How the World's Top 52 Healthcare-Related Fortune 500 Companies Are Transforming the Medical Industry

On July 22, Fortune magazine released the 2019 Global 500 list. The ranking featured many encouraging figures: for the first time, China surpassed the United States with 129 companies on the list; Xiaomi made its debut as the youngest company ever to enter the Global 500; Walmart retained the top spot for the sixth consecutive year, while Sinopec Group secured second place, achieving the highest ranking among Chinese enterprises.

Based on this list, VCBeat (WeChat ID: vcbeat) has compiled a roster of 52 Fortune 500 companies with healthcare-related operations, reviewed their profiles, and further analyzed the current status of their healthcare businesses as well as key developments in the medical sector.

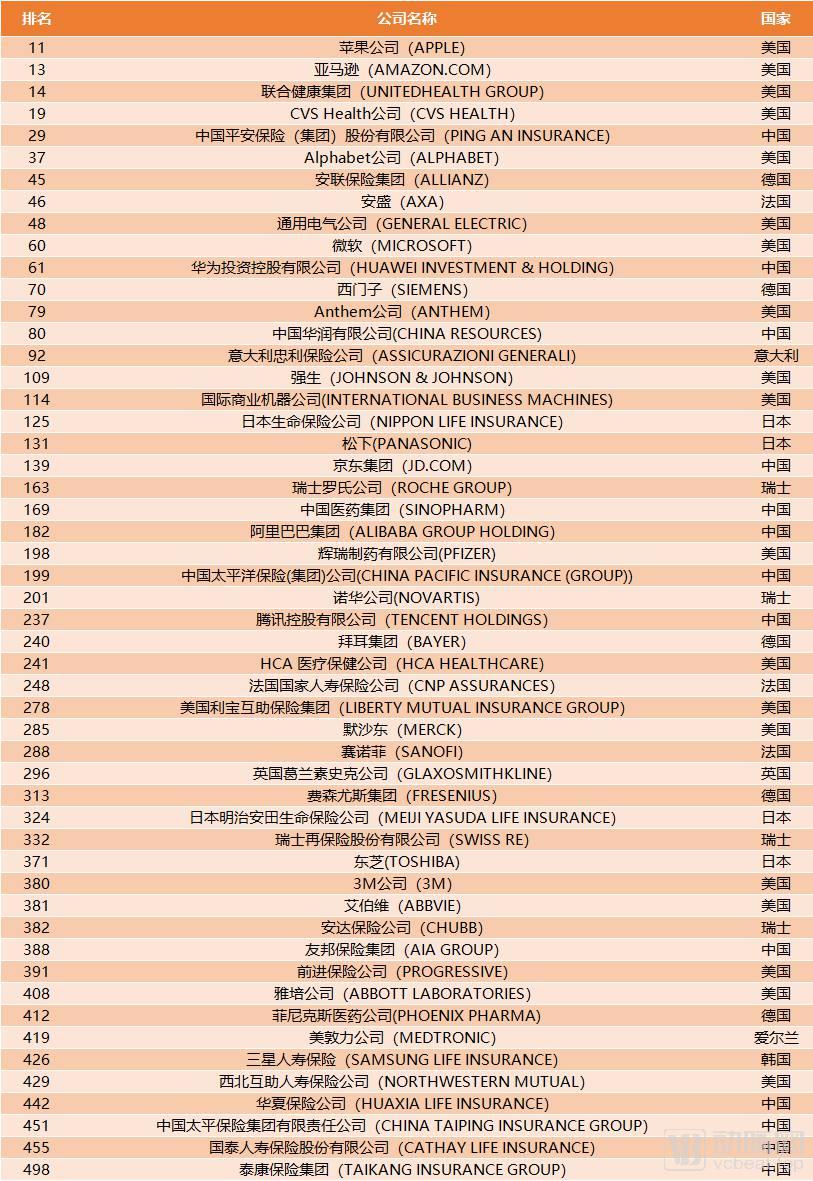

List of 52 Healthcare-Related Fortune 500 Companies

Among the Fortune 500 companies, a total of 52 are involved in the healthcare industry, including medical enterprises, health-related insurance companies, and technology firms engaged in the healthcare sector.

