Second Wave of 'Genetic Testing + Insurance' Pilots: Who Pays When Targeted Cancer Drugs Fail?

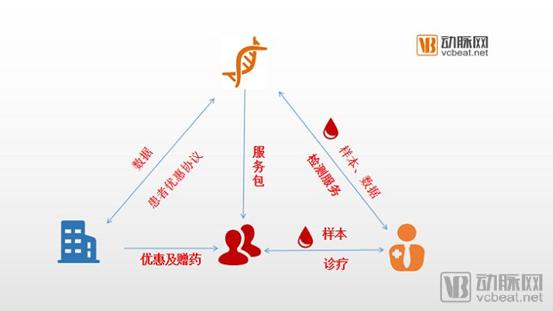

In late July, Zhenhe Technology announced a strategic partnership with Nuohui Medical and Beijing Jianyibao. By leveraging complementary strengths, Zhenhe Technology will establish an integrated four-dimensional platform encompassing “genetic testing, clinical diagnosis and treatment, insurance, and patients,” and jointly launch the “Lung Cancer NGS Testing and Combination Therapy Coverage Plan” with Nuohui Medical and Beijing Jianyibao.

Zhenhe Technology is not the first domestic cancer testing company to launch such a product. Six months ago, another cancer testing company also announced an innovative payment insurance plan for tumor detection and therapeutic medication. Through the deep integration of genetic testing, clinical diagnosis and treatment, and insurance, this approach appears to be emerging as a product model under discussion among cancer testing companies, further promoting the innovation and development of precision medicine in China.

In fact, as early as 2016, the genetic testing sector experienced a surge in “gene + insurance” combination products. Major companies such as BGI Genomics, Daan Gene, Novogene, ZhongAn Insurance, Taikang Life, and China Pacific Insurance participated in these initial trials. However, the products launched at that time were predominantly consumer-oriented tests. Genetic testing companies primarily served as providers of testing kits, while insurers retained greater control over the offerings. Due to the weak integration between biotechnology and insurance payment mechanisms, this initial endeavor ultimately fizzled out.

The newly launched products represent significant breakthroughs in patient medication and commercial insurance payment. As an exploration into integrating commercial insurance with oncology genetic testing and medication payment, these products hold promise for innovating business models by combining technology with payment solutions. In this article, we interviewed companies engaged in the development of “genetic testing + insurance” products, as well as other industry experts, aiming to address the following four questions:

1. What Problems Does “Medication Insurance” Solve, and Who Pays for It?

2. How do all parties benefit?

3. Who is involved?

4. How will it develop in the future?

The core of oncology medication insurance is to address patients’ payment challenges. While consumer-grade testing insurance products revolve around the risk of future diseases, medication insurance focuses on current illnesses, providing coverage for individuals who are already diagnosed. It serves as a hub for multi-party integration, offering benefits to patients, insurers, and testing companies alike.

Following the initial testing, neither patients, their families, nor physicians can determine with certainty whether the medication will be effective; thus, this is inherently a risk-selection decision. During this process, insurance products are bundled and sold alongside the diagnostic tests. If a patient’s disease progresses or metastasizes despite taking targeted therapy as guided by the test results, the insurance company will provide compensation to the patient.

Although research on mutated genes and targeted therapies for lung cancer is relatively mature, there are still clinical cases where patients with specific mutations do not respond to the prescribed medications. The core purpose of medication insurance products is to address patients’ financial burden in such scenarios; if the treatment proves ineffective, insurance compensation can support patients in undergoing secondary testing.

These are the prerequisites for the existence of “Medication Insurance” products; only by addressing this pain point can the product logic hold water. Furthermore, as insurtech companies and health management firms gradually align with market demands, seeking to bridge the gap between insurance providers and healthcare enterprises to create a comprehensive service covering payment, diagnosis, and treatment, “Medication Insurance” products have emerged. Typically, the insurance premiums are covered by testing companies, thereby imposing no additional financial burden on patients. Given that tumor medication testing and subsequent treatment costs are already substantial, adding further costs for patients and their families would undoubtedly hinder the promotion of such products.

