Capital Insights from 5,000 Enterprises Reveal the Present and Future of 12 Medical Subsectors

Capital infusion is critical to startups and emerging industries. VCBeat (WeChat ID: vcbeat) believes that as we walk alongside the healthcare innovation industry, it is necessary to conduct a review to better clarify the path ahead.

To date, the VCBeat database has recorded nearly 25,000 domestic and international investment and financing events, covering 39,000 projects. These data points are far more than mere bytes stored on servers or simple query tools for entrepreneurs and investors; they constitute the most authentic and objective record of past developments, offering a robust logical synthesis of trends and serving as compelling evidence for gauging market sentiment and direction.

We reviewed 5,000 domestic companies in the primary market with financing records in the VCBeat database (excluding listed healthcare companies), selected those that publicly disclosed their financing rounds and amounts, and conducted statistical analysis on investment and financing events across five major healthcare sectors based on nearly a decade of financing activities from 2010 to July 2019. If a company’s core business spanned multiple sectors, it was counted in each relevant sector.

Including:

I. Pharmaceuticals and Medical Devices: Pharmaceuticals, Medical Devices

II. Biotechnology

III. Service Innovation: Internet Healthcare, Pharmaceutical Retail, and Financial Services

IV. Digital Innovation: Healthcare Informatics, Artificial Intelligence and Big Data, and Smart Devices

V. Service Settings: Private Healthcare, Rehabilitation and Elderly Care, Third-Party Medical Services

We spent over half a month cleaning, modeling, and analyzing these data. Drawing on the industry observation methodologies we have refined over the past five years through the production of 23 million original articles, we have compiled this report. Although constrained by limited length, restricted data dimensions, and the inherent boundaries of our industry understanding, we have strived to uncover the underlying patterns across 12 sub-sectors within five major domains. This article aims to help readers cut through the noise and quickly gain insights into the historical trajectory, current landscape, and future outlook of each sub-sector.

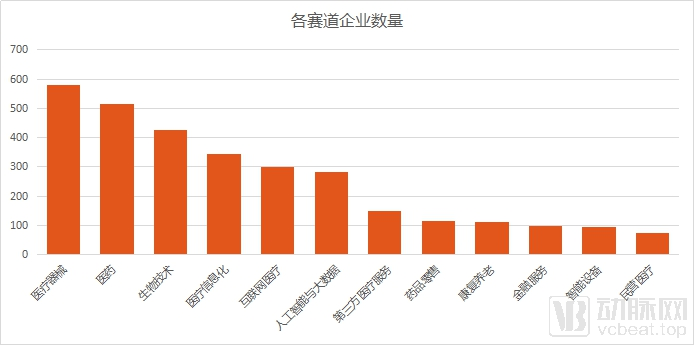

Distribution of Companies Across Various Sectors, Chart by VCBeat

Our statistics reveal that the medical devices, pharmaceuticals, and biotechnology sectors are the most “crowded.” The core of healthcare lies in the diagnosis and treatment of diseases, with medical devices and drugs serving as the essential “tools” for these purposes. They represent the most direct means of accomplishing this task and can be regarded as the “essential demand” of the entire healthcare industry. Therefore, it is only natural that the pharmaceutical and medical device sectors have attracted a large number of companies.

The bio-industry is a strategic emerging industry designated by the state. National planning proposes the establishment of a new biomedical system, aiming to achieve sales revenue of RMB 4.5 trillion in the pharmaceutical industry by 2020. It also aims to enhance the development level of biomedical engineering, with the annual output value of the biomedical engineering industry reaching RMB 600 billion by 2020. With broad market prospects, coupled with policy incentives and talent acquisition, a large number of biotechnology enterprises have been established and gained favor from capital investors.

The private healthcare sector has the fewest financed enterprises. Private hospitals require substantial capital investment, have long return cycles, and exhibit clear trends toward specialization, groupization, and chain operations. Consequently, although the number of private hospitals has surpassed that of public hospitals, relatively few companies in this segment have secured