Apple, Huami, and Huawei Double Down: $600M in 14 Investments in Six Months Signals Health-Focused Wearables Rebound

Samsung Electronics

South Korea's largest electronics manufacturing company

Magic Leap

Wearable Device Supplier

Apple

Designers, manufacturers, and sellers of electronic products such as personal computers and software

Jawbone

Wearable Device R&D and Manufacturer

Fitbit

Wearable Device Developer

Wearable devices, once dormant for a long time, have recently regained momentum by leveraging the tailwinds of the healthcare sector. The current fervor surrounding wearables is also evident from the recent moves of key industry players. On August 19, Huami Technology (NYSE: HMI), a global leader in wearable devices, released its financial report for the second quarter of 2019, delivering impressive results. Just a few days earlier, Huami held its autumn product launch event, unveiling new sports and health-focused smartwatches and fitness bands. Meanwhile, Apple is also expected to release the next-generation Apple Watch at its September autumn event, with medical applications becoming the key determinant of its continued popularity. In the future era of data-driven healthcare, wearable devices, as one of the primary data interfaces, are receiving increasing attention. A war without visible smoke is underway.

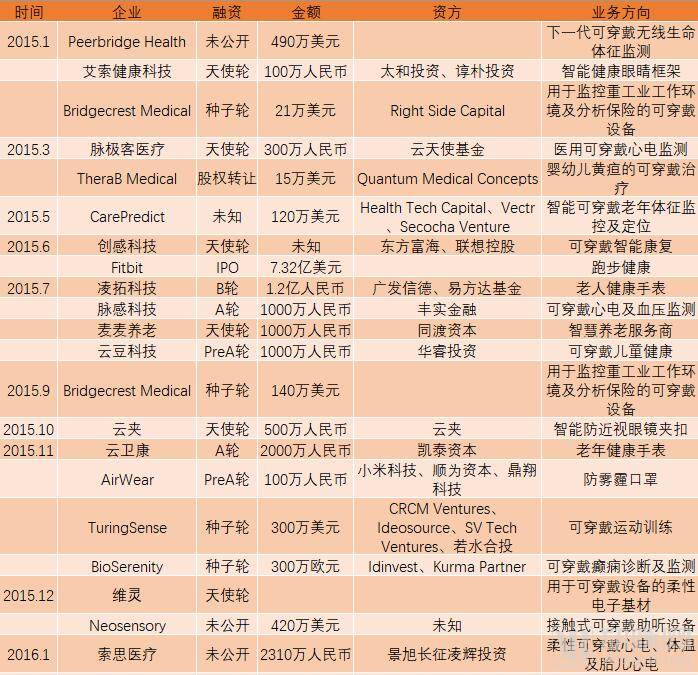

It is fair to say that the potential for wearable devices in healthcare is as vast as the scope of medicine itself. Consequently, capital has remained highly enthusiastic about wearable technology. In just six months, VCBeat (WeChat ID: Vcbeat) recorded a total of 14 financing and acquisition deals in the digital health wearables sector, with a combined value exceeding $600 million, fully demonstrating the market’s热度.

Wearable Devices Start Strong but Fade: Lack of User Stickiness Is the Original Sin

Like any emerging technology, wearable devices initially experienced a “bubble.” Fitbit (NYSE: FIT) and Jawbone were regarded as pioneers and benchmark companies in the wearables sector. Fitbit was founded in San Francisco in March 2007. In 2009, it launched its first-generation Fitbit Tracker. The product received acclaim upon release and became widely popular across North America within less than three years. Due to strong interest from venture capital managers, U.S. venture investment in wearable devices—then primarily focused on personal health tracking—reached $150 million in 2011, including Fitbit’s $12 million Series C financing round. That same year, Aliph (founded in 1998), which had already established a presence in the Bluetooth headset market with its Jawbone product line, changed its corporate name to Jawbone and released its first fitness-tracking wristband, the Jawbone UP, designed for recording running activities.

On April 16, 2013, Google released its first wearable device—Google Glass. Coupled with the then wildly popular Fitbit Flex and Jawbone UP, 2013 marked a period of rapid growth for wearable devices—in the United States at that time, one in every five adults owned a wearable device.

Fitbit was basking in the spotlight at the time. According to NPD’s market report on fitness tracking devices for the third quarter of 2014, Fitbit’s market share had reached 69%, far surpassing Jawbone, which ranked second with a 14% share. Buoyed by such a promising market outlook, Huang Wang, founder of Huami, decided to step out of the stagnant tablet market and focus on wearable devices after touring the Consumer Electronics Show (CES). At the end of 2013, Hefei Huaheng Electronics, under Huang Wang’s leadership, jointly established Huami Technology with Xiaomi.

