Chinese Pharma Goes Global: 24 Companies Showcase Six Blockbuster Candidates at J.P. Morgan Healthcare Conference

CHIATAI TIANQING

High-quality pharmaceuticals research, production, and sales provider

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Salubris

Pharmaceutical Product R&D Developer

Akeso

Innovative Antibody Drug Developer

Johnson & Johnson

Medical Device R&D and Manufacturer

Clarivate

A Medical Information Service Company

January 15,J.P. Morgan Healthcare Conference Enters Final Day: 24 Chinese Pharmaceutical Companies Showcase Strength with Major Deals, Impressive Pipeline Data, and FDA Approvals on the Horizon

This global top show of the "Chinese pharmaceutical corps" has become a dazzling highlight at this year's JPM Health Conference, sparking a frenzy in the A-share and Hong Kong stock markets.

Coincidentally, Clarivate recently released an in-depth report titled "Predictions of the Most Promising Drugs in 2026," which devoted significant coverage to the robust development of China's pharmaceutical market.

Behind this, China is continuously becoming a key strategic hub for the global pharmaceuticals industry, transitioning from a manufacturing center to an innovation powerhouse.

01

How Valuable Are the Star Innovative Drugs in China?

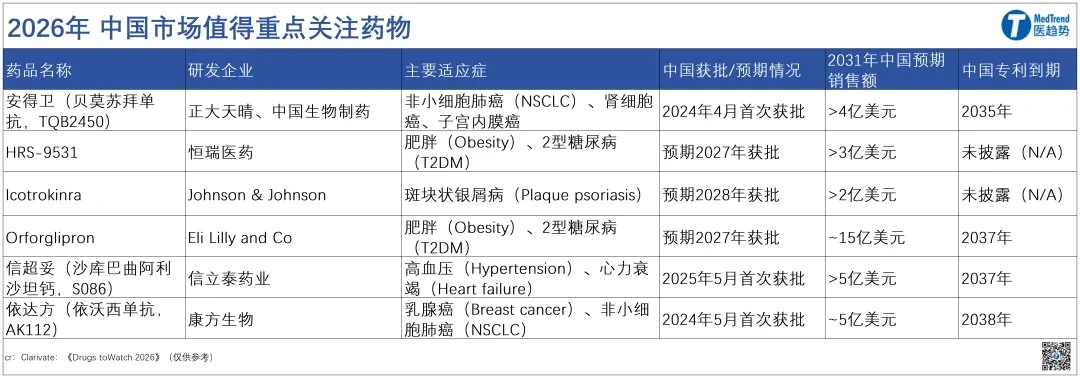

Clarivate report points out,Six Top Candidate Drugs in China's Market Worth Watching in 2026, Four from Local Chinese InnovatorsCHIATAI TIANQING, Hengrui Pharma, Salubris, and Akeso, indicating that their R&D capabilities can now rival multinational brands.

Why are these drugs worth attention? Clarivate provides scientific annotations through clinical data in the report and also draws the following predictions.

CHIATAI TIANQING - Andewei (Expected sales in China by 2031 > $4 billion):

With strong clinical efficacy, competitive pricing strategy, and clear differentiation advantages compared to durvalumab and sugemalimab, Andewei is expected to dominate the treatment market for unresectable stage III NSCLC in China.

Hengrui Pharma —— HRS-9531 (Expected sales in China by 2031 > $3 billion):

As China’s first domestically self-developed GIP/GLP-1 dual receptor agonist with the potential to gain approval, it will directly compete for market share with Mounjaro (tirzepatide, Eli Lilly) upon its launch.

Johnson & Johnson —— Icotrokinra (Expected sales in China by 2031 > $200 million):

Expected to become the world's first oral IL-23 receptor antagonist. More importantly, it may accelerate the transformation of oral therapies into first-line treatments for moderate to severe psoriasis, significantly improving patient access to treatment and potentially reshaping the clinical treatment landscape for moderate to severe psoriasis in China.

