2018-2019 China Pharmaceutical Retail Industry Panorama Report: Traditional Pharmacy Models Face Obsolescence as the Sector Enters a Transformation Era

On August 14, Li Junguo, Vice President of Sinopharm Information, released the “Comprehensive Analysis of the Competitive Landscape of China’s Pharmaceutical Retail Industry (2018–2019)” report at the 2019 Xipu Conference. The report analyzed and forecasted the current competitive status and future changes in China’s pharmaceutical retail industry, sparking heated discussions among attendees on the immediate challenges and future development pathways for the sector.

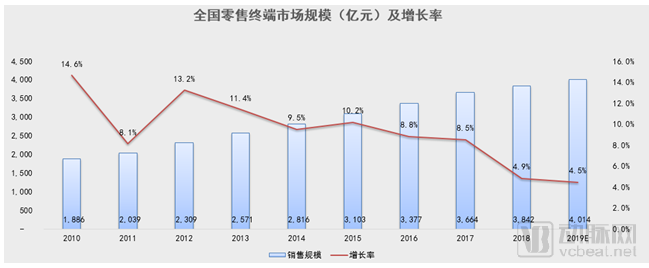

First, the low-growth trend in pharmaceutical retail continues. Data from Sinohealth CMH shows that the total market size of all categories at the retail terminal reached RMB 384.2 billion in 2018, a 4.9% increase from RMB 366.4 billion in 2017; the growth rate decreased by 3.6 percentage points compared to 8.5% in 2017. The sales volume is expected to reach RMB 401.4 billion in 2019, with the year-on-year growth rate declining to 4.5%.

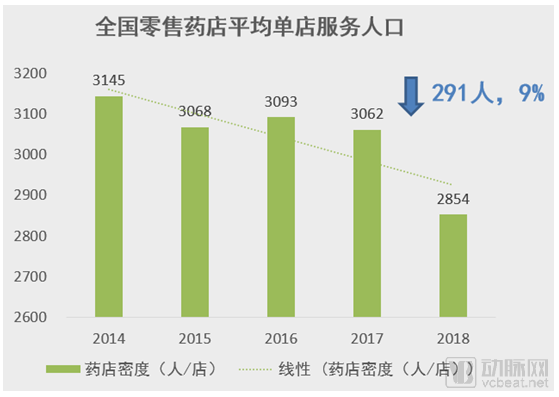

Secondly, despite the slowdown in growth, the number of pharmacies continues to increase, leading to a continued decline in the average population served per store. In 2018, the total number of pharmacy outlets in China reached 489,000, representing a year-on-year increase of 7.7%—the highest growth rate in the past five years. As a result, the average population served per store decreased from 3,145 persons/store in 2014 to 2,854 persons/store currently, a decline of 9%. The pharmacy market can thus be described as oversaturated. According to relevant statistical data from the United States and Japan, the average population served per store was approximately 5,250 persons/store in the U.S. in 2016, while drugstores in Japan served an average of 7,052 persons/store. This indicates that there is considerable room for improvement in the service capacity of pharmacies in China.

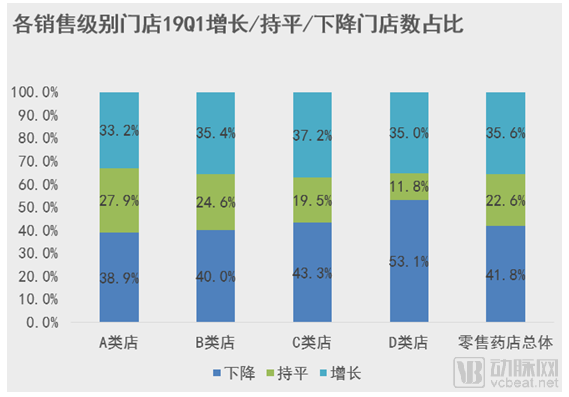

Third, the average annual revenue per store among the top 100 pharmacy chains has declined. Nationwide, small and medium-sized stores account for the largest share of performance downturns. The former indicates that the competitive advantage derived from scale is weakening, while the importance of individual store competitiveness is rising; the latter suggests that the convenience factor, which pharmacies have long taken pride in, is losing its appeal to consumers.

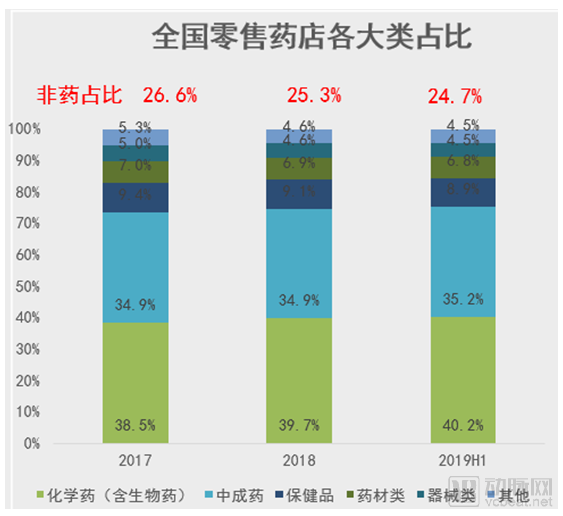

Fourth, the proportion of non-pharmaceutical products in pharmacy sales revenue continues to decline. This is a matter of significant concern given the market landscape characterized by a sharp drop in prescription drug prices triggered by the “4+7” volume-based procurement policy.

