Billions in Capital Flow into Health Insurance: Has Innovative Payment Broken Through?

Jianyibao

Comprehensive Medical Service Platform

RHC

Private Equity Fund Management Institution

Four years ago, at a café in Zhongguancun, Beijing, Chen Penghui, a partner at Sequoia Capital China, delivered a presentation at a healthcare industry forum. He stated, “The healthcare sector is arguably one of the few industries most resistant to transformation by the internet. Precisely because it is so difficult to disrupt, there remain many pain points that are not easily addressed or monetized. This also means that opportunities exist across various healthcare subsectors.”

Among the subsectors of the healthcare industry in 2019, the biggest surprise undoubtedly came from health insurance. Health insurance represents an innovative solution to the current challenges in healthcare payment. From RMB 3.654 billion in 1999 to RMB 544.813 billion in 2018, the market size of health insurance grew 149-fold over two decades. In the past five years, the compound annual growth rate (CAGR) of health insurance reached 35.95%, and it is projected to surpass the trillion-yuan mark by 2021.

Selected Health Insurance Companies That Raised Funding in 2019

In this market, not only are more than a hundred insurance companies participating and thousands of health insurance products being launched, but internet giants such as Tencent and Alibaba have also entered the fray. Investment institutions have been exceptionally active; on July 8 this year, alone on the VCBeat platform, three companies announced on the same day that they had secured financing ranging from tens of millions to hundreds of millions of yuan. Prominent investors included Sequoia Capital and BV Baidu Venture Capital.

“There is no doubt that China’s healthcare payment system will evolve toward diversification; meanwhile, there is immense potential for both basic medical insurance and commercial health insurance to leverage technology-driven cost containment and efficiency improvements. The trends in this sector are clear, making it highly promising,” said Huang Shengxuan, Managing Director of RHC, in an interview with VCBeat. RHC (Sunshine Ronghui Capital) is the investment arm of Sunshine Insurance Group and stands as one of the active investors focusing on the innovative payment sector. In recent years, the Sunshine Insurance system has invested in healthcare technology companies such as Miao Health.

For a long time, the healthcare industry has been plagued by numerous dilemmas and pain points. This year, however, health insurance has begun to break through in the emerging field of innovative payment solutions, serving as a catalyst that carries the hope of transforming the entire industry.

To this day, the challenges of “difficulty in accessing medical care and high healthcare costs” still loom large before the public. This stereotype, primarily held by patients, creates a palpable perception that falling ill inevitably entails substantial consumption of both time and money.

According to data disclosed by China’s National Health and Family Planning Commission, 48.8% of patients seeking medical care chose tertiary hospitals, even though these institutions accounted for only 12.5% of all hospitals in the country. Consequently, the workload of physicians in tertiary hospitals is far higher than the national average, which inevitably prolongs patient waiting times and shortens the duration of each consultation, giving rise to the widely recognized phenomenon of “difficulty in accessing medical care.”

Policies such as “tiered diagnosis and treatment” and “first-contact care at primary healthcare institutions,” which are being promoted by the state, aim to address the difficulty of accessing medical services. Meanwhile, the widespread adoption of basic medical insurance has significantly alleviated the burden of high healthcare costs. However, a new challenge has emerged: the national healthcare system is struggling to sustain affordability. According to a report jointly released by Huazhong University of Science and Technology and People’s Publishing House in 2014, the basic medical insurance fund is projected to face a severe deficit, with an accumulated shortfall of RMB 735.3 billion by 2024.

Thus, improving the efficiency of medical insurance fund expenditures and implementing cost-containment measures have become the focus of the government’s healthcare reforms in recent years. Against this backdrop, the continued emphasis on developing commercial health insurance to serve as a supplement to basic medical coverage appears to be an effective solution to the current payment dilemmas.

Moreover, in addition to alleviating pressure on the social medical security system, health insurance can also resolve supply-side contradictions. With rising personal health expenditures, an aging population, accelerated urbanization, a growing middle-income group, and an expanding population with chronic diseases, the current capacity of social security provision is far from meeting the people’s rapidly growing demand for health protection.

