BV Industrial Intelligence White Paper: Transforming Industrial Efficiency through AI-Driven Solutions and Operational Innovation

1.1 Industrial intelligence refers to cost reduction and efficiency enhancement, transformation of production organization methods, or reconstruction of industry efficiency models driven by technology.

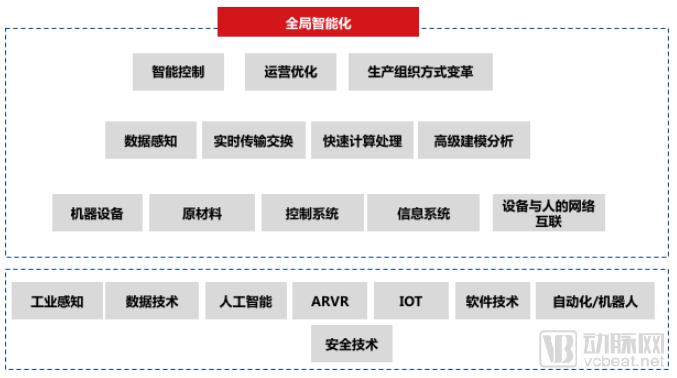

What we refer to as industrial intelligence focuses on products or technological solutions that can drive cost reduction and efficiency improvement, as well as transform production organization methods, along with operational opportunities arising from the transformation and reengineering of efficiency models. Industrial intelligence is built upon technologies such as industrial sensing, IoT, AI, data, software, and robotics, to achieve globally semanticized intelligent perception, control, scheduling, and decision-making.

Through these measures, it may be possible to optimize and transform existing equipment, processes, factories, and supply chains to achieve the goals of improving quality, reducing costs, increasing efficiency, or changing production organization methods. It is also possible that new intelligent equipment, new processes, new OEMs, new forms of supply chain organization, and even new product categories will emerge.

However, the transformation of efficiency models is not an overnight achievement across industries. The industrial sector will undergo a gradual intelligent transformation in the process of digitalization and informatization. This article systematically reviews the opportunities for improving operational and commercial efficiency brought about by technological changes in the industrial supply chain, and analyzes the value of the data industry chain from the perspectives of data, models, and decision-making.

Figure 1 Overview of Industrial Intelligence Technologies

1.2 Forms and Business Model Evolution of Industrial Intelligence: Strong Solution-Oriented Vendors & Operation-Centric Clients

What are the forms and business models of industrial intelligence achieved through technological means? This article attempts to elaborate on and analyze the directions and possibilities of industrial intelligence from the perspectives of a technology and industry observer, as well as an industry investor. As summarized in the figure below, the manifestations of industrial intelligence may include hardware, software, business systems, algorithms, platforms, and solutions. In terms of business models, it may emphasize solution provision, with the ultimate path being to become a major service provider; alternatively, it may leverage robust operational models to recreate new clients or emerge as a new type of client.

Figure 2 AI-Enabled Opportunities: Solutions or Heavy Operations

Yet, with a proliferation of platforms, where do opportunities lie for startups? Amidst numerous niche sectors, which fields offer significant potential? Should the focus be on solution provision or operational services? This article seeks to identify investment and entrepreneurial opportunities by analyzing platforms, reviewing technological configurations and industry selections, deconstructing factories, segmenting industrial chains, and examining data flows. The key findings are summarized as follows:

Figure 3 Future Directions and Development Possibilities of Industrial Intelligence

1. Platform-based enterprises are not monopolistic; mutual empowerment is timely and appropriate

In recent years, numerous industrial internet platform-level enterprises have emerged in the market. However, the industrial sector is highly fragmented, with significant variations in industry-specific attributes and characteristics across different segments. Consequently, no single model or technology can serve as a universal solution applicable to all scenarios. The logic behind technology application and the formation of a viable commercial closed loop may require the participation and validation of individuals or companies with diverse technological and industrial backgrounds.

Taking some of China’s earlier industrial internet platforms as an example, these platforms, shaped by the endowments and characteristics of their parent companies or original enterprises, inevitably bear the imprint of those legacy organizations.

For instance, Genyun Interconnect establishes control over the entire equipment lifecycle and builds an industrial cloud platform based on the Internet of Things (IoT) for devices. Centered on SANY Heavy Industry’s global product sales, it leverages IoT, big data, and artificial intelligence technologies to innovate its business model, extending these capabilities to other equipment and industries.