For insurance companies, launching “medication insurance” represents a completely new endeavor, as the insured population is not composed of healthy individuals. Furthermore, in traditional commercial insurance, insurers incur disproportionately high expenses on distribution channels and sales personnel. Most insurance agents are primarily sales-oriented and largely lack backgrounds in medicine or healthcare. If genetic testing companies promote these insurance products through their own channels, the sales representatives would possess stronger professional expertise, while insurers could save significantly on channel-related costs.

Moreover, insurance companies and health management firms can obtain first-hand clinical and prognostic data on the insured population during this process. Such data are highly valuable to these entities and will play a significant role in the future design of other health insurance products.

For physicians, this additional insurance service also helps alleviate concerns about subsequent treatment plans, thereby indirectly improving patient adherence. In the event of a covered claim, the insurer can provide tangible compensation to patients to support future treatment needs.

“In this collaboration, both doctors and patients are direct beneficiaries,” Dr. Wang Fanping, Vice President of Business Development at Zenith & Harmony Technology, told VCBeat.

For testing companies, the fact that insurance carriers are willing to collaborate with them to jointly launch medication insurance products inherently signifies the insurers’ endorsement of the accuracy of their tests. The introduction of such co-branded products means that the test results are backed by insurance underwriting. Furthermore, since these insurance products do not impose additional costs on patients, they serve as a value-added benefit provided by the genetic testing company from the patient’s perspective. Under comparable conditions, this business model and product offering will be more competitive.

More importantly, such cross-sector collaborations have strengthened testing companies’ penetration into the industry value chain, enabling them to further reach the forefront of the industry in areas such as insurance reimbursement, clinical application of pharmaceuticals, and efficacy tracking. This allows them to accumulate industrial experience in exploring the “integration of healthcare and insurance” model and to establish a four-dimensional integrated platform encompassing “genetic testing + clinical diagnosis and treatment + insurance + patients.”

Currently, two companies have successively launched medication insurance products in the market. Focusing on high-incidence cancer types in China, they have taken the first step in involving commercial insurance in precision medicine.

Burning Rock Biotech

Genecast Biotechnology was founded in 2016, focusing on the research and development of international high-tech solutions and their clinical translation in the field of oncology. In February 2019, Genecast Biotechnology, in collaboration with Beijing Jianyibao and Shanghai Nuohui Medical, launched China’s first innovative payment insurance plan tailored for tumor testing and targeted therapy medications.

The program, titled “Oncology Testing and Combination Therapy Diagnostic and Treatment Insurance,” is underwritten by a well-known domestic life insurance company. In its initial phase, this diagnostic and treatment insurance will provide coverage for breast cancer patients with ERBB2 (HER2) or BRCA1/2 gene mutations, as well as lung cancer patients with EGFR, ALK, or ROS1 gene mutations.

Patients who undergo tumor genetic testing using the next-generation sequencing (NGS) technology from Ben Medical Technology and agree to enroll in the insurance program are eligible to receive commercial diagnostic and treatment insurance free of charge. During the coverage period, if tumor progression occurs despite the patient following the prescribed treatment guidelines, they may receive compensation of up to RMB 20,000.

Zhenhe Technology

Zhenhe Technology is a precision oncology company specializing in non-invasive precision diagnosis and treatment of cancer, as well as companion diagnostics, providing personalized health guidance to patients. In July 2019, Zhenhe Technology co-designed and developed an insurance product for lung cancer medication with Nuohui, named the “Lung Cancer NGS Testing and Combination Therapy Coverage Plan.” This plan currently covers lung cancer patients who undergo genetic testing for BestBo-guided medication at Zhenhe Technology. These patients receive this insurance service complimentary when using BestBo for testing. If a patient experiences tumor progression or metastasis within two months while taking one of the nine recommended targeted anticancer drugs listed in the report—such as Iressa, Tagrisso, or Anshengsha—they are eligible for corresponding compensation based on the specific targeted therapy used.