Driven by multiple factors, residents are increasingly conscious of controlling their medical expenses, leading to surging market demand for health insurance. “Demand for health insurance remains robust in the market. From the perspectives of the current external macroeconomic environment, regulatory guidance within the industry, and the strategic development goals of leading life insurers, the demand for protection-oriented insurance products, represented by health insurance, will be effectively stimulated in the future. Premiums for health insurance are expected to maintain a growth rate exceeding that of the industry as a whole,” said Liu Xinqi, an analyst at Guotai Junan Securities, in an interview.

The revolutionary explosion in the health insurance market is attributable to the entry of internet giants with massive user traffic. As of July 2019, Ant Financial’s “Xianghubao” reported that its user base had surpassed 80 million, just 10 months after its launch. Shuidi Huzhu, a well-established online mutual aid platform founded in 2016, also boasted more than 80 million users.

In addition, more tech giants such as Didi, JD.com, Meituan, and 360 are either entering or have already entered the market. For these giants’ online mutual aid businesses, the primary consideration lies in acquiring traffic and usage scenarios. Taking Waterdrop Inc.’s model as an example, Shuidichou (Waterdrop Crowdfunding) leverages social connections to educate users on fundraising for critical illnesses; Shuidi Huzhu (Waterdrop Mutual Aid) then serves those users within the fundraising pool who seek protection coverage; a significant portion of these mutual aid participants subsequently convert into customers of Shuidibao (Waterdrop Insurance), purchasing insurance products. This three-tier funnel model employed by Waterdrop effectively creates a closed-loop ecosystem.

It is foreseeable that online mutual aid will become the breakthrough point for major tech giants to enter the trillion-yuan health insurance market, and even the broader big health sector.

The Dilemma of Payment Undoubtedly Means Opportunities for Enterprises.

Policyholders eliminate economic uncertainty by paying premiums in advance in exchange for loss compensation when risks materialize in the future; insurers aggregate the needs of the insured, transform dispersed risks into approximate certainty, and realize commercial value. This is the essence of insurance.

Health insurance is no exception. As a supplementary safeguard to basic medical insurance, commercial health insurance in China has advanced alongside the reform and development of social medical insurance, entering a period of rapid growth. Its evolution can be broadly divided into three developmental stages.

From the restoration of commercial insurance in 1980 to the promulgation of China’s first Insurance Law in 1995 and the subsequent launch of basic medical insurance reform for urban employees the following year, marked the nascent stage of health insurance development in China. During this period, reforms to the public healthcare financing system created opportunities for the growth of health insurance. In 2003, amendments to the Insurance Law permitted property insurance companies to underwrite short-term health insurance products. Two years later, PICC Health, the country’s first specialized health insurance company, was established. By 2009, with the initiation of the new healthcare reform, the supplementary role of commercial insurance was explicitly affirmed. This phase represented a period of expanded promotion, characterized by the accelerated introduction of health insurance products and regulatory frameworks.

Since 2012, health insurance has entered its third phase, ushering in a period of explosive growth. In the subsequent years, the annual premium growth rate for health insurance remained above 40%. Health insurance seemed to have embarked on a vigorous sprint; however, amidst this rapid development, numerous issues began to emerge. The prevalence of short-to-medium duration products, the frequent emergence of dark horses, significant adjustments in market structure, and capital giants sweeping through the secondary market... Insurance appeared to be drifting further and further away from its fundamental essence of protection.

During this period, some products with short to medium durations were also labeled as “health insurance” and included in health insurance premiums. For example, in 2016, Hexie Health Insurance alone reported premium income as high as RMB 107 billion, accounting for 26.5% of the total health insurance premium scale, most of which was actually “policyholder deposits and investment accounts.”