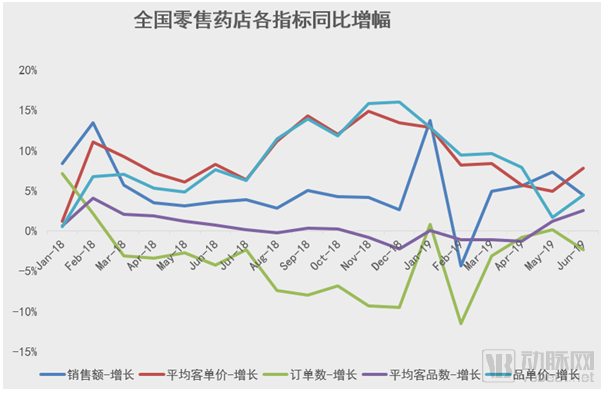

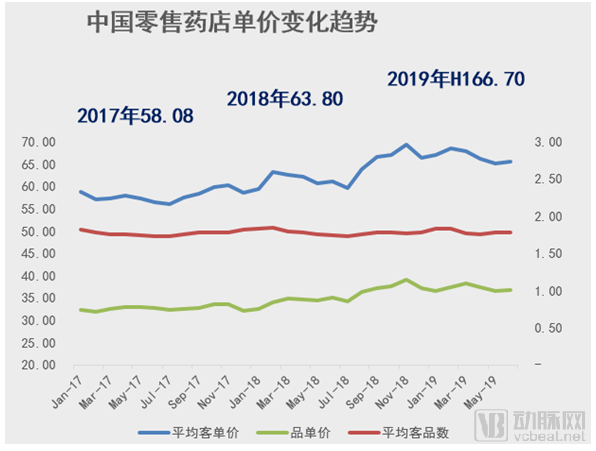

Fifth, the situation where declining foot traffic is offset by price-driven sales growth has not improved. Amidst surging demand for health services, retail pharmacies must urgently develop effective models to attract and retain customers.

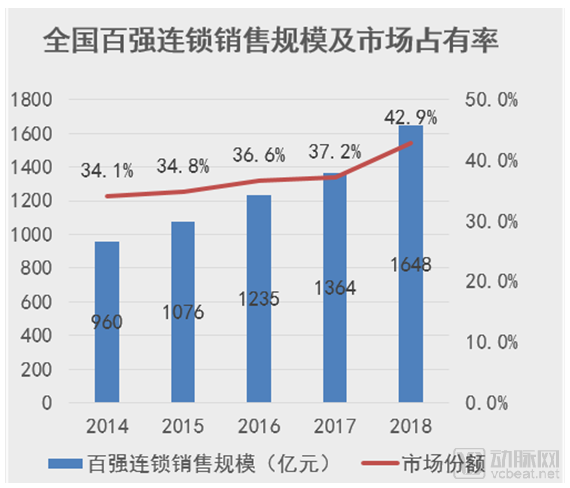

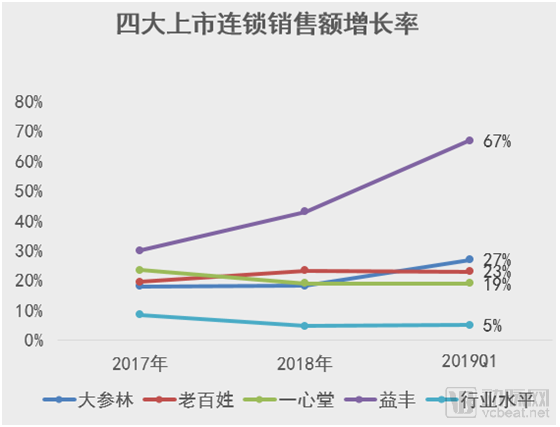

Despite the fierce competitive landscape, driven by capital forces, the concentration of the pharmaceutical retail industry has accelerated, with the top 100 comprehensive competitiveness chain enterprises capturing a market share of 42.9%. Meanwhile, the sales revenue growth rates of the four major listed chain enterprises have surged significantly over the past three years, maintaining a growth rate of over 18%, far exceeding the industry average.

