth, with a clear business structure and strong profit margins. From 2016 to 2018, the company’s operating revenues were RMB 125.3267 million, RMB 165.1348 million, and RMB 231.1275 million, respectively, representing a compound annual growth rate (CAGR) of 35.8%. Net profits amounted to RMB 41.1411 million, RMB 63.3862 million, and RMB 90.6479 million, respectively, with a CAGR of 48.5%. Sales of aortic stent products accounted for approximately 80% of total revenue and increased year by year. Over the past three years, the gross profit margin remained above 70%, and the net profit margin exceeded 30%. MicroPort Endovascular applied for its initial public offering under the first set of listing criteria.

In its inquiry letter, the Shanghai Stock Exchange focused on questions regarding MicroPort Endovascular MedTech’s equity structure and the basic profiles of its directors, supervisors, and senior executives; core technologies; business operations; corporate governance and independence; related-party procurement with its indirect controlling shareholder; channel overlap; and R&D independence.

Prior to the determination of MicroPort Endovastec’s IPO price, certain securities firms projected its 2019 net profit attributable to shareholders of the parent company at approximately RMB 110 million, based on the company’s aforementioned financial performance. Using Lepu Medical and Double Medical—companies with similar business models—as comparables and applying the P/E valuation method, a P/E multiple of 27–35x was assigned, yielding a fair value range of RMB 43.88–56.88 per share. The actual IPO price of MicroPort Endovastec was RMB 46.23, positioned toward the lower end of this range, corresponding to a P/E ratio of 39.75x and a market capitalization of RMB 3.328 billion.

Micro-Tech (Nanjing) Co., Ltd. (688029)

Nanwei Medical is primarily engaged in the research and development, manufacturing, and sales of minimally invasive medical devices. Its main product lines include endoscopic minimally invasive diagnostic and therapeutic devices and tumor ablation equipment, forming three core product portfolios: endoscopic diagnostic and therapeutic products, tumor ablation products, and OCT technology-based products. The company’s quality and technology in its core areas—endoscopic diagnostic and therapeutic products, tumor ablation products, and EOCT products—are industry-leading. Currently, the company has developed 30 products across six major categories and eleven series, built upon 40 core technologies. From 2016 to 2018, products based on these core technologies generated revenues of RMB 328 million, RMB 534 million, and RMB 785 million, respectively, clearly demonstrating that core technologies are driving the company’s growth.

From 2013 to 2018, Nanwei Medical’s sales revenue and net profit attributable to parent company shareholders increased from RMB 169 million and RMB 24.89 million to RMB 922 million and RMB 193 million, representing a 5.5-fold and 7.7-fold increase, respectively, with compound annual growth rates (CAGR) of 40.39% and 50.58%, respectively. The company applied for its initial public offering under the first set of listing criteria.

Previously, a securities firm projected that Nanwei Medical’s 2019 revenue would reach RMB 1.212 billion, with net profit attributable to shareholders amounting to RMB 284 million. Based on a price-to-earnings (P/E) ratio of 30–40 times its 2019 performance, Nanwei Medical’s implied market capitalization ranged from RMB 8.52 billion to RMB 11.36 billion. Upon its actual listing, the market accepted a P/E ratio of 34.47 times, with a share price of RMB 52.45, resulting in a total market capitalization of RMB 6.994 billion.

MicroPort Endovastec and Nanwei Medical are both medical device companies, so they have comparable peers in the market. Lepu Medical, which also specializes in interventional medical devices like MicroPort Endovastec, has a P/E ratio of 30.54x. Meanwhile, these two STAR Market-listed companies enjoy market-accepted P/E ratios in the range of 35–40x, indicating relatively reasonable valuations.