The turning point came in 2017, when regulatory authorities began to exert control. The issuance of “Document No. 134” by the China Insurance Regulatory Commission (CIRC) promptly cooled the previously rampant growth in the insurance sector. The document emphasized that insurance should “return to its fundamental roots” and signaled a strict regulatory stance, including severe penalties for companies or individuals violating regulations. That year, the growth rate of health insurance premiums dropped to 8.58%.

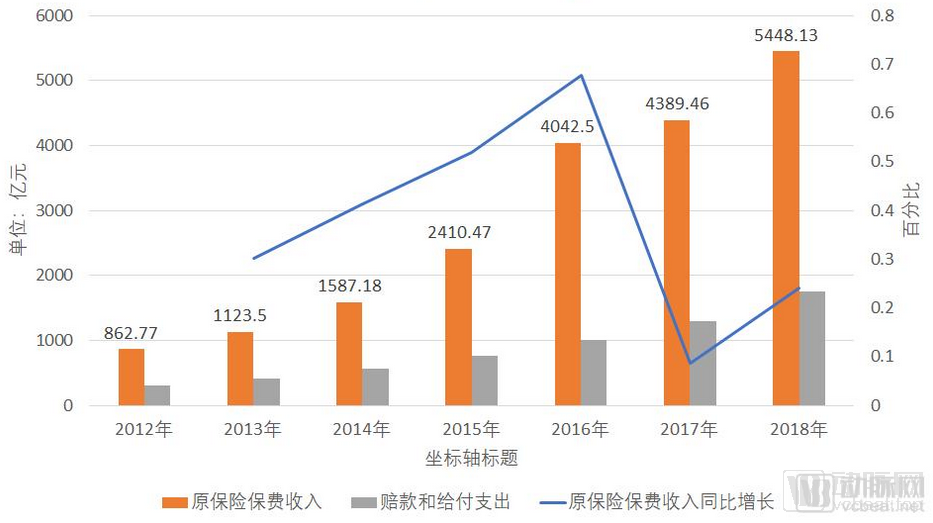

Since 2018, empowered by technological advancements and policy changes, the health insurance sector has resumed rapid growth in a relatively rational manner. According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the original premium income from health insurance business reached RMB 544.813 billion in 2018, a year-on-year increase of 24.12%. Claims and benefits paid out in the health insurance business amounted to RMB 174.434 billion, representing a year-on-year increase of 34.72%.

Macro Data of the Health Insurance Market in Recent Years

China’s current economic and social structure underpins immense market potential for health insurance, while consistently favorable policies make its rapid growth virtually inevitable. Professor Zhu Minglai of the School of Finance at Nankai University predicts that “by 2020, the commercial health insurance market will reach approximately RMB 800 billion, and by 2021 at the latest, health insurance premiums will surpass those of auto insurance, making it the second-largest insurance segment.”

Based on the information revealed during this year’s Two Sessions, the Government Work Report explicitly calls for “enhancing the risk protection function of the insurance industry.” As one of the insurance products with the strongest protection attributes, health insurance still holds significant potential for future growth. Peng Xuan, Co-CEO of Yuanxin Huibao, stated in an interview with VCBeat: “In recent years, policies have consistently encouraged the development of health insurance, and the policy trend is quite favorable. The health insurance market is just getting started, and it will undoubtedly accelerate and achieve rapid growth in the future.”

Although the health insurance market exhibits clear blue-ocean characteristics, the industry’s development still faces numerous bottlenecks that need to be overcome.

