2019 Rehabilitation Industry Report: Six High-Potential Segments Unlocking a Billion-Dollar Market – Business Models Worth Emulating

“Evolve through innovation or perish in stagnation”—this is an immutable law of industrial development. With the emergence of new technologies such as the internet, artificial intelligence, the Internet of Things (IoT), and 5G, a wave of innovation has swept across the entire healthcare industry. New entities such as telemedicine, smart hospitals, and internet hospitals have emerged with strong momentum, bringing disruptive innovation to traditional healthcare. As an important branch of healthcare, rehabilitation medicine also needs to reshape its value through innovation to achieve better development.

China’s rehabilitation medical sector has progressed through its initial and expansion phases and has now entered a phase of standardization, establishing a three-tier rehabilitation service system that encompasses rehabilitation departments in general hospitals, specialized rehabilitation hospitals, and rehabilitation medical centers or home-based rehabilitation. Moreover, the market size of the entire rehabilitation industry shows promising prospects, with projections indicating it will surpass RMB 100 billion in 2022. The capital market has also shown strong favor toward the rehabilitation industry, with a number of high-quality enterprises securing substantial venture capital financing.

To better analyze the current state of the rehabilitation industry and explore future development opportunities, VCBeat Institute has proposed the "Nine-Box Model for Industry Development Potential Evaluation." Based on extensive expert interviews, corporate surveys, rehabilitation industry investment and financing data, and relevant research methodologies and theories, this model comprehensively evaluates the development potential of various sub-sectors within the rehabilitation industry. It identifies six golden tracks: rehabilitation robotics, telerehabilitation, rehabilitation informatics, musculoskeletal rehabilitation, rehabilitation nursing, and cardiopulmonary rehabilitation, aiming to provide reference for corporate strategic decision-making.

Rehabilitation Medicine Aims to Help Patients Return to Daily Life

Rehabilitation medicine is an emerging discipline that arose in the mid-20th century, primarily serving individuals with disabilities or those suffering from major diseases. Through therapeutic interventions such as physical therapy, occupational therapy, speech therapy, and psychotherapy, it aims to help patients with disabilities or illnesses achieve maximal functional recovery in a timely manner, thereby facilitating their better reintegration into daily life and work.

Rehabilitation medicine can be categorized by disease area into musculoskeletal rehabilitation, cardiopulmonary rehabilitation, pediatric rehabilitation, postpartum rehabilitation, hearing and vision rehabilitation, psychiatric rehabilitation, rehabilitation for disability and dementia, and other forms of rehabilitation.

Figure 1. Subcategories of Rehabilitation Medicine

Image source: VCBeat

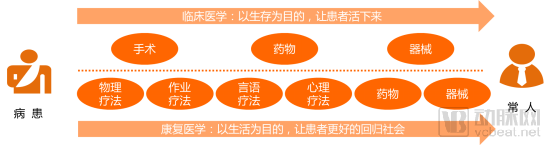

Clinical medicine primarily aims at survival, enabling patients to survive through therapeutic interventions such as pharmaceuticals, medical devices, and surgery. In contrast, rehabilitation medicine focuses on quality of life, employing rehabilitative therapies to partially or fully restore impaired functions, thereby facilitating patients’ better reintegration into society.

Therefore, clinical medicine and rehabilitation medicine are complementary. Clinical medicine intervenes during the treatment phase, while rehabilitation medicine intervenes during the recovery phase. Both ultimately aim to eliminate disease and help patients gradually return to normal life.

Figure 2. Differences Between Rehabilitation Medicine and Clinical Medicine

Image source: VCBeat.

China's Rehabilitation Medical System Construction Has Entered a Standardized Phase

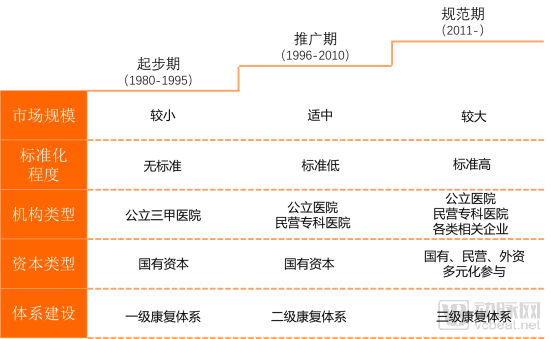

China introduced the modern rehabilitation medical system in the 1980s. After nearly 40 years of development, progress has been made in rehabilitation medical services. Based on indicators such as market size, standardization level, institution types, capital sources, and system construction, the development of rehabilitation medicine is divided into three stages: the initial stage, the promotion stage, and the standardization stage, each characterized by distinct features.