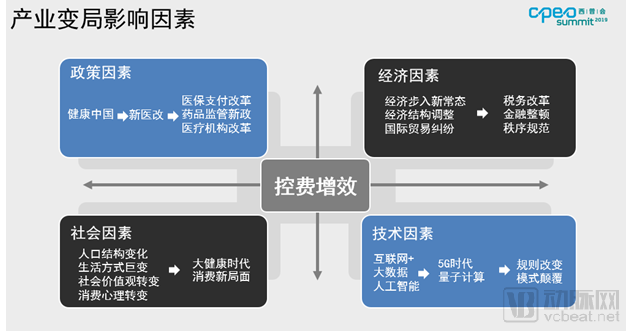

Over the past year, China’s pharmaceutical retail industry has been profoundly impacted by policy changes, particularly a series of new policies aimed at controlling medical insurance expenditures, which have posed significant challenges to the existing business models of retail pharmacies. In fact, “cost control and efficiency enhancement” is not only the core of the new healthcare reform but also reflects a broader consensus across macro-level dimensions—policy, economy, society, and technology (PEST).

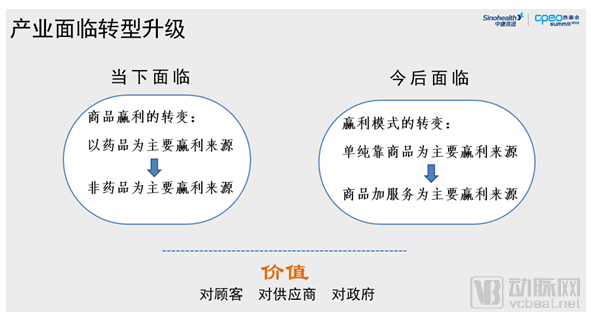

In terms of industrial transformation and upgrading, the primary task currently facing pharmacies is to shift their product profit structure from relying mainly on pharmaceuticals to relying mainly on non-pharmaceutical products. In the future, the key challenge will be to transform the pharmacy’s business model from one driven solely by product sales to one based on a combination of products and services. Only by creating value for customers, suppliers, and the government can retail pharmacies find a viable path forward.

Therefore, the pharmaceutical retail industry will henceforth compete along three core dimensions: competition centered on professional systems anchored in pharmaceutical care capabilities and chronic disease management services; competition driven by business models oriented toward meeting customers’ health needs; and competition focused on big data capabilities aimed at delivering continuous, precision-based services.

In the coming phase, retail pharmacies will primarily develop the following business formats: new specialty pharmacies and hospital-adjacent pharmacies designed to address prescription outflow and the separation of prescribing from dispensing; community-based specialized pharmacies and niche specialty pharmacies that focus on chronic disease management and self-medication for minor ailments; and comprehensive health pharmacies and diversified pharmacies that cater to the diverse health needs of consumers pursuing a high-quality lifestyle.

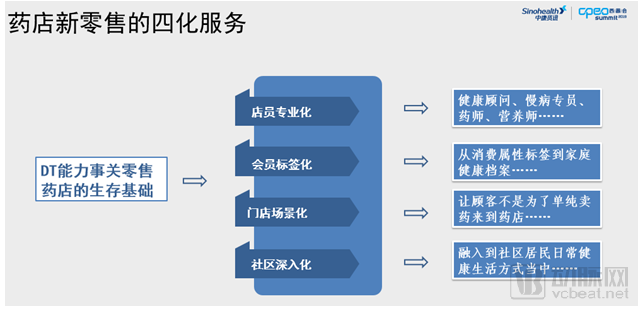

Meanwhile, the new retail model for pharmacies will truly take off, leveraging data and technological capabilities to deliver four key services: professionalization of pharmacy operations, member tagging, scenario-based store experiences, and deeper community engagement.

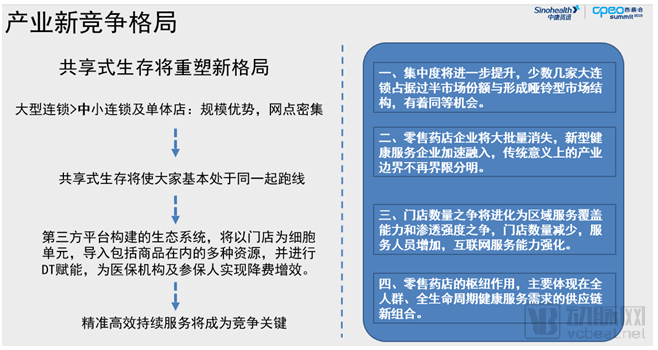

It is foreseeable that as industry concentration increases, a large number of retail pharmacy enterprises will disappear, while new types of health service providers will accelerate their integration. The competition over store count will evolve into a contest of regional service coverage and penetration intensity. The hub role of retail pharmacies will primarily be reflected in the new supply chain combinations addressing the health service needs of the entire population across the full life cycle.

However, the shared living model brought about by the era of artificial intelligence and big data will make it difficult for China to develop an industry landscape in which a few chain pharmacy operators capture more than half of the market share.

The ultimate form of retail pharmacies will be an integrated health service hub that combines self-care experience terminals, hubs for healthy lifestyle connections, professional venues for daily health education, and chronic disease management service centers. In the future, traditional pharmacy models primarily focused on drug sales will struggle to survive.