Multidimensional Data Analysis of 32 Medical Companies Applying for Listing on the STAR Market

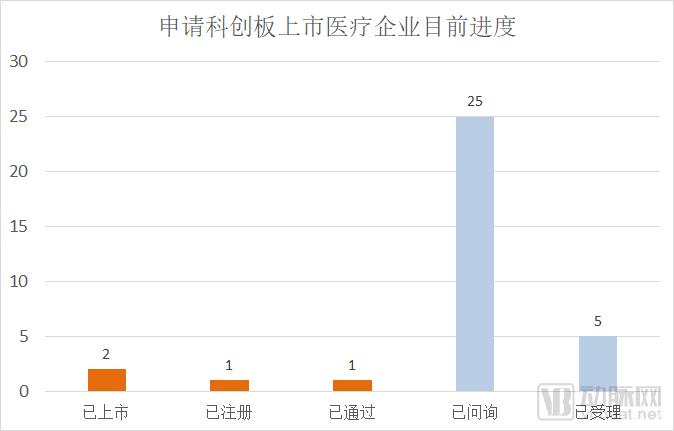

Listing Progress: 2 Companies Listed, 1 in Registration, 1 Approved

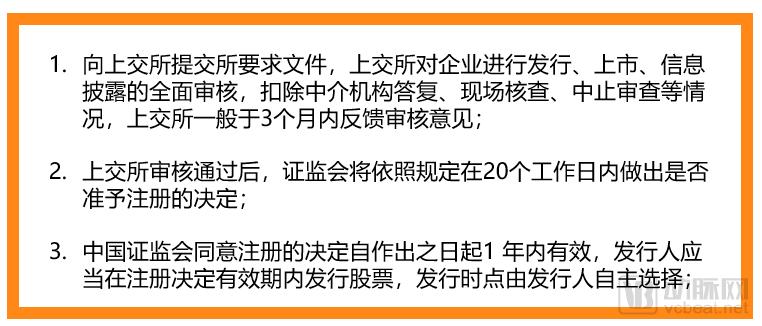

The “Implementation Opinions on Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System” clearly states that, under the registration-based review framework, it generally takes 6 to 9 months for a company to complete the entire process from submitting its initial public offering (IPO) application to final review and registration. The main steps are as follows:

The review period for the STAR Market is generally six months, with the Shanghai Stock Exchange’s review not exceeding three months, and the total time for issuers, their sponsors, and securities service providers to respond to inquiries not exceeding three months.

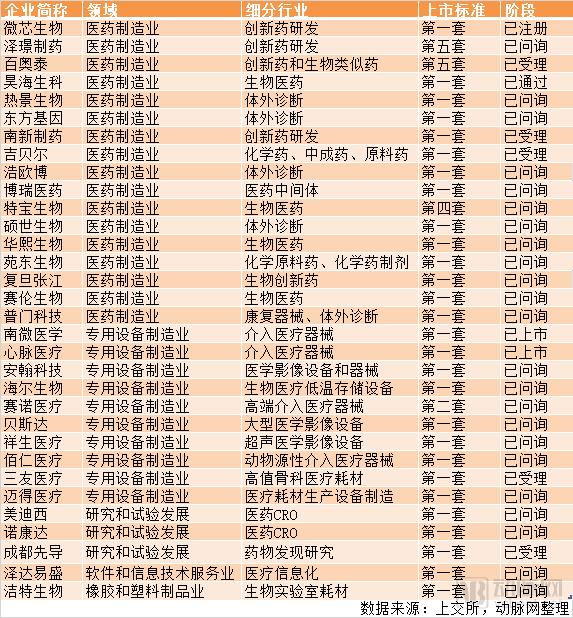

Among the 32 companies, in addition to MicroPort Scientific and Mindray Medical which are already listed, Chipscreen Biosciences, a highly anticipated innovative drug company, has completed its registration, while Haohai Biological Technology has passed the review.

Chipscreen Biosciences is primarily engaged in the research and development of innovative small-molecule drugs. Its nationally classified Class 1 original innovative drug, chidamide (brand name: Epidaza), has been launched and is marketed for the treatment of peripheral T-cell lymphoma. It is the world’s first subtype-selective histone deacetylase (HDAC) inhibitor.

On June 11, Chipscreen Biosciences made its debut as one of the first three companies to gain approval, following three rounds of in-depth inquiries. However, while many other companies had already obtained registration and confirmed their listing schedules within a month, Chipscreen Biosciences—the most closely watched by the market—had yet to secure registration, sparking widespread rumors. On July 17, the China Securities Regulatory Commission (CSRC) finally issued an official announcement approving the initial public offering (IPO) registration of Chipscreen Biosciences.