Below are the ranking data for Chinese companies:

Four technology companies made the list: Huawei (61st), JD.com (139th), Alibaba (182nd), and Tencent (237th);

In the pharmaceutical sector, China Resources Group (ranked 80th) and Sinopharm (ranked 169th) made the list;

In the health insurance sector, seven Chinese insurers made the list: Ping An Insurance (29th), China Pacific Insurance (199th), AIA Group (388th), Huaxia Life Insurance (442nd), China Taiping Insurance (451st), Cathay Life Insurance (455th), and Taikang Insurance Group (498th).

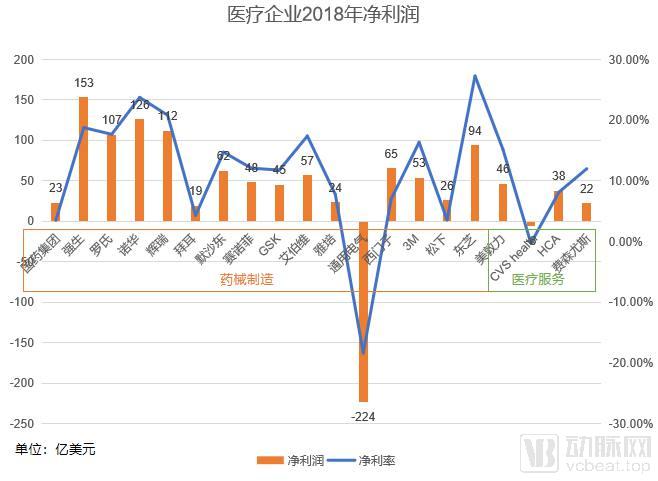

Among Fortune 500 healthcare companies, the most profitable was Johnson & Johnson, which reported a net profit of $15.3 billion in 2018. In addition to Johnson & Johnson, three other pharmaceutical companies achieved net profits exceeding $10 billion: Novartis ($12.6 billion), Pfizer ($11.2 billion), and Roche ($10.7 billion).

Well-operated enterprises in the healthcare sector typically report net profit margins of 15%–20% of their operating revenue. Sinopharm Group has long maintained a profile characterized by high revenue, high costs, and low net profits, while remaining profitable, thereby distinguishing its revenue performance from that of other companies. Toshiba’s fiscal year 2018 net income of ¥94 billion was primarily attributable to the ¥966 billion (approximately $8.93 billion) gain from the sale of its NAND flash memory business to Bain Capital in the second quarter; in reality, Toshiba’s underlying performance in fiscal year 2018 was lackluster.

Among the 16 healthcare companies, U.S. pharmacy retail giant CVS Health and General Electric (GE) reported losses. The former incurred a loss of $594 million in 2018, while the latter posted a staggering loss of $22.4 billion in 2018, marking the largest deficit among Fortune 500 companies.

Amid years of underperformance, GE has been attempting to address its debt issues through downsizing. In June 2018, GE announced the spin-off of its healthcare business, establishing GE HealthCare as an independent medical company. In November 2018, GE sold its medical equipment financing assets for $1.5 billion; in February 2019, it sold its biopharmaceutical business to Danaher for $21.4 billion. Following this series of streamlining measures, this year may well be the last in which we classify GE as a healthcare enterprise.

