U.S. Convenient Care Survey: Positive Industry Impact Amid Quality and Cost Concerns, with DTC Telehealth Emerging as Top Competitive Threat

NEJM Catalyst recently released a survey report based on responses from 664 members of the NEJM Catalyst Insights Council, examining the current state of convenient care services in the United States.

The committee comprises healthcare administrators, clinical leaders, and clinicians. The survey explored topics related to convenient care services, such as whether organizations own or have partnered with retail clinics, urgent care centers, and direct-to-consumer (DTC) telehealth providers; the primary benefits of owning or partnering for convenient care; threats or opportunities associated with convenient care; the quality of care in convenient care versus primary care; the impact of convenient care growth on healthcare industry spending; the greatest competitive threat to traditional healthcare organizations; and the overall impact of the proliferation of convenient care on the healthcare industry.

In recent years, a large number of convenient healthcare services have rapidly emerged in the medical industry, such as retail clinics, urgent care centers, and direct-to-consumer (DTC) telemedicine. The U.S. healthcare system has responded in various ways—some providers have incorporated convenient care services by expanding their service offerings, while others have adopted a wait-and-see approach. Surveys indicate that respondents hold diverse views on the value of convenient care models and the next steps for their organizations.

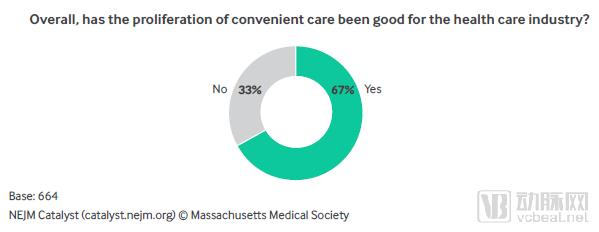

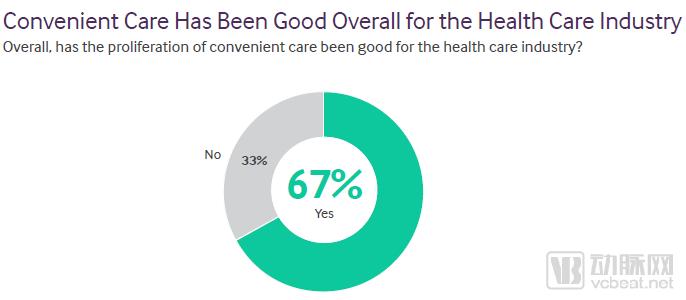

Has the emergence of convenient medical services brought positive impacts to the healthcare industry? 33% No, 67% Yes.

Ateev Mehrotra is an Associate Professor of Health Care Policy and Medicine at Harvard Medical School and a hospitalist at Beth Israel Deaconess Medical Center. His research primarily focuses on innovations in payment models, such as retail clinics and e-visits, and their impact on the quality, cost, and accessibility of healthcare services (these three factors are also the key elements of the “impossible trinity” model in healthcare frequently cited by VCBeat).

“Survey results from NEJM Catalyst show that leaders in the healthcare industry have diverse perspectives on how to respond to convenient care delivery models,” said Mehrotra. “Many view convenient care as a threat, fearing that this model may compromise the quality of medical care and increase healthcare expenditures. Meanwhile, others see it as an opportunity for growth and are integrating these new models into their systems.”

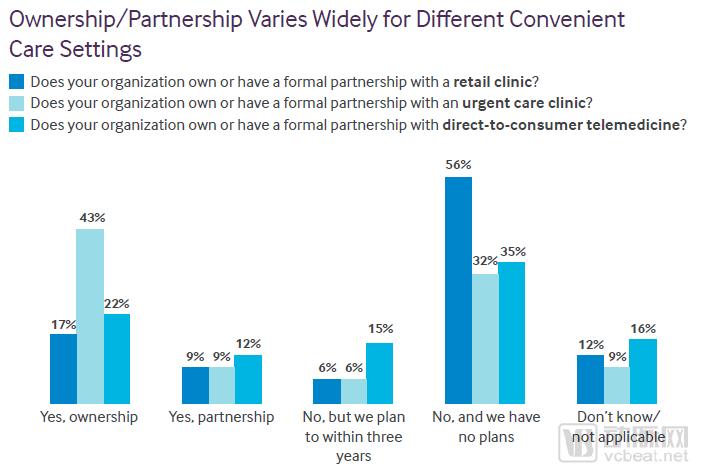

This survey, completed in March 2019, reveals that among U.S. organizations directly involved in clinical care delivery, clinical leaders, administrators, and clinicians are far less engaged with retail clinics than with urgent care clinics, although interest in direct-to-consumer (DTC) telemedicine continues to grow. One-quarter of respondents (26%) reported that their organizations own or co-operate retail clinics, whereas the ownership rate for urgent care clinics exceeds half (52%). Urgent care may align more closely with these organizations’ existing clinical and business models.