Haier’s CosmoPlat is a user-centric flexible manufacturing platform. Unlike the intelligent upgrading and transformation of factories under Germany’s Industry 4.0 framework, CosmoPlat focuses not only on operational efficiency within plants but also places greater emphasis on enhancing business efficiency. Through CosmoPlat, zero inventory for certain product categories and large-scale customization with controllable costs have been achieved. Furthermore, it seeks to extend the systematic mass customization capabilities developed in the home appliance sector to other industries, such as ceramics and textiles and apparel.

Leveraging Foxconn’s extensive customer base, long-standing and stable strategic partnerships, as well as its industrial and supply chain advantages driven by economies of scale, Industrial Fulian, a newly listed company, aims to extend its reach across the upstream and downstream segments to build an industrial internet platform. Judging from its business progress since the IPO, the company has begun to make significant strides in areas such as tooling prediction and process optimization.

Compared with emerging industrial internet platforms in China, GE Predix and Siemens MindSphere are among the earliest international platforms to apply concepts such as the industrial internet and big data to industrial applications. From a historical development perspective, they have continuously enriched their product portfolios, solutions, and industry verticals through various mergers and acquisitions.

In addition to long-established giants such as Siemens and GE, as well as emerging industrial internet platforms, traditional software vendors and system integrators are also seeking transformation and strategic positioning in the direction of the industrial internet, including Yonyou, Hand Enterprise Solutions, Bonc, and Baosight.

Another category is represented by internet or technology companies with strong B2B capabilities in China, such as Alibaba Cloud and Huawei. Alibaba Cloud’s ET Industrial Brain has been extensively applied in process industries, including steel, petrochemicals, and energy. The Tao Factory platform primarily provides manufacturing and supply chain capabilities to Taobao merchants. However, these companies aim to offer more generic, foundational, and standardized capabilities. Within their ecosystems, they also require greater collaboration with solution providers that possess in-depth industry-specific know-how and algorithms.

So-called platforms aim to build a more open and expansive ecosystem to empower a greater number of industrial enterprises. However, China’s industrial internet and industrial intelligence are still in their early stages. Large platform companies represent only the tip of the iceberg, and significant differences in industry-specific know-how persist, leaving ample opportunities for entrepreneurs.

2. Great Potential in Deeply Developing Vertical Industrial Intelligence Systems for Niche Industries

"Industry" is a broad concept, with significant variations across different sectors. Process industries and discrete manufacturing differ notably in terms of production automation levels, data availability, and industrial complexity, leading to distinct opportunities in each. The most prominent commonality, however, is that every scenario has unique requirements; entering any specific niche demands deep industry know-how and strong capabilities in integrating upstream and downstream resources. Intelligent transformation needs may also vary across different industries.

The advantage of this characteristic is that, at the level of industrial services, it prevents the formation of monopolies by traditional large enterprises, while creating platform-level opportunities in various niche segments. From discrete to hybrid and then to process manufacturing, from products to services, and from production to management, there are diverse opportunities for intelligent transformation.

There are numerous technological approaches available for selection and configuration, each varying in maturity and level of advancement. What constitutes a valuable opportunity, and how should one make informed choices? This article attempts to provide a logical framework for addressing these questions.

Integrating the aforementioned technologies with industry-specific functions and segments can give rise to corresponding business models and entrepreneurial opportunities.

Figure 4. From Discrete to Continuous: Opportunities in Technology and Industry Allocation

To illustrate, intelligent transformation holds potential across various industries, presenting opportunities either in solution sales or in operational models.

• Integrated Production, Supply, and Marketing in B2C Product-Oriented Industries: B2C products typically require customization and flexible manufacturing, as seen in sectors such as textiles and apparel, food and beverages, and home appliances. The B2C segment is relatively fragmented with low market concentration due to differentiated demands and products, presenting opportunities to create new product categories, establish new distribution networks, and increase market consolidation. Achieving this may involve the integration of big data, production scheduling, operations research optimization, flexible production line retrofitting technologies, and various industrial software solutions.

• High energy-consuming process industries: Industries such as steel, non-ferrous metals, chemicals, and ceramics are highly cyclical, vital to national welfare and people's livelihoods, and characterized by large scale. These sectors often face overcapacity issues, with energy consumption accounting for a significant portion of their costs. Consequently, there is strong demand for solutions in areas such as sensing, real-time monitoring, and energy efficiency. This presents an opportunity to emerge as a major solution provider.

• Equipment manufacturers: Leveraging edge computing and industrial Internet of Things (IIoT) technologies, equipment manufacturers have the potential to transform their business models, creating significant added value in areas such as sales service efficiency and capital efficiency.

