After the Disappearance of a Million Pharma Reps, Drugmakers Surge into Digital Transformation

Pharmaceutical representatives have been having a tough time lately.

Data circulating online suggests that nearly 1 million of the 3.5 million pharmaceutical sales representatives have left the industry. While this figure may be somewhat exaggerated, the successive implementation of the “Two-Invoice System” and “Volume-Based Procurement,” along with hospitals’ self-initiated soft policies, has indeed had a significant impact on pharmaceutical sales representatives of all types.

“Since 2019, we have not received any support for sales expenses. When we discuss these drugs, we refer to ‘maintaining sales’ rather than ‘sales growth,’” a pharmaceutical sales representative for a distributor of drugs included in the “4+7” volume-based procurement list, who requested anonymity, told VCBeat. His 20 years of experience as a medical representative did not equip him with sufficient strategies to cope with this series of policy changes.

Biologics sales representatives are also preparing for a rainy day. A Johnson & Johnson pharmaceutical representative stated, “Although the policies have not directly impacted us, management is still actively exploring new management and sales approaches. In this broader trend, no one can be certain about what changes lie ahead.”

The Challenges Facing Pharmaceutical Companies Are Breeding New Market Demands. Recently, VCBeat (WeChat ID: vcbeat) has observed numerous new initiatives by pharmaceutical companies, as they seek to achieve digital transformation in pharmaceutical sales through project collaborations or service purchases with third-party platforms.

The companies selected by pharmaceutical firms include those with physician communities, such as DXY, Xingshulin, Mixi Technology, and Yixuejie; software service providers with clear objectives focused on internal management solutions for pharmaceutical companies, such as Ruansu Technology and Yunshi Software; as well as artificial intelligence and informatics companies that are increasingly entering this space through partnerships. The landscape of digital transformation in the pharmaceutical industry has never been more vibrant.

Therefore, we conducted separate interviews with multiple pharmaceutical executives, solution providers, and medical representatives to seek answers to the following three questions:

Why Do Pharmaceutical Companies Need to Transform?

How Should Pharmaceutical Companies Choose Digital Products?

In the Digital Wave, Who Is Assisting Pharmaceutical Companies in Their Digital Transformation?

“Overall, China is at the forefront of global digitalization; in terms of service scale, degree of innovation, complexity, and effectiveness, other countries can hardly compare,” said a digital service provider. By contrast, the pace of digitalization in pharmaceutical sales has been somewhat lagging, which is not unrelated to the tangled web of vested interests across various pharmaceutical sales channels.

From an external perspective, under the immense pressure of medical insurance, policy has become the primary driver promoting reform in pharmaceutical companies. After the implementation of the “Two-Invoice System,” pharmaceutical companies could still inflate invoices, agency firms could absorb individuals as employees, or costs could be shifted to consumers to safeguard the interests of doctors and medical representatives. However, volume-based procurement represents a disruptive, dimension-reducing strike; in the sales market for drugs involved, there is no longer any room for medical representatives to survive.

In this scenario, pharmaceutical companies with strong R&D capabilities see opportunities; they are channeling more capital into research and development and consistency evaluations to enhance the prospects of their later-to-market drugs in government procurement tenders. Meanwhile, some pharmaceutical firms lacking in-house R&D capabilities can only adopt a short-term survival strategy under the prevailing policy landscape, biding their time for a market recovery.

However, regardless of the category of enterprise or whether they won bids in the “4+7” volume-based procurement program, pharmaceutical companies have seen their expected profits significantly downgraded. Winning bidders such as Huahai Pharmaceutical and Salubris saw their stock prices cumulatively drop by more than 10% within a week.

Furthermore, large-scale pharmaceutical companies will place increasing emphasis on compliance. The joint audit campaign launched in June by the Ministry of Finance and the National Healthcare Security Administration will serve as a reckoning for the chaotic practices prevalent in pharmaceutical sales. Tu Honggang, founder of Yiku Software, stated, “In the aftermath of this storm, certain behaviors that cross high-voltage red lines will escalate to issues critical to corporate survival.” Liu Xiao, COO of Shanggong Yixin, joked half-seriously, “Sales representatives may now only be able to treat clients to boxed lunches during breaks at academic conferences.”