“Traditional healthcare providers, facing new competitors and concerns over their bottom lines being impacted, are attempting to meet patient needs by offering retail and urgent care services along with new options enabled by their technology. Many members of the Insights Council are concerned about new entrants such as CVS Health-Aetna.”

Institutional Ownership/Partnership Status for Various Convenient Medical Services

Findings from the VBInsight Council survey indicate that approximately one-quarter (26%) of members hold ownership or partnership interests in retail clinics, with little evidence to suggest this figure will change significantly in the coming years. Survey responses also reveal that urgent care clinics have a higher penetration rate than retail clinics, and about one-third (34%) of respondents reported that their organizations hold ownership or partnership interests in direct-to-consumer telehealth services.

However, although an almost equal proportion (35%) indicated that they do not plan to engage in telemedicine, the remaining 15% intend to do so within three years, which would bring the participation rate to nearly half (49%).

Among the surveyed organizations, the ownership rate of DTC telemedicine was 34%, yet this model offered the greatest potential advantages among the three convenient healthcare service models. While 6% of the surveyed organizations planned to introduce retail clinics and urgent care clinics, 15% intended to launch telemedicine services within the next three years.

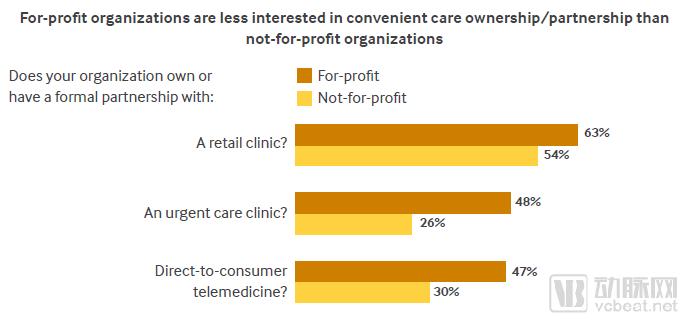

For-profit institutions show less interest than non-profit institutions in holding or partnering for rights to convenient healthcare services.

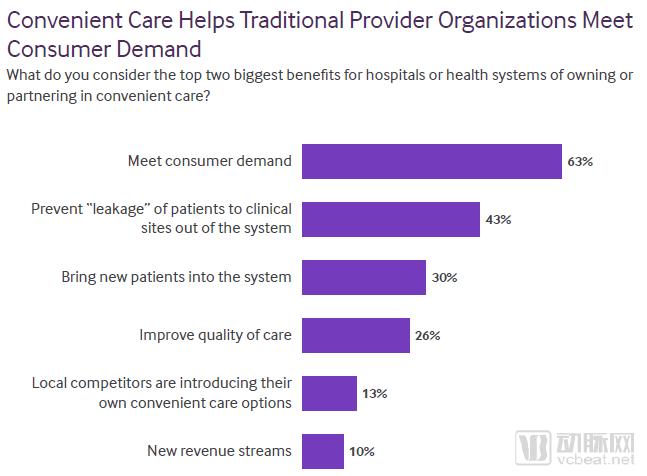

Members of the VBInsight Council pointed out that the two major benefits of owning or partnering with convenient medical services are meeting consumer demands and preventing patient leakage to external clinics. 63% of respondents believed that the greatest advantage for hospitals and health systems in introducing or collaborating with convenient care facilities is their ability to meet consumer needs. The second most cited benefit (43%) was addressing competitive threats and preventing patient attrition. Among nonprofit organization respondents, 66% considered meeting consumer demands the primary advantage, whereas a relatively smaller proportion—55%—of those from for-profit organizations shared this view.

Convenient Medical Services Help Traditional Healthcare Institutions Meet Consumer Needs

Q: What are the two biggest advantages of ownership or partnership between hospitals/health systems and convenient care facilities?

63% to meet consumer needs, 43% to prevent patient leakage outside the system, 30% to attract new patients, 26% to improve care quality, 13% to encourage local competitors to develop new convenient care models, and 10% to generate more revenue

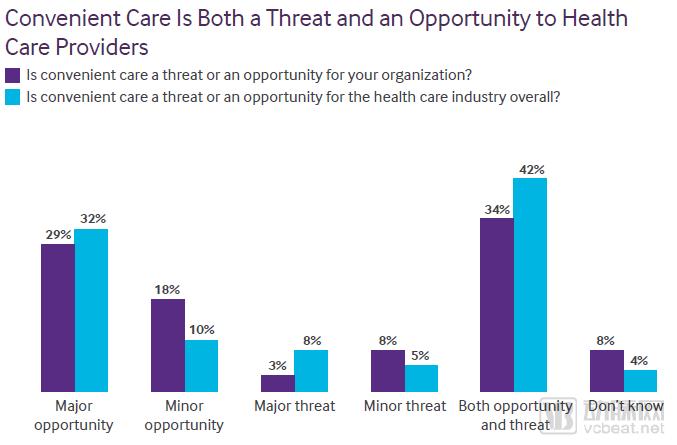

Survey respondents believe that convenient medical services present more opportunities than threats to organizations and the industry. An equal proportion of respondents (42%) believe that convenient medical care can serve as either a primary or secondary opportunity for the healthcare industry, or simultaneously represent both an opportunity and a threat.