• Semiconductor and display panel industries: While these sectors already exhibit high levels of precision and automation, the localization rate of their supply chains remains low. Improving yield rates significantly enhances the value-added of the entire industry.

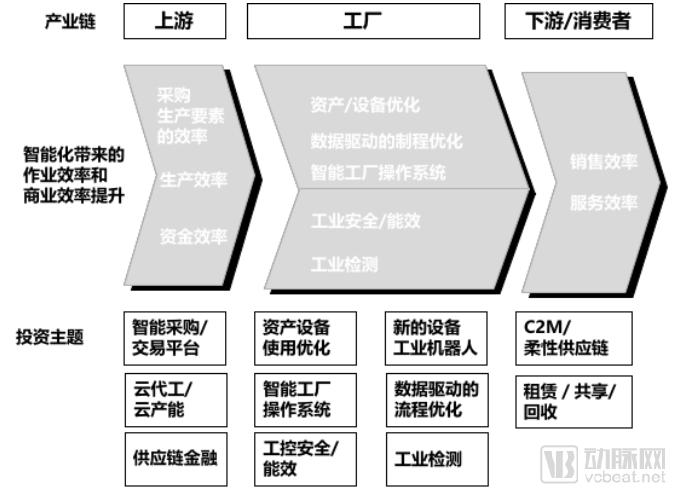

From the perspective of a single industry’s value chain, where should we begin and find our entry point? By aligning with the strategic directions of major suppliers (“Party B”) and emerging buyers (“Party A”), the author, through systematic research and investment practice, has identified opportunities for improvements in operational efficiency and commercial efficiency driven by technological transformations both along the industrial value chain and within factories. These are briefly summarized as follows:

Figure 5. Worldview of Industrial Intelligence

3.1 Intelligent Opportunities for Assets/Equipment

3.1.1 Industrial Robots and Intelligent Equipment

From the perspective of equipment and assets, factories with varying levels of informatization and automation all have demands for asset upgrades and iterative renewal. In recent years, a number of rapidly growing new integrators and original equipment manufacturers (OEMs) have emerged. Meanwhile, in terms of product systems, new demands and teams focused on parallel and collaborative operations have appeared, while emerging technologies such as human-machine integration, bionics, and self-adaptation continue to proliferate. We believe that robotics itself represents a significant systemic investment opportunity, spanning from the industrial chain to various niche segments; further elaboration will not be provided here.

Another direction is the intelligentization of equipment. While automation levels in certain industries and factories are already relatively high, there remains significant room for technological breakthroughs in the equipment and assets themselves. By leveraging technologies such as industrial vision, big data, and computer simulation, equipment can achieve greater adaptability, self-calibration, and autonomy. Furthermore, the extension of equipment capabilities into manufacturing processes and their integration with production lines can further enhance product yield rates.

3.1.2 Equipment Fault Prediction and Health Management (PHM)

Traditional original equipment manufacturers (OEMs) have not paid sufficient attention to after-sales service issues arising from equipment and product sales. While the three major aero-engine manufacturers—GE, Rolls-Royce, and Pratt & Whitney—have performed well in the realm of Prognostics and Health Management (PHM), a large number of mechanical equipment manufacturers lack the inherent capability to provide PHM services. From the perspectives of data acquisition and analysis, fault diagnosis and prediction for equipment integrate algorithmic capabilities, engineering expertise, and an understanding of complex mechanistic models, posing significant technical challenges for traditional equipment manufacturers.

From a technical perspective, performing feature extraction on the edge and training models in the cloud is a validated approach; however, teams with such capabilities are relatively scarce in the market. Take Uptake in the United States as an example: leveraging predictive health management (PHM) for Caterpillar’s internal combustion engine products, it rapidly grew into a multi-billion-dollar unicorn within a few years. Another representative case is Vestas, the world’s largest wind turbine manufacturer. Starting from manufacturing, Vestas retrofitted its wind turbines by deploying sensors across all components. Since 2016, its service revenue has exceeded equipment sales revenue, successfully transforming the company into a wind turbine service provider.

In terms of market size, China has 1,000 steel blast furnaces, 470,000 coal-fired boilers, 2 million CNC machine tools, 300,000 large and medium-sized air compressors, and 50,000 internal combustion engines, along with a vast number of pumps and other mechanical equipment. However, the overwhelming majority of these devices, products, and equipment have not taken health management into consideration.

