Market Restructuring and Investment Opportunities in China's Healthcare, Pharmaceutical, and Medical Device Sectors

Driven by factors such as population growth, rising household incomes, and an aging demographic, domestic demand for healthcare services is steadily increasing. The healthcare market has undergone profound transformations, with accelerating innovation in business models and deeper industry integration.

1.1 The overall market size will continue to grow steadily

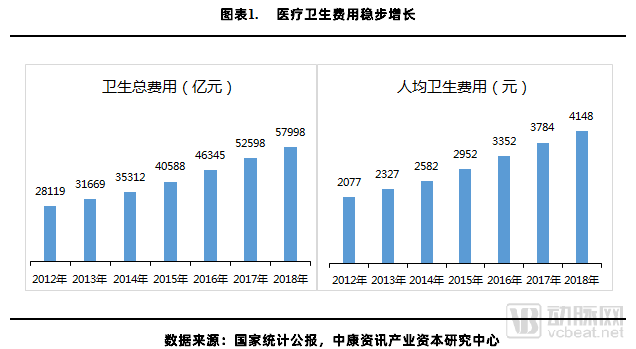

In recent years, the healthcare market has become increasingly hot. It is estimated that by 2020, the market size of China's health industry will reach 10 trillion yuan, making it a new focal point for investment. Over the next decade, the healthcare market is expected to maintain steady growth. From the perspective of supply and demand, on one hand, with the further intensification of population aging and the steady increase in per capita disposable income, the demand for health has been fully unleashed; on the other hand, advancements in pharmaceutical technology, biotechnology, and intelligent technologies have significantly improved the products and services provided by the health industry, thereby meeting more health needs.

1.2 Compression of Cost Bubbles and Slowing Market Growth

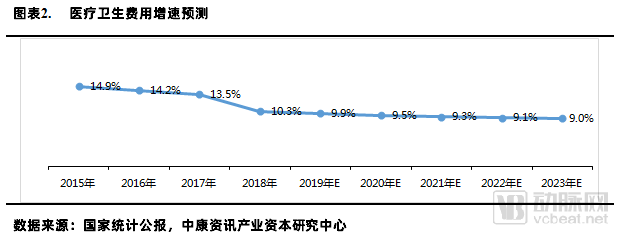

As cost-containment policies advance, the bubble in the healthcare market will be compressed, making sustained high-speed growth untenable and leading to a gradual decline in growth rates.

Currently, there are three main influencing factors:

First, healthcare insurance cost-containment policies, including volume-based procurement and Diagnosis-Related Groups (DRGs), along with the gradual advancement of payment reforms and the separation of prescribing from dispensing, have yielded significant reductions in costs.

Second, public hospital reform policies: new performance assessment mechanisms are driving the implementation of healthcare reforms, with extensive substitution of originator drugs by generics, along with measures such as zero markup and drug proportion assessments, to reduce losses in medical insurance funds.

Third, the implementation of health management strategies, driven by the deepening adoption of the concept that "prevention is better than cure," will yield substantial savings in future healthcare costs.

1.3 Industry Upgrade Imminent, Giving Rise to New Opportunities

With the rapid improvement in people’s living standards, a new wave of consumption upgrading is poised to take off. After pursuing material upgrades, the new middle class has begun to adopt a more rational approach to consumption, prioritizing personal experiences and willingness to pay for premium quality and high-quality services. Meanwhile, the massive health industry, valued at trillions of yuan, has attracted fierce competition from private capital.

Driven by the dual forces of consumption upgrading among the new middle class and the influx of private capital, the upgrade and transformation of China’s healthcare industry has become an established trend. In the future, the industry will shift from being price-driven and marketing-driven to being quality-driven, cost-driven, and efficacy-driven.

The Upgrading of the Healthcare Industry Will Bring New Opportunities to Commercial InsuranceIn the past three years, the growth rate of medical insurance expenditures has surpassed that of revenues. As the largest payer, the basic medical insurance fund is under significant pressure and may struggle to support the consumption upgrade demands of the middle class in the future. Consequently, commercial insurance, serving as a valuable supplement to basic medical insurance, is poised for new development opportunities.

In recent years, the premium scale of health insurance in China has grown rapidly: In 2010, health insurance premiums in China were only RMB 67.747 billion, rising to RMB 544.813 billion by 2018, accounting for 14.33% of the total premium income of China’s insurance industry. The year-on-year growth reached 24.12%, making it the fastest-growing insurance category, with a growth rate 6.15 times that of the overall industry’s premium income growth.