Convenience for medical staff presents both an opportunity and a threat to the health insurance industry.

“Many people view convenient healthcare as a threat, fearing that this model may compromise the quality of medical care and increase health insurance expenditures. Meanwhile, others see it as an opportunity for development and are integrating these new models into their systems.”

Edward Prewitt, Editor-in-Chief of NEJM Catalyst, stated: “Traditional healthcare providers, facing new competitors and threats to their interests, are attempting to meet patient needs by offering retail clinics, urgent care services, and new technology-enabled services. Many members of the Insights Council express concern about new entrants, such as the CVS Health–Aetna merger completed late last year.”

In late November 2018, CVS Health, the largest prescription drug retailer in the United States, acquired Aetna. Interviewees commented on the impact of this transaction within the industry. A clinical executive from the western United States stated, “The alliance between major payers and convenient care providers is beneficial for corporate growth; however, it will continue to erode the primary care sector and drive up overall healthcare expenditures.”

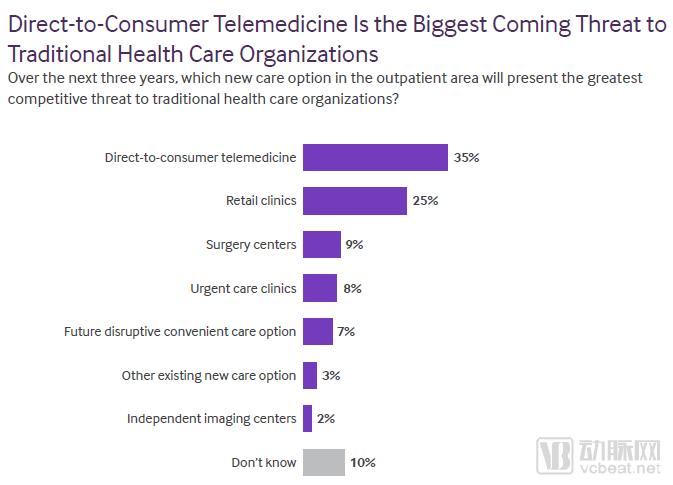

Telemedicine Will Become the Biggest Competitor to Traditional Healthcare Institutions

Q: Over the next three years, which outpatient care model poses the greatest threat to traditional healthcare?

35% telemedicine, 25% retail clinics, 9% ambulatory surgery centers, 8% urgent care clinics, 7% future breakthrough convenience care initiatives, 3% other existing novel care models, 2% independent imaging centers, 10% unsure.

Direct-to-consumer telemedicine will become the most formidable competitor to traditional healthcare institutions within three years. One-third of respondents (35%) identified telemedicine as the greatest competitive threat to the traditional healthcare industry, followed by retail clinics (25%), while urgent care clinics posed the least significant threat (8%).

Mehrotra stated, “I had initially hypothesized that retail clinics would emerge as the most disruptive new model following the merger of Aetna and CVS; however, survey results indicate that direct-to-consumer (DTC) telemedicine ranks first. Interestingly, while DTC telemedicine services currently operate on a much smaller scale compared to other alternatives, nationwide data in China show higher visit volumes for urgent care clinics. This may be because novel concepts are often more intimidating than familiar ones.”

Mehrotra added, “We have recently documented the growth of telemedicine in our research. Although its utilization rate remains very low nationwide, the growth curve is impressive. This may be partly why some healthcare institutions view it as a threat. Furthermore, while telemedicine providers offer services on a national scale, traditional healthcare institutions have always operated with a relatively localized scope. The broad geographic coverage and lower barriers to entry associated with these emerging services represent another form of competition.”

Prewitt stated that healthcare providers in the industry are gradually realizing that the impact of telemedicine is imminent. “Although telemedicine has existed for a long time, it was only after some regulatory barriers were overturned recently that people finally saw its huge potential.”

Healthcare industry leaders selected the service models they deemed most suitable for their organizations during the survey. A small minority of respondents (13%) indicated that their organizations were engaged in all three convenient care delivery models. However, achieving this requires substantial organizational scale and financial resources. Survey data further confirm that large healthcare systems and hospital-led entities dominate the provision of these comprehensive convenient care services.