However, three factors have constrained development in this direction: first, AI technology fails to integrate effectively with industrial know-how, and most teams lack relevant engineering experience; second, the high cost of computing power prevents asset owners from obtaining cost-effective predictive solutions; and third, the scarcity of failure data and annotations makes it impossible to employ classical deep learning approaches for prediction.

Predictive maintenance was a highly discussed topic at this year’s Hannover Messe. Tech giants, traditional industrial software vendors, equipment manufacturers, and numerous specialized startups have all entered this field. From the perspective of the European market, predictive maintenance represents one of the more practical application scenarios for industrial AI and the Industrial Internet of Things (IIoT). Given factors such as high labor costs, the business case for predictive maintenance is compelling; for instance, while a single on-site inspection and maintenance visit can cost €300 per technician, predictive maintenance can significantly reduce or even eliminate this expense. Equipment manufacturers are also actively embracing this technology and attempting to transform their business models. A notable example is the collaboration between Dürr Group and Software AG, which helps Dürr shift from equipment sales toward service-oriented offerings.

3.1.3 Business Model Transformation through IoT Integration

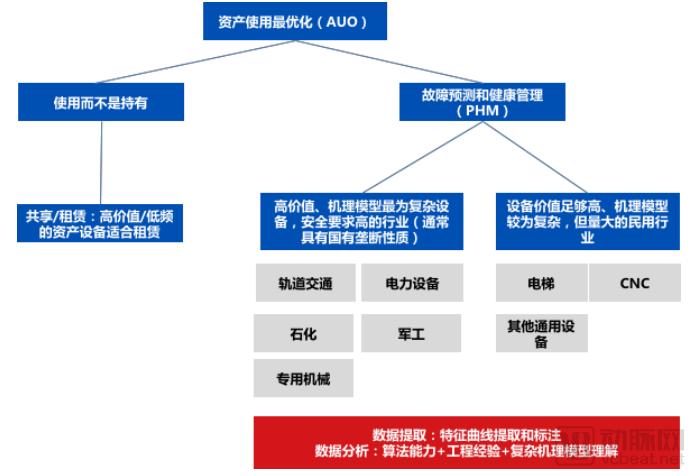

From the perspective of equipment utilization, the Party A can opt for usage rather than ownership through sharing or leasing models. Meanwhile, by integrating long-term data extraction and analysis, business models from insurance and finance can be incorporated. For instance, Yard Club, a U.S.-based construction equipment leasing platform, was acquired by Caterpillar. In China, companies such as Rootcloud, XCMG Information, and Zoomlion Cloud Valley have also implemented practices in equipment financing and insurance.

From the perspective of capital demand, some domestic financial institutions are also seeking opportunities for the financial leasing of intelligent devices such as robots. Leasing models based on precise IoT monitoring and data services may bring new industrial growth opportunities to the intelligent device sector.

Integrating business model transformations related to PHM and IoT, we have summarized the following technological changes and innovation opportunities.

Figure 6. Diagram of Asset Utilization Optimization

3.2 Algorithm- and Data-Driven Process Optimization to Build a Novel Scheduling Decision-Making System

Beyond individual devices, large-scale clients are also seeking diverse process optimization solutions. However, significant variations exist across different industries, and even within the same industry, processes are often complex, involving physical, chemical, and biological changes. By leveraging data analytics, optimizations of raw materials, equipment, and processes are implemented to achieve improvements in quality, efficiency, and energy conservation.

We have systematically reviewed various industries, ranging from discrete manufacturing to continuous manufacturing, and conducted comparative analyses across dimensions such as market size, level of informatization, potential for capability enhancement, and capacity expansion. We have identified several manufacturing processes that present significant market opportunities and potential for technological empowerment.

BV has also expanded into the 3C, environmental protection, and steel sectors, targeting companies involved in process optimization. For instance, in mobile phone manufacturing, dozens of processes—such as molding, stamping, alloy processing, coating, and surface treatment—are involved, each offering room for optimization through data and algorithms. The ultimate goal is to develop a new scheduling decision system with AI closed-loop control and an intelligent factory operating system.

Past expert systems were largely mechanistic models, but data-driven decision-making must ultimately be integrated with process engineering and mechanistic models. This is also why a universally applicable general-purpose platform has not emerged in the industrial sector.