Lilly —— Orforglipron (Expected sales in China by 2031 ~$1.5 billion):

With its potent blood glucose control, clinically significant weight loss effects, and the advantage of convenient oral administration, it is not only expected to capture a significant share in China's rapidly growing T2DM and obesity markets but also greatly enhance treatment accessibility for a broader patient population.

Salubris——Xin Chao Tuo (Expected sales in China > $5 billion by 2031):

Although the drug’s initial indication is for hypertension, its potential to expand into heart failure with reduced ejection fraction (HFrEF) is significant, based on positive early clinical data and the substantial unmet medical needs in this area in China.

The core differentiation advantage lies in its ability to reduce serum uric acid levels, a feature that is particularly beneficial for heart failure patients with diuretic-associated hyperuricemia, filling a specific treatment gap for such patients.

Relying on local R&D background, anticipated price advantages, and greater potential to improve accessibility in rural areas, it is expected to achieve widespread clinical application in the future.

Akeso - Yida Fang (Expected sales in China by 2031 ~$5 billion):

By integrating immune checkpoint inhibition and anti-angiogenesis dual mechanisms in a single formulation, Edavarone has established a differentiated therapeutic advantage. It is expected to become a transformative treatment drug in the field of PD-L1 positive NSCLC and EGFR-TKI resistant non-squamous NSCLC, while also possessing the potential to expand into solid tumors such as triple-negative breast cancer.

In addition, the Clarivate report also lists other noteworthy pipelines under development in China, including:

GLP-1 Field:Another related drug from Hengrui Pharma and a GLP-1 dual-target drug under research by Huadong Medicine.

Multiple Sclerosis (MS):

NOCION Biopharma's BTK inhibitor orelabrutinib is currently conducting Phase III clinical trials in collaboration with Zenas BioPharma, targeting primary progressive multiple sclerosis (PP-MS) and non-relapsing secondary progressive multiple sclerosis (nrSP-MS).

Protein Degraders:

BeiGene's BGB-16673, a BTK-targeted chimeric degradation activating compound (CDAC), is aimed at relapsed/refractory chronic lymphocytic leukemia/small lymphocytic lymphoma (CLL/SLL). Relevant clinical trial data indicate potential efficacy against both BTK wild-type and mutant diseases.

Haisco Pharmaceutical recently obtained a patent for SMARCA2 degrader PROTACs, which has been reported to be applicable for lung cancer treatment.

Clarivate report points out,In the fields of PROTACs, molecular glue degraders (MGDs), and E3 ligase-related patents, China has ranked second globally.In the past decade, there have been a total of 717 related patents globally, with 265 filed by companies in mainland China (accounting for 37%), second only to the United States (319 patents, accounting for 44.5%).

Besides technological breakthroughs, China's vast and highly potential market has become fertile ground for the development of these innovative drugs.

With 690 million people being overweight or obese (nearly twice the population of the United States) and the continuous rise in cancer incidence, China presents immense commercial opportunities.

Over the past 20 years, the prevalence of overweight and obesity in mainland China has increased nearly threefold. As of 2022, approximately 34.8% of the population is overweight, and 14.1% meet the criteria for obesity (Chen et al., 2023). Among those who are overweight or obese, the prevalence rates of prediabetes, dyslipidemia, and hypertension are approximately 68%, 74%, and 58%, respectively.

The incidence of cancer continues to rise, with breast cancer being the second most common malignant tumor among women in China, having an incidence rate as high as 51.71 per 100,000 (Han et al, 2024).

Clarivate Report Concludes: China's Pharmaceutical Market is Experiencing a Significant Shift in Innovation Leadership. The Chinese market is transitioning from being historically dominated by generic drugs to developing therapies that can compete with, and even challenge, multinational brands, demonstrating that China is not only a manufacturing hub but also a key player in global pharmaceutical innovation.

This conclusion has evidently been corroborated at top global conferences, marking the entry of China's innovative drugs into the "home field era."

02

Why Are They on the Main Stage of JPM?