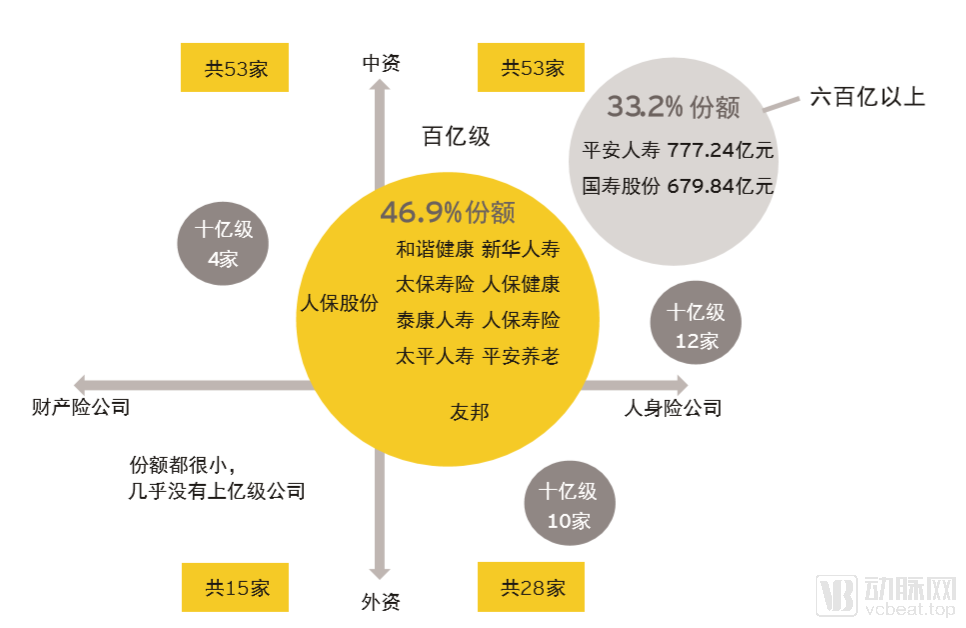

China's health insurance market is highly concentrated, with 80% of revenues accounted for by the top 8% of companies. The primary participants are life and property & casualty insurers, while specialized health insurers remain limited in both scale and number.

Market Concentration of Health Insurance Operators (Source: EY Report)

However, as an increasing number of players enter the health insurance market, the competitive landscape is shifting toward diversification, expanding from traditional insurers alone to include internet companies, healthcare institutions, pharmaceutical groups, health management organizations, medical big data firms, and entities from other real-economy sectors.

Severe product homogenization is also a major bottleneck. Disease insurance and medical insurance dominate the market, while long-term care insurance and disability insurance account for a relatively low share of premiums. Commercial health insurance plays a limited role in supplementing basic medical insurance, and the actual claims paid by health insurers as a proportion of China’s total health expenditure lag far behind those in countries with mature insurance markets. There is little differentiation among commercial health insurance products offered by various insurers, and many are sold in bundles as riders to life insurance policies.

“The traditional insurance market is a red ocean, with severe product homogenization; price competition is often the go-to marketing strategy for companies,” said Zhang Shengming, founder of Jianyibao, in an interview with VCBeat. Prior to founding Jianyibao, he worked in the insurance industry for many years.

From the perspective of sales channels, health insurance distribution can be categorized into online and offline segments. Traditional channels are dominated by individual agents, with health insurance policies sold through insurance agents accounting for more than 60% of the market, indicating that strong offline channels hold the majority market share. However, it is evident that online channels, leveraging their massive traffic, are redefining the sales model for health insurance. “As incomes rise and the user base becomes younger, an increasing number of people will purchase insurance via the internet,” said Peng Xuan, Co-CEO of Yuanxin Huibao.

Regarding health insurance, another issue is that the general public has long had a limited understanding of the insurance industry, often harboring negative sentiments. “People tend to believe that insurance sales agents lack overall professionalism and expertise, with the perception that anyone can sell insurance,” said Zhang Huan (a pseudonym), Chief Life Insurance Planner at MetLife, in an interview with VCBeat. She noted that in today’s society, many people still view insurance as fraudulent.

According to data disclosed in the "2018 China Commercial Health Insurance Development Index Report," the current coverage rate of commercial health insurance is less than 10%. It is easy to imagine the substantial market potential that will be unlocked by heightened insurance awareness.

From the perspective of the industry chain, health insurance operations involve multiple segments: “medical care, pharmaceuticals, insurance, and wellness.” Customers receive financial compensation for health-related expenses directly or indirectly from payers; obtain diagnostic, therapeutic, and prescription dispensing services from healthcare providers; and access full-cycle health management services and health incentives from wellness service providers. Payers and service providers achieve integration through shared customer bases, data interoperability, and system connectivity. Nevertheless, numerous pain points persist across these segments.