However, bad news gradually began to mount in that year for independent wearable device companies led by Fitbit and Jawbone. In March 2014, Google announced the Android Wear platform, designed specifically for wearable devices, prompting major Android smartphone manufacturers to enter the wearable market. On July 11, Huami (Beijing) Information Technology Co., Ltd. was officially established, and on July 22, it jointly launched the Mi Band with Xiaomi. By December 2014, Apple had also joined the fray, releasing the Apple Watch. Under immense pressure, Fitbit went public on the New York Stock Exchange on June 18, 2015, becoming the first publicly traded company in the wearable device sector. Its closing price on the day reached $29.87, a 49% surge from its $20 IPO price, pushing the company’s valuation to $6.2 billion.

However, market enthusiasm for wearable devices cooled significantly thereafter. One reason was that the functionality of wearables at the time was overly simplistic, resulting in low user stickiness. Meanwhile, although wearable devices appeared to collect substantial amounts of data, such data held limited additional value. In its NPD DisplaySearch Wearable Device Market and Forecast Report released in early 2014, Enboyuan also predicted that the wearable device market would begin to cool from 2016 onward, and would not rebound until wearables became essential items or the industry underwent consolidation.

Fitbit, the first publicly traded wearable device company, validated this prediction in early 2016. In early January, it launched its new Blaze smartwatch, and its stock price plummeted by 18% on the day of the release—clearly, investors did not believe that Fitbit’s new Blaze could compete head-on with the Apple Watch. Although Fitbit carried out multiple acquisitions in 2016 and acquired the intellectual property rights of another well-known brand, Pebble, these efforts proved futile. Fitbit’s financial report for the first quarter of 2017 showed revenue of only $299 million, a significant decline from the $550.4 million recorded in the same period of 2016. Meanwhile, Fitbit’s stock price fell by 67% compared to the same period in 2016, and its market capitalization shrank by nearly 50%.

Jawbone, once considered one of the two giants of wearable devices alongside Fitbit, is in even worse shape. Jawbone has never lacked funding; its investors have included major backers such as Sequoia Capital, Andreessen Horowitz, Khosla Ventures, Kleiner Perkins Caufield & Byers, and the Kuwait Investment Authority, securing a total of up to $951 million in investment. However, its market share has continuously hit new lows. In July 2017, Jawbone was forced into liquidation. Former CEO Hosain Rahman founded a new company called Jawbone Health Hub, Inc., and many former Jawbone employees joined this new venture.

Misguided direction may have been one of the reasons why wearable devices were stuck in a dilemma at that time. Functions such as step counting, sleep monitoring, and activity tracking have become standard features, but we have failed to see the practical significance of collecting this data. The young user group, which is the main target of wearable devices, is not interested in the collected physiological data—most of them are healthy and do not need to monitor these data all the time.

Meanwhile, the populations that truly need these data monitoring technologies, such as the elderly and patients with chronic diseases, have been intentionally or unintentionally overlooked by wearable device manufacturers. According to a 2014 study by the Pew Research Center, 45% of American adults suffer from at least one chronic disease. Among them, 40% of those with one chronic condition track their health metrics, while 62% of those with two or more chronic conditions do so. In contrast, only 19% of individuals without chronic diseases track their health metrics.

Unfortunately, the technology for wearable devices to collect vital signs such as blood pressure, blood glucose, and blood oxygen saturation remains immature. Meanwhile, medical device certification requires lengthy clinical trials and is subject to stringent regulatory oversight. Most high-profile wearable manufacturers, accustomed to making quick profits, are reluctant to invest the effort required to engage with authoritative bodies such as the FDA and HIPAA (Health Insurance Portability and Accountability Act). As a result, they have missed out on the chronic disease management market, which boasts an annual size of nearly $2 trillion.

It is not that wearable device manufacturers have overlooked these directions. In fact, VCBeat recorded a total of 73 financing and IPO events involving wearable device companies between 2015 and 2017. However, the financing amounts and scales of most of these enterprises were simply too small. As tech giants with ecosystem-building capabilities—such as Apple, Xiaomi, Huawei, and Samsung—entered the wearable device market and aggressively captured market share through coordinated, ecosystem-wide strategies, the opportunities for independent players to grow and thrive have diminished significantly. The successive setbacks of Fitbit and Jawbone are, to some extent, attributable to this factor. After all, single-branch operations cannot compare to combined arms warfare involving land, sea, and air forces.