If the localized innovation achievements are considered the "internal cultivation" of Chinese pharmaceutical companies, then the 2026 J.P. Morgan Healthcare Conference showcased a "new posture" of China's innovative drug globalization.

In terms of participation methods,From being "listeners" and "visitors" to becoming more "speakers" and "leaders";

In terms of innovation quality,From "Selling Green Shoots" to "Source Innovation Cooperation," cutting-edge technologies such as bispecific antibodies, ADC, PROTAC have become the main force in overseas expansion, with clinical data aligned to global standards;

From the perspective of the cooperation pattern,From "Low Valuation" to "High Value": More Chinese Innovative Drugs Have Gained Global Pricing Power and a Voice.

As the world's largest and most influential healthcare investment and industry cooperation summit, the JPM Health Conference’s attendance and exhibition specifications directly reflect a company's standing in the global industry.

The main venue has always been the "competitive stage" for global pharmaceutical giants, and being able to secure a spot is itself an affirmation of a company's global competitiveness.

This year, the speaker list for the main venue features three WuXi-related CXO companies (WuXi AppTec, WuXi Biologics, WuXi XDC) and four leading innovative pharmaceutical companies (BeiGene, Zai Lab, Ascentage Pharma, Legend Biotech), becoming key negotiation targets for global capital and multinational pharmaceutical companies.

BeiGene, Zai Lab, and Legend Biotech have also delivered speeches at the main venue of the JPM Healthcare Conference for four consecutive years. Ascentage Pharma missed the speech last year due to its IPO.

BeiGene

Zanubrutinib Reaches the Global Summit, Aiming to "End Cancer"

At the conference, John Oyler, Co-Founder, Executive Chairman, and CEO of BeiGene (BeOne), led the core team in a high-profile appearance. Centering on the key topic of "Ending Cancer," they announced dual breakthroughs in financial profitability and pipeline development for 2025. They elaborated on the advantages of the leading drug in the CLL (Chronic Lymphocytic Leukemia) field and disclosed several critical milestone plans for 2026.

The current scale of the CLL track is 12-13 billion US dollars and is in a continuous growth trend.John Oyler stated that the core BTK inhibitor BRUKINSA (zanubrutinib) has topped the CLL market in the United States and globally, outperforming similar drugs.Data show that BRUKINSA outperformed the first-generation drug ibrutinib and the second-generation drug acala.

The Phase I data for BRUKINSA+Sonro (ZS combination) is highly promising, with the potential to fulfill the promise of a fixed treatment course; the innovative BTK-CDAC therapy for relapsed CLL has achieved an overall response rate of 86% and is currently undergoing a head-to-head Phase III trial.

BeiGene has a 4,800-member R&D team that has advanced 15 NMEs into clinical trials in the past 18 months, with plans to add 8-10 more annually in the future. The company has built its own clinical team to enhance efficiency, prioritizing the advancement of differentiated pipelines while establishing dual goals of "growth + margin improvement."

The CLL market continues to grow, with the ZS combination and BRUKINSA jointly expanding their market share. The ZS combination has tapped into the high-end market segment with fixed-duration treatment, while BRUKINSA continues to strengthen its leading position in the continuous treatment field.

John Oyler stated bluntly that 2025 will be a "turning point year" for BeiGene; in terms of finance, the company will fulfill last year's promise, achieving product revenue growth, GAAP profitability, and substantial cash flow.

The company has set a dual goal of "growth + profit margin improvement," relying on technological breakthroughs, efficiency enhancements, and economies of scale. In the long term, it aims to approach the profit margin levels of large pharmaceutical enterprises.

Currently, its hematology oncology asset Sonro has received the U.S. Breakthrough Therapy Designation, submitted four regulatory applications, and obtained the first global approval, while initiating five Phase III trials; in the solid tumor field, six assets have completed proof-of-concept, and five new molecules have entered clinical trial stages.

In 2026, BeiGene will reach key milestones such as the Phase III frontline MCL data and the global launch of Sonrotamab, continuously reshaping the landscape of cancer treatment and advancing towards the goal of "eradicating cancer."