Turning to internal factors, pharmaceutical sales management has long been characterized by its extensive, rather than intensive, approach. Medical representatives from different pharmaceutical companies track physicians across varying departments, with differing frequencies of engagement and required cycle times ranging from two weeks to two months. Consequently, KPI assessments for sales personnel in most pharmaceutical companies are predominantly results-oriented.

Nowadays, as pharmaceutical distribution models are gradually simplified, the performance assessment of medical representatives has become relatively straightforward. However, under cost pressures, pharmaceutical companies also need more refined management approaches to oversee their sales personnel.

In the past, pharmaceutical sales representatives were selective in their physician outreach, relying on subjective judgment to identify and target physician resources. Most focused their attention on physicians with whom they had established relationships and found easy to communicate with, while devoting insufficient effort to engaging with unfamiliar physicians. This approach made it difficult for pharmaceutical sales representatives to achieve comprehensive and objective coverage of the physician population.

Under the promotion of the tiered diagnosis and treatment policy, pharmaceutical representatives also need to step out of the first-tier cities where they have long been based and expand their business into more grassroots medical institutions, a shift that requires resources provided by third-party agencies.

Finally, the advancement of internet healthcare and the heightened emphasis placed by physicians and patients on follow-up processes have reshaped pharmaceutical distribution channels. In addition to promotion through traditional academic conferences, many pharmaceutical companies and e-pharmacy platforms are collaborating with health IT firms to integrate drug sales into follow-up care and mobile consultation channels.

In summary, the causes can be attributed to the following five points:

1. Policies such as the "Two-Invoice System" and volume-based procurement have led to a decline in pharmaceutical prices and reduced revenues for pharmaceutical companies, necessitating compensation for these losses through alternative channels;

2. Increasingly stringent compliance requirements have transformed pharmaceutical marketing models, necessitating new technologies and management approaches to meet physicians’ needs;

3. The previously extensive management model in pharmaceutical sales offers significant room for optimization; through refined management, pharmaceutical companies can enhance efficiency;

4. The traditional pharmaceutical sales model has blind spots; pharmaceutical companies require technological support to cover these gaps and precisely reach every physician.

5. Changes in the behavior of hospitals and physicians have made traditional channels increasingly difficult to navigate; the conversion rate of promotional activities such as academic promotion needs improvement, requiring pharmaceutical companies to secure new sales channels through internet hospitals, patient follow-ups, and other avenues.

In response to the aforementioned factors, some pharmaceutical companies either issue prescriptions independently or seek solutions from third-party enterprises. The primary objectives of these initiatives include reducing sales costs, expanding sales channels, establishing more effective KPI systems, enhancing the transparency of sales personnel’s activities, achieving broader physician coverage, and improving regulatory compliance.

So, how do pharmaceutical companies actually operate in practice?

“Undoubtedly, Pfizer is the best among all pharmaceutical companies in terms of digitalization,” remarked an executive at a major pharmaceutical company. As the world’s largest pharmaceutical company, Pfizer has not only been ahead of the curve in awareness but has also made remarkable investments in its digital sales transformation.

In the healthcare sector, data has always been the most critical asset. For a long period, pharmaceutical companies kept data firmly in-house, developing their own management systems and organizing various conferences independently. However, after 2018, many enterprises had a change of perspective, questioning why they should build their own platforms from scratch instead of leveraging existing ones through partnerships.

Mo Kewang told VCBeat, “With the advent of cloud computing, you will find that companies such as Tencent, Alibaba, and JD.com have all begun to build platforms for healthcare and wellness, promoting the concept of sharing. Many pharmaceutical companies have started to realize that it is sufficient for them to join these platforms, rather than operating independently.”

Large-scale, cross-sector collaborations have thus been launched. “Many pharmaceutical companies are widely publicizing their strategic partnerships. What’s the logic behind this? They are staking out their territory,” said Wang Nan. “Internet companies hold vast amounts of patient data, with these potential patients firmly in their hands.”