2.1 Slow Growth in the Pharmaceutical Market May Become the New Normal

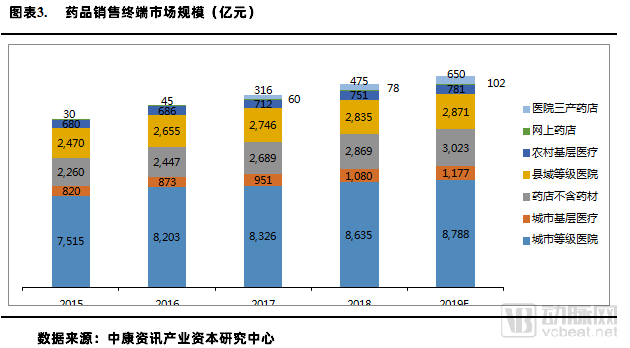

Affected by healthcare reform policies aimed at cost control and price reductions, the growth rate of China’s pharmaceutical terminal market has declined year over year for the past three years, with the 2019 growth rate projected to drop to 4%. Among these, urban tiered hospitals and county-level tiered hospitals have been significantly impacted by the healthcare reform policies, with their growth rates expected to be only 1.8% and 1.3%, respectively.

The projected growth rate for over-the-counter (OTC) drugs is 4.4%. Compared with 2018, only the rural primary-care and urban primary-care terminal markets maintained an upward trend among all major terminals. The projected growth rate for prescription drugs is 2.7%, with growth rates declining across all major terminals compared with 2018.

However, driven by population aging, consumption upgrading, and supply-side structural reforms, the market size will continue to grow.

2.2 Innovative Drugs: The Primary Driver of Industry Growth

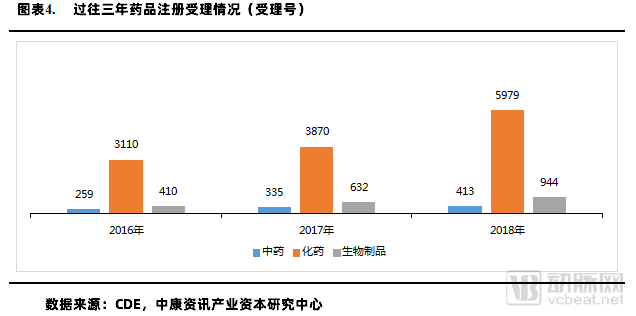

In recent years, innovative drugs have received strong policy support, exhibiting a trend of "accelerated review, rapid market launch, and swift volume growth." In the future, innovative drugs will become the primary driver of market growth. In 2018, the Center for Drug Evaluation (CDE) accepted registration applications for 264 Class 1 innovative drug varieties, representing a 21% increase compared to 2017.

Among these, 239 investigational new drug (IND) applications for Class 1 innovative drugs were accepted, representing a 15% increase compared with 2017; 25 new drug applications (NDA) for Class 1 innovative drugs were accepted, representing a 150% increase compared with 2017.

From a segmented perspective, the biological products sector saw its growth rate reach 3.0% in 2019, an improvement over 2018, driven by sustained rapid growth in the vaccine and growth hormone industries and a recovery in the blood products industry.

Innovative R&D is focused on oncology, with biopharmaceuticals as a key area of emphasis. Investment should prioritize innovative products with well-defined targets and molecular biomarkers.

2.3 Generic Drugs: The Era of Thin Margins Is Gradually Arriving

Initiatives such as the “4+7” volume-based procurement, generic drug consistency evaluation, and the introduction of imported generics have significantly impacted drug prices and pharmaceutical companies’ profits. As healthcare reform deepens, the scope of coordination linked to the “4+7” program will continue to expand.

In recent years, healthcare reforms have sought to control the prices of generic drugs, thereby creating space for innovative medicines. Measures such as substituting originator drugs with generics, curbing inflated generic drug prices, and allowing imported generics to participate in tendering competitions can structurally reduce drug costs. Historically, generic drugs enjoyed high gross profit margins and prices; however, under the influence of healthcare reforms, both the gross profit margins and prices of generics are expected to decline significantly, returning to rational levels.