The Power of Ecosystems: The Market Is Gradually Concentrating in the Hands of Major Players

According to the quarterly wearable device market report released by IDC in May, the wearable device market rebounded rapidly in the first quarter of 2019. Shipments for the entire quarter reached 49.6 million units, representing a 55.2% year-over-year increase. Among these, wrist-worn devices such as watches and bands grew by 31.6% year over year. These devices accounted for the absolute majority of the wearable device market, with their shipment share reaching 63.2%. Notably, ear-worn devices experienced rapid growth, surging 135.1% year over year and capturing a 34.6% share of the overall wearable device market.

In Q1 2019, the top five wearable device vendors were Apple, Xiaomi, Huawei, Samsung, and Fitbit. It is worth noting that due to differences in data sources and reporting periods, there may be discrepancies between IDC’s reports and the official financial statements released by each vendor.

Apple

Apple continues to rank first, with total shipments in Q1 increasing by 49.5% year-on-year and capturing a 25.8% market share. Throughout the quarter, Apple shipped a total of 12.8 million units, nearly double the shipment volume of Huami (Xiaomi), which ranked second. In 2018, Apple’s wearable device shipments reached 46.2 million units, slightly lower than the combined annual shipments of the top three vendors—Huami, Fitbit, and Samsung—which occupied the top five positions on the 2018 list.

The Apple Watch accounts for the majority share of Apple’s wearable device product line and is also a primary source of profit. Compared to the same quarter last year, the average selling price (ASP) of the Apple Watch has increased from $426 to $455. However, Apple’s year-over-year shipment growth rate ranked second-to-last among the top five vendors, with only a 14.8% increase in shipments. Its market share also declined from 26.8% in the same period last year to 25.8%. In Apple’s fiscal 2019 third-quarter earnings report released in late July, sales of wearable devices, led by the Apple Watch, reached $5.525 billion, representing a substantial 48% increase from the previous quarter’s revenue of $3.733 billion, making it one of the few highlights of that quarter’s financial results.

Apple has long had its sights on the healthcare market. Between 2016 and 2018, Apple acquired Gliimpse, a startup specializing in personal health data processing; Beddit, a developer of sleep monitoring devices; and Tueo Health, a software company that developed solutions for managing pediatric asthma in conjunction with respiratory sensors. In 2018, Apple launched the Health Records app and announced that the Apple Watch Series 4 had received FDA clearance.

The single-lead ECG feature of the Apple Watch Series 4 can monitor heart rhythm in the background and promptly alert users when it detects atrial fibrillation (AFib), an irregular heartbeat, thereby increasing the likelihood of early stroke screening. By the end of 2018, Apple had recruited dozens of physicians to accelerate the integration of medical and health technologies into its products. Additionally, based on historical patterns, Apple is highly likely to unveil the next-generation Apple Watch at its September fall event. There is widespread anticipation that the new device will offer enhanced capabilities, such as elevating the series’ medical monitoring functions to a higher level through more precise sensors.

AirPods, which have already disrupted the wireless earbud market, are considered another wearable device with potential medical applications. A patent held by Apple indicates that AirPods have the capability to capture biometric data such as core body temperature, heart rate, and VO2 (oxygen consumption). Previously, the United States passed the Over-the-Counter Hearing Aid Act, allowing manufacturers to sell medical-grade hearing aids directly to consumers without a physician’s prescription. This has significantly increased the likelihood of AirPods evolving into smart hearing aids.

An increasing number of third-party medical wearable startups are leveraging Apple’s iOS ecosystem to enhance user experience and engagement. Notable examples include Butterfly Network (portable ultrasound), AliveCor (multi-lead ECG), and Cellscope (iPhone otoscope). These partners have formed a value alliance with Apple in the consumer health sector, fueling Apple’s growing ambitions in the services space, particularly in healthcare payments. In the United States, approximately 5% of patients use Apple Pay for healthcare transactions, indicating substantial market potential. Recently, Apple announced that it would charge commissions on medical platforms within the App Store. Although adjustments were made under public pressure, Apple’s underlying intentions are clear to all.

Although the Apple Watch has become Apple’s lever for entering the healthcare market, it still falls far short of Tim Cook’s original vision for this sector. Some core members of Apple’s healthcare team believe that the company remains on the periphery of the healthcare industry, with progress in areas such as medical devices, telemedicine, and healthcare payment systems proceeding far too slowly. Apple’s longstanding culture of strict project confidentiality clashes fundamentally with the healthcare sector’s tradition of open dialogue and public clinical research, making the advancement of healthcare initiatives exceedingly difficult. As a result, Apple’s health team recently experienced a wave of departures, with several key employees from health-related projects resigning—a trend that may well impact Apple’s future healthcare strategy.