Therefore, pharmaceutical companies no longer view digital marketing as a “one-size-fits-all” promotional approach. Instead, they leverage physician profiling for precise targeting and actively seek feedback. In the past, information dissemination was largely one-way, making it difficult for pharmaceutical companies to assess campaign effectiveness, let alone obtain feedback. This has become a key factor driving pharmaceutical companies’ adoption of digital platforms.

Who can provide such services? AI companies represent one viable direction. Mr. Wang illustrated this model using diabetes as an example: pharmaceutical companies may partner with AI firms to secure large-scale diabetes projects. The AI companies, adopting a platform-based approach, would execute these projects and deliver services to patients through methods such as cloud-based imaging. This process facilitates the establishment of patient communities, which are precisely what pharmaceutical companies seek.

Of course, not every pharmaceutical company has opted for this open model; some possess the capability and resources to build their own vertical ecosystems, with Fosun Pharma being one such example.

Chen Tao, Director of System Applications at Fosun Pharma, stated: “Fosun’s digital marketing initiative began in 2016, with the direct establishment of a subsidiary that year.”

The company primarily encompasses two projects: one internal and one external. The internal project, named the “AI Marketing Middle Platform,” aims to transform Fosun’s entire marketing system into a modular middle-platform architecture. Within this framework, the “Smart Marketing Platform” module integrates with Fosun’s internal GIM system, enabling sales personnel to conduct all sales promotion and management activities, as well as handle expense reimbursement processes, on this platform.

Externally, the project is branded as the “New Retail” platform, featuring an F2B2C model. Chen Tao told VCBeat, “We have signed contracts with more than 3,000 retail pharmacies. The primary objective is to help them channel electronic prescriptions from hospitals to these pharmacies, enabling patients to pick up their medications directly at these locations. The platform supports various online payment methods, provided that hospitals can issue electronic prescriptions.”

“The primary function of digital marketing is customer acquisition, namely attracting new customers. For instance, if we aim to onboard professional physicians, we set a KPI for the sales team requiring a specific number of new physician sign-ups per month, thereby incentivizing sales efforts and aligning with the company’s goal of acquiring new customers. At this stage, performance assessment has not yet been linked to sales compensation. This is due to two main reasons: first, there may be no substantial growth in the short term; second, it is difficult to establish and verify a direct causal relationship between new customer acquisition and digital initiatives. Overall, we are still in an exploratory phase.”

It is difficult to determine which of the two models is superior, but there is no doubt that some companies are playing a significant role in this transformation.

The pharmaceutical digitalization support companies discussed in this article mainly fall into two categories: the first provides digital sales management solutions for pharmaceutical companies; the second seeks new sales channels and develops new customers for pharmaceutical sales. During its investigation, VCBeat found that, apart from industry leaders such as Veeva, most companies assisting pharmaceutical firms with digital transformation are not specialized in this field. Many have entered the sector from other industries, leveraging their existing resources to develop new products, with each company offering distinct strengths. After screening hundreds of enterprises, VCBeat selected several mature and representative companies for in-depth interviews, aiming to uncover the hidden value within this sector.

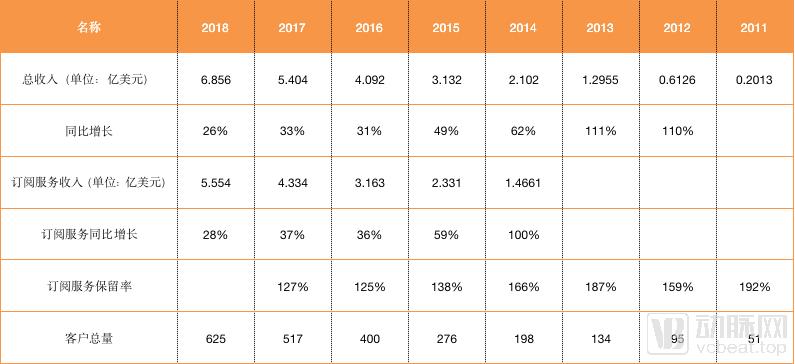

Veeva is a veritable leader in the field of digital healthcare management. Its core business involves providing sales force management solutions for pharmaceutical companies and user-friendly commercial software for medical representatives. Since its founding in the United States in 2007, Veeva’s client base has come to include nearly all of the top 20 pharmaceutical companies worldwide. It took the company only eight years to grow its annual revenue from $20 million to $700 million.