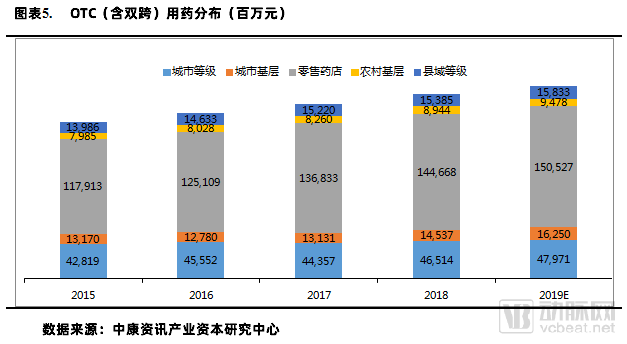

2.4 OTC: The market is concentrated among leading enterprises, with high barriers to entry for new players.

With price increases for over-the-counter (OTC) drugs and the deepening public awareness of health management, the OTC drug market has experienced steady growth, maintaining a growth rate of approximately 4.4%. In recent years, the OTC drug market has exhibited the following characteristics:

a. Retail pharmacies are the largest sales channel for OTC products, accounting for over 60%.

b. The brand effect of leading market players is significant. Compared with prescription drugs, consumers exhibit a higher reliance on brands and reputation. Several major domestic over-the-counter (OTC) drug brands are expected to maintain substantial market shares for the long term, resulting in high barriers to entry for new competitors.

c. Health-oriented products are developing faster than therapeutic ones. As the public’s awareness and capability in health management grow, health-oriented and preventive products will gain opportunities for growth.

2.5 The growth rate of the pharmaceutical chain market continues to decline

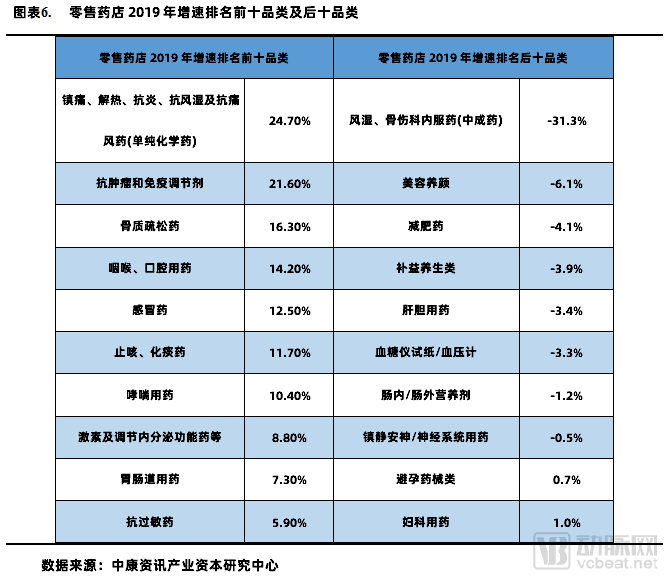

As the second-largest terminal in the pharmaceutical industry, pharmaceutical retail has experienced a continuous decline in growth rate in recent years due to the impact of healthcare reforms, with the growth rate expected to be only 4.5% in 2019. Among them, the drug market grew by 5.4%, while non-drug products grew by 0.3%; prescription drugs increased by 6.8%, and over-the-counter (OTC) drugs by 4%. From the perspective of category growth rates, several high-volume functional categories, such as analgesics, antipyretics, anti-inflammatory, antirheumatic, and antigout medications, as well as antineoplastic agents and immunomodulators, all saw growth rates exceeding 20%. In contrast, beauty-enhancing and health-promoting products have gradually declined.