It is understood that these reimbursements are provided in the form of "supplementary medical insurance" and can be used to cover out-of-pocket expenses for targeted therapies incurred by patients beyond the coverage of social health insurance and their private commercial insurance.

“We have always believed that the greatest value of testing lies in assisting physicians with clinical decision-making, thereby guiding patient medication more effectively,” said Wang Fanping. The design of medication insurance is driven by the needs of both physicians and patients, aiming to support lung cancer patients who experience disease progression or metastasis despite using targeted therapies based on genetic test results, due to factors such as drug efficacy and the complexity of genetic mutations. They hope to receive certain insurance payouts to support their subsequent diagnosis and treatment.

It was revealed that Trust Mutual Insurance, the insurance company currently partnering with Zhenhe Technology, is an insurer under Alibaba. In addition, Zhenhe Technology is currently in discussions with multiple other insurance companies regarding additional “genetic testing + insurance” projects. The company plans to collaborate with more industry partners in the future to develop insurance plans covering a broader range of cancers and offering more comprehensive coverage options.

Nuohui Medical

Founded in November 2018 and headquartered in Shanghai, Nuohui Medical is a professional provider of innovative medical payment and insurance solutions. The company primarily offers commercial health insurance and payment solutions for major diseases, including medication reimbursement, efficacy guarantees, and medication assurance programs, with the aim of reducing patients’ out-of-pocket expenses and improving medication accessibility and adherence.

"Unlike traditional models that base insurance product design on policy terms and then incorporate drugs and treatment services, NuoHui Medical takes disease treatment itself as the starting point for designing insurance products. Leveraging professional medical expertise and extensive clinical experience, it precisely addresses patients’ core needs to reduce medical costs while ensuring treatment efficacy. It acts more like a bridge between insurance companies and enterprises, creating a complete closed-loop within the healthcare system."

This company is, in fact, the architect behind the “Medication Insurance” products offered by Zhiben Medical Technology and Zhenhe Technology. Its team primarily consists of professionals from healthcare resource providers, with some members having previously led core product development at insurance institutions. Leveraging their pharmaceutical industry experience and resources, the team ensures that Nuohui Medical’s insurance offerings are underpinned by scientifically robust financial models and well-structured policy terms.

To date, Nuohui Medical has completed two rounds of financing, with investors including Legend Star and BV Baidu Venture Capital.

It is not difficult to observe that the medication insurance products launched by the aforementioned two companies are both related to lung cancer. Whether in terms of mutation sites or targeted therapies, research and products associated with lung cancer are more abundant. Furthermore, as lung cancer has the highest incidence rate among all cancers in China, it represents the preferred choice for medication insurance products in terms of population coverage. Breast cancer, on the other hand, is the most prevalent cancer among Chinese women, and there is also a relatively rich array of targeted therapy products available for this indication.

However, such products are merely the first step. In interviews with Geneseeq Technology, the company repeatedly emphasized its intention to deepen its engagement in “genetic testing + insurance” products. Beyond expanding coverage to more cancer types and launching additional medication insurance products for a wider range of therapeutic drugs, how might the “genetic testing + insurance” model evolve and advance in the future? Previously, Mr. Shi Shangliu, a reader of VCBeat, contributed an article titled “How Tumor Targeted Drug Testing Companies Innovate Their Business Models,” which offered extensive insights into the future prospects of “tumor medication testing and insurance.” We have once again interviewed Mr. Shi Shangliu, aiming to explore further possibilities for integrating NGS technology with insurance.

Shi Shangliu believes that insurance covers risk-related behaviors, and all products with risk attributes can be integrated with insurance. In addition to medication insurance products for patients, ancillary products targeting patients’ family members may also warrant attention.