Zai Lab

Dual-Driven Strategy Safeguards World's First ADC, Multiple Innovations Land in Quick Succession

Dr. Samantha Du, Founder, Chairperson and CEO of Zai Lab, clearly stated on-site that the company is entering a new phase driven by a "dual-engine" model of “China Commercialization Business + Global Innovation Engine." The company currently has eight commercialized products in China, forming a sustainable pipeline portfolio that lays a solid financial foundation for global R&D. Its cross-border integrated R&D platform efficiently transforms innovation, exemplified by Zoci’s rapid progression from the first-in-human trial to global pivotal clinical studies.

President and Chief Operating Officer Josh Smiley added that the differentiated pipeline in the Chinese market continued to contribute to steady growth, while the company's reputation as the "preferred partner" in the industry enabled it to continuously attract high-quality innovative achievements and efficiently advance the development of its global pipeline.

DLL3 ADC Product – Zoci Takes the Lead Globally, Three Pivotal Registration Studies to Kick Off Within the Year

As the core of the global pipeline, the progress of Zoci, a potential first-in-class/best-in-class drug, has become the focus. The conference disclosed that it plans to launch three pivotal registrational studies by the end of 2026.

Second-line/Third-line SCLC: Phase III registrational study has been initiated. Previous data showed an overall objective response rate of 68%, with a low incidence of grade 3 or higher adverse events at the 1.6 mg/kg dose, and no treatment-related discontinuations.

First-line SCLC: Phase I study of combined PD-L1 ± chemotherapy is ongoing, paving the way for a Phase III study by the end of the year; another Phase I study of a novel combination therapy initiated in the first half of the year.

Neuroendocrine Carcinoma (NEC): Phase I study ongoing, results to be announced in the first half of the year, pivotal clinical trial to be initiated in the second half.

In addition to Zoci, the timelines for the advancement of multiple globally innovative pipelines have been disclosed simultaneously:

ZL-6201 (LRRC15 ADC): The first novel ADC targeting tumor-associated fibroblasts, intended for use in sarcoma, breast cancer, etc., with global Phase I trials initiated in the first quarter.

ZL-1222 (PD-1xIL-12): A next-generation immunocytokine effective in both PD-1 sensitive and resistant models, with clinical trial applications to be completed this year.

ZL-1311 (MUC17xCD3): The first global rights TCE project, targeting gastrointestinal tumors such as gastric cancer, entering global clinical trials within the year;

ZL-1503 (IL-13xIL-31R): Dual-target therapy for atopic dermatitis, with first-in-human study data in healthy subjects to be released in the second half of the year.

Commercialization Further Expanded, Early Layout for Medical Insurance Access

In terms of regional business, it has been approved.TheKailiUpCommercialization to begin in half a year, focusing on physician education, real-world evidence, and paving the way for medical insurance access. In addition, potential market entries such as povetacicept and elegrobart (VRDN-003) will further enrich the pipeline and support regional growth.

2026 is defined as a "pivotal year" for Zai Lab.In addition to the pipeline progress, several important data readings and regulatory milestones will be achieved:

Global Phase III Data of Fgartigimod in Ocular Myasthenia Gravis and Myositis; Interim Analysis of Global Phase III Study of Povetacicept for IgA Nephropathy; Potential Approval in China for IVDAK (TF ADC) in Recurrent/Metastatic Cervical Cancer; NMPA Acceptance in China for TFields in Pancreatic Cancer. These milestones will continue to reduce R&D risks and accelerate value realization.

Zai Lab stated that it will continue to tackle unmet medical needs in the fields of oncology and immunology by relying on its globally integrated R&D platform, solid financials, and scaled operational capabilities, steadily advancing towards becoming a globally competitive biopharmaceutical company.

Legend Biotech

CARVYKTI Annual Sales Exceed 1.7 Billion, Aiming for Full Profitability by 2026

At the conference site, Dr. Ying Huang, CEO of Legend Biotech, made a significant appearance with the core product CARVYKTI. As the world's largest independent cell therapy company, Legend Biotech disclosed on-site the commercial achievements, pipeline progress, and 2026 strategic goals of its CAR-T therapy, aiming for an absolute leadership position in the multiple myeloma CAR-T field.