Figure 3. Development History of China’s Rehabilitation Medical System Construction

Image source: VCBeat

(1) Initial Stage (1980–1995)

Rehabilitation medicine originated in Europe and the United States. China began exploring the development of rehabilitation medical services in the 1980s, exemplified by the establishment of the China Rehabilitation Research Center in Beijing in 1988. During this initial phase, the overall market size for rehabilitation medical services in China was relatively small and concentrated primarily in major cities such as Beijing and Shanghai. Rehabilitation services were mainly provided by certain public tertiary Grade A hospitals, with costs covered by state fiscal support. As the sector was still in an exploratory stage of development, China had not yet established a standardized service system for rehabilitation medicine.

(2) Promotion Phase (1996–2010)

After more than a decade of exploration and experimentation, extensive experience in the development of rehabilitation medical services has been accumulated, leading to the nationwide promotion of such initiatives. In 2009, the State Council issued the “Opinions on Deepening the Reform of the Pharmaceutical and Health Care System,” which proposed integrating prevention, treatment, and rehabilitation to enhance the level of healthcare coverage, thereby providing policy support for local efforts in developing rehabilitation medical services. More than twenty provinces have subsequently established rehabilitation service institutions.

During this period, the rehabilitation market continued to expand. In addition to public hospitals, private specialized rehabilitation institutions emerged, represented by Beijing Yingzhi Rehabilitation Hospital and Beijing Hexie Rehabilitation Hospital, initially forming a two-tier rehabilitation system comprising comprehensive tertiary hospitals and specialized rehabilitation hospitals. However, due to the lack of policies on rehabilitation standardization, the level of standardization in rehabilitation services and facility development remained relatively low.

(3) Standardization Phase (2011–)

In 2011, the Ministry of Health issued the Guidelines for the Construction and Management of Rehabilitation Medicine Departments in General Hospitals, mandating that all general hospitals at Level II and above must establish rehabilitation medicine departments. This policy provided clear direction for the development and management of hospital-based rehabilitation departments. In 2012, the Ministry of Health further released the Basic Standards for Rehabilitation Hospitals (2012 Edition), thereby bringing the construction of rehabilitation hospitals onto a standardized track.

In 2017, the National Health and Family Planning Commission issued the "Notice on Printing and Distributing the Basic Standards and Management Specifications (Trial) for Rehabilitation Medical Centers and Nursing Centers," which put forward standardized construction requirements for rehabilitation medical centers. Therefore, the construction of China's rehabilitation medical system has entered a period of standardization.

Three-Tier Service System Builds the Infrastructure for Rehabilitation Medical Care

As early as 2011, the Ministry of Health issued the “Notice on Launching Pilot Work to Establish and Improve the Rehabilitation Medical Service System,” proposing the establishment of a three-tier rehabilitation medical service system and launching pilot programs in 14 provinces (municipalities directly under the Central Government), including Beijing, Heilongjiang, Shanghai, Jiangsu, and Fujian. The notice required each pilot province (municipality) to select at least two cities to explore the establishment of a rehabilitation medical service system and complete the pilot work within two years.

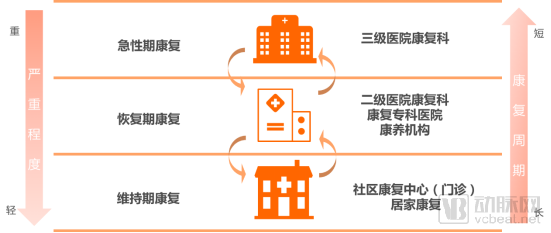

Figure 4. Schematic Diagram of the Three-Tier Rehabilitation Medical System

Image source: VCBeat

China's rehabilitation medical system consists of rehabilitation departments in tertiary hospitals, rehabilitation departments in secondary hospitals (specialized rehabilitation hospitals), community rehabilitation centers (outpatient clinics), and home-based rehabilitation. Rehabilitation departments in tertiary hospitals primarily provide rehabilitation treatment during the acute phase; those in secondary hospitals (specialized rehabilitation hospitals) mainly handle rehabilitation during the recovery phase; while community rehabilitation medical centers (outpatient clinics) and home-based rehabilitation primarily deliver maintenance-phase rehabilitation care.

Establish a two-way referral mechanism among rehabilitation institutions at all levels. After the Department of Rehabilitation Medicine in tertiary hospitals completes acute-phase rehabilitation for patients, they are referred downward to secondary hospital rehabilitation departments and other institutions for recovery-phase and maintenance-phase rehabilitation treatment. If deterioration occurs during the recovery or maintenance phase, patients can be promptly referred upward to the Department of Rehabilitation Medicine in tertiary hospitals for treatment.

By establishing a three-tier rehabilitation medical system, comprehensive and phased rehabilitation services can be provided to patients throughout the entire care continuum, ensuring optimal rehabilitation outcomes.

Figure 5. Main Differences Among Rehabilitation Service Institutions at Various Levels

Image source: VCBeat

Within the three-tier rehabilitation system, rehabilitation institutions at different levels have distinct functions and characteristics.