“If a relative is diagnosed with a tumor, family members tend to pay closer attention to their own health status,” stated Shi Shangliu. Therefore, he believes that in addition to the current single-item testing for tumor medications, tumor risk screening for patients’ family members could also be offered as an optional add-on.

Of course, such a combination is merely lightweight. The core issues in oncology treatment are solutions and payment. Neither testing companies nor insurance companies will directly participate in the research and development of oncology solutions. Therefore, the collaboration between the two holds more promise for addressing the payment issue.

Currently, most pharmaceutical manufacturers are implementing a patient assistance program wherein patients who demonstrate a sustained response to a specific targeted therapy become eligible for complimentary medication after completing a predefined treatment duration (e.g., three or six months). However, the complimentary medication is dispensed at regular intervals, typically on a monthly basis, and requires in-person pickup by the patient. Furthermore, patients must undergo periodic examinations at designated hospitals, obtain signatures from specified physicians, complete required forms, and submit these documents back to the pharmaceutical manufacturer.

To receive free medication, patients must undergo regular medical examinations. However, there is currently no systematic framework or standardized guidelines for the medical tests that patients should receive. Taking lung cancer as an example, patients typically undergo a chest CT scan every three months to monitor for tumor recurrence or progression. If no such changes are detected, the treatment is deemed effective, and the patient may continue with the current regimen. Nevertheless, this approach carries hidden risks: lung cancer has a high propensity for brain metastasis, making chest CT scans alone insufficient. Regular contrast-enhanced brain MRI scans are also necessary.

However, if permitted, patients could also consider undergoing circulating free DNA (cfDNA) testing in their blood during this process. This gives rise to a potential business model: testing companies could offer patients an initial bundled package. If a patient purchases the company’s testing services and the test identifies a suitable targeted therapy, the patient would then undergo periodic MRI scans (benefiting hospitals) and cfDNA tests (benefiting the testing company). The cost of these examinations, when purchased as part of a bundled package (with installment payment options), would be lower than purchasing them individually. Furthermore, throughout this process, the testing company could collaborate with pharmaceutical manufacturers to offer discounts on drug prices to patients who sign long-term agreements (providing long-term benefits to pharmaceutical companies). Through more comprehensive monitoring and follow-up, hospitals can promptly detect any abnormalities in patients and adjust treatment plans accordingly (benefiting patients).

This model is not only suitable for companies offering free medication samples but also applicable to pharmaceutical manufacturers whose patients must pay out-of-pocket (or receive partial reimbursement) for their medications. Furthermore, value-added services can be integrated into the ecosystem chain, such as expedited medical access channels (with a corresponding increase in the price of the bundled service package). It is even possible to collaborate with insurance companies to develop tailored insurance products designed specifically to support such bundled service solutions.

Of course, the above content is merely a vision for the future form of “genetic testing + insurance” products. Given the numerous stakeholders involved, reality may not prove as ideal. However, it is certain that cross-industry collaboration between the insurance and genetic testing sectors will continue. From consumer genetic testing insurance to NIPT insurance, and now to pharmacogenomic insurance, the genetic testing industry’s exploration into the insurance sector has never ceased.

On the other hand, China’s commercial health insurance market has been experiencing robust growth in recent years. The emergence of internet-based insurers has further accelerated this rapid expansion, with innovation embedded in the DNA of these new-age companies, which are keen to develop products that break away from traditional models. Meanwhile, established large-scale insurers and reinsurers are also proactively seeking transformation, aiming to achieve breakthroughs in insurance product development.

No one can provide a definitive answer regarding how “genetic testing + insurance” products will evolve in the future or what new forms they may take. However, one thing is certain: the recent emergence of several “medication insurance” products is merely the prologue to a larger story. The industry has already taken its first step in exploring new business models for oncology testing and innovative payment mechanisms for cancer diagnosis and treatment.

THE END