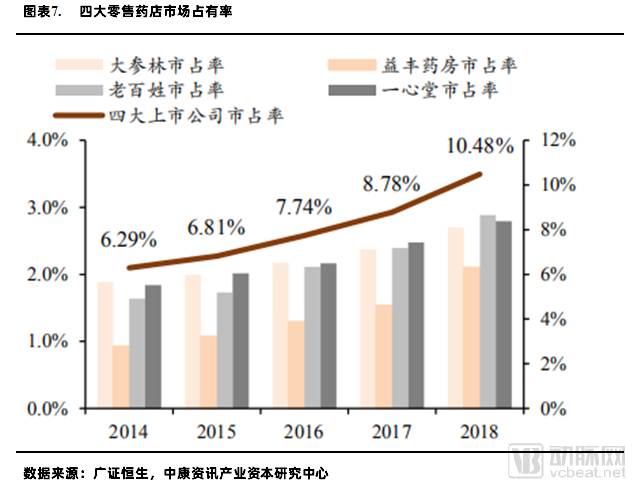

2.6 Industry Concentration Continues to Rise, with Clear Advantages for Leading Players

During the implementation of the new healthcare reforms, industry policies were issued intensively, significantly altering the competitive landscape of the pharmaceutical retail sector and markedly increasing industry concentration. The outflow of prescriptions has greatly promoted the separation of prescribing from dispensing, with leading enterprises demonstrating clear advantages in capturing this demand. Volume-based procurement, while reducing drug prices, has also spurred the development of out-of-hospital channels; consequently, pharmacy profit margins are expected to gradually decline, driving a greater need for scale expansion. Measures such as the classified and graded management of pharmacies, the crackdown on the illegal leasing of pharmacist licenses, and efforts to combat insurance fraud will further increase industry concentration and progressively standardize the operations of chain pharmacies.

Capital-driven growth is another critical factor, with capital inflows accelerating consolidation in the pharmaceutical retail market. In the early stages, driven by capital, most publicly listed pharmacy companies were willing to acquire high-quality assets and stores in strategically important regions at premium prices to accelerate expansion, leading to a sharp rise in the valuations of retail pharmacies. After 2018, as the market gradually cooled, the focus of numerous acquisitions shifted toward operational integration, with buyers in the primary market consisting mainly of large pharmacy chains. Among the top four pharmacy chains, Laobaixing and Yifeng demonstrated outstanding expansion capabilities, while Yixintang and Dashenlin exhibited significant regional advantages.

2.7 Integrating Online and Offline Channels to Unlock New Opportunities

To date, brick-and-mortar pharmacies remain the more robust channel for customer traffic, with their professional services and prescription fulfillment constituting irreplaceable scenarios. As a supplementary channel, online pharmacies will coexist and develop alongside physical stores in the future. Currently, the market share of online pharmaceutical retail is minimal—less than 1%—and does not pose a significant threat to brick-and-mortar pharmacies. However, sales volume through online channels is growing rapidly, driven by the integration and penetration of internet technologies, which have enhanced efficiency and extended the service radius.

In the future, with the emergence of new business models such as O2O “online order, in-store pickup” and “online order, store delivery,” the synergistic development of offline and online pharmaceutical retail is expected to unlock new growth potential in the out-of-hospital retail market. The growth potential of online pharmacies depends on their ability to fulfill prescriptions from physical hospitals and the maturity of internet-based medical institutions; therefore, internet technology and telemedicine services will become key directions for the upgrading of pharmaceutical retail.

2.8 Investment Opportunities in the Pharmaceutical Market

Although the growth rate of the pharmaceutical market has slowed, significant investment opportunities remain, focusing on:

Innovative pharmaceutical or CRO companies with strong capital operation capabilities, mature teams, and broad R&D pipelines

A generic pharmaceutical company with strong cost control capabilities and integrated API and formulation operations

Established OTC brands with proven efficacy, strong direct-to-consumer (DTC) operational capabilities, and high consumer recognition

Leading Chain Retail Pharmacies with Strong Expansion Capabilities, Digital Technology Capabilities, and Professional Service Capabilities

3.1 Rapid Market Growth with Promising Future Potential

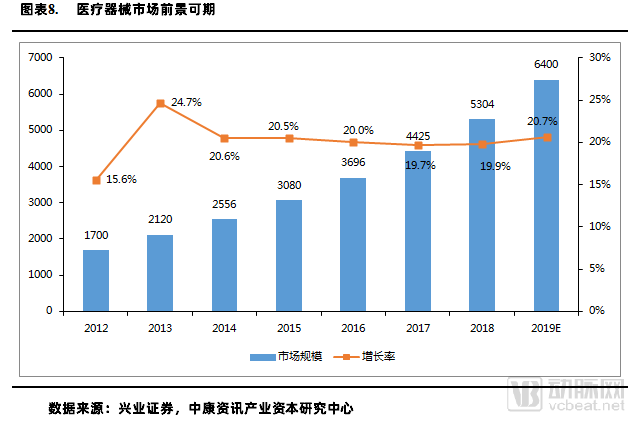

In recent years, continuous technological advancements by Chinese medical device enterprises have driven the maturation of the supporting supply chain. Meanwhile, propelled by national policies such as healthcare reform, tiered diagnosis and treatment, and support for domestically produced equipment, China’s medical device industry is poised to enter a period of rapid growth. The ratio of pharmaceuticals to medical devices in China stands at only 1:0.35, significantly lower than the global average of 1:0.7 and far below the 1:0.98 ratio observed in developed countries, indicating substantial potential for future expansion. It is projected that China’s medical device market will surpass RMB 700 billion in 2020, becoming the fastest-growing subsector within the healthcare industry.