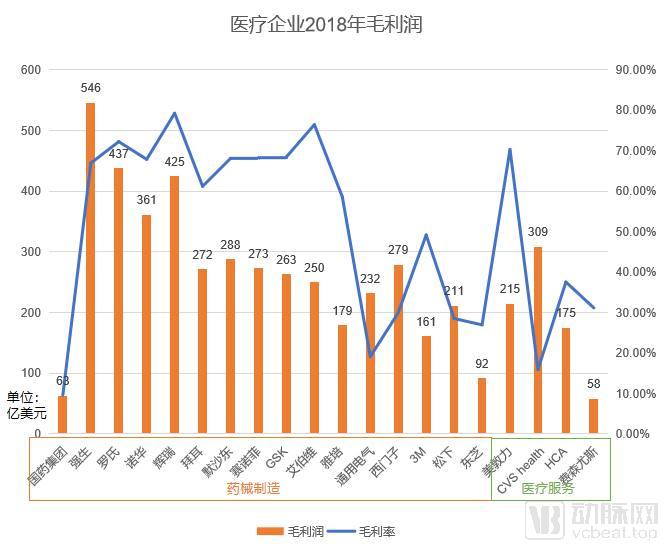

In the healthcare sector, companies in the pharmaceutical and medical device manufacturing industry generally have higher gross profit margins than those in the healthcare services industry. Among them, pharmaceutical and medical device manufacturers whose primary business operations are within the healthcare field include Johnson & Johnson, Roche, Novartis, Pfizer, Bayer, Merck & Co., Sanofi, GSK, AbbVie, Abbott, andMedtronic, the gross profit margins of these 11 companies are almost all above 60%, with Abbott, the lowest, at 58.6%.

Industrial companies with only a portion of their business within the medical sector, such as General Electric, Siemens, 3M, Panasonic, and Toshiba, have lower gross profit margins, all below 50%. The gross profit margin for healthcare service companies is only around 30%.

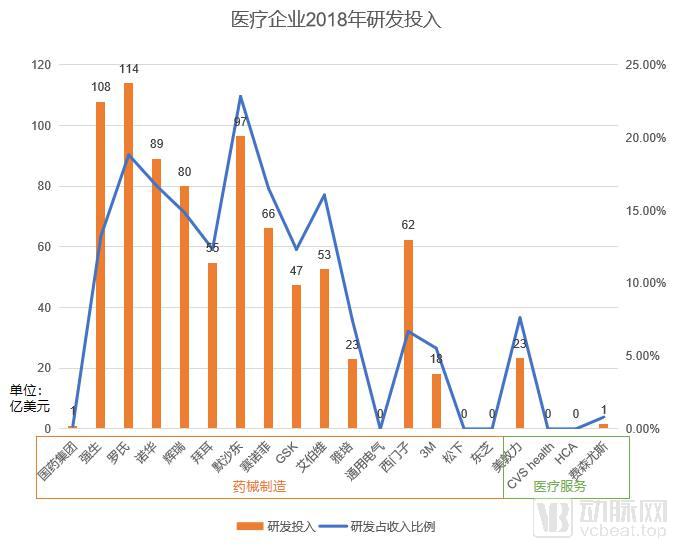

High gross margins are accompanied by high R&D investment. Among the 11 companies primarily engaged in healthcare mentioned above, nine have maintained consistently high levels of R&D spending, with Merck & Co.’s R&D intensity reaching as high as 22.8%. In contrast, healthcare service providers incur virtually no R&D expenses.

Insurance companies sitting on substantial capital are poised to make their move. While most are entering the healthcare sector through investments, some enterprises are exploring alternative strategies by building their own healthcare facilities or forming partnerships to establish a presence in the industry.

Insurance companies themselves have weak technological foundations, so they are better suited to pursue channel-driven development paths such as internet healthcare when entering the medical sector. Among Fortune 500 insurers, the most representative example is Ping An Good Doctor, under China Ping An.

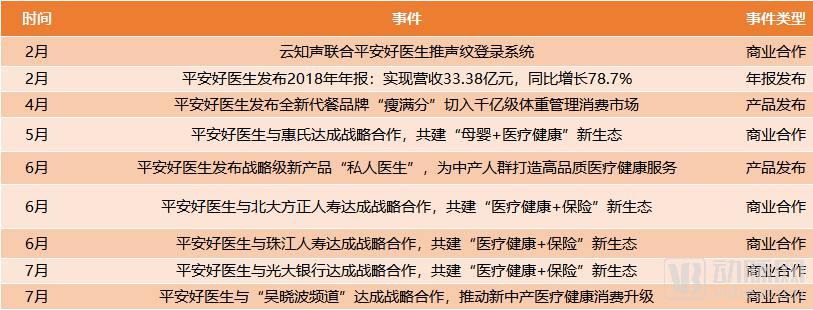

2019 Ping An Good Doctor Medical Milestones

Data Source: VCBeat Dongguan

Ping An Good Doctor is a key member of Ping An Group’s internet business segment and was listed on the Hong Kong Stock Exchange in May 2018. Adopting a dual strategy of health management and mobile healthcare, Ping An Good Doctor is deeply committed to technological innovation, striving to build a one-stop, end-to-end medical and health ecosystem. With online healthcare at its core, it provides standardized pan-medical products and comprehensive health management services.