Amidst the profit-driven nature of capital and the booming development of technologies such as big data and artificial intelligence, health insurance has become a highly sought-after growth frontier.

Amid the current boom, as in all other industries, the internet has begun to disrupt every node of the health insurance value chain, signaling that the industry is on the eve of profound transformation.

On July 8, one month ago, Yuanxin Huibao, Nuohui Medical, and Zhanlue Data simultaneously announced their financing news on the VCBeat platform. Yuanxin Huibao secured RMB 50 million in Series A funding, led by Sequoia Capital, to provide insurers with solutions for actuarial product pricing, risk control, and user acquisition. In an interview with VCBeat, Peng Xuan stated that future health insurance will transcend traditional coverage, evolving toward health management and comprehensive health services.

Nohui Medical, established in November last year, secured a Series B financing round led by Legend Star. The company provides health insurance and payment solutions for major diseases, covering medication reimbursement, efficacy guarantees, and medication security. Zhanlue Data raised nearly RMB 100 million in its Series B financing, led by Lingfeng Capital, to provide enterprise-level big data risk control solutions for insurance companies and intermediaries.

The fact that these three companies secured financing on the same day is no mere coincidence; capital has been highly active in the health insurance market over the past year. Capital is undoubtedly the most sensitive barometer of market trends, and what lies ahead for health insurance is clearly a trillion-yuan blue ocean.

“The outlook for this sector is relatively clear, with the landscape currently dominated by early- to mid-stage companies. The industry is poised for imminent breakthroughs driven by technology and data. Given the substantial market size and well-defined demand, we believe that multiple scaled enterprises will emerge within the next two to three years,” said Huang Shengxuan, Managing Director at RHC, in an interview with VCBeat. As an investor, he is particularly optimistic about solution integrators capable of connecting customers, data, payment systems, and supply chains, as well as companies that provide incremental empowerment to commercial insurers and social security programs.

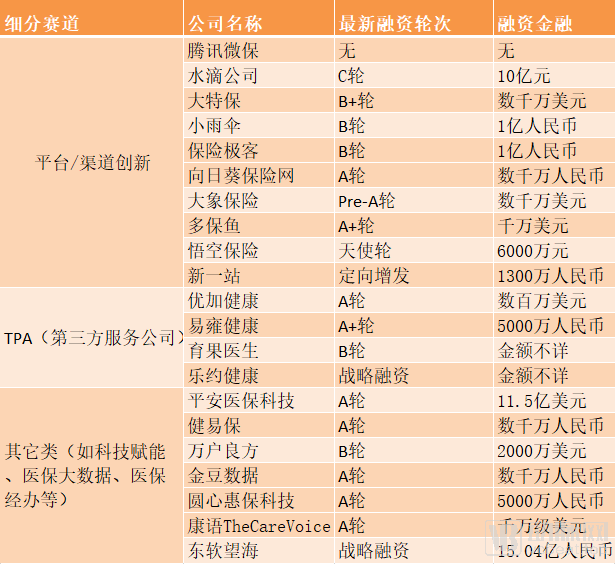

Across various stages and segments of the health insurance sector, a large number of innovative companies have already emerged.

List of Selected Companies in Various Sub-sectors of the Innovative Payment Field

Taking channel innovation as an example, companies that leverage information technology to provide online insurance knowledge, product comparisons, product screening, purchasing, and services have attracted significant investment. Notable examples include Da Te Bao and Insurance Geek, both of which have secured over RMB 100 million in financing. As shown in the table above, platform-based enterprises are a type favored by capital markets and often command higher valuations. Internet giants entering the health insurance sector also tend to focus primarily on this track of channel innovation.

In November 2017, Tencent launched WeSure, an insurance agency offering products such as medical insurance, critical illness insurance, and long-term critical illness insurance for children. Additionally, Tencent has participated in four consecutive funding rounds of Waterdrop Company, starting from the angel round.