Huami

According to IDC statistics, Huami, ranked second, shipped 6.6 million units this quarter, representing a 68% increase from the previous quarter. Its market share reached 13.3%, a 1 percentage point increase from the prior quarter. In the wrist-worn device segment alone, Huami has become the global leader—the Mi Band shipped 5.3 million units this quarter, capturing a 10.7% share of the entire wrist-worn device market. This surpasses Apple’s shipments of 4.6 million units and its 9.3% market share. Compared with Apple’s comparable products, the Mi Band offers superior value at a lower price, making its market popularity well-deserved.

On August 19, Huami also released a strong financial report. The report showed that revenue in the second quarter reached RMB 1.0387 billion (USD 151.3 million), a year-on-year increase of 36.6%, with revenue exceeding expectations for two consecutive quarters. Total revenue for the first half of the year amounted to RMB 1.8383 billion (USD 267.8 million), representing a year-on-year growth of 36.6%. Net profit attributable to Huami Technology was RMB 164.6 million (USD 24 million), marking a significant year-on-year increase of 64.1% compared to the net profit of RMB 100.3 million recorded in the first half of 2018.

In addition to the Xiaomi Mi Band 4, which shipped over one million units in just eight days—setting a historical record for the fastest shipment rate—Huami has also strengthened its penetration into the medical field through its proprietary brand, the Amazfit Huami Health Band (Huangshan No. 1 Edition). At Huami’s 2019 New Product Launch Event held just a few days ago, the company unveiled several new wearable devices targeted at sports and health. Among them, the Amazfit Smart Sports Watch 3 features Huami Technology’s self-developed BioTracker PPG high-precision biological tracking optical sensor, which enhances the accuracy of PPG detection. It enables 24-hour daily heart rate monitoring and includes features such as high heart rate alerts and heart rate zone viewing.

Earlier, at the Summer 2019 New Product Launch in June, Huami Technology also released the Amazfit Mi Move Health Watch. This was the first wearable product in China to support ECG (electrocardiogram) monitoring. In fact, as early as January 2018, the wearable dynamic ECG recorder (in a bracelet form factor) from Anhui Huami Health Medical Co., Ltd., an affiliate of Huami Technology, had already obtained CFDA certification. In contrast, Apple has not yet received CFDA certification and is therefore unable to enable ECG recording features in the Chinese market. In 2018, Huami upgraded this product series to the 1S model, adopting the second-generation ECG analysis algorithm and AI neural networks, while adding a self-developed high-precision PPG optical sensor to improve the accuracy of heart rate monitoring.

Huami has also developed core components such as chips. The Huangshan No. 1 chip, used in the Amazfit Health Band (Huangshan No. 1 Edition) and the Amazfit Health Watch, is touted as the world’s first wearable AI chip. This chip integrates Huami’s self-developed RealBeats AI biological data engine, enabling real-time local detection of PPG-based arrhythmias (including atrial fibrillation) and ECG-based arrhythmias (including atrial fibrillation). It enhances the accuracy and efficiency of cardiac health monitoring, delivering results to users in the shortest possible time.

Not only that, but Huami also officially launched the newly upgraded Mi Health VIP service in August. Leveraging its strengths in smart wearable hardware and big data, the service covers more than ten features, including expert ECG interpretation, cardiac anomaly alerts, telephone and text/image consultations, green channels for medical care, emergency rescue assistance, and quarterly health reports, enabling users to quickly access high-quality online and offline medical and health resources. With Huami Technology’s medical and research teams now initially established, this marks the maturation of Huami’s “Chip + Device + Cloud” strategy, bringing the company one step closer to fulfilling its mission: “To empower everyone in the world with better sports, health, and medical services through the power of technology.”

Huawei

Huawei, ranking third, has demonstrated remarkably impressive growth. Its Q1 shipment volume reached 5 million units, slightly lower than that of Huami. However, its year-on-year growth rate soared to 282.2%, six times that of Apple, while its market share rose from 4.1% in the same period last year to 10% in the current quarter. In 2017, Huawei ranked only sixth; by 2018, it had surpassed Samsung to claim fourth place. In 2019, it broke into the top three with explosive growth. This becomes easier to understand when comparing smartphone market shares during the same period—Huawei’s smartphone shipments also achieved explosive, high-speed growth during this time.