Rather than serving as a traffic gateway, Ping An Good Doctor has primarily enhanced user stickiness for Ping An Insurance. According to the annual report, during the reporting period, member products developed in collaboration with commercial insurance providers (primarily from the Ping An Group) generated cumulative revenues exceeding RMB 200 million and served over one million insurance members. Under this insurance partnership model, annually subscribed commercial insurance members can access comprehensive healthcare membership services provided by Ping An Good Doctor, covering the entire continuum of care from prevention and medical consultation to rehabilitation.

Whether this model is truly successful becomes evident at a glance by examining Ping An Good Doctor’s list of partners. In 2019, Ping An Good Doctor sequentially entered into collaborations with Peking University Founder Life Insurance, Zhujiang Life Insurance, and China Everbright Bank. These partnerships all adopted a “healthcare + insurance” model to provide medical services to members, thereby enhancing user stickiness for insurance products. Ping An Good Doctor’s collaboration with Wyeth also aimed to deliver private physician services to the 12 million members of the Wyeth Moms Club.

In June 2019, Ping An Good Doctor launched its strategic new product, “Private Doctor,” targeting the 200 million middle-class consumers with the aim of digitizing healthcare access and ensuring that “high-quality medical and health resources revolve around users.” Beyond attracting a broader user base, the primary objective of this product launch was to enhance member stickiness.

This also corroborates VCBeat’s analysis of Ping An Good Doctor’s prospectus when news of its IPO emerged: once hospitals, doctors, pharmacies, the medical community, and insurance sectors are fully integrated, Ping An Good Doctor will become the entry point for healthcare services tailored to Ping An Group’s “Big Health” strategy.

Among the eight technology companies, there are notable differences in their healthcare sector strategies.

Apple and Google have primarily focused on smart hardware; Huawei, leveraging its years of accumulated expertise beyond smart hardware, is also attempting to empower healthcare through AI and cloud services; Microsoft, having fallen behind in the smart hardware arena, has pivoted to expand its B-end business via cloud service platforms; JD.com, Alibaba, and Amazon, all e-commerce giants, have adopted similar development paths by entering the healthcare sector through pharmaceutical distribution and subsequently laying out their strategies in technical platforms; Tencent, placing greater emphasis on connectivity, has primarily pursued its healthcare strategy through partnerships.

As a relatively closed sector, pharmaceutical and medical device manufacturing has yet to attract entry from tech giants. This may be attributed to the high barriers to market entry resulting from stringent technical thresholds and rigorous regulatory requirements in the pharmaceutical industry. Moreover, for technology companies, venturing into the pharmaceutical sector offers limited synergy or enhancement to their core businesses.

Apple: Breaking Through with Hardware

2019 Apple Healthcare Milestones

Source: VCBeat Dongguan

Apple’s healthcare strategy is inseparable from its hardware devices. Leveraging a product lineup that includes the iPhone, iPad, iPod, and iMac, Apple has established a comprehensive ecosystem centered on its proprietary hardware. Consequently, Apple’s foray into the healthcare sector uses patents as a fulcrum, focusing on smart hardware devices to drive the health monitoring ecosystem. The Apple Watch, in particular, is a wearable device specifically designed by Apple to integrate into the healthcare landscape.

At the end of 2018, Apple rolled out the ECG feature for the U.S. version of the Apple Watch Series 4, providing users with medical-grade electrocardiogram testing capabilities and alerts for abnormal heart rhythms. In the first half of 2019, this feature was expanded to an increasing number of countries and regions.Patents related to health monitoring are becoming one of the core pivots for Apple to disrupt the healthcare market.

