Qiming Medical Files for Hong Kong IPO: Backed by 6 Funding Rounds and 379 Patents, How Will This Heart Valve Unicorn Compete Globally?

Venus Medtech

Artificial Heart Valve System Device Developer

On August 6, Venus Medtech (Hangzhou) Inc. (“Venus Medtech”) submitted its IPO prospectus to the Hong Kong Stock Exchange. The prospectus disclosed that the joint sponsors for this Hong Kong listing application are CICC, Goldman Sachs (Asia) L.L.C., UBS Securities, and China Merchants Securities. After numerous twists and turns, Venus Medtech’s path to going public appears to have finally been settled.

In 2006, the founding team of Venus Medtech embarked on the research and development journey in the field of transcatheter valve therapy, with the company being formally established three years later. In 2014, the VenusA-Valve transcatheter aortic valve and the VenusP-Valve transcatheter pulmonary valve were included in the first batch of the “Special Examination and Approval Procedure for Innovative Medical Devices” (Green Channel). They received support from the National Science and Technology Support Program of the 12th Five-Year Plan under the Ministry of Science and Technology and are currently implementing key projects under the National Science and Technology Support Program of the 13th Five-Year Plan.

Over the past few years, Venus Medtech has achieved numerous milestones. It won the Grand Prize in China’s biomedical industry for its “Novel Biological Heart Aortic Valve Project” and became the first domestic interventional valve company to receive clinical trial approval from the China Food and Drug Administration (CFDA).

In terms of financing, Venus Medtech has enjoyed a smooth journey, bolstered by support from industry heavyweights. Since 2010, the company has successively secured investments from Qiming Venture Partners, Sequoia China, and Goldman Sachs.

Venus Medtech Financing Overview

However, the high-value consumables market for heart valves is already crowded with formidable players. With overseas giants such as Medtronic and Edwards Lifesciences blocking the way, and domestic listed companies like MicroPort CardioFlow, MicroPort Endovascular, and Lepu Medical catching up, how can Venus Medtech carve out a path to break through in the heart valve sector?

On August 4, Blue Sail Medical’s acquisition of the Swiss heart valve company NVT thrust the high-value consumables sector for heart valves into the spotlight. Just two days later, Venus Medtech officially released its prospectus for listing on the Hong Kong Stock Exchange. Behind the overt and covert competition among multiple companies lies a potential market worth tens of billions of yuan.

In China, with the advent of an aging society, the incidence of degenerative valvular disease in the elderly is continuously increasing, among which aortic stenosis has gradually become the most common valvular heart disease in this population. Due to advanced age, poor physical condition, severe disease status, or multiple comorbidities, these elderly patients are unable to undergo open-heart surgery. The emergence of transcatheter aortic valve replacement (TAVR), a minimally invasive surgical technique, has brought hope to these elderly patients.

On October 3, 2010, Professor Ge Junbo from Zhongshan Hospital Affiliated to Fudan University in Shanghai successfully performed the first TAVR procedure in China, pioneering the field of TAVI in the country. However, due to limitations in valve devices, TAVR did not develop well domestically, and the domestic valve market remained monopolized by imported brands. It was not until 2017 that Venus A, a domestically produced TAVI valve co-developed by Venus Medtech, finally received approval for market launch. In 2018, Venus Medtech implanted valves via the transfemoral approach in over 2,000 cases, ten times the number achieved by its competitors.

Nowadays, Venus A has entered the second-generation TAVR stage, and TAVR technology is gradually becoming widespread in top-tier hospitals, with the potential demand for heart valves gradually emerging. According to current indications, there are at least 500,000 patients in China who meet the criteria for TAVR, and the vast majority of these patients have not been hospitalized for treatment. Data from Huatai Securities shows that by the end of 2018, more than 80 hospitals had experience performing TAVR procedures, indicating that this field is still in its infancy. As this technology enters more hospitals, the domestic market is expected to exceed RMB 10 billion by 2029.

In terms of market share, Edwards and Medtronic have carved out 65% and 30% of the global TAVR market, respectively. However, in the Chinese market, only Edwards is domestically registered. In contrast, Venus Medtech, a latecomer that has rapidly risen to prominence, holds an absolutely leading position. Meanwhile, against the backdrop of import substitution and Sino-U.S. trade competition, Venus Medtech’s potential competitors are increasingly coming from among China’s many leading medical device manufacturers.