Haohai Biotech is an innovative enterprise engaged in the research and development, production, and sales of medical devices and pharmaceuticals by applying biomedical material technologies and genetic engineering techniques. Its main products include intraocular lenses, lubricating eye drops, hyaluronic acid, and recombinant human epidermal growth factor, which are applied across four major sectors: ophthalmology, medical aesthetics and wound care, orthopedics, and anti-adhesion and hemostasis.

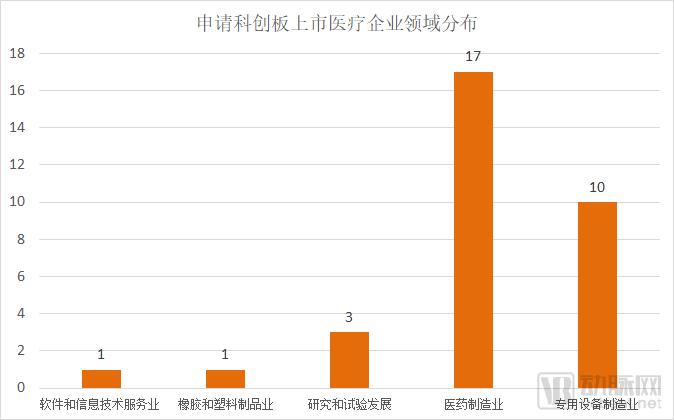

Pharmaceutical companies are the most numerous, followed by medical device firms.

Among the 32 healthcare companies, pharmaceutical manufacturers are the most numerous, primarily focusing on innovative chemical drugs, innovative biological drugs, and in vitro diagnostics. There are 10 specialized equipment manufacturing companies, mainly involved in medical devices and high-value consumables. Three companies operate in the field of research and experimental development, while one company each belongs to the software and information technology services sector and the rubber and plastic products industry. Jet Biofil, from the rubber and plastic products industry, primarily provides single-use plastic consumables for biological laboratories.

Two Pharmaceutical Companies Report Losses, While Eight Post Profits Exceeding 100 Million Yuan

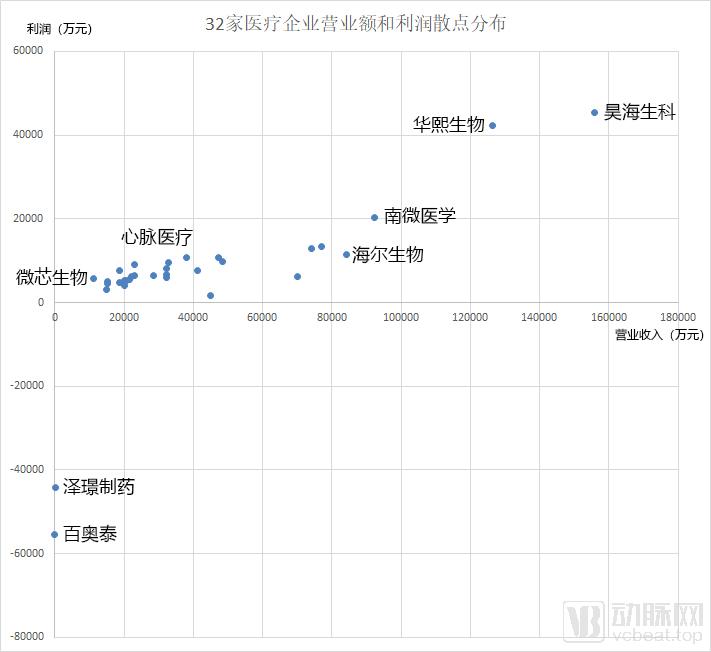

Among the 32 applicant companies, Haohai Biological Technology and Bloomage Biotechnology, which recorded the highest operating revenues in 2018, both surpassed RMB 1 billion, with net profits exceeding RMB 400 million. These two companies share a common characteristic: they are both manufacturers of sodium hyaluronate/hyaluronic acid, which is widely used in ophthalmology, orthopedics, and aesthetic products.

Eight companies reported net profits exceeding RMB 100 million, with four pharmaceutical companies and four medical device companies.

Pharmaceutical companies and in vitro diagnostic (IVD) enterprises boast relatively high gross profit margins, exceeding 80%. In contrast, medical device manufacturers have lower gross profit margins, ranging between 40% and 50%. Among the two CROs, Medicilon and Nuokangda exhibit significant differences in their gross profit margins. Medicilon’s gross profit margin stands at 36.13%, which is slightly lower than those of WuXi AppTec and Tigermed, though the gap is not substantial. Nuokangda, on the other hand, has reached a gross profit margin of 71.89%.