In terms of hardware technology, Apple is developing advanced medical-grade sensors. Furthermore, features such as illumination, cameras, and machine vision on the iPhone can enhance facial recognition, monitoring, and diagnostic capabilities. On the software front, Apple is a major proponent of FHIR (Fast Healthcare Interoperability Resources) technology. The brand itself also serves as a key entry point for Apple’s health monitoring ecosystem. Although tech giants like Google, Microsoft, and Amazon enjoy global renown, Apple—having built its empire on smartphones and boasting a large base of loyal fans—holds a distinct advantage in prioritizing user experience and privacy protection. Financially, Apple is certainly well-capitalized.

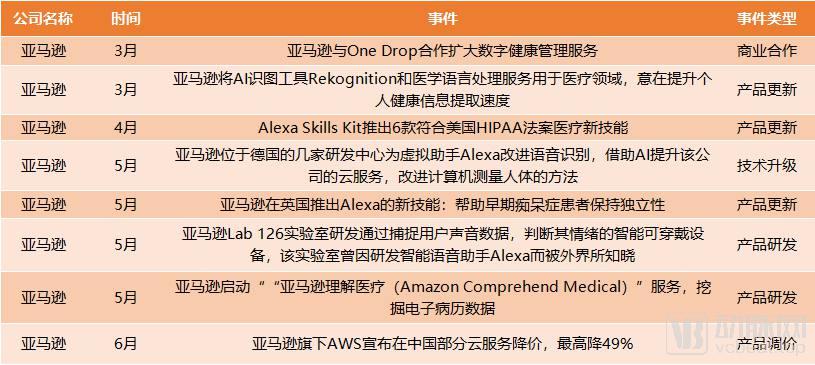

Amazon: Focusing on Technology + Pharmaceutical Retail

2019 Amazon Healthcare Milestones

Data Source: VCBeat Insights

In June 2018, Amazon completed its acquisition of PillPack, an online pharmacy startup, officially entering the pharmaceutical e-commerce sector. Amidst the intricate supply chains in the United States,PillPack through its ownPrescription Drug Management Platform pharmacyOSManage medication distribution, monitoring, and support.It also provides these services to payers, manufacturers, and new companies in the form of a delivery interface. This can be well integrated with Amazon's existing distribution model.

Since entering the healthcare sector, Amazon has not only continued to develop its pharmaceutical retail business but also remained firmly focused on AI technology, continuously expanding the capabilities of its strategic product, Alexa. In the first half of 2019, Amazon further doubled down on Alexa, concentrating on its “Alexa Everywhere” strategy.

In April 2019, Amazon announced the launch of six Alexa healthcare skills compliant with the HIPAA Act;In May, Amazon launched a new Alexa skill in the UK—My Carer Alexa—to help patients with early-stage dementia maintain their independence; in the latter half of May, Amazon also rolled out its “Amazon Comprehend Medical” service, aiming to extract more insights from electronic health record data.

Amazon also possesses channels that directly connect manufacturers, brands, retailers, and consumers, while maintaining its own supply chain, retail stores, and product delivery teams. Amazon can not only build a smart assistant ecosystem around Alexa by integrating it into more third-party products, but its vast base of Prime members also provides a distribution foundation for Alexa-related products.

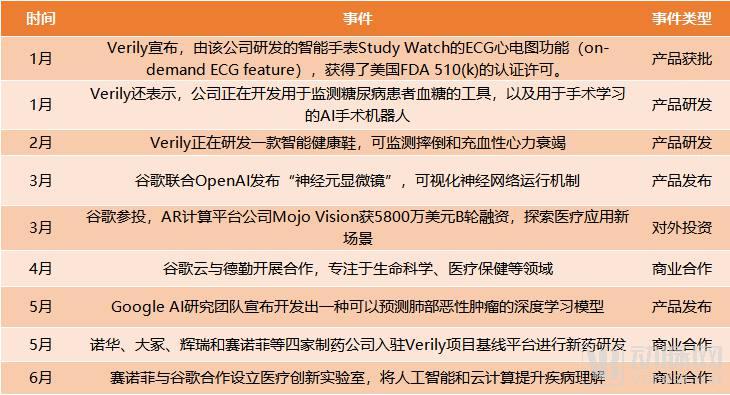

Alphabet (Google’s Parent Company): Medical AI + Traffic Gateway

Alphabet’s 2019 Healthcare Milestones

Data source: VCBeat Dongguan

Following the 2015 restructuring, Google Ventures (GV), Verily, and Calico became subsidiaries under Alphabet responsible for healthcare operations. Among them, Verily serves as Google’s primary vehicle for entering the medical sector.

