Trust Mutual Life Insurance: China's Pioneer Mutual Insurer Backed by Ant Group

The purposes and characteristics of mutual organizations are typically twofold:

First, this is your company;

Second, we jointly fulfill the mission of helping people.

In May 2014, the former China Insurance Regulatory Commission (CIRC) released the Interim Measures for the Administration of Mutual Insurance Organizations (Draft for Comments). Upon seeing the news, Yang Fan, then Executive Director and President of a certain pension insurance company limited by shares, was immediately intrigued.

“Abroad, the mutual insurance model is already highly mature.” Yang Fan, who entered the industry in 1992, has closely followed innovations brought by the internet to the insurance sector alongside the rise of the digital age. During his tenure as General Manager of Taiping Pension Insurance Company, the company pioneered a partnership with Qunar.com to launch aviation accident insurance. In 2014, while serving as President of Taikang Pension, he introduced the O2O-model “Health Appointment” critical illness insurance...

After numerous innovations, Yang Fan still felt that something was missing. “The defining characteristics of the internet era are high transparency, real-time capabilities, and highly symmetric information with rapid dissemination.” In his view, these traits aligned well with the nature of mutual insurance. Consequently, he resigned in 2015 to assemble a team and establish a mutual life insurance organization—Trust Mutual Life Insurance Company.

After preparing materials, communicating with investors, establishing and validating the business model, and forming the core team, more than a year later, on June 22, 2016, the former China Insurance Regulatory Commission (CIRC) officially approved the preparatory establishment of Trust Mutual. In May 2017, China’s first mutual life insurance organization—Trust Mutual Life Insurance Company (hereinafter referred to as “Trust Mutual”)—officially commenced operations.

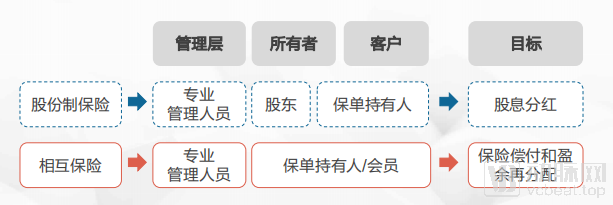

Mutual insurance organizations are owned by all members and provide insurance services to members through mutual cooperation. Unlike the "capital-based" joint-stock system, where voting at shareholders' meetings is conducted based on shareholdings, the mutual system is "person-based," with voting at the general meeting of members (or their representatives) conducted on a one-member-one-vote basis.

Differences Between Mutual and Stock Corporate Structures (Source: Provided by the Company)

The business philosophy of mutual insurance organizations, characterized by joint ownership, participatory management, and shared surplus among members, inherently leads these entities to prioritize member services, face lower moral hazard, focus more on long-term interests, and demonstrate greater resilience against external shocks.

According to statistics from the International Cooperative and Mutual Insurance Federation (ICMIF), mutual insurance demonstrated strong risk resilience and competitive vitality during the 2008 financial crisis, with its market share increasing from 23.4% in 2007 to 26.7% in 2017.

Mutual insurance refers to an economic activity in which policyholders with identical risk protection needs, on the basis of equality, voluntariness, and democratic management, procure insurance for themselves with the aim of mutual assistance and shared risk pooling. This insurance model is well-established abroad, as exemplified by State Farm, New York Life, and Northwestern Mutual in the United States, as well as Nippon Life and Meiji Yasuda Life in Japan. Kaiser Permanente, a renowned U.S. healthcare organization, is also a similar non-profit entity. According to data from Swiss Re’s sigma Report No. 4/1999, “Mutual Insurance Companies: Facing the Challenge of Full Demutualization,” 21 of the top 50 insurance companies ranked in 1997 were mutual insurance companies.

In China, due to historical reasons, mutual insurance officially launched in 2016. As the first batch of mutual insurance organizations, Zhonghui Property Mutual Insurance Cooperative, Trust Mutual Life Insurance Company, and Huiyou Construction Engineering Mutual Insurance Cooperative were successively approved to commence operations. Among them, Trust Mutual is the only institution specializing in life insurance and also one of the first entities to operate under market-oriented rules.

A close examination of the investors in Trust Mutual Life Insurance Company reveals the strength of its backing. Ant Financial, as the largest investor and member entity, holds a 34.5% stake, followed by Tianhong Asset Management with 24.0%. Other investors include nine institutions such as Guojin Dingxing, Chengdu Jiachen, and By-Health.

However, they are not shareholders but long-term creditors. In accordance with regulatory requirements, all capital contributors cannot receive operating surpluses from Trust Mutual Life Insurance Company; instead, they are entitled only to certain interest income based on their contributions. The true owners of Trust Mutual Life Insurance Company are all holders of long-term insurance policies (with a term of more than one year)—i.e., the members. Members of Trust Mutual Life Insurance Company possess rights similar to those of shareholders, including voting rights, election rights, and rights to surplus distribution.