Tertiary hospitals were the earliest to integrate rehabilitation services, providing early specialized treatment for patients with diseases and injuries. These facilities require a multidisciplinary service team comprising specialist physicians, rehabilitation physicians, rehabilitation therapists, and rehabilitation nurses. Upon completion of acute care, patients can be referred to lower-tier rehabilitation institutions, resulting in a shorter rehabilitation cycle.

Rehabilitation departments in secondary hospitals and similar institutions primarily provide restorative rehabilitation services to patients who have undergone treatment and whose conditions are stable. These patients typically require a period of inpatient recovery, with medical services mainly delivered by rehabilitation physicians, rehabilitation therapists, and rehabilitation nurses.

Community rehabilitation medical centers and similar institutions primarily provide long-term rehabilitation services to patients who have undergone treatment. Patients generally do not require hospitalization; instead, they either visit rehabilitation facilities regularly for therapeutic training or receive in-home guidance from rehabilitation physicians (therapists).

In the development of the rehabilitation medical system, relevant competent authorities have established corresponding construction standards for rehabilitation departments in general hospitals and various types of rehabilitation medical institutions. Through systematic classification and organization, these standards primarily cover five aspects: departmental area, departmental setup, bed allocation, staffing, and equipment configuration.

Table 1 Construction Standards for Hospital Rehabilitation Departments and Rehabilitation Medical Institutions

Data source: "Basic Standards for Rehabilitation Hospitals (2012 Edition)" and other government public documents

Through comparison, we find that:

(1) In terms of software and hardware infrastructure, tertiary rehabilitation specialty hospitals are the best, featuring large departmental construction areas, comprehensive departmental setups, a larger number of beds, rational staffing, and well-equipped facilities.

(2) In terms of staffing, general hospitals hold an advantage, with higher standards for the allocation of physicians, rehabilitation therapists, and rehabilitation nurses per bed. This is primarily attributable to their rich pool of high-quality medical talent, which provides robust personnel support for the development of rehabilitation departments.

(3) In terms of service functions, both rehabilitation departments in general hospitals and specialized rehabilitation hospitals cover key processes such as rehabilitation assessment, functional evaluation, and therapeutic interventions, thereby providing patients with integrated rehabilitation services.

However, current construction standards do not yet address issues such as the standardization of rehabilitation service processes, the digitalization of rehabilitation equipment, and coordination mechanisms among rehabilitation institutions. These factors directly impact the efficiency of rehabilitation treatment and the quality of rehabilitation services. Relevant competent authorities will subsequently formulate corresponding standards and policies to continuously improve rehabilitation medical services.

China’s rehabilitation medical system has entered a phase of standardization, which implies that there will be more formalized and standardized rehabilitation service institutions in the future, offering an increasingly diverse range of rehabilitation services. What is the current size of China’s rehabilitation industry market, and what are the primary drivers of its growth? We will explore these questions further.

During the initial phase, market demand for the rehabilitation industry was not particularly evident. In the promotion phase, as the rehabilitation system gradually improved, it drove consumption of rehabilitation medical services, leading to a slow growth in market demand. After entering the standardization phase, the rehabilitation system became capable of meeting the rehabilitation needs associated with various types of diseases, and public awareness of rehabilitation steadily increased, propelling the entire rehabilitation industry into a stage of rapid development.

The Rehabilitation Industry Market Continues to Grow, with Its Scale Exceeding 100 Billion Yuan

China's rehabilitation industry started relatively late and is currently in a growth stage. There remains a significant gap compared to the United States in terms of the number of rehabilitation institutions, the number of rehabilitation physicians, and per capita rehabilitation expenditure, indicating substantial potential for future development.

Table 2 Comparison of the Rehabilitation Industry Development in China and the United States

Data Source: VCBeat Database

A comparison of the rehabilitation industry development in China and the United States reveals that the number of rehabilitation institutions in the U.S. is ten times that of China, the number of rehabilitation physicians is three times higher, and per capita rehabilitation expenditure in China is 1/17th of that in the U.S. Particularly regarding rehabilitation insurance coverage, the U.S. employs a prospective payment system based on the Uniform Data System for Medical Rehabilitation (UDSMR), utilizing the Functional Independence Measure (FIM) as an assessment tool and a series of Function-Related Groups (FIM-FRGs) as the basis for reimbursement, covering the majority of rehabilitation services.

According to the latest medical rehabilitation insurance policy, the "Notice on Including Certain Medical Rehabilitation Items in the Basic Medical Insurance Payment Scope" (Ren She Bu Fa [2016] No. 23), only 20 medical rehabilitation items are currently covered by medical insurance in China, primarily focusing on musculoskeletal rehabilitation and pediatric disease rehabilitation, resulting in limited coverage. It is precisely this shortfall in China’s rehabilitation medical services that has created significant opportunities for development.