By examining Google’s strategic footprint in the healthcare sector, it becomes evident that artificial intelligence (AI) serves as the core focus for Google and its subsidiary Verily in their expansion within this field. Although hardware represents the primary product category in their AI-driven healthcare initiatives, the underlying technological foundation relies on Google’s extensive accumulation of AI expertise over the years.

Leveraging its massive search engine as a gateway, Google has amassed health data from billions of users, constituting a significant strategic asset for its entry into the medical AI sector. Furthermore, through collaborations with academic institutions and commercial healthcare organizations, Google gains access to novel, high-value clinical medical data. These datasets, combined with other user information collected by Google, are utilized to train algorithms capable of identifying patterns along the continuum between health and disease.

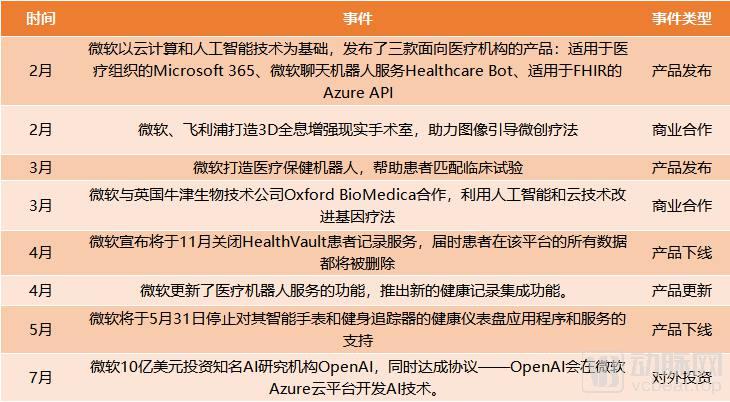

Microsoft: Exiting the B2B Wearables Market

2019 Microsoft Healthcare Milestones

Data source: VCBeat Insights

In the consumer market, Microsoft has been considering a withdrawal since last year due to the poor performance of its consumer-facing products. Senior executives at Microsoft have also explicitly stated that the company will exit the consumer wearables market. A series of moves by Microsoft in 2019 indicated that it might completely withdraw from the consumer market.

After abandoning the consumer segment, Microsoft has shifted its focus to “capturing” the business sector. For Microsoft, this may well be the right choice.

Over the years, Microsoft has accumulated a substantial base of healthcare organization clients. According to a report by Morgan Stanley, more than 25,000 U.S. health organizations are currently using Microsoft Cloud. This market position provides Microsoft with opportunities to upsell to its existing healthcare customers and establish new partnerships. Meanwhile, as the world’s largest provider of computer software, Microsoft possesses inherent advantages in computer vision, speech recognition, image recognition, natural language processing, and expert systems. Its capability to empower business-to-business (B2B) enterprises is significantly stronger than its offerings for consumer-to-consumer (C2C) markets.