Individuals purchasing products with a term of more than one year are classified as members, while those purchasing short-term products are classified as customers. This approach enables Trust Mutual Life Insurance Company to cater to the needs of the “three-highs” demographic—characterized by high quality, high income, and high educational background—while also meeting the demands of the young internet-savvy consumer segment. As of June 30, 2019, Trust Mutual’s gross written premiums reached RMB 1.635 billion, with 41,134 members and 34.98 million customers.

Behind such achievements lies a wealth of innovation by Trust Mutual Life Insurance Company:

First, Cloud-Based Core Life Insurance System

During its establishment phase, Trust Mutual Life Insurance Company built all its systems on the cloud. By leveraging Ant Financial Cloud, the company eliminated the need for traditional data centers and a large operations and maintenance team, significantly reducing IT operational costs and saving up to tens of millions of yuan annually. Furthermore, its core cloud-based system was developed under the leadership of Trust Mutual’s in-house team and is protected by intellectual property rights.

Second, the Compassionate Aid Account

Approved by the Member Representative Assembly of Trust Mutual, a Compassionate Relief Fund has been established for all members. The fund is financed by allocating a certain percentage of premiums from Trust Mutual’s operational expenses (and may also accept donations from members). In the event that members suffer from major disasters, accidents, or serious illnesses and continue to face financial hardship despite active self-rescue efforts, the Compassionate Relief Fund will provide consolation and assistance to the members, their spouses, and minor children.

It is understood that Trust Mutual Life Insurance Company has established two funds: the Love Relief Fund and the CUFE-Trust Love Relief Fund, which was jointly established in collaboration with alumni of the Central University of Finance and Economics. Both funds are committed to fulfilling their responsibility of assisting members.

Yang Fan cited an example: if a child’s parents both pass away, but the compensation is insufficient and the family faces financial hardship, Trust Mutual Life Insurance Company can utilize this fund to support the minor until they reach the age of 18. During this period, in addition to the fund’s own resources, members may also initiate donations.

Third, the Claims Review Panel Mechanism

To effectively resolve long-standing claims disputes between insurance institutions and consumers, Trust Mutual Life Insurance Company partnered with Ant Financial to pioneer the “Claims Review Panel” mechanism in the industry. In the event of a dispute over an insurance claim, the claimant may file an application, and a “Claims Review Panel,” composed of Trust Mutual’s members and customers of specific products, will determine whether the claim should be paid.

Fourth, Blockchain Business

Trust Mutual Life Insurance Company has placed certain insurance user and policy-related data, as well as charitable assistance accounts, on the blockchain. Yang Fan stated that the life insurance industry is highly specialized; life insurance data must be retained over an individual’s entire lifespan, during which substantial data iterations occur due to changes in personal and family information. Consequently, its data storage requirements are even more stringent than those of the banking sector.

“Attention to the pediatric segment within the insurance industry is insufficient, resulting in inadequate coverage for children,” said Yang Fan. “Children aged 1 to 3 are the group most susceptible to illness.”

Consequently, in July 2017, Trust Mutual Life Insurance Company launched the “Baby Guardian Plan” on Alipay. By June 2019, the plan had provided coverage for over 20 million children. Claims data from the Baby Guardian Plan revealed a high incidence of leukemia among children, prompting Trust Mutual to introduce the “Love My Baby” Pediatric Leukemia Critical Illness Insurance in March 2018.

Yang Fan told reporters that Trust Mutual Life Insurance Company offers not just an insurance policy, but a comprehensive service ecosystem. Taking children as an example, those in third- and fourth-tier cities or remote mountainous areas can access scarce medical resources in addition to receiving claim payouts when they fall ill. Trust Mutual has partnered with several pediatric healthcare institutions to provide services such as online pediatric consultations and expedited access to medical care.

From the perspective of the overall development trends in the insurance industry, Yang Fan divides its evolution into four stages. Stage 1.0 relies on manpower, selling insurance through traditional channels such as agents, counters, and banks. Stage 2.0 largely depends on internet and technological means to improve sales efficiency. Stage 3.0 involves fully online operations enabled by obtaining an internet insurance license, as exemplified by ZhongAn Insurance. Stage 4.0 represents insurance companies that build upon the internet foundation while incorporating natural attributes such as social connectivity.

“Our model is actually at the 4.0 stage, with our organizational structure and systems designed according to the 4.0 framework; however, the current market and policy environment has not yet reached this phase,” said Yang Fan. “Therefore, while continuously building our strength and refining Trust Mutual’s comprehensive service system, we are actively exploring social attributes and collaborating innovatively with partners who share our values, striving to achieve co-creation, co-construction, consultation, and win-win outcomes, thereby forging a new path.”

In terms of future planning, Trust Mutual Life Insurance Company will focus more on patients with special diseases and chronic conditions, deeply integrating insurance with pharmaceuticals.