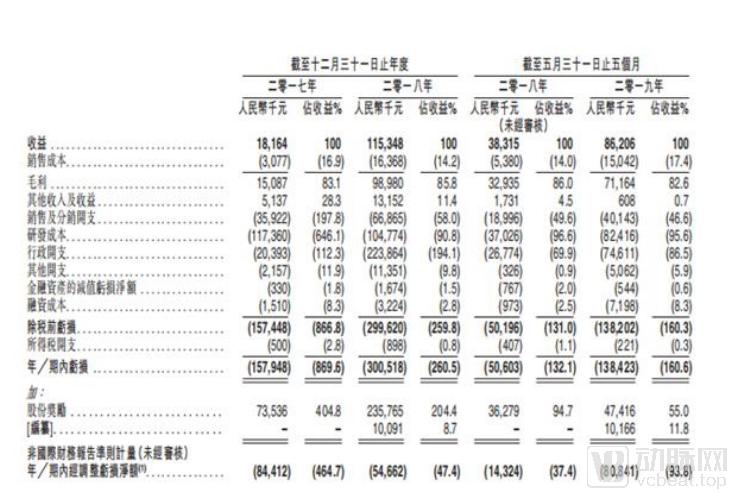

The prospectus submitted this time shows that Venus Medtech's turnover for the first five months of 2019 was RMB 86.206 million, a year-on-year increase of RMB 47.891 million from RMB 38.315 million in the same period of 2018; Venus Medtech's turnover for the full year of 2018 was RMB 115 million, an increase of RMB 97.184 million from the same period of the previous year. Venus Medtech's gross profit for the first five months of 2019 was RMB 71.164 million, an increase of RMB 38.229 million compared with RMB 32.935 million in the same period of 2018; Venus Medtech's gross profit for the full year of 2018 was RMB 98.98 million, an increase of RMB 83.893 million from the same period of the previous year.

Source: Venus Medtech Prospectus

Venus Medtech’s R&D expenses have surged accordingly. As disclosed in its prospectus, although the company’s R&D expenses decreased slightly in 2018, from RMB 117.36 million to RMB 104.774 million, they rose from RMB 37.026 million in the first five months of 2019 to RMB 82.416 million, representing a month-on-month increase of 122.6% and approaching the full-year R&D expenses for 2018. Overall, Venus Medtech’s R&D expense ratios were 646.1%, 90.8%, and 95.6% as of 2017, 2018, and the first half of 2019, respectively.

In addition to being used for the upgrade and iteration of the existing Venus product series, R&D expenditures also cover the substantial design and development costs for two valve technologies: transcatheter mitral valve repair (TMVR) and transcatheter tricuspid valve replacement (TTVR). These products account for the majority of R&D spending.

Venus Medtech’s administrative expenses also saw a significant increase. In the first five months of 2018, this figure stood at only RMB 26.774 million, whereas in the remaining seven months of the same year, it surged to RMB 197.090 million. On a comparable basis, Venus Medtech’s administrative expenses for the first five months of 2019 amounted to RMB 74.611 million, representing a month-on-month increase of 178.7%.

VCBeat speculates that after Venus Medtech acquired Keynote Heart in December 2018, it likely bore the FDA approval costs for related products, while the expansion of its product pipeline in 2019 accelerated administrative expenses for that year.

High R&D and administrative expenses have led to continuous losses for Venus Medtech. The prospectus shows that as of May 2019, Venus Medtech's loss amounted to RMB 80.841 million.

Venus Medtech’s operational shortcomings are equally evident. Although the company’s sales revenue approached RMB 100 million, its revenue sources were relatively concentrated, with the VenusA-Valve accounting for the vast majority of sales income. In 2017, 2018, and the five months ended May 31, 2019, sales revenue from the VenusA-Valve represented 95.4%, 98.6%, and 99.4% of total revenue, respectively.

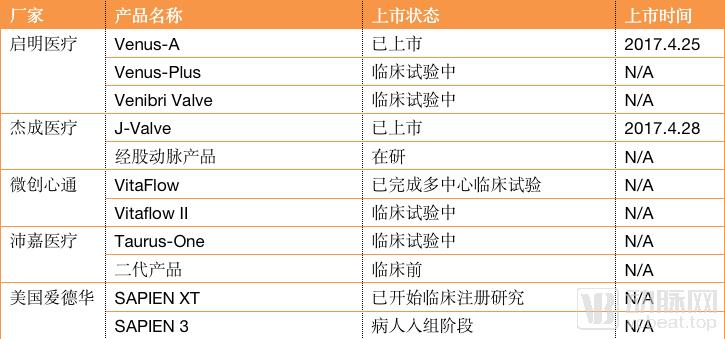

In addition, two other products from Venus Medtech, the VenusA Plus and the Venibri Valve, are both in clinical trials, making their specific market launch dates uncertain. Therefore, the VenusA-Valve is likely to remain the primary contributor to Venus Medtech’s sales revenue for a considerable period.