Some investors have raised concerns about the non-standard nature of manufacturing processes, as these non-universal requirements and scenarios have, to some extent, limited the speed of replication and the realization of economies of scale. To reiterate, we are seeking two types of investment opportunities in the field of industrial intelligence: solution providers and operators. During the era of informatization and automation, many industries—such as consumer electronics (3C), steel, and petrochemicals—gave rise to multiple publicly listed companies. In terms of market size, many industries in the age of intelligence can similarly support the emergence of several major solution providers or operators. Our core focus is to identify promising industries, teams that combine emerging technologies with a deep understanding of industrial scenarios, and solutions that can truly transform and enhance industry efficiency models.

In addition to industry-specific processes, and in light of the common demands for integration with technologies such as the Internet of Things (IoT), data, and artificial intelligence (AI), I would like to highlight three further aspects: design, security, testing, and energy efficiency.

3.2.1 Design + AI

Industrial simulation is inherently linked to machine learning. To achieve optimal practices in design, assembly, and operation and maintenance, new types of intelligent industrial simulation software are required. CAD and CAE constitute a vast ecosystem, comparable to Android and iOS. Major players such as Siemens and Dassault Systèmes are actively strategizing and acquiring optimization algorithms and solvers in various domains, including fluid dynamics, thermal management, and vibration mechanics. Their software and plugin products are widely used across industries such as automotive, aerospace, mechanical equipment, and consumer electronics (3C).

However, no software company in the Chinese market has yet achieved significant scale in design. The substantial growth potential may lie in integrating models such as mass customization and flexible supply chains to capture demand data, leveraging advanced software simulation and AI technologies for seamless integration, rapidly producing marketable products, directly entering the operational domain, reinventing new product categories, and restructuring the supply chain.

3.2.2 Necessity and Value of Safety Elements

In the transition toward an era of industrial intelligence, a vast number of machines, equipment, and stations are inevitably dispatched through systems such as DCS and SCADA. Beyond traditional industrial software, numerous emerging business scheduling and decision-making systems have come to the fore. As human intervention diminishes, rigorous safety control becomes increasingly indispensable.

In the field of industrial safety, procurement in China was previously dominated by monopolistic enterprises driven primarily by compliance or classified protection requirements. In recent years, however, the market has gradually shifted from policy-driven to market-driven dynamics. Teams with robust product capabilities and the ability to parse diverse industrial control protocols are poised to rapidly emerge as leaders. These entities will continuously iterate their product lines and build reserves for next-generation security solutions that integrate data and AI.

U.S. industrial cybersecurity firm Claroty has secured investments from industrial giants such as Rockwell Automation, Siemens’ venture capital arm Next47, and Schneider Electric, gaining support for its work in the parsing of industrial control protocols and the convergence of operational technology (OT) with information technology (IT). The company has also attracted interest from financial investors including Temasek.

3.2.3 The Intersection of Energy Efficiency and AI

Energy is one of the major costs for many industrial enterprises. In process industries such as steel, oil, cement, and environmental protection, energy consumption accounts for a significant portion of corporate costs. Traditional Laboratory Management Systems (LMS) have played a certain role in energy efficiency management but have limited capabilities in optimization. Some research institutions possess numerous mechanistic models and control logic that achieve certain energy-saving effects. The new opportunity lies in the further integration of these mechanistic models with AI.

On the other hand, with the gradual reform and marketization of the electricity market and the deregulation of industrial and commercial electricity consumption, diverse participants have entered this market. We also anticipate that technology and data will generate a certain “catfish effect,” helping enterprises reduce costs and improve efficiency.

3.2.4 Common Requirements and Non-Standard Characteristics of Industrial Inspection

Leveraging computer vision technology to enhance the efficiency of inspection processes is not a new concept, with companies already active in sectors such as 3C display panels, cover glass, lithium-ion batteries, wafers, and pharmaceuticals. However, significant challenges remain, including non-standardized requirements, high development costs, and long lead times for machine vision systems. Additionally, algorithms and software often suffer from poor usability and a steep learning curve. Technical hurdles related to high precision, high dynamics, and high reflectivity also persist. Nevertheless, substantial opportunities will inevitably arise for companies that can develop a more universal platform and address the challenge of low-cost, scalable replication across industries.