Quality and Cost Issues in Convenient Healthcare

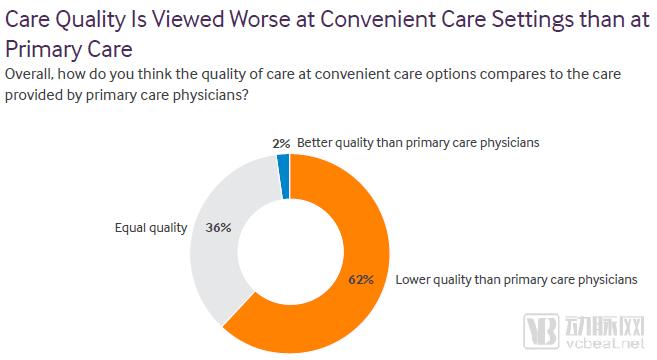

A notable survey finding reveals that nearly two-thirds (62%) of respondents believe the quality of care provided by convenient medical services is inferior to that of primary care physicians. Compared with management personnel (52%), a higher proportion of clinicians (68%) and clinical leaders (64%) consider the quality of care delivered by convenient medical services to be below the standard of primary care physicians.

The quality of care in convenient healthcare is not viewed favorably.

Q: How would you evaluate the overall quality of care in convenience healthcare compared to primary healthcare?

38% equivalent in quality, 62% inferior to primary care physicians, 2% superior to primary care physicians

Mehrotra stated, “These concerns are well-founded. Last year, we published several papers on the quality of direct-to-consumer (DTC) telemedicine services, highlighting various quality issues. For instance, in pediatric cases, we observed overprescription of antibiotics, incomplete examinations, and increased follow-up rates.”

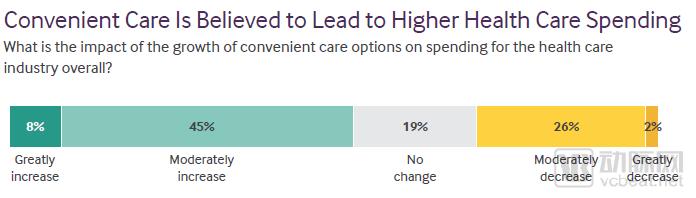

Survey respondents also expressed concerns about the impact of convenient care on health insurance costs. More than half (53%) indicated that the increased availability of convenient care options would significantly or moderately raise overall industry spending. Over half of the respondents believed that the expansion of convenient care has increased total expenditures in the healthcare sector. A higher proportion of clinical leaders (59%) and clinicians (55%) held this view, compared with management personnel (46%).

Convenient Medical Services Have Raised Overall Expenditure in the Healthcare Industry

Q: What impact do you think the expansion of convenient healthcare services has on overall healthcare industry spending?

8% significant increase, 45% moderate increase, 19% no impact, 26% moderate decrease, 2% significant decrease.

Cheaper Options May Increase Total Spending? This May Seem Counterintuitive. But Mehrotra Believes Healthcare Leaders’ Intuition Is Correct. “This Has Been the Focus of My Research: Attempting to Quantify the Impact of Convenient Care Solutions on Spending. Surveys Show That Retail Clinics and Direct-to-Consumer (DTC) Telemedicine Both Increase Healthcare Expenditures. However, We Estimate That This Increase Is Only Modest.”

“For example, retail clinics are approximately 30% to 40% less expensive than visits to a physician’s office. Therefore, considering retail clinics as substitutes for in-person consultations does yield cost savings. However, most retail clinics are not substitutes but rather independent new offerings. In the absence of retail clinics, patients would choose to stay at home. The same applies to direct-to-consumer (DTC) telemedicine; we estimate that approximately 90% of these consultations represent incremental service utilization.”

Although findings on the impact of convenient healthcare services on individual organizations, quality, and costs have been mixed, two-thirds (67%) of Insights Council respondents stated that the proliferation of convenient healthcare is beneficial to the healthcare industry. Prewitt noted that this is likely because it helps improve mass access to healthcare and addresses unmet needs among patient populations. More than two-thirds of respondents believed that convenient healthcare has had a positive impact on the medical industry. The proportion was slightly higher among management personnel (74%), while 65% of clinicians and 64% of clinical leaders agreed.

Convenient healthcare has had a positive impact on the medical industry.

Q: Overall, has the expansion of convenient healthcare brought benefits to the medical industry?

“While operating convenient medical facilities, traditional healthcare providers are responding to consumer demands,” he said. “Despite their concerns, patients all wish to make the most of their time by completing consultations as quickly as possible.”

Compiled by: Zhang Xian

Report Source: https://catalyst.nejm.org/