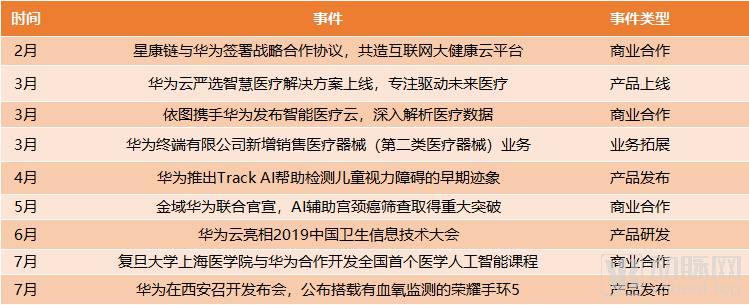

Huawei: Wearables + 5G + Healthcare IT Empowerment

2019 Huawei Healthcare Milestones

Source: VCBeat Insights

Huawei’s initial foray into the healthcare sector primarily focused on wearable devices. Today, Huawei’s wearables have achieved the highest shipment growth rate in China, and the company has established various health laboratories and five global R&D centers. The HUAWEI WATCH GT features Huawei’s self-developed TruSeen 3.0 heart rate monitoring system. In March 2019, Huawei expanded its business scope, a move likely aimed at keeping pace with Apple and Xiaomi by adding further medical capabilities to its wearable devices. On July 23, 2019, Huawei held a new product launch event in Xi’an, unveiling the Honor Band 5, which introduced blood oxygen saturation monitoring. Therefore, in the foreseeable future, Huawei will continue to increase its investment in wearable devices.

While developing wearable devices, Huawei is also leveraging AI and cloud computing services to empower the healthcare sector. In 2019, Huawei disclosed numerous collaborative projects with leading domestic companies in specialized fields, such as Yitu Technology and KingMed Diagnostics. Huawei’s strategic positioning in cloud services benefits from its leadership in 5G technology. As 5G gradually penetrates the healthcare market, Huawei has the opportunity to capitalize on its 5G advantages to secure a leading position.

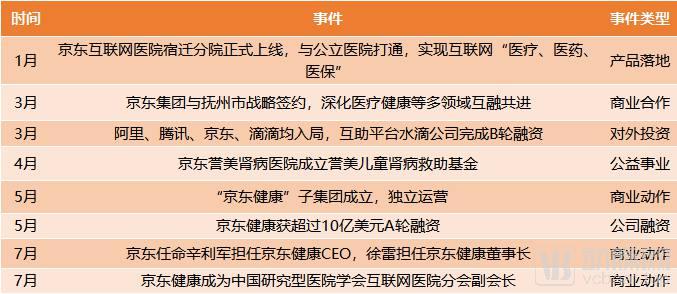

JD.com: Building a New Unicorn in Pharmaceutical Distribution

2019 JD Health Major Events

Data Source: VCBeat Dongguan

In May 2019, JD.com announced the establishment of its “JD Health” subsidiary by integrating four business segments: pharmaceutical retail, pharmaceutical wholesale, internet healthcare, and healthy cities. Concurrently with the release of its first-quarter financial results, the newly formed JD Health announced that it had secured $1 billion in Series A financing, with participation from multiple foreign institutional investors.

JD.com’s strategic layout in pharmaceutical distribution represents its primary direction for development in the healthcare sector. Launched in December 2017, “JD Internet Hospital” serves as the core product of JD Health’s online medical services and is among the first batch of internet hospitals in China to obtain an internet hospital license. In January 2019, Suqian First People’s Hospital was fully integrated into the JD Internet Hospital platform. Meanwhile, with the systematic integration of Suqian’s medical insurance system with JD’s platform, Suqian saw the emergence of the first individual in China to complete an online medical insurance payment on a pharmaceutical e-commerce platform.

Meanwhile, leveraging its unique pharmaceutical supply chain advantages, JD Health pioneered the industry’s first online “medical consultation + medication” closed-loop system. After consulting with a doctor, patients can directly purchase medications on the JD platform and enjoy home delivery services, truly achieving a comprehensive, smart, and convenient patient-centered experience for medical consultations and medication purchases.