Data sourced from Yaozhi.com and Huatai Securities Research Institute

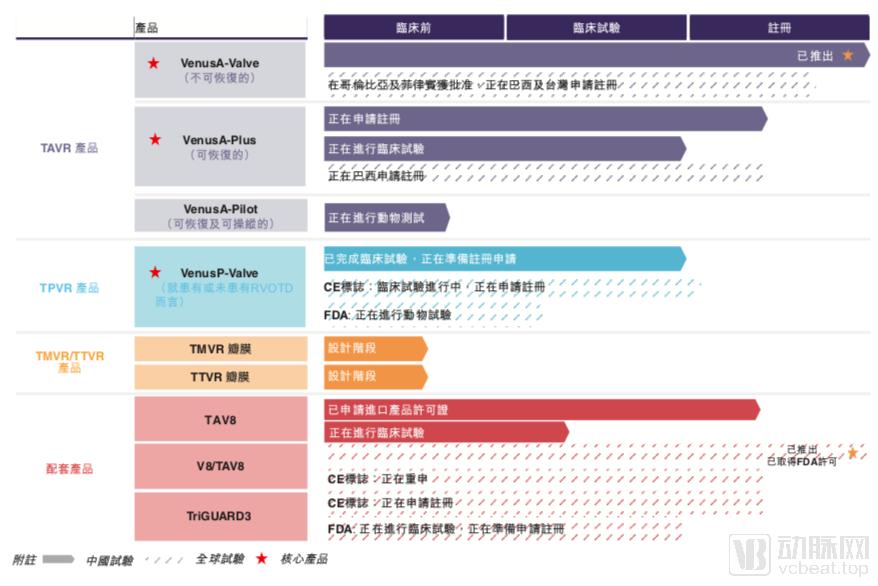

However, Venus Medtech’s R&D pipeline has gradually expanded. Building on its existing TAVR technology, the company is attempting to make implanted prosthetic valves controllable. The VenusP-Valve, currently in clinical trials, is the world’s first self-expanding pulmonary valve. It has been implanted in 178 patients across 27 medical centers in nearly 20 countries and regions, with favorable follow-up results. Market approval is expected in 2019.

Venus Medtech has also initiated clinical trial designs for its cutting-edge transcatheter mitral valve replacement (TMVR) and transcatheter tricuspid valve replacement (TTVR) systems. Furthermore, following the acquisition of Keystone Heart, Venus Medtech’s product portfolio is no longer confined to heart valves; its TriGUARD 3 cerebral embolic protection device has entered the FDA clinical trial phase. Upon successful completion, this device will further enhance the safety of cardiovascular procedures by reducing the risk of procedure-related brain injury.

Clinical Status of Venus Medtech’s Products

Regardless of the outcome of Venus Medtech’s latest IPO, the company has already established formidable barriers to entry. After reviewing extensive materials, VCBeat has summarized three major advantages of Venus Medtech, each of which places it far beyond the reach of latecomers.

Technical Advantages

Currently, the surgical approaches for TAVR primarily include transfemoral and transapical access. Due to its minimally invasive nature and technical maturity, the transfemoral approach is considered the first-line option, accounting for approximately 70% of procedures in China in 2017.

The transapical approach, as a secondary option, offers the advantages of a shorter access route and the ability to deliver larger surgical devices; however, it is associated with greater trauma (including to the heart itself) and a higher incidence of acute renal failure. Severe thoracic diseases and severely compromised cardiopulmonary function are contraindications.

Venus Medtech’s products utilize the transfemoral approach, which is minimally invasive and technically mature. Drawing from the development trajectory of mature markets such as the United States, this technology is poised to become the mainstream in China. Meanwhile, Venus Medtech is also developing transcatheter mitral valve repair, a safer but more surgically challenging procedure. Furthermore, the more cutting-edge transcatheter tricuspid valve replacement (TTVR) has been incorporated into Venus Medtech’s clinical trial design, underscoring the company’s determination to secure a leading position in technological innovation.

Currently, Venus Medtech holds a total of 379 patents and patent applications, including 81 granted patents and 70 patent applications in China. In major overseas markets such as the United States and the European Union, Venus Medtech has 96 granted patents and 132 patent applications.

Market Advantages

Due to variations in femoral artery diameter among different patients, market requirements for TAVR products differ across regions worldwide. Huatai Securities pointed out that, based on the characteristics of Chinese patients, TAVR devices demanded by the domestic market should possess the following features:

1. Focus on enhancing radial support force to address bicuspid valve issues and aortic valve calcification;

2. Better adjustment and adaptation to the irregular annulus caused by bicuspid valves;

3. Optimize the skirt design to reduce the incidence of paravalvular leak.

Compared with overseas companies, Venus Medtech’s products are specifically developed to address the characteristics of Chinese patients, who exhibit a higher prevalence of severe calcification and bicuspid aortic valves. By significantly enhancing radial force and the positioning system, complemented by a skirt design, these devices are better suited for the Chinese population and demonstrate clear differentiated advantages over imported products.