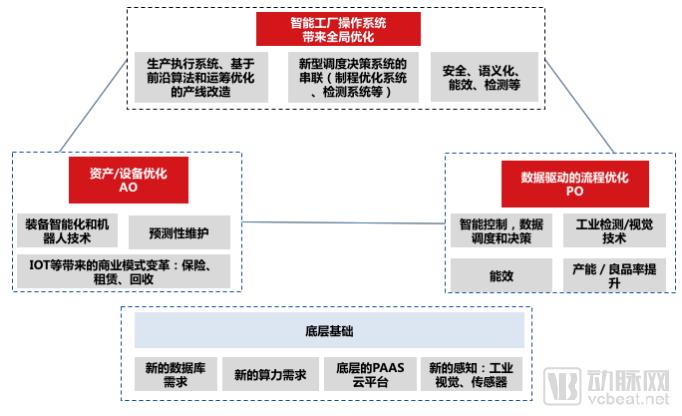

If equipment represents points and processes represent lines, let us examine the transformative opportunities of intelligence at the plane level. The ideal state of an intelligent operating system is achieved by linking segmented process optimizations, supplemented by industrial software, advanced sensing technologies, automation technologies, and robotics, to realize globally semantic scheduling and decision-making. From the perspective of factory operations, we focus on improving operational efficiency. We evaluate investment opportunities in factory intelligence across three layers: assets/equipment, processes, and the Factory Operating System; with databases, edge computing, PaaS, and new sensing technologies serving as the foundation for intelligent transformation.

Figure 7. Architecture of the Smart Factory Operating System

4.1 Integrating Manufacturing Execution to Capture Business Data: The Value of MES

The Advanced Manufacturing Research (AMR) institute defines MES as “a management information system oriented toward the shop-floor layer, situated between upper-level planning management systems and lower-level industrial control systems.” Overall, the penetration rate of MES in China remains relatively low.

MES products exhibit strong industry-specific and customized characteristics. Leading products and technologies are predominantly held by foreign enterprises, such as Rockwell, Siemens, and GE, which have further expanded their industry coverage through mergers and acquisitions. In the field of semiconductor software, leading technologies are controlled by foreign companies like Applied Materials. Looking at the historical development of some domestic enterprises, they have either grown by relying on highly concentrated industries, such as Baosight and Sinopec Yingke, or failed to scale up due to product-specific limitations. Meanwhile, teams with the capability to develop robust MES products remain scarce in China. Nevertheless, we believe that MES, as the foundation of intelligent factory operating systems, will be indispensable in the future.

There are two layers of investment logic here. The first is whether the company can become a large-scale solutions provider. MES companies offer value in three aspects:

- First, customer barriers: High customer stickiness in niche industries makes accumulation difficult; medium-to-large clients and foreign enterprises prioritize service quality and stability, typically establishing long-term, stable partnerships with service providers.

Second is industry understanding: being close to users, understanding business logic, and potentially undertaking certain custom development;

3. Advantage of Scenario-Based Data: Leveraging accumulated data and applying data science to transform efficiency models;

The second investment thesis considers whether there is strong product potential and feasibility for cloud migration. Leading MES vendors such as Rockwell, GFOS, and ITAC Software all regard the cloud as the future direction of development. They are actively discussing IoT platforms, migrating data to the cloud, and expanding from manufacturing execution toward areas like workflow collaboration and security. Against the backdrop of China’s industrial internet, this trend is also evolving progressively.

MES is a system that connects factory operations and manufacturing processes, but it faces development bottlenecks such as high customization requirements and long implementation cycles. Overall, the penetration rate of MES in China remains relatively low. However, as the foundation of intelligent operating systems, MES bridges the management layer with the production layer (industrial control), enabling global data analysis, scheduling, and decision-making. Furthermore, by integrating AI, efficiency can be enhanced in areas such as energy consumption analysis and optimization, production scheduling, and flexible manufacturing.

MES typically encompasses all aspects of factory operations, including personnel, machinery, materials, methods, and environment, and is closely tied to industry know-how and business processes. For example, only with MES can energy consumption per unit and output per worker be effectively quantified.

Broadly speaking, Advanced Planning and Scheduling (APS) is a component of Manufacturing Execution Systems (MES), playing the role of optimizing production scheduling and execution. Production scheduling itself is an optimization problem in operations research, which, when combined with multi-constraint conditions, seeks the optimal production schedule; artificial intelligence can enhance efficiency in this process. For example, the extraction cycle of an oil field lasts 8–10 years, and determining the optimal output is inherently a multi-stage optimization process. Furthermore, advanced scheduling algorithms can grant production greater flexibility, potentially increasing production efficiency by several folds in certain sectors.