It can be said that wearable devices have become increasingly important in Huawei’s health strategy. In March 2019, Huawei Device Co., Ltd. expanded its business scope to include the sales of medical devices (Class II medical devices). This move sent shockwaves through the industry, prompting media outlets and analysts to predict that Huawei would further diversify its business operations by venturing into the healthcare sector through wearable devices. In response, Huawei stated that it would focus exclusively on smart wearable devices capable of connecting with medical equipment.

As early as 2018, Huawei partnered with the Chinese PLA General Hospital (301 Hospital). Huawei collaborated with cardiovascular experts to develop specialized algorithms for arrhythmia detection using the high-performance heart rate sensors in its smart wearable devices. The aim was to screen for arrhythmia risks through continuous monitoring, thereby pioneering a new approach to large-scale population screening and management for the prevention and treatment of arrhythmias, ultimately reducing the incidence of adverse events such as stroke. This successful R&D effort eventually evolved into the TruSeen 3.0 heart rate monitoring system featured on the Huawei Watch GT smartwatch.

Samsung

With 4.3 million units shipped and an 8.7% market share this quarter, Samsung successfully overtook Fitbit to claim fourth place—having ranked fifth with a 6.8% market share in the previous quarter. Nevertheless, Samsung’s Q2 2019 financial report released recently indicates that the company is currently facing considerable challenges. Affected by weakness in its core semiconductor memory business, slowing smartphone sales, and the trade dispute between Japan and South Korea, Samsung’s revenue remained relatively stable during the quarter, but its net profit declined significantly. Net profit for Q2 amounted to KRW 5.18 trillion (approximately USD 4.4 billion). Although this figure halted the continuous downward trend and represented a slight increase from the previous quarter’s KRW 5 trillion, it marked a sharp 53% year-on-year drop compared to the KRW 11 trillion recorded in the same period last year.

Samsung has long sought to develop the medical capabilities of wearable devices. In 2014, Samsung announced the Simband, a conceptual smartwatch. Although it was merely an experimental platform, it featured a comprehensive suite of built-in sensors—including optical, thermal, and galvanic skin response sensors—capable of measuring heart rate and blood oxygen levels. In late 2015, Samsung unveiled the Bio-Processor, a sensing chip specifically designed for wearable devices. This chip integrated ECG functionality and could measure five health metrics: body fat percentage, skeletal muscle mass, heart rate, skin temperature, and stress levels. However, this chip apparently never made it into practical application; even though the Galaxy Watch Active, released by Samsung in early 2019, added numerous health monitoring features, it still lacked ECG functionality. It was not until a few days ago that Samsung launched the Galaxy Watch Active 2, which includes ECG capability. However, this feature is not yet activated and is reportedly scheduled to be enabled in 2020.

Samsung also offers the Galaxy Gear VR, a wearable virtual reality (VR) headset. Although VR has primarily been used for entertainment to date, it holds significant potential in the healthcare sector. In March 2018, Samsung, Travelers Partners Insurance, Cedars-Sinai Medical Center, Bayer, and appliedVR jointly conducted a study on the use of VR for pain relief. The study utilized wearable devices and VR-assisted therapy to distract patients, thereby alleviating acute orthopedic and limb pain, reducing the risk of opioid addiction, and lowering healthcare costs.

Fitbit

Fitbit, once the leader in the wearable device market, continues to see its market share decline. In this quarter, Fitbit’s shipments reached 2.9 million units, a year-on-year increase of 35.7%. Although Fitbit’s growth rate is not slow, its competitors have grown even faster, causing it to be overtaken by Samsung and drop to fifth place.

Medical applications emerged as a highlight in Fitbit’s Q2 financial report, released in late July. The report showed that Fitbit generated $313.6 million in sales revenue in Q2, with a net loss of $68.5 million, effectively halting its downward trend. The medical solutions segment contributed significantly to this performance, with revenue increasing by 16% year-over-year. Fitbit forecasts that the medical solutions segment could achieve approximately $100 million in annual sales revenue. If this target is met, this division, established in 2016, will account for at least 30% of Fitbit’s total sales revenue.

Fitbit’s continued decline is certainly attributable to its own products, but the fact that the top four vendors are all smartphone giants with ecosystem-building capabilities also indicates that brands like Fitbit and Jawbone, which lack a full-industry-chain ecosystem and rely solely on wearable devices, will face significant competition and challenges in future market competition.