3.2 Market Segments: High Share in Imaging Diagnostics, Rapid Growth in IVD, Domestic Substitution as the Main Theme, and Significant Potential for Home-Use Devices

In terms of market share by medical device subsector, diagnostic imaging holds the largest proportion at 16%, followed by in vitro diagnostics (IVD) at 14%, low-value consumables at 13%, cardiovascular devices at 6%, and orthopedic devices at 6%. Regarding growth rates, IVD, cardiovascular, and ear, nose, and throat (ENT) devices rank as the top three, with growth rates of 19.2%, 18%, and 18%, respectively, all exceeding those of the global market.

Domestic substitution is the main theme of medical device development in China over the next decade. Drawing on the successful experiences of segments where domestic substitution has already been achieved, more fields in China will realize domestic substitution in the next five to ten years.

The maturity of domestically produced equipment is key to import substitution, with endoscopes, chemiluminescence immunoassays, CT scanners, MRI systems, color Doppler ultrasound devices, and hematology analyzers emerging as prime sectors for domestic replacement. The domestic market share for certain implantable consumables and medical devices—including dural patches, cardiac occluders, patient monitors, digital radiography (DR) systems, biochemical diagnostics, and cardiovascular stents—has already exceeded 50%. In contrast, the domestic market share for endoscopes, chemiluminescence immunoassays, CT scanners, MRI systems, color Doppler ultrasound devices, and hematology analyzers remains below 30%.

Benefiting from the accelerating aging of the population and the rising prevalence of chronic diseases, the home medical device market continues to expand. With the advancement of preventive medicine and the gradual maturation of domestic home medical device technologies, the market holds significant potential. It is projected that the market size for home medical devices will reach RMB 95.75 billion in 2020, nearly triple the 2014 level, with a compound annual growth rate (CAGR) of 19%.

3.3 Investment Opportunities in the Medical Device Market

The medical device industry offers numerous market opportunities, focusing on:

IVD manufacturers of high-end products and high-value consumables with significant market share and strong hospital market operational capabilities;

Growth-oriented enterprises with strong capital operation capabilities and excellent integration skills, capable of standing out in niche sectors and expanding into higher-tier markets;

Leading enterprises with outstanding performance across multiple market segments;

Leading Home Medical Device Company.

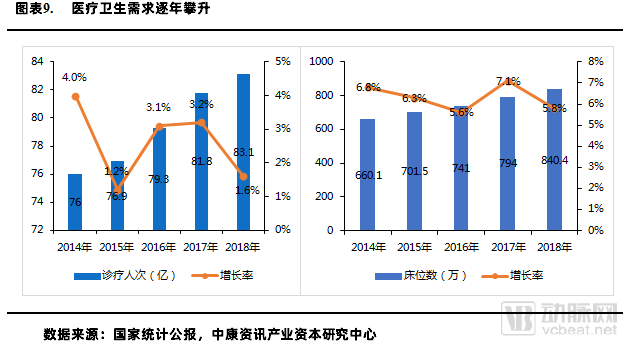

4.1 Aging Drives a Rapid Rise in Healthcare Demand, Poses Challenges to Medical Resources

China has fully entered the stage of population aging. Data shows that in 2018, the elderly population accounted for 11.9%. It is projected to enter the stage of deep aging by 2023, with the elderly population reaching 390 million and accounting for as high as 30% by 2050. One of the impacts of aging is the rapid rise in disease prevalence. Statistical data indicate that the prevalence rate among the elderly population is 2.6 times the average.

The rapidly growing demand among the elderly population for medical care, assistance, nursing, and rehabilitation is posing severe challenges to healthcare and service resources, manifesting in difficulties such as limited access to medical consultations and scarce hospital beds.

Although the state continues to increase investment in medical services and the supply of production factors, the current incremental supply of medical services still fails to meet the rapidly growing demand, and the contradiction between the supply and demand sides of medical services persists.