Breaking out in the life sciences vertical is no easy feat. A decade after its founding, Veeva’s market capitalization has surpassed $10 billion. Its success stems from its keen insight into the structural changes within pharmaceutical companies; over these ten years, its platform has played a significant role in the transformations of major pharma giants such as Pfizer and GSK.

Veeva provides a comprehensive suite of solutions for the pharmaceutical industry, covering everything from research and development to sales. Veeva’s first product was designed for medical sales representatives, and its business truly took off after the launch of the iPad in 2010. This CRM system, compatible with iOS, was successfully adopted by U.S. pharmaceutical sales representatives who widely used iPads in their work. By 2018, this CRM software had captured an 80% market share.

Without a viable competitor in clinical data management, Veeva Vault is poised to become the Microsoft Office of the life sciences and pharmaceutical industry. As more users adopt clinical management informatics solutions, the product’s value to customers continues to grow.

Currently, Veeva serves more than 600 clients, including leading global pharmaceutical companies and emerging biopharmaceutical firms such as AstraZeneca, Pfizer, Merck, Novartis, Eli Lilly, and Amgen. Veeva’s financial reports from 2016 to 2018 indicate that its revenue sources are highly diversified, with no single customer accounting for more than 10% of sales, demonstrating Veeva’s strong risk resilience.

As the sales of innovative drugs increasingly shift to academic exchange conferences, a group of healthcare companies long entrenched in the internet sector have begun to collaborate with pharmaceutical firms. The most significant commonality among these enterprises is their well-established physician communities, through which pharmaceutical companies can more easily identify their “target audiences.” While BATJ (Baidu, Alibaba, Tencent, and JD.com) also play important roles in this landscape, this article focuses exclusively on startup companies as case studies.

1. DXY

Founded in 2000, DXY is China’s largest connector in the healthcare sector and a leading provider of professional digital services. Through its platform for sharing authoritative professional content, extensive and comprehensive data assets, and standardized, high-quality medical services, DXY connects hospitals, physicians, researchers, patients, biopharmaceutical companies, and insurers. It serves tens of millions of general users and boasts 5.5 million professional users, including 2 million physicians.

In collaborations with pharmaceutical companies, Zhang Wei, Vice President of DXY, stated: “Purely product-driven marketing models are prone to homogenization; upgrading product marketing into a comprehensive service system for both doctors and patients will create greater differentiation.”

Taking the “Youxing” diabetes chronic disease management service collaboration among Yilai, DXY, and Tencent as an example, all patients meeting specific criteria can receive high-value comprehensive patient care services free of charge. This helps patients better treat and manage their conditions, thereby achieving compliant, multi-party win-win outcomes. This is also one of the key cooperation models within DXY’s integrated physician-patient service system offered to pharmaceutical companies.

This case also illustrates that while DXY’s core focus was previously on physician education, it is now maximizing the value of its high-quality physician resources in doctor-patient services.

Furthermore, DXY’s advantages also lie in its infrastructure system and organizational capabilities, which determine the value that the platform can deliver to enterprises, physicians, and patients.

2. Mixi Tech

The platform developed by Mixi Technology primarily serves academic promotion and does not involve sales channels. “We are fostering the healthy development of this sector, rather than helping to sell drugs,” summarized Gao Wei, a partner at Mixi Technology.

In the realm of digital pharmaceutical marketing, Mixi Technology offers four major categories of services. First, precision education and academic conference services. Second, services for the transformation and upgrading of medical representatives, acting as “agents” for physicians to help them increase their income in a compliant manner. Third, compliance services for sales activities; given that many pharmaceutical companies have non-compliant cash flow practices, Mixi provides online solutions to ensure these expenses are reasonable and regulatory-compliant. Fourth, market management services, enabling the migration of offline processes between “manufacturers and distributors” to online platforms.