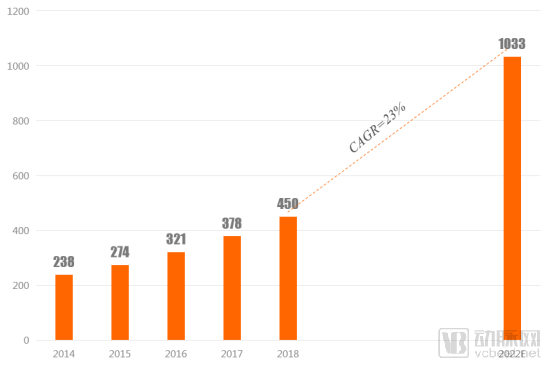

Figure 6 Growth of China's Rehabilitation Medical Market Size, 2014–2022

Data Source: VCBeat Database; Chart by VBInsight

According to market research, the per capita rehabilitation expenditure in China was approximately RMB 32 in 2018. With rising income levels and increased spending on rehabilitation services, the per capita expenditure is projected to reach around RMB 74 by 2022, at which point the size of China’s rehabilitation market is expected to attain RMB 103.3 billion.

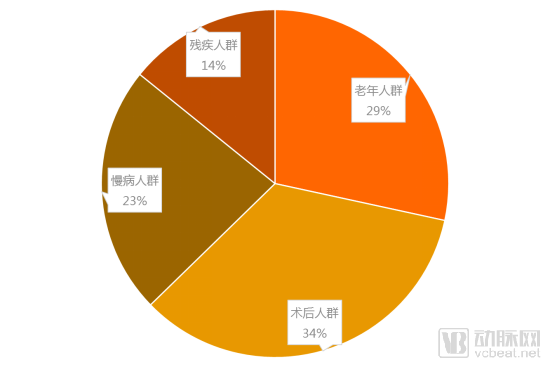

Postoperative Patients Become the Primary Population for Rehabilitation Medical Services

Figure 7 Proportion of Various Service Populations in China's Rehabilitation Market

Data source: VCBeat database; Chart by VBInsight

Based on the distribution of rehabilitation patients in 2018, postoperative patients accounted for more than one-third. This group represents a population with strong demand for rehabilitation services, as surgical procedures invariably cause varying degrees of physical trauma. Rehabilitation facilitates recovery from such trauma and further consolidates therapeutic outcomes. Patients undergoing orthopedic, cardiopulmonary, and neurological surgeries constitute the primary sources of the postoperative rehabilitation population.

For patients who have undergone pelvic fixation, knee arthroplasty, or limb bone segment reconstruction, the absence of scientifically guided postoperative rehabilitation can lead to complications such as pelvic malalignment, thromboembolism, and prosthetic loosening. Additionally, patients who have undergone coronary artery bypass grafting or heart valve replacement require exercise-based rehabilitation therapy to improve their mental well-being and restore organ function.

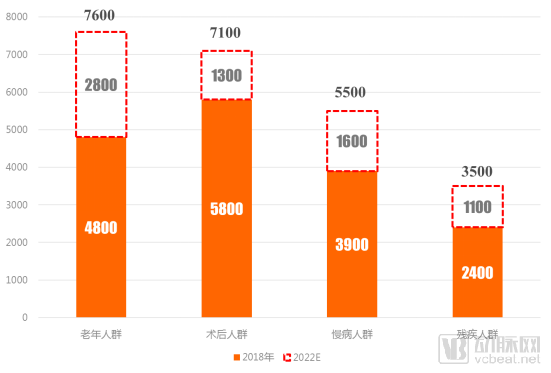

Figure 8 Future Growth Scale of the Rehabilitation Market's Service Population

Data Source: VCBeat Database; Chart by VBInsight

Population aging has become the primary trend in the evolution of China’s demographic structure. In 2018, the proportion of the population aged 60 and above reached 17.9%, and the elderly population is projected to reach 255 million by 2020. We estimate that approximately 30% of the elderly population requires rehabilitation medical services; consequently, the number of elderly individuals needing rehabilitation will increase by 28 million, exceeding 76 million. In particular, disabled and partially disabled older adults will become the key target group for rehabilitation services.

Another rapidly growing segment of rehabilitation patients comes from the population with chronic diseases. According to the Blue Book of Health Management: Report on the Development of China’s Health Management and Health Industry (2018), jointly released by Zhongguancun New Zhiyuan Health Management Research Institute, the Health Management Research Center of Central South University, and Social Sciences Academic Press, the prevalence rates among individuals undergoing health examinations in 2017 were 94.24‰ for hypertension, 62.78‰ for fatty liver disease, and 34.03‰ for diabetes. Rehabilitation treatment for individuals with chronic diseases is a long-term, continuous process and will become a significant driving force in the development of the rehabilitation market.

Rehabilitation Institutions Have Become the Primary Force Driving the Development of the Rehabilitation Medical Market

The rehabilitation medical supply market is primarily situated in the upstream and midstream segments of the rehabilitation industry chain. The upstream segment encompasses rehabilitation devices, rehabilitation robots, rehabilitation informatics, the construction and operation of specialized rehabilitation departments, and the training of rehabilitation professionals. The midstream segment mainly refers to institutions that provide rehabilitation medical services to downstream patients, including general hospitals, specialized rehabilitation hospitals, rehabilitation medical centers or clinics, tele-rehabilitation services, and rehabilitation nursing facilities.