Ant Financial has established the “Ant Insurance” section within Alipay, offering insurance products across multiple major categories, including health, accident, travel, property, and life insurance. Product providers include PICC Health, ZhongAn Insurance, Ping An Insurance, Guohua Life, and Taikang Online, among others. Additionally, Trust Mutual Life Insurance Society partnered with Alipay to launch the mutual aid insurance product “Xianghubao” (initially named “Xianghubao,” later renamed “Xianghubao”) in October 2018. As of now, the number of users has exceeded 80 million.

Notably, marked by the launch of “Xianghubao,” internet giants began to enter the market in full force, piloting online mutual aid services. In November 2018, JD.com launched “JD Mutual Aid”; in December, Didi Chuxing rolled out “Didi Mutual Aid”; in May 2019, Suning introduced “Ning Hubao”; in June 2019, Qihoo 360 released “360 Mutual Aid”; and on July 11, 2019, Meituan launched “Meituan Mutual Aid.”

Online mutual aid is currently the most critical scenario for health insurance. Once established, this model enables precise outreach to and education of potential insurance customers, generating a steady stream of leads for subsequent commercial insurance operations. It is foreseeable that channel innovation will become the most fiercely contested segment within the various sub-sectors of the health insurance industry.

Health insurance third-party service providers are generally referred to as TPAs,Our services include providing new policy issuance and policy administration services, claims processing, building medical service networks, and arranging medical expense settlement services. In the TPA sector, innovative enterprises can help traditional commercial insurance companies address pain points, such as establishingHigh-quality medical service networks, effective control and intervention of medical costs, establishment ofRapid claims settlement and direct reimbursement systems, health management, etc.

Take Youjia Health, a player in this sector, for example; it providesTwo Solutions for the Insurance and Healthcare Sectors. On the insurance side, we assist insurance companies in integrating medical resources, curating preferred provider networks, and building an integrated empowerment platform based on the S2B (Supplier-to-Business) model through internet technologies. On the healthcare side, we establish a value-based healthcare service evaluation system and collaborate with hospitals to build a preferred direct-billing network. When Youjia customers require hospitalization due to illness, Youjia Health provides guarantees to the preferred hospitals, enabling customers to enjoy the convenience of direct settlement for inpatient medical expenses.

In the arena of technology empowerment, data-driven approaches will be a key direction for future development. Taking Ping An Health Insurance Technology and Neusoft Wanghai as examples, Ping An Health Insurance Technology has currentlyHaving provided medical insurance and commercial insurance management services to over 200 cities and a population of 800 million, the accumulation of big data will further empower its business operations;while Neusoft WanghaiStriving to maintain a leading position in the field of lean information data services for hospitals.

In other sectors, companies such as Jianyibao, which pioneered insurance sales and services for individuals with pre-existing conditions, and Wanhuliangfang, which specializes in pharmacy benefit management, have each secured financing exceeding tens of millions of yuan, validating their business models.

Through interviews with multiple stakeholders, VCBeat has learned that providing solutions centered around payers will be a major direction for market development, with opportunities available at every node of the industry chain.

Another trend is that the influx of leading internet companies has sparked greater imagination for the future of health insurance. Educating the market, acquiring traffic, monetizing traffic, subsidizing users, transforming the supply chain... numerous disruptors appear to have already entered the arena.

In 1989, amid the AIDS epidemic in the United States, the American writer Susan Sontag wrote in her book *AIDS and Its Metaphors*: “Health becomes proof of virtue, just as disease becomes evidence of depravity.”

Nowadays, in China’s vast tier-two to tier-five markets, many people have little understanding of insurance, and some may even immediately harbor the perception that it is “a scam.”

Perhaps, as public awareness of insurance grows, the health insurance market will unlock even greater potential.

References:

1.Today’s Bao, Trillion-Dollar Health Insurance: Whose Cake, Whose Trap? https://www.iyiou.com/p/106484.html

2.Ernst & Young, "White Paper on Commercial Health Insurance in China"