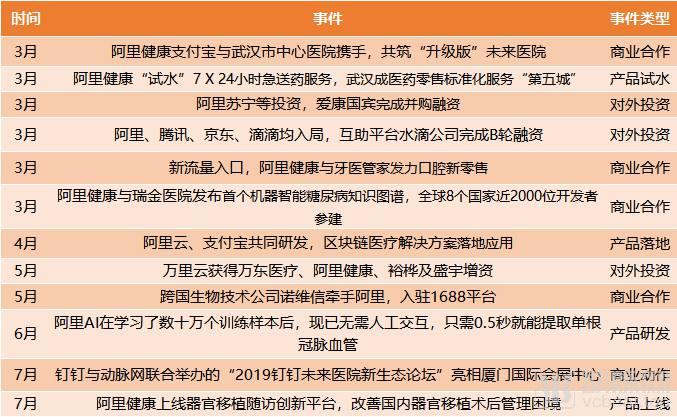

Alibaba: Building a Complete Ecosystem Leveraging AliHealth

2019 Ali Health Medical Milestones

Data Source: VCBeat Dongguan

Alibaba Health is Alibaba Group’s operational platform for implementing and advancing its initiatives in the broader healthcare sector. With its e-commerce origins, Alibaba has always possessed a strong platform-building DNA; consequently, even when launching new products, Alibaba Health tends to prioritize platform-based services. For instance, in March 2019, Alibaba Health piloted a 24/7 emergency medication delivery service in Wuhan, leveraging its operational service capabilities and the deep integration between Alibaba and local pharmacies.

Nevertheless, Alibaba is also seeking new growth engines through technology. For instance, the blockchain-based healthcare solution jointly developed by Alibaba Cloud and Alipay, which was released in April, has been officially implemented for electronic prescriptions at Wuhan Central Hospital, aiming to streamline every link in the prescription circulation process. Alibaba’s AI initiatives are also breaking into the healthcare sector from other angles to enhance clinical efficiency.

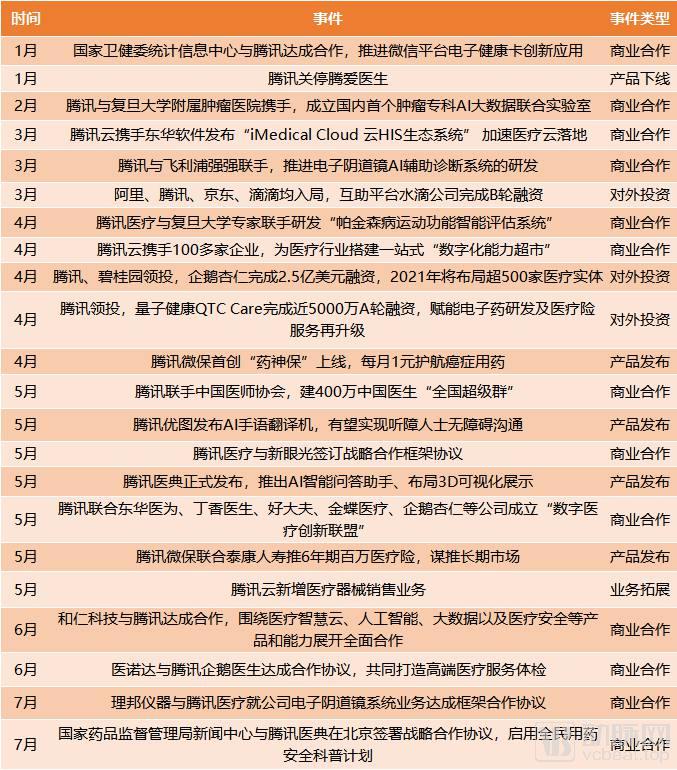

2019 Tencent Healthcare MilestonesSource: VCBeat Dongguan Channel

According to statistics from VCBeat’s Dongguan Channel, of the 22 new developments involving Tencent to date, 13 were commercial collaborations.

In other words, Tencent places greater emphasis on connectivity in the healthcare sector. Meanwhile, Tencent has built a comprehensive ecosystem through initiatives such as Tencent Medical Dictionary, Tencent Youtu, Tencent Cloud, and Yaoshenbao Insurance. The Tencent Medical Dictionary, launched this year, is a key project that fills the gap in the consumer-facing (C-end) market following the shutdown of Tengai Doctor.

Nevertheless, while connecting various stakeholders, Tencent also places significant emphasis on the application of AI technology in the healthcare sector. For instance, in February 2019, Tencent collaborated with Fudan University Shanghai Cancer Center to establish China’s first joint laboratory dedicated to AI and big data for oncology. In April, Tencent Healthcare joined forces with experts from Fudan University to develop the “Intelligent Assessment System for Motor Function in Parkinson’s Disease.” In May, Tencent Youtu launched an AI sign language translator to facilitate barrier-free communication for individuals with hearing impairments.