4.2 Tiered Diagnosis and Treatment, Medical Consortiums, and Other Measures Fall Short of Expected Outcomes

To address the "inverted triangle" mismatch between medical resource allocation and healthcare demand, measures such as tiered diagnosis and treatment and the establishment of medical consortia have been introduced and elevated to a national strategy. The implementation of tiered diagnosis and treatment primarily relies on the development of medical consortia. Models represented by Shanghai and Hangzhou’s family doctor contracting system, and Beijing’s medical consortium framework, have achieved certain positive outcomes.

However, with the implementation of the tiered diagnosis and treatment model, numerous issues have been exposed. Patients’ misconceptions about tiered diagnosis and treatment, coupled with uneven healthcare-seeking behaviors, have hindered its adoption. The professionalism of primary healthcare institutions is constrained by a shortage of licensed physicians; insufficient quantity and quality of licensed physicians have become the most significant bottleneck in implementing the tiered diagnosis and treatment policy. Consequently, the actual outcomes of tiered diagnosis and treatment have fallen short of expectations, necessitating continued vigorous efforts to remove obstacles in the future.

4.3 New Opportunities for High-End Healthcare, Third-Party Medical Services, and Internet-Based Healthcare

Driven by consumption upgrades, robust demand has spurred rapid growth in the high-end medical services market. Data shows that the high-end medical services market is growing at a rate of approximately 25%, outpacing the overall medical services sector. Both the number of individuals served and per capita spending are rising rapidly. It is projected that by 2019, the market size will reach RMB 175 billion, with 42.35 million patient visits. Particularly in developed regions, niche segments such as high-end general practice and specialty clinics, as well as premium services within public hospitals, have experienced rapid development, attracting substantial capital investment and further driving the expansion of the high-end medical market.

The new healthcare reform proposes a “multi-tiered and diversified” medical service system. Multiple policies explicitly support the development of third-party medical service providers and encourage capital investment in the private healthcare sector to address the shortcomings of public healthcare. Against this backdrop, the third-party medical services market has grown rapidly, forming several representative segments such as medical imaging, hemodialysis, health check-ups, and rehabilitation medicine.

It is worth noting that the top three subsectors by scale—medical imaging, hemodialysis, and health check-ups—have each reached a market size of RMB 100 billion. The industry’s robust growth has given rise to a cohort of high-market-capitalization listed companies, such as Aier Eye Hospital (RMB 92 billion), Meinian Onehealth (RMB 40.8 billion), and Tigermed (RMB 38.8 billion).

In April 2018, the “Opinions on Promoting the Development of ‘Internet + Healthcare’” were issued, clarifying development strategies for internet-based healthcare and encouraging its diversified growth. According to the latest report from the National Health Commission, 19 provinces across China have established provincially unified telemedicine network platforms relying on the internet or private networks, with the number of internet hospitals reaching 158, indicating a positive industry trend. It is estimated that the growth rate of the internet healthcare market will remain above 40% in the next two years.

Currently, a surge in investment is sweeping through internet healthcare platforms; however, due to unclear profitability models, the industry remains in an exploratory phase. Taking Ping An Good Doctor as an example, internet healthcare still relies primarily on health e-commerce and consumer-oriented medical services. The sales and profitability models for service-based offerings, such as family doctor services and health management, remain ill-defined, resulting in significant current losses. In the future, with technological advancements in 5G and artificial intelligence, the industry is expected to accelerate its development. Bubbles caused by overheated investment will gradually deflate, and companies lacking core resources and technical capabilities will be eliminated.

4.4 Investment Opportunities in the Healthcare Services Market

Investment Fervor in the Healthcare Services Market: Future Opportunities Lie in:

Specialized Private Medical Institutions with Strong Chain and Group Operation Capabilities

The first enterprise to form a closed loop with commercial insurance and private capital

Third-Party Medical Service Companies with a Large Market Share

The era of transformation in the pharmaceutical and healthcare market has arrived; linear thinking of the past is no longer applicable to future market dynamics. The growth model of the past 30 years, centered on marketing, channels, and advertising, will be difficult to sustain, giving way to a new model driven by therapeutic efficacy, cost, and quality. The core competitiveness of leading enterprises in the pharmaceutical and healthcare sectors will lie in product design, R&D, cost control, manufacturing processes, and supply chain management capabilities.

The next decade will be an uncharted territory for China’s healthcare reform; however, enterprises that navigate this unexplored landscape will emerge stronger from the ashes, giving rise to a cohort of internationalized pharmaceutical and healthcare companies.