Although pharmaceutical companies generally enjoy high gross profit margins, their R&D expenditures are also substantial. Taking Chipscreen Biosciences as an example, its revenue in 2018 was RMB 147.69 million, with R&D spending accounting for 55.85% of total revenue. Similarly, the losses of RMB 400–500 million reported by Zeltz Pharma and Bio-Thera Solutions were primarily attributable to R&D investments. For some innovative drug developers, once their products are launched and generate revenue, the proportion of R&D expenditure relative to total revenue can drop to below 10%.

Two Loss-Making Pharmaceutical Companies Choose to List Under the Fifth Set of Criteria

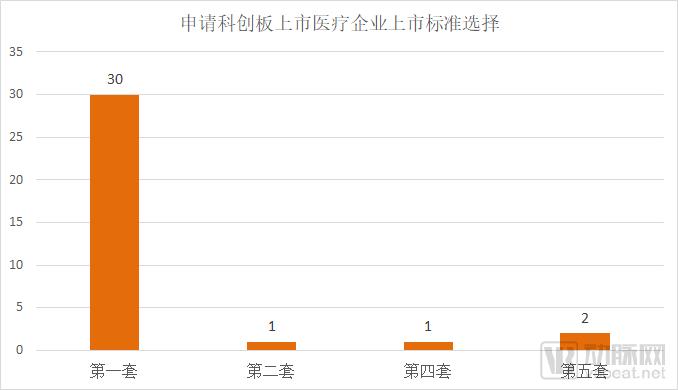

In terms of listing criteria, the vast majority of companies opted for the first set of standards, namely "market capitalization plus profitability." One company each selected the second and fourth sets of standards, while two companies chose the fifth set.

Currently, innovative drug R&D companies have substantial capital requirements but cannot achieve profitability in the short term, representing a typical niche sector characterized by significant upfront investment and substantial long-term potential. In other niche sectors, development timelines and costs are not as pronounced as those for innovative drugs. Consequently, to date, the two companies that have filed for listing under the fifth set of criteria are both pharmaceutical firms; neither has achieved profitability, nor do they yet generate operating revenue.

Another company that chose to list under the fourth set of standards is Amoytop Biotech. The fourth set of standards adopts the “market capitalization + revenue” listing criteria, requiring an estimated market capitalization of no less than RMB 3 billion and annual operating revenue of no less than RMB 300 million in the most recent year. Amoytop Biotech is engaged in the research, development, and industrialization of biopharmaceuticals centered on genetic engineering technology. It has four products on the market, including one national Class 1 new drug: Pegylated Interferon α-2b Injection (brand name: “Pegbin”), which is primarily used for the treatment of chronic hepatitis C and hepatitis B. The company also has three former national Class 2 new biological products—Telrise, Teljin, and Telkang—all of which are adjunctive chemotherapy agents. Although Amoytop Biotech achieved operating revenues of RMB 280 million, RMB 323 million, and RMB 448 million in 2016, 2017, and 2018, respectively, its net profits during these three years were only RMB 29.31 million, RMB 5.16 million, and RMB 16 million, respectively.

A review of Tobe Biopharmaceuticals’ financial statements reveals persistently high selling expenses, which reached RMB 266 million in 2018. In 2017, the company even experienced a situation where the growth rate of selling expenses outpaced that of operating revenue, a key factor contributing to its previous failed attempt to list on the ChiNext board. With the STAR Market lowering profitability requirements for companies, Tobe Biopharmaceuticals has filed for an IPO once again.

On the other hand, as an innovative pharmaceutical company, T&B Bioengine has an R&D investment ratio of less than 10% of its operating revenue. Whether it will pass the review remains subject to the CSRC’s opinion. On the evening of July 17, there was a glitch in the disclosure of the progress of IPO reviews on the STAR Market by the China Securities Regulatory Commission (CSRC). At that time, both T&B Bioengine and Sailun Bio were briefly shown as having their reviews suspended, before being reverted to the “under inquiry” status. It remains unclear what the final outcome will be.