Figure 9. Panoramic Map of the Rehabilitation Medical Services Market

Image source: VCBeat.

We have identified the specific pain points in rehabilitation medical services addressed by each type of institution operating in the market:

(1) Rehabilitation equipment enterprises mainly provide assistive devices such as canes, wheelchairs, orthoses, braces, and splints. These devices assist patients in undergoing rehabilitation training during the course of treatment, enabling therapists to enhance rehabilitation outcomes. However, traditional rehabilitation equipment has seen limited integration with emerging technologies such as the Internet of Things (IoT) and artificial intelligence (AI), resulting in a relatively low level of intelligence.

(2) Rehabilitation robotics companies are applying high-tech solutions such as artificial intelligence, the Internet of Things, and big data to rehabilitation equipment, making these devices more user-friendly and intelligent. This enables goals such as human-machine interaction, intelligent assisted training, and precise force control. There is a wide variety of rehabilitation robots, including exoskeleton robots, TMS-navigated robots, gait training robots, and nursing robots. However, current applications are mainly concentrated in a few areas, such as musculoskeletal rehabilitation, hearing and vision rehabilitation, and speech rehabilitation. In the future, greater technological innovation is needed to expand applications into fields such as cardiopulmonary rehabilitation and neurological rehabilitation.

(3) Rehabilitation informatics companies provide information management systems that cover the entire workflow, including rehabilitation assessment, medical record management, rehabilitation documentation, treatment planning, staff scheduling, data collection and management, and follow-up care. These systems address pain points such as non-standardized rehabilitation data, high subjectivity in assessment scales, and the lack of interoperability among rehabilitation data sources, thereby achieving standardization of rehabilitation therapy through comprehensive digital management. However, rehabilitation informatics systems still need to further resolve integration issues with other hospital systems, such as HIS, LIS, and PACS.

(4) The development and operation of rehabilitation departments are primarily designed to serve medical institutions or enterprises that lack the capacity to build rehabilitation disciplines and have limited experience in management and operations. The establishment of a rehabilitation department must take into account the hospital’s existing clinical departments, physician workforce structure, and regional disease spectrum characteristics, while aligning with public demand. Differentiated rehabilitation services serve as the foundation for building the department’s core competitiveness.

(5) The cultivation of rehabilitation professionals primarily aims to address the shortage of rehabilitation medical personnel in China. This shortage directly constrains the coverage and quality of rehabilitation services. As a country with substantial demand for rehabilitation services, China needs to establish a comprehensive talent development mechanism to provide adequate human resource support for rehabilitation medical institutions.

(6) Within the three-tier rehabilitation service system, general hospitals primarily address the challenges of early-stage specialized treatment for patients with diseases or injuries, enabling them to exit the critical phase as soon as possible. Specialized rehabilitation hospitals provide inpatient rehabilitative services to patients whose conditions have stabilized following initial treatment. Rehabilitation medical centers, outpatient clinics, and similar institutions mainly offer long-term non-inpatient rehabilitation services to patients who have undergone treatment. Rehabilitation service providers must improve the two-way referral mechanism to achieve seamless, integrated rehabilitation care.

(7) Tele-rehabilitation leverages internet technology to shift certain rehabilitation medical services from offline to online platforms. Physicians can provide patients with remote rehabilitation consultations, guidance on rehabilitation training, medical record management, and follow-up care, thereby making rehabilitation more accessible and convenient.

(8) Rehabilitation nursing primarily provides professional home-based and hospital care services to individuals with functional impairments, the elderly, and patients with chronic diseases, addressing their daily living challenges or assisting them in better completing rehabilitation treatment. Future rehabilitation nursing will evolve toward customization, premium quality, and intelligent solutions.

Table 3 Major Pain Points in Rehabilitation Therapy Addressed by Different Types of Institutions

Data Source: Public Information

In 2022, the market size of China’s rehabilitation industry is expected to exceed RMB 100 billion, with the rehabilitation market further segmented into multiple service areas. Faced with such a substantial market opportunity, which sectors will capture significant market share? We will identify the most promising “golden tracks” in rehabilitation using the “Nine-Box Model for Industry Development Potential Assessment.”

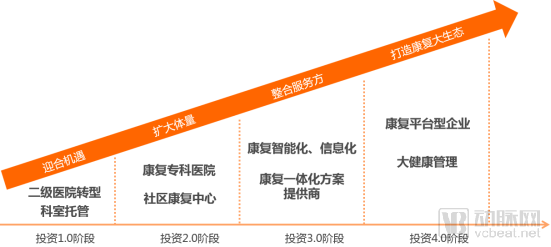

Capital Invests in the Rehabilitation Industry Along the “Point–Line–Plane” Trajectory

No industry can thrive without the support of capital. By compiling and analyzing investment events in the rehabilitation sector, it has been found that capital investment in this industry follows a “point–line–plane” trajectory.