“The correlation of interests between online academic activities and pharmaceutical sales is too strong,” said Gao Wei. “As a third-party platform, we do not wish to be heavily entangled with such interests. Mixi generates revenue through services: doctor interactions on our platform lead to home visits by physicians and chronic disease management for patients, thereby encouraging patients to purchase service packages. These packages allow patients to access physician services within a specified period. Physicians benefit from this arrangement, and we also earn service fees.”

Recently, a large number of health IT and AI companies have received overtures from pharmaceutical firms both in China and abroad. These companies specialize in various niche sectors within healthcare. Their competitive advantage lies in leveraging big data to create detailed profiles of patients and physicians, or in establishing highly focused platforms that facilitate promotional activities for pharmaceutical companies.

1. Cloud Power Software

Yunshi Software is a SaaS platform company in China with first-class artificial intelligence technology,

In the digitalization of pharmaceutical distribution and sales, Yunshi Software provides pharmaceutical enterprises with a comprehensive solution. The entire system encompasses key functionalities such as master data management, product flow tracking, order management, organizational architecture, performance metrics, CRM, remote detailing, meeting management, incentive compensation, and BI reporting.

Hu Junping, President of Yunshi Software, categorizes the value of informatization in pharmaceutical distribution and sales into two levels: “The first level is information transparency, enabling data to assist management in decision-making rather than relying solely on business experience. Currently, all data are recorded by the system and available for analysis.”

“The second, more critical level is that Yunshi Software can help enterprises implement specific processes in sales management. All management philosophies require a vehicle for realization. If such a vehicle is software, it will enable sales personnel to develop habits or adopt standardized business practices through its use, thereby assisting the enterprise in establishing a tangible sales philosophy.”

Today, Cloud Software is not only focused on providing solutions for pharmaceutical companies, because the wave of digitalization is reshaping not only the management of pharmaceutical companies and the circulation of drugs. In drug discovery and clinical trial management, Cloud Software is also making strategic moves.

2. Huimei Yijian

Among the myriad of AI and health IT enterprises, Huimei Medical Group—a joint venture between Mayo Clinic and Hillhouse Capital—stands out with a distinctive character. Its Sino-American DNA enables Huimei to discern even the most subtle shifts within the healthcare sector.

After recognizing the opportunities in the digital transformation of pharmaceutical companies, Huimei Medical Group established Huimei Yijian. This subsidiary primarily leverages professional medical knowledge systems and technical methods to provide pharmaceutical companies with big data management platforms, offer technological and data support for academic interactions between pharmaceutical companies and physicians, and deliver consulting services for interactions among pharmaceutical companies, physicians, and patients.

Like Huimei Technology, Huimei Yijian also empowers clients with technology, enhancing efficiency by digitally transforming traditional business and management models.

From the perspective of marketing development trends in any enterprise, marketing must inevitably be built upon a precise understanding of customers. For instance, when we make purchases on e-commerce platforms, these sites collect data to create accurate user profiles—determining whether we are new mothers or middle-aged women—and subsequently recommend products tailored to our needs.

Huimei Yijian’s Data Management Platform (DMP) is built on this concept. It aggregates various physician-patient data, including user (physician) behavioral information and digital interaction data between pharmaceutical companies and physicians. By leveraging data science to construct user profiles, the platform guides pharmaceutical sales representatives in conducting academic promotion of medications, thereby enabling digital marketing and enhancing both marketing efficiency and effectiveness.

What Information Does the DMP Platform Collect from Physicians? Non-private data, such as physicians’ online lightweight consultation records, patient dialogues, published papers, participation in clinical trials and medical conferences, as well as their interests in medical devices and pharmaceuticals and preferred brands, are deconstructed into various tags using natural language processing techniques. Meanwhile, by implementing tracking mechanisms with diverse technical methods on professional medical websites, pharmaceutical company websites, and even offline communication channels between pharmaceutical companies and physicians, it is possible to collect data on users’ areas of interest and trending topics.