Uneven R&D Investment

We have observed that some pharmaceutical companies maintain R&D investments as low as less than 5% of their revenue. For instance, Jibeier relies primarily on its leukocyte-promoting drug, Likjun tablets, for main income. According to its annual reports, the R&D expenses from 2016 to 2018 were RMB 16 million, RMB 17 million, and RMB 19 million, accounting for 3.77%, 3.79%, and 4.04% of the operating revenue during the same periods, respectively—figures significantly below the average level of companies listed on the STAR Market. Nanxin Pharmaceutical’s R&D investment is also relatively low; however, it has managed to launch one innovative drug and maintains a pipeline comprising three innovative drugs and two improved new drugs under development. It remains uncertain whether pharmaceutical companies with such low R&D investment will ultimately pass the regulatory review.

We have reviewed the R&D pipelines of pharmaceutical companies. Based on current drug pipelines, two unprofitable pharmaceutical companies have a relatively large number of drugs under development. Bio-Thera Solutions has 21 projects in its pipeline, among which one product (the adalimumab biosimilar BAT1406) has submitted a marketing application and is expected to be approved for launch by the end of 2019; four products (the bevacizumab biosimilar BAT1706, the ADC drug BAT8001, the tocilizumab biosimilar BAT1806, and batifiban BAT2094) are in Phase III clinical trials; one product is in Phase II clinical trials; and four products are in Phase I clinical trials.

Zelgen Biopharmaceuticals has 23 ongoing R&D projects covering 11 innovative drugs. Among these, multiple indications for donafenib tosylate tablets, topical recombinant human thrombin, and itacitinib hydrochloride tablets have entered Phase II/III clinical trials, respectively. Ocaratuzumab and recombinant human thyroid-stimulating hormone for injection are in Phase I clinical trials. The IND application for itacitinib hydrochloride cream has been submitted, while itacitinib hydrochloride tablets for the treatment of autoimmune-related diseases and ZG5266 are in the preparation stage for IND applications. In addition, the small-molecule new drugs ZG0588 and ZG170607, as well as the novel anti-tumor dual-target antibodies ZG005 and ZG006, are in the preclinical development stage, with IND applications expected to be submitted in 2020–2021.

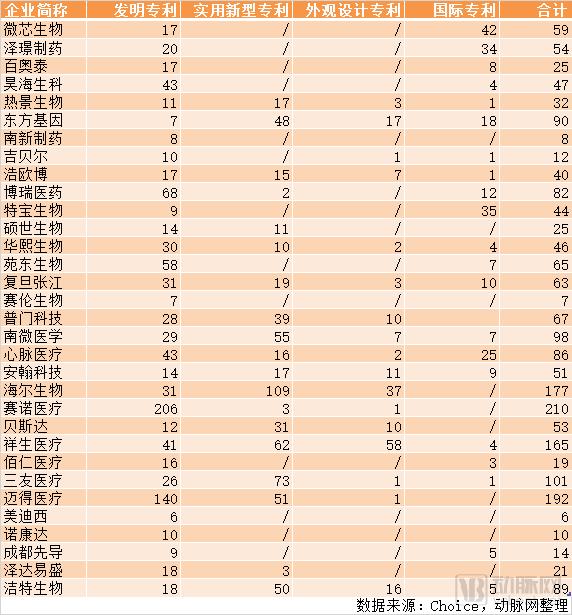

The purpose of establishing the STAR Market is to implement the innovation-driven development strategy. A basic requirement for listing on the STAR Market is that enterprises possess core technologies with independent intellectual property rights, which continuously drive revenue growth. The intellectual property status of STAR Market-listed companies will directly affect their operational efficiency and impact the interests of a broad base of investors. Characterized by high technology and high risk, these companies are also prone to patent disputes. The lack of core patents is a significant weakness for many companies undergoing initial public offerings (IPOs).

We compiled patent data for 32 medical companies. Sino Medical Sciences Technology holds the largest number of patents, totaling 210, most of which are invention patents. In terms of international patents, Chipscreen Biosciences has the highest count, with 42 patents. Design patents are of limited significance and are primarily filed by medical device companies for the instruments and equipment they manufacture.