Figure 10. Capital Investment Pathway of China’s Rehabilitation Industry

Image source: VCBeat

(1) "Point" Investment

This primarily refers to the 1.0 and 2.0 phases of investment in the rehabilitation industry. During the 1.0 phase, investments mainly capitalized on opportunities arising from the transformation of public hospitals. At that time, relevant policies mandated that general hospitals at the secondary level and above establish departments of rehabilitation medicine. Coinciding with a wave of public hospital restructuring, this period saw the emergence of high-quality investment targets among secondary hospitals transitioning into rehabilitation-focused facilities. Investment strategies during this phase primarily involved entrusting the management of rehabilitation departments in public hospitals or directly participating in equity investments for the transformation of secondary hospitals.

Having accumulated experience in the management and operation of rehabilitation hospitals during the 1.0 phase, capital seeks to expand the scale of its targets and enter the 2.0 phase. It has begun to screen sub-sectors of the rehabilitation industry, with key criteria including a large patient population base, easily identifiable target groups, strong willingness to pay, high unit prices, and robust profitability. As a result, specialized rehabilitation hospitals or community rehabilitation centers focusing on musculoskeletal rehabilitation, pediatric disease rehabilitation, and cardiopulmonary rehabilitation have become primary investment targets, with an emphasis on standardized and chain-based expansion.

(2) “Line”-Style Investment

With the application of high-tech innovations such as the Internet, big data, artificial intelligence, and the Internet of Things (IoT) in rehabilitation medicine, the rehabilitation industry has entered Investment Phase 3.0, characterized by intelligent and informatized advancements in rehabilitation healthcare. While capital continues to value enterprises that address specific bottlenecks within the rehabilitation care continuum, there is a growing emphasis on integrated solution providers capable of delivering comprehensive services encompassing rehabilitation equipment, professional talent, management and operations, and IT infrastructure development. Investors aim to better serve patients by integrating various rehabilitation service providers.

(3) “Face”-style Investment

Future investment in the rehabilitation industry will trend toward building a comprehensive rehabilitation ecosystem, with capital focusing on platform-based enterprises. These platforms will not only provide one-stop, full-cycle rehabilitation medical services to C-end patients but also empower B-end enterprises by aggregating technology, capital, talent, and management resources. They will serve healthcare, pharmaceutical, and medical insurance companies across the rehabilitation industry chain, creating a “second” growth engine for their future development.

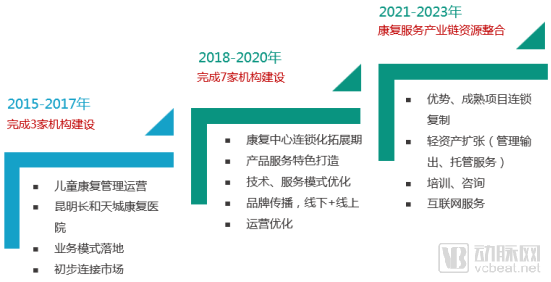

For instance, Changhe Medical, as a representative enterprise in the rehabilitation sector, is dedicated to investing in, managing, and operating rehabilitation medical institutions. It introduces internationally advanced rehabilitation technologies, services, and management models, integrates industrial resources, and promotes the development of rehabilitation healthcare in China.

From 2015 to 2017, the company made its initial entry into the rehabilitation medical market by investing in and constructing the Changhe Dayun Pediatric Rehabilitation Outpatient Clinic and the Kunming Changhe Tiancheng Rehabilitation Hospital.

From 2018 to 2020, Changhe Medical will leverage its investment and operational management expertise in the rehabilitation sector, center on its core competencies, continuously optimize its technology and service models, and focus on cultivating distinctive product and service features. The company will implement a chain-based investment strategy for rehabilitation facilities in cities including Beijing, Shanghai, Shenzhen, and Kunming.

From 2021 to 2023, while strengthening its core business, Changhe Medical will export its rehabilitation management and operational capabilities, integrate resources across the rehabilitation services industry chain, and vertically consolidate key assets—including rehabilitation equipment, professional education and training for rehabilitation personnel, and entrusted operation of rehabilitation medical facilities—to leverage the benefits of resource aggregation.

Figure 11. Investment Layout of Cheung Kong Medical Rehabilitation Industry

Image source: VCBeat

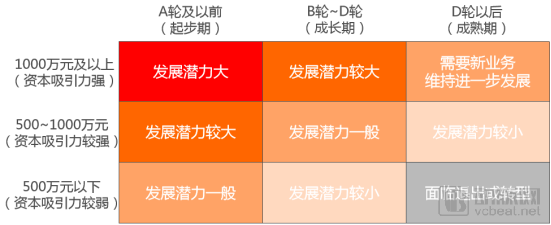

“Nine-Box Model for Evaluating Industry Development Potential” Explained

To further reflect the current state of capital financing and investment in the rehabilitation industry, VCBeat Research Institute, building on its prior research findings and referencing similar studies, has proposed the “Nine-Box Model for Industry Development Potential Assessment.” This model provides a comprehensive evaluation of the industry’s development potential by analyzing two dimensions: financing rounds and financing amounts.