Flagship Product CARVYKTI (CAR-T Therapy for Multiple Myeloma) Shows Strong Growth Potential

Data shows that as of the end of the third quarter of 2025, CARVYKTI's net sales reached $1.7 billion in the past 12 months, with more than 10,000 patients treated cumulatively since its launch.

Clinical Data Continues to Lead:

In the CARTITUDE-1 study, one-third of heavily pretreated patients who had a median of 6.5 prior lines of therapy achieved 5 years of treatment-free remission after a single infusion, with a median progression-free survival (PFS) of 35 months; in the CARTITUDE-4 Phase III trial, the median PFS was not reached after nearly 3 years of follow-up in over 400 patients receiving 1–3 prior lines of therapy, with a median PFS of 50.4 months observed in third-line patients, setting a new efficacy benchmark.

Significant Advantages in Production and Accessibility:

Global manufacturing success rate of 97%, with a presence in 14 countries and 279 treatment sites; the expanded New Jersey manufacturing base in the United States becomes the world's largest cell therapy facility, combined with four global supply sites, offering an annual capacity to support treatments for 10,000 patients. A unique delayed cytokine release syndrome (CRS) profile allows nearly half of the usage scenarios to be outpatient treatments, promoting community outreach.

Huang Ying emphasized on-site that Legend Biotech is one of the few companies in the industry that possesses both commercial scale and a next-generation pipeline reserve. It is projected that by 2026, 75% of CARVYKTI's annual revenue will come from second- to fourth-line early treatment scenarios (currently accounting for 60%). Additionally, one-third of the 141 treatment sites in the U.S. are located in community settings (where 70% of relapsed/refractory multiple myeloma patients in the U.S. receive treatment). By 2026, the company plans to expand its community collaboration network with the goal of enabling all multiple myeloma patients in the U.S. to find a treatment site within 30 miles.

Currently, due to supply constraints and pricing reimbursement considerations, CARVYKTI has not been marketed in China. In the future, the focus will be on promoting more cost-effective off-the-shelf or in-vivo CAR-T therapies to meet local needs.

While consolidating CARVYKTI's leading position, Legend Biotech accelerates the layout of next-generation cell therapies, with 10 ongoing projects in the pipeline.

Pipeline Focuses on Three Core Directions:

① Hematological tumors and next-generation multiple myeloma therapies (including allogeneic and in vivo therapies);

② Solid tumors (such as the DLL3 autologous CAR-T project in collaboration with Novartis);

③ Autoimmune diseases (Phase I has been initiated, tapping into the unapproved CAR-T blue ocean). The company's R&D efficiency is remarkable, with an in vivo project taking only six months from candidate drug screening to first-in-human dosing.

The newly completed Philadelphia R&D center focuses on the development of in vivo CAR-T technology – which can reduce manufacturing complexity and expand accessibility. A Phase I clinical trial has been initiated, and relevant data will be disclosed in 2026.

The company currently has nearly 1 billion US dollars in cash and liquidity, and CARVYKTI achieved operational profitability in the third quarter of 2025; the gross profit margin remains stable at around 60%.Clearly Define the Goal of Achieving Company-Wide Profitability by 2026.

In addition,Hengrui Pharma, Baili Tianheng, 3SBio, RemeGen, and 17 other Chinese pharmaceutical companies made a collective appearance at the "Asia-Pacific Session" of the 2026 JPM Health Conference.Its business covers multiple fields such as innovative drugs, biologics, and medical devices. From established pharmaceutical companies to emerging unicorns, from ADCs, bispecific antibodies to AI-driven drug discovery, the diversified corporate matrix and technological layout highlight the ecosystem of China's pharmaceutical industry, characterized by "full-chain innovation and multi-level globalization."

References:

Clarivate:《Drugs toWatch 2026》