How to Value Unprofitable Pharmaceutical Companies

The medical device and biopharmaceutical industries comprise numerous subsectors. For instance, the medical device sector can be broadly categorized into high-value consumables, low-value consumables, medical equipment, and in vitro diagnostics (IVD). Subsectors such as low-value consumables, medical equipment, biochemical diagnostics, immunodiagnostics, and point-of-care testing (POCT) have developed relatively stably, with most companies achieving profitability; thus, the price-to-earnings (P/E) ratio is a suitable valuation metric. In contrast, certain high-value consumable segments face profitability challenges due to substantial R&D investments, making the price-to-sales (P/S) ratio a more appropriate valuation approach.

Although MicroPort Endovascular and Nanwei Medical operate in the high-value consumables sector, both companies possess core technologies that ensure stable revenue and profitability, and have therefore opted for the first set of listing criteria. Their market capitalizations can be reasonably estimated based on the price-to-earnings (P/E) ratios of comparable companies in the main board market.

Valuation is particularly challenging for pharmaceutical companies in the pharmaceutical manufacturing sector, especially for Zeltigen Pharmaceuticals and Bio-Thera Solutions, which both went public under the fifth listing standard. In December 2018, Zeltigen Pharmaceuticals completed its last capital increase prior to its IPO, resulting in a post-money valuation of approximately RMB 4.756 billion. This valuation was primarily based on multiple factors, including the progress of drugs in its current R&D pipeline, the market size of the targeted indications, and the competitive landscape of its products. Currently, the status of Zeltigen Pharmaceuticals’ application on the STAR Market is shown as “under inquiry,” with responses to the inquiries yet to be submitted.

“The Dawn of a New Era for Pharmaceutical Innovation Companies”

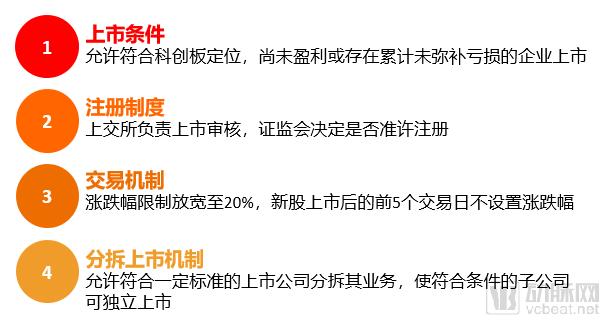

VCBeat has compiled all the relevant detailed rules, and we outline the four major characteristics of the STAR Market:

Innovative medical technology companies require substantial long-term investments in talent and capital during their early startup stages. These enterprises often face a predicament characterized by an inability to achieve profitability in the short term, difficulties in securing financing, and a lack of profitable products, despite their offerings possessing explosive market potential. The fifth listing standard imposes certain requirements only on the core qualifications of pharmaceutical companies, without mandating profitability. This has established a new channel for equity financing and public listing for high-quality, pre-profit enterprises.

For pharmaceutical companies, the journey of an innovative drug from research and development (R&D) to clinical trials and finally to the patient market can take anywhere from a few years to over a decade. The STAR Market’s fundamental principle of “prioritizing R&D” provides financial support to companies with market potential, enabling them to successfully navigate the clinical R&D phase and address survival challenges in their early stages of development. Notably, the fifth set of criteria in the STAR Market’s detailed rules specifically stipulates that pharmaceutical companies must have at least one core product approved for Phase II clinical trials, while other companies aligned with the STAR Market’s positioning must demonstrate significant technological advantages and meet corresponding requirements.

Excluding innovative pharmaceutical companies, many niche sectors—such as precision medicine and gene sequencing—face survival challenges characterized by high upfront investments and low initial returns. The establishment of the STAR Market will help these enterprises secure financial support for development, enabling them to focus wholeheartedly on increasing early-stage R&D investment, thereby significantly enhancing the viability of high-quality, innovative healthcare companies.

Overall, the launch of the STAR Market provides effective capital support for a cohort of high-quality, innovative medical enterprises with strong technical capabilities and expertise, thereby leveraging financial instruments to accelerate the development of the healthcare industry. It also encourages companies to increase their R&D investment, drive transformation and upgrading, establish technological barriers, and enhance market competitiveness. By establishing a valuation framework for pre-profit companies, it reshapes the overall landscape of the healthcare sector. Key areas prioritized for accelerated growth include innovative drugs, precision medicine, biotechnology, and innovative medical devices.