Corporate financing rounds are closely linked to an industry’s development stage. In the early stage of an industry, corporate financing primarily consists of angel and Pre-A rounds. As companies continue to grow and expand, their financing rounds progressively advance. When the majority of companies reach Series D financing or beyond, it signals that the industry is entering a mature phase. Financing rounds are mainly categorized into three stages: Series A and earlier, Series B to Series D, and post-Series D, which correspond to the early, growth, and mature stages, respectively.

The size of financing directly reflects the level of attention and recognition from the capital market for the industry in which a company operates. A higher financing amount indicates stronger appeal to capital, which can enhance the overall capital attractiveness of the industry and attract more institutional investors to participate in industry investments. Financing amounts are primarily categorized into three tiers: below RMB 5 million, RMB 5 million (inclusive) to below RMB 10 million, and RMB 10 million and above.

Figure 12 Nine-Box Matrix Model for Evaluating Industry Development Potential

Image source: VCBeat

We categorize the industry’s development potential into five tiers based on variations in financing rounds and the distribution of funding amounts: high development potential, relatively high development potential, moderate development potential (including cases requiring new business lines to sustain further growth), low development potential, and facing difficulties in exit or transformation.

(1) Significant growth potential

If the majority of companies in an industry have secured financing at Series A or earlier stages, with each round amounting to RMB 10 million or more, it indicates that the industry has attracted significant capital interest from its inception. Investment firms are willing to make substantial bets on the sector, which largely reflects their optimism about the industry’s future prospects. This suggests that further investment will likely follow, highlighting the industry’s strong growth potential.

(2) Significant growth potential

It is mainly divided into two scenarios: one where the industry is in its nascent stage, characterized by high financing volumes and strong appeal to investment institutions; and another where the industry has entered the growth phase, marked by high investment amounts but more stringent selection criteria by investors, resulting in a limited number of companies securing substantial funding.

(3) Average development potential

The industry is in its infancy with low financing volumes, making it unattractive to investment institutions; alternatively, the industry has entered the growth stage, yet capital investment remains low and investor recognition is limited. Furthermore, while the industry has reached maturity and investment firms are willing to provide funding, this is contingent upon sustained corporate growth. Specifically, companies must continuously explore new business lines to maintain their existing growth trajectory, thereby facing significant developmental pressure.

(4) Limited development potential

The industry is in its growth stage, yet it holds limited appeal to capital. Investment institutions perceive significant uncertainty within the sector and are therefore hesitant to make substantial investments. Even as the industry matures, its attractiveness to capital remains moderate, making it difficult for the sector to secure the large volumes of funding needed to sustain its development.

(5) Facing Exit or Transformation

The industry is in its mature stage, yet capital remains indifferent and pessimistic about its future growth. Companies face the dual dilemma of either exiting the market or undergoing transformation; successful transformation will offer them a chance for rebirth.

Analysis of the Development Potential in Sub-sectors of the Rehabilitation Industry

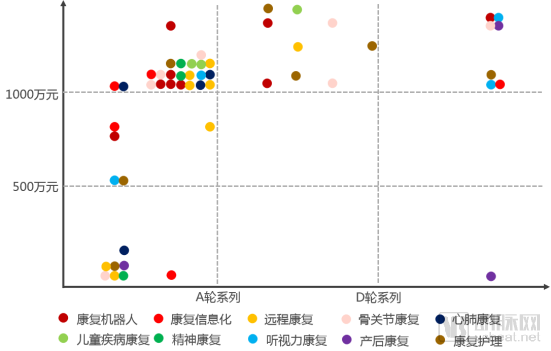

According to the service map of the rehabilitation medical industry, midstream rehabilitation medical services are further subdivided by disease type into seven areas: musculoskeletal rehabilitation, cardiopulmonary rehabilitation, pediatric rehabilitation, psychiatric rehabilitation, hearing and vision rehabilitation, postpartum rehabilitation, and rehabilitative nursing (rehabilitation for disability and dementia). In addition, three emerging areas have been identified in recent years: rehabilitation robotics, rehabilitation informatics, and tele-rehabilitation.

VCBeat has compiled investment and financing data for 53 rehabilitation companies across the aforementioned ten sub-sectors (see Appendix). Based on the financing status of these companies, a heat map of industrial investment and financing trends was developed. The overall distribution of investment and financing hotspots is concentrated primarily in the Pre-Series A to Series A stages, with financing amounts of RMB 10 million or more. This indicates that the rehabilitation industry holds significant growth potential and attracts substantial attention from the capital market. Investment institutions are optimistic about the industry’s development prospects, as evidenced by the large number of companies securing substantial funding during their early stages.

Figure 13 Distribution of Investment and Financing Hotspots in the Rehabilitation Industry

Source: VCBeat Database; Chart by VBInsight

Further analysis of the distribution of investment and financing hotspots in the sub-sectors of the rehabilitation industry reveals that financing amounts in the rehabilitation robotics sector are all RMB 10 million or above, with over 60% of these transactions occurring prior to Series A. Similarly, in the tele-rehabilitation sector, more than 60% of financing events also involve amounts of RMB 10 million or above and occur at Series A or earlier stages. According to the nine-box matrix model for evaluating industry development potential, both rehabilitation robotics and tele-rehabilitation are classified as industries with high growth potential.

Financing events in the field of rehabilitation informatics have primarily occurred at Series A and earlier stages, with funding amounts mainly ranging between RMB 5 million and RMB 10 million, demonstrating strong appeal to capital. In contrast, financing in the fields of musculoskeletal rehabilitation and rehabilitative nursing has been concentrated at RMB 10 million or more, with half of these deals occurring after Series A, indicating that the industry has entered a growth phase. Furthermore, all financing events in the cardiopulmonary rehabilitation sector have taken place at Series A and earlier stages, but most funding amounts were below RMB 10 million, suggesting that this industry is still in its infancy, with only a select number of projects securing substantial investment.

Similarly, according to the 3x3 matrix model for evaluating industry development potential, the aforementioned four sub-sectors all belong to industries with significant growth potential.

Therefore, by combining the distribution of investment and financing hotspots in sub-sectors of the rehabilitation industry with the nine-box model for evaluating industry development potential, we believe that six key areas—rehabilitation robotics, telerehabilitation, rehabilitation informatics, musculoskeletal rehabilitation, rehabilitation nursing, and cardiopulmonary rehabilitation—will emerge as the prime growth sectors in the future of rehabilitation. Next, we will focus on analyzing representative companies in these prime sectors to gain further insights into industry development through their corporate trajectories.

The above is an excerpt from the report. The report also provides an in-depth analysis of the business models of representative companies in high-growth sectors, for reference by industry professionals. Below is the overall structure of the report:

I. Insight: The Industry Enters a New Era, with a Three-Tier System Building Rehabilitation Services

1.1 Rehabilitation Medicine Aims to Facilitate Patients’ Return to Daily Life

1.2 China’s Rehabilitation Medical System Construction Has Entered a Phase of Standardization

1.3 A Three-Tier Service System Constructs the Infrastructure for Rehabilitation Medical Care

II. Market: Promising Future Prospects and a Diversified Consumer Base

2.1 The Rehabilitation Industry Market Is Growing Continuously, with Its Scale Expected to Exceed RMB 100 Billion

2.2 Postoperative Patients Become the Primary Population for Rehabilitation Medical Services

2.3 Rehabilitation Institutions Become the Primary Force Driving the Development of the Rehabilitation Medical Market

III. Market Segments: Evaluating Growth Potential in Niche Areas to Identify Prime Opportunities in Rehabilitation

3.1 Capital Invests in the Rehabilitation Industry Along the “Point–Line–Plane” Trajectory

3.2 Explanation of the “Nine-Box Model for Evaluating Industry Development Potential”

3.3 Analysis of the Development Potential in Sub-sectors of the Rehabilitation Industry

IV. Case Studies: In-Depth Analysis of Representative Enterprises to Create a Model for Rehabilitation Services

4.1 MaiBu Robotics: Four Key Technologies Empower the Intelligentization of Rehabilitation Equipment

4.2 Yujian Weilai: Home-Based Intelligent Rehabilitation Platform Empowers Remote Rehabilitation

4.3 Huawei Technology: Four Major Solutions Comprehensively Support the Informatization Construction of Rehabilitation

4.4 Yuanzizai Rehabilitation: Specialized Disciplines and Diseases, Deeply Cultivating the Bone and Joint Rehabilitation Market

4.5 Julu Medical: Focusing on the Systematic Development of Rehabilitation Services, Specialized Comprehensive Care, and Cardiopulmonary-Diabetes Rehabilitation Diagnosis and Treatment Systems

4.6 Reihuaxinkang: Three Major Systems + Five Prescriptions Build Characteristic Cardiac Rehabilitation Services

V. Trends: Assessing Future Developments and Identifying Industry Growth Drivers

5.1 Internet-Based Rehabilitation Hospitals Emerge as a New Business Model in the Rehabilitation Medical Industry

5.2 Technology, Talent, and Service Build the Future “Golden Triangle” of Rehabilitation

5.3 Specialized Rehabilitation Will Become the Mainstream Model of Rehabilitation Services

Scan the QR code below to access the full version for free.“2019 Research Report on the Development Potential of the Rehabilitation Industry”andList of Investment and Financing for Rehabilitation Industry Enterprises。