4.2 Precision and Flexibility: From Process Optimization to Holistic Intelligent FOS (Factory Operating System), Envisioning the Factory of the Future

At the current stage, most intelligent solutions have not yet achieved full-plant, enterprise-wide coverage; they are largely limited to point-specific or linear technologies. However, in terms of direction and pathway, some large enterprises and entrepreneurs are attempting to extend their capability boundaries, evolving from single-process applications to end-to-end process integration. Imagine an industrial operational environment where physical-world information undergoes global semantic parsing, enabling efficient interaction between machines, as well as between humans and machines. Meanwhile, an intelligent operating system handles extensive control, scheduling, and decision-making tasks, including guiding human workers or digital employees through AR and computer vision technologies, enabling flexible scheduling for warehousing and logistics, executing decision-based scheduling via new business software systems, and capturing user intent for 3D reconstruction and simulation. Furthermore, such control, scheduling, and decision-making capabilities ensure optimal practices. This will undoubtedly propel industrial enterprises into a new era of enhanced efficiency.

The above analysis focuses on the level of factory operations. If we elevate the perspective to view the factory as an enterprise and a profit-generating entity, it is necessary to comprehensively consider R&D, production, supply, and sales in conjunction with the upstream and downstream value chains.

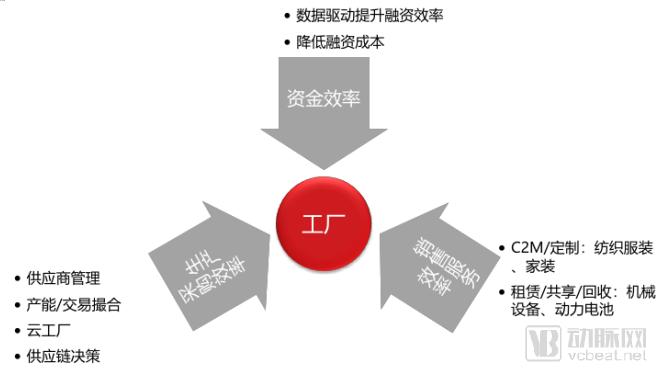

Figure 8: Opportunities for Efficiency Transformation Beyond Factory Operations

5.1 Factory-Centric, Enterprise-Led: Technology-Enabled Efficiency Gains Across the Upstream and Downstream Value Chain

Industrial intelligence not only involves a globally semantic-aware intelligent operating system within factories, but also offers substantial room for efficiency gains across upstream and downstream collaboration, as well as in production, capital management, and sales services.

At the production and procurement level, by connecting equipment and data, empowering through IoT, and integrating online and offline operations, cloud factories can enhance supply chain efficiency, achieving qualitative breakthroughs in output, pricing, and input.

Leveraging various optimization algorithms, industrial enterprises have opportunities to reduce costs and improve efficiency in procurement, inventory, logistics, and other areas. As early as the beginning of this century, HP Inc. applied inventory optimization and mathematical programming models to restructure its supply chain model, saving $130 million over two years.

Leveraging data from the industry chain to develop more precise risk models can also help enterprises improve capital efficiency.

In terms of sales and service, Haier and Kute Smart are typical representatives of the C2M model. Through reverse customization, Haier has achieved zero inventory for certain products, generating substantial financial gains. This outcome is also a testament to the effectiveness of industrial software, data accumulation, and intelligent technologies.

Overall, data algorithms and intelligent software and hardware can serve as configurators to facilitate capacity matching, supply-demand alignment, capital matching, and empowered supply chain collaboration.

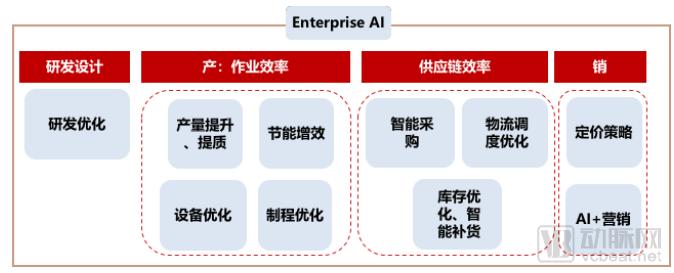

5.2 Connecting R&D, Production, Supply, and Sales: Enterprise-Level Process Reengineering and Business Value Reshaping

From the perspective of manufacturing enterprises, the closed loop of value is realized through R&D, production, supply, and sales. The logic of entrepreneurship or investment can also follow the logic of a company’s own value realization to explore new opportunities. In the past, some lean consulting firms played a role in local or global optimization. In the AI era, empowered by technology, new opportunities may emerge from the perspective of corporate value realization, including investments in new departments, new forms of supply chain organization, or even new product categories (companies).