Fitbit has clearly long recognized these disadvantages and has sought to address such shortcomings through external collaborations. In 2017, Fitbit launched a health partnership program with Solera Health, allowing patients with type 2 diabetes enrolled in the program to redeem points earned via their Fitbit devices throughout the course of the initiative. This program was designed to encourage these patients to increase their physical activity and enhance weight-loss outcomes. In 2018, Fitbit replicated this model in partnerships with other companies, enabling users to earn points based on steps taken, activity duration, and sleep quality, which could then be redeemed for products or services offered by partner companies such as Adidas, Blue Apron, and Deezer.

Furthermore, as early as September 2017, Fitbit successfully joined the FDA’s newly launched Pre-Cert Pilot Program for digital health products. In the first quarter of 2018, Fitbit acquired Twine Health, a collaborative care management platform, and shortly thereafter launched Fitbit Care, a service incorporating health coaching and virtual care. This service helps users achieve their health goals and manage chronic conditions such as diabetes, depression, and COPD through collaboration with health coaches via telephone and in-person sessions. Fitbit also partnered with the National Institutes of Health (NIH) to launch the All of Us Research Program, which aims to collect health data from one million Americans to accelerate and improve research in precision medicine.

Through these initiatives, Fitbit aims to expand beyond wearable hardware by integrating software and services into the healthcare ecosystem, thereby establishing a sustainable, context-driven revenue model.

Nine Major Application Scenarios: Wearable Devices Empowering Healthcare

What are the potential applications of wearable devices in the medical field? We believe that wearable devices can directly empower the following nine application scenarios: exercise monitoring, disease prevention, early intervention, definitive diagnosis, continuous monitoring, assisted diagnosis and treatment, personalized therapy, efficacy evaluation, and chronic disease management. We will elaborate on each of these below.

Activity Monitoring: It is evident from the development trajectory of wearable devices that activity monitoring was one of the earliest selling points to gain consumer favor. Fitbit and Jawbone achieved rapid growth precisely by leveraging this feature. The implementation of activity monitoring is straightforward, as the required sensors—such as three-axis gyroscopes, accelerometers, and distance and heart rate sensors—are already highly mature. Consequently, nearly all wrist-worn wearable devices are equipped with activity monitoring capabilities. There is little more to be said about this technology, as it has essentially become a standard feature for wrist-worn wearables.

Disease Prevention: The mature micro-sensor technology and information processing and storage technologies employed by wearable devices enable accurate and precise collection of various user data. On this basis, it becomes possible to prevent specific diseases by monitoring one or more physiological signals, analyzing them, and making predictive judgments. In addition to the common observation of vital signs such as electrocardiogram (ECG), blood pressure, and temperature, the latest technologies can also utilize sweat for detection. Furthermore, wearable smart glasses can monitor the retina to help prevent diseases such as diabetes.

Early Intervention: Building upon disease prevention, this approach incorporates remote connectivity features. By uploading monitored key vital signs to the cloud and having professional medical personnel analyze the data, a comprehensive understanding of the user’s health status can be achieved. In emergency situations, notifying medical professionals for early intervention maximizes the utility of data collected by wearable devices. An increasing number of healthcare institutions are adopting wearable devices to provide more comprehensive out-of-hospital physical monitoring services. Users can even communicate directly with healthcare institutions and medical staff through these wearables. This functionality requires highly accurate data acquisition; currently, ECG-based electrocardiogram monitoring is the most common method.

Definitive Diagnosis: At times, a single examination is insufficient to establish a definitive diagnosis of a condition, necessitating prolonged, uninterrupted monitoring and observation. Historically, this could only be achieved through inpatient hospitalization. Even then, due to inherent limitations, the monitoring results were not always consistently accurate. Wearable devices, which can be worn close to the body and continuously collect user signals, largely address this challenge. A detailed temperature variation curve, a set of precise motion amplitude data, or an accurate, continuous electrocardiogram (ECG) can all play a significant role in facilitating a definitive clinical diagnosis.

Continuous Monitoring: During the course of treatment and rehabilitation, diseases may recur. Wearable devices can continuously track and monitor health signals, enabling patients and healthcare institutions to keep abreast of the patient’s condition in real time. This approach offers a far more comprehensive overview than the intermittent, sampling-based vital sign collection methods used in the past.

Assisted Diagnosis and Treatment: Wearable devices are not only beneficial to patients but also assist physicians in collecting and transmitting various types of information, serving as instrumental tools in clinical practice. For instance, smart glasses equipped with augmented reality (AR) capabilities can not only enhance medical education but also improve the accuracy, convenience, and safety of clinical procedures. Finger sleeves with monitoring functions can further facilitate physicians’ operational efficiency.