Compared with domestic competitors, Venus Medtech has significantly enhanced radial force and retrievability, while also introducing a pre-loaded feature. In addition to retaining the traditional advantages of Venus Medtech, VitaFlow’s design features a smaller catheter outer diameter, thereby reducing vascular complications. Peijia Medical’s product focuses on improving catheter crossability while maintaining its traditional strengths.

Technical Integrity and Overseas Layout

While heart valve consumables remain the core business of Venus Medtech, the company has not limited itself to this area but has instead set its sights on a more distant future.

In 2016, Venus Medtech embarked on its M&A journey by acquiring the entire portfolio of patented technologies from Germany’s Transcatheter Technologies GmbH. These newly acquired patented technologies will be applied to Venus Medtech’s third-generation TAVI products, providing new solutions for patients with structural heart and valvular diseases in China and worldwide, while also facilitating the overseas expansion of Venus Medtech’s valve products and accelerating its internationalization process.

In April 2017, Venus Medtech’s transcatheter aortic valve replacement (TAVR) system officially received approval from the China Food and Drug Administration (CFDA) and was launched on the market. Two subsequent mergers and acquisitions were particularly noteworthy. The first was the acquisition of InterValve on June 13, 2017, through which Venus Medtech fully acquired this U.S.-based supplier of balloon valvuloplasty products. The second was the acquisition of Keystone Heart on December 26, 2018, marking a strategic move by Venus Medtech to establish its presence in the European and American markets.

US-based InterValve is a company specializing in transcatheter aortic valve therapy. Its two products, V8 and TAV8, are the world’s first balloon aortic valvuloplasty catheters featuring anatomical morphology characteristics, both of which received FDA approval in 2013.

Venus Medtech’s CEO, Zhenjun Zi, stated following the acquisition: “The InterValve balloon is precisely matched to the annulus, ensuring stable balloon expansion and full expansion of the native leaflets without damaging the implanted valve. It conforms well to the anatomical structure, and when used in conjunction with self-expanding transcatheter aortic valves, it significantly reduces the incidence of paravalvular leakage. Meanwhile, it also reduces the need for rapid pacing and substantially lowers the risk of annular rupture.”

This means that Venus Medtech is not only focused on the research and innovation of transcatheter aortic valve products, but also places significant emphasis on the comprehensive management of TAVR procedures. The company strives to systematically and holistically mitigate the risks of cerebral and annular injury associated with TAVR, thereby ensuring and providing patients with a comprehensive and complete total solution.

In the acquisition of Keystone Heart, Venus Medtech acquired the TriGUARD 3 device—the world’s first and only cerebral embolic protection device designed to prevent cerebral embolism by covering the entire ascending aortic arch. This device minimizes the risk of brain injury during cardiovascular procedures, providing comprehensive protection for brain tissue.

The two acquisitions reflect Venus Medtech’s focus on the entire process of heart valve surgery, while also positioning the company for expansion into European and American markets. Zhenjun Zi has publicly expressed his determination to make Venus Medtech a global leader, and in practice, the tech company is continuously advancing toward this goal.

High-value medical consumables have long been a sector where China lags behind, but with recent policy support and talent influx, initial progress has been made in import substitution. In this context, Venus Medtech has spared no effort in continuously advancing its technological research and development.

Now, Venus Medtech is once again at a critical juncture for financing. To capture more market share and launch additional products, the company requires further capital injection. Stabilizing R&D, continuously introducing new products to seize market share, and ultimately achieving profitability has become an inevitable path for technology companies. This is precisely the original intention behind the establishment of the STAR Market, which has just begun trading.

Technological innovation is characterized by high investment, long cycles, and elevated risks. Indirect financing and short-term financing often prove inadequate in this regard; thus, technological innovation cannot proceed without the guidance and catalytic role of long-term capital. The capital market plays a crucial role in promoting the integration of technology and capital, as well as accelerating the formation and efficient circulation of innovation capital.

Therefore, we should perhaps place sufficient confidence in Venus Medtech. The power of Chinese technology is continuously advancing. In the near future, Venus Medtech will compete on a level playing field with Medtronic and Edwards Lifesciences. The competition between China and the United States will inevitably drive more rapid development in the heart valve sector, benefiting all stakeholders.

References:

1.http://www.sino-manager.com/11595.html

2.https://vcbeat.top/NmY3ODEwZWQ2ZmJmNTQ5YjI4OTY3ZTEzODNhZmJjMmU=

3.https://vcbeat.top/NjQ0OTBjMzRmOTIwMWJjZWUxZWIzZTZiMjllYWJhMWQ=

4.https://www.haodf.com/zhuanjiaguandian/mofeisite_5948611476.htm

5.http://app.jg.eastmoney.com/html_News/NewsShare.html?infoCode=NW201908061198628688&keywords=ÆôÃ÷Ò%C2%BDÁÆ&info=A19009.SH&buriedPoint=2