Figure 9 Enterprise-Grade AI: Connecting R&D, Production, Supply, and Sales

Beyond the frameworks of operational efficiency, commercial efficiency, and the asset-to-process-to-FOS model, let us discuss another overarching theme: data. Past investments in the industrial sector have focused primarily on product equipment, automated products, and solutions, with an overall emphasis on hardware. Broadly speaking, these investments aimed to replace human limbs and manual labor.

What AI can do is certainly not limited to the execution of actions. At the level of data-driven decision-making, AI can empower certain internal departments of industrial enterprises or replace some large professional service firms, helping them make better operational and business decisions.

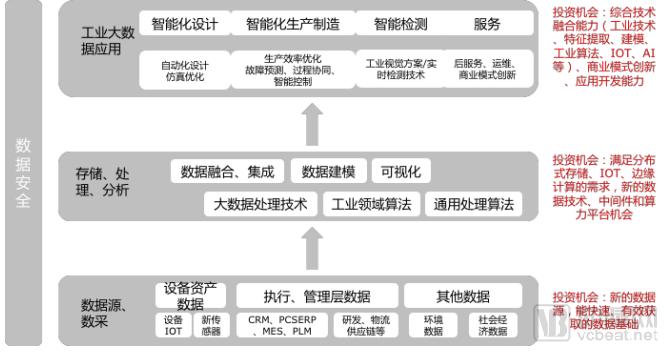

From the perspective of the data industry chain, we have divided it into three levels for analysis:

Figure 10 Investment Opportunities in the Industrial Data Industry Chain

From the perspective of the Internet of Things (IoT), addressing heterogeneous devices with coexisting multi-protocol standards and determining how to connect them, aggregate and fuse their data, and enable edge or cloud computing is a fundamental challenge. At the level of data sources and acquisition, we are also focusing on new data dimensions and novel sensing and acquisition methods, such as leading-edge, next-generation sensors. BV has systematically invested in multiple domestic and international frontier sensor companies in this field. Additionally, software products that can rapidly help enterprises achieve Industry 3.0 capabilities are critical; if an enterprise cannot quantify key metrics such as energy consumption, costs, or labor hours, it cannot effectively engage in advanced data-driven decision-making.

From the perspectives of storage, processing, and analysis, we focus on emerging data technologies, middleware, and computational power requirements; data fusion and integration are also universal needs for intelligence. Meanwhile, the insufficient accumulation of experience and knowledge in industrial mechanisms, industrial processes, and modeling methodologies has become a bottleneck at the algorithmic level in the industrial sector.

At the application layer, data empowers humans to make holistic decisions across the entire lifecycle of supply chain, design, manufacturing, inspection, and after-sales service. This has given rise to a variety of technical solutions and business models. The aforementioned operational efficiency and commercial efficiency demonstrate that data’s capability boundaries are sufficient to drive significant performance improvements and transformation in industry.

Enterprises across different industries and regions in China are at varying stages of development: some are still at Industry 2.0 and need to make up for foundational gaps, others are at Industry 3.0 awaiting widespread adoption, and a few are at Industry 4.0 requiring demonstration projects. This diversity in development stages, coupled with differentiated transformation needs and fragmented market orders, has created the most complex market for intelligent industrial transformation in China.

In the process of investment incubation and deep industry integration, we have also observed numerous challenges facing technological innovators, such as data integrity issues, inability to close the loop on solutions, unattractive business models, lack of high-quality environmental data and simulation environments, narrow operational boundaries, as well as many other difficulties and problems traditionally faced by large B-end enterprises. The future is undoubtedly promising, yet the path forward is undeniably tortuous.

BV’s strategy is to align with the major trends of efficiency transformation across industries, positioning itself as a solutions provider or operational company leveraging cutting-edge technologies. Meanwhile, it facilitates industrial upgrading and transformation in China and globally by integrating research resources from its Intelligent Industry Lab and academic research institutions, and by connecting technological solutions.

About the Author:

Fang Xin, Vice President of Investment at Baidu Ventures (BV), has long focused on AI industry solutions, intelligent enterprise services, industrial intelligence, and data intelligence. He is committed to helping industry players, academic researchers, entrepreneurs, and technology owners develop and refine innovative solutions for industry intelligence. In the field of industrial intelligence, he has led or participated in investment projects including Xuanyu Technology, Huidian Yunlian, Paifang Technology, Airidi, Changyang Technology, Shujian Technology, and Yunding Technology.