Meanwhile, Huimei Yijian places significant emphasis on patient education. The Mayo Clinic knowledge system encompasses numerous standard clinical practice guidelines in the medical field, presented in an illustrated format that is highly suitable for pharmaceutical companies to use in educating both physicians and patients. By localizing Mayo Clinic’s guidelines and patient education materials, Huimei Yijian can provide pharmaceutical companies with educational support for primary care physicians, as well as content support for patient education initiatives within patient services and chronic disease management programs.

3. SG Medical Information

What sets Shanggong Yixin apart from other companies is that it is, first and foremost, an artificial intelligence firm specializing in the management of ocular diseases and diabetic complications. So how did such a company become a partner for pharmaceutical enterprises? Liu Xiao, Deputy COO of Shanggong Yixin, provided a detailed explanation to VCBeat.

Diabetes is a typical chronic disease, and its treatment is not a single point in time but rather a prolonged continuum. Among all diabetic complications, ocular complications are the most challenging to manage. ShangGong YiXin leverages AI-based screening for diabetic retinopathy to help patients effectively manage these ocular complications, thereby establishing an intelligent management platform for diabetes and its associated complications.

Currently, ShangGong YiXin has established a medical service platform that integrates scientific research, demonstration projects, departmental exchanges, and patient education. While providing patients with AI-based diabetic retinopathy screening services, the platform automatically updates patient information. Healthcare professionals leverage this platform to deliver free clinics, preventive education, and community-based diabetes management services.

Liu Xiao stated, “Patients on the Shangong Yixin platform tend to exhibit strong stickiness. As diabetes is a lifelong condition, patients undergo at least one examination annually, which means they will remain active on the platform over the long term, and we have an obligation to proactively remind them to get checked.” This demonstrates that the platform is highly attractive to pharmaceutical companies.

In specific collaborations with large pharmaceutical companies, Liu Xiao categorized them into two models: first, collaborating with the medical affairs department to conduct real-world data studies, assisting in the validation of drug therapeutic efficacy and standardized diagnosis and treatment protocols; second, partnering with the marketing and sales departments to build academic platforms and diversify forms of multi-party collaboration.

Overall, the key to Shangong Yixin’s collaboration with pharmaceutical companies lies in its extensive hospital-patient network. This model is well-suited for establishing a patient-centric collaborative platform for pharmaceutical companies and physicians through innovative partnership arrangements.

In addition to the aforementioned enterprises, advertising agencies and pure-play service providers have also joined the effort to facilitate digital transformation. Companies such as WPP and Yiduo, which do not possess direct physician-patient resources, provide tailored support based on pharmaceutical companies’ specific needs. Other key players include live-streaming technology firms, medical writing and service agencies, visual content creators (producing posters, comics, animations, videos, etc.), and media placement partners. All of these entities constitute important components of the digital marketing industry chain.

If we focus on the present moment, it becomes evident that digital pharmaceutical sales in China are still in their infancy. Among the five medical representatives interviewed by VCBeat, four had only heard of physician profiling technology and CRI systems, while only one had actually used these systems, noting that they have not yet become a necessity.

What Is Hindering the Development of Digital Marketing in the Pharmaceutical Industry? VCBeat believes that the factors currently limiting the digital development of the pharmaceutical industry mainly include the following:

1. Volume-based procurement remains in the pilot phase, and off-invoice sales practices persist in cities not designated by the policy. Before the policy is extended to these cities, many enterprises will not alter their existing sales models.

2. The consignment sales model is deeply entrenched; even in major cities, bribery during the sales process cannot be eradicated at this stage. More stringent punitive measures are the solution to this problem.

3. Erosion of Trust: Physicians are reluctant to place sufficient trust in pharmaceutical companies’ products and digital models, which will reduce conversion rates.

4. Talent Shortage: There is a severe scarcity of professionals who possess expertise in pharmaceuticals, platform operations, and digitalization; this industry requires greater inflow of cross-border talent.

Fortunately, with policy guidance, these issues can be resolved over time. What warrants attention is the trajectory of companies specializing in artificial intelligence (AI) in healthcare. After years of accumulation, these AI enterprises may leverage their amassed resources of physicians and community networks to discover new profit models. Can the hundreds of related companies assisting pharmaceutical firms roll out new business models in the second half of 2019? Undercurrents are stirring.