Personalized Diagnosis and Treatment: Unlike traditional therapeutic devices, wearable devices allow users to adjust settings in real time based on their individual conditions while ensuring safety, thereby achieving optimal therapeutic outcomes. Currently, well-established applications include pain relief, insulin delivery, and assistance with motor rehabilitation using wearable devices.

Evaluating Therapeutic Efficacy: Previously, the assessment of patient recovery relied on subjective evaluations and descriptions by both physicians and patients, lacking intuitive and convenient quantitative objective measures. The emergence of wearable devices has filled this gap by visually presenting previously difficult-to-assess conditions through collected data. Quantifiable assessment data not only enables patients to gain a clearer understanding of their condition but also allows physicians to comprehensively monitor recovery progress, facilitating timely adjustments to treatment plans and the formulation of more personalized rehabilitation strategies. For instance, wearable knee braces, ankle supports, insoles, and chest garments can be used to detect changes in patients' range of motion, thereby assessing their rehabilitation status.

Chronic Disease Management: In the past, patients faced numerous inconveniences in managing their chronic conditions outside of hospital settings. Unobtrusive and silent wearable devices, serving as key enablers of health, allow users to monitor changes in their chronic diseases more effectively and safely, significantly improving their quality of life. Wearable cardioverter-defibrillators and wearable insulin pumps are already relatively mature medical wearable technologies.

These devices have obtained medical certification.

In the medical field, both CFDA and FDA approvals are of paramount importance. So, which devices have currently obtained CFDA or FDA approval, and what are their primary areas of focus?

CFDA Certification

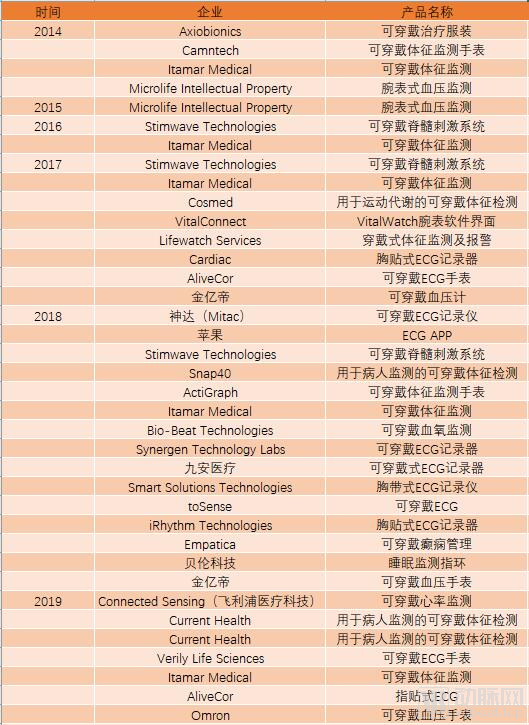

A search on the official website of the China Food and Drug Administration (CFDA) using keywords such as “wearable,” “ECG,” “wrist blood pressure,” and “arm blood pressure,” while excluding cases of certification renewal upon expiration, identified products from certain companies that have obtained CFDA certification. Nevertheless, the list may be incomplete because many companies’ products do not include the aforementioned keywords in their names or are produced under private-label arrangements (we welcome any corrections regarding omissions). With the exception of one sleep apnea monitor from Itamar Medical, all devices are domestically manufactured in China. The vast majority of these devices are used for electrocardiogram (ECG) recording and blood pressure monitoring, indicating that these two functions remain among the primary medical applications of wearable devices at present.

In addition to the well-known Huami Technology, Shenzhen Kingyield Technology Co., Ltd. is particularly noteworthy. Established in 2005, the company holds a total of 16 certifications from the China Food and Drug Administration (CFDA). Within the past five years, as many as six wearable devices have received certification, all of which are wearable electronic blood pressure monitors. As a major original equipment manufacturer (OEM) for wearable electronic blood pressure monitors, it is evident from their design and functionality that multiple brands of wearable smart electronic blood pressure monitors available on the market are OEM products manufactured by this company.

Additionally, THOTH (Suzhou) Medical Technology Co., Ltd. deserves mention. From 2017 to 2018, the company consecutively obtained CFDA certification for five wearable products, accounting for half of all medically certified wearable devices approved by the CFDA to date. Established in 2016 and focused on the R&D of flexible wearable medical devices, THOTH completed its Series B financing in April 2018, raising RMB 10 million. Its current product portfolio includes wearable dynamic ECG recorders, wearable continuous temperature monitors, and wearable fetal ECG monitors. Although its products exhibit a high level of maturity and have been deployed in numerous hospitals and schools, they still lag behind mainstream smart wearable devices in terms of integration, portability, and industrial design. The current form factor—requiring replaceable chest electrodes paired with a wireless transmitter—is unlikely to achieve widespread adoption.

FDA Certification

What about the FDA? We searched the FDA database using “wearable” as a keyword, and then added supplementary keywords such as “watch,” “eye glass,” and “ECG” to prevent omissions due to variations in product descriptions and definitions. Subsequently, we conducted another search using mainstream wearable device brands as keywords, including “Fitbit,” “Jawbone,” “Apple,” “Huami,” “Xiaomi,” and “Huawei.” In total, 34 wearable devices approved by the FDA between 2014 and 2019 were recorded. While some products may still have been missed, the data collected is believed to be relatively comprehensive. Similar to CFDA certifications, vital sign monitoring accounted for an absolute majority, reflecting the current reality that the medical application of wearable devices is predominantly concentrated in this area.

Itamar Medical, a company from Israel, is considered a relatively active manufacturer, with new products gaining certification almost every year; its most recent certification was obtained in 2019. Founded in 1997, the company went public in 2012 (OTCPINK: ITMMF). It has been dedicated to researching and developing non-invasive medical devices for diagnosing various diseases, including cardiovascular and respiratory conditions. The WatchPat series is its flagship product line. These devices are primarily used to continuously measure and monitor vital signs while the user sleeps, employing a measurement setup consisting of a wristband, finger probe, chest patch, and wired connection. However, the WatchPat One, which received certification in 2019, features a significantly reduced form factor compared to previous models. If the company can continue to miniaturize its products and introduce wireless connectivity in the future, there will be substantial room for growth and innovation.

Based on CFDA and FDA certifications, currently certified wearable devices are primarily used for vital signs monitoring, with ECG accounting for the vast majority. The certified brands are mostly specialized medical device manufacturers of relatively small scale, whose product design lags significantly behind mainstream wearables, making it unlikely for them to create major market disruptions in the future. Even if individual startups develop disruptive medical applications, they are likely to be acquired by major industry players. As for the giants in the medical device sector, they appear to lack immediate interest in this market, with no noteworthy products to date. However, as technology matures, these medical device giants may become more active in this space in the future.

The Battle for the Data Gateway of Wearable Devices

As a rapidly growing emerging technological field, the development of novel wearable medical devices is of significant importance. As China gradually transitions into an aging society, the population suffering from chronic diseases continues to expand and shows a trend toward affecting younger individuals. Consequently, public health concepts are shifting from passive treatment to active monitoring and prevention. Wearable devices can detect potential risks at an early stage and enable timely intervention to prevent disease onset. According to forecasts, the domestic market size for medical wearable devices was expected to exceed RMB 12.2 billion in 2020.

Although current wearable devices offer relatively limited medical functionalities, their significance as a critical data entry point is undeniable. As wearable monitoring becomes increasingly precise and captures a growing array of physiological signals—expanding from basic metrics such as body temperature, heart rate, blood pressure, and respiratory rate to more advanced indicators like blood glucose, electrocardiogram (ECG), electroencephalogram (EEG), and blood oxygen saturation—the integration of cloud computing and artificial intelligence (AI) enables these massive volumes of health data to drive a qualitative transformation. This shift opens new avenues for exploring innovative approaches to disease prevention and treatment.

For this very reason, this data entry point is poised to become a fiercely contested strategic battleground in the future. As early as May 2015, the State Council issued the “Made in China 2025” initiative, elevating the development of medical-grade wearable devices to a strategic priority and calling for enhanced innovation capabilities and industrialization levels. Given that the wearable medical device sector is still in its nascent stages, advancing smart wearable medical devices will help bolster China’s competitiveness in the global medical device market, potentially enabling it to achieve leapfrog development.

In fact, Chinese-made wearable devices have experienced rapid growth in recent years. Huami and Huawei have broken into the top three in the global wearable device market, with a particularly strong upward trajectory. Huawei, which has long been internationalized, needs no further introduction. By the end of 2018, Huami had entered more than 60 countries and regions worldwide, including the United States, Japan, and Germany. In the first half of this year, overseas shipments accounted for over 50% of Huami Technology’s total volume for the first time, reaching 51.3%. Similar to smartphones, Chinese brands are poised to become a major force in the wearable device sector in the future.

References:

IDC:Worldwide Quarterly Wearable Device Tracker 1Q 2019

VCBeat: Nine Application Scenarios of Wearable Devices in the Medical and Health Sector

PwC: Health Wearables: Early Days

Wired: Wearable Devices Overlook the People Who Need Them Most

Iyiou: Market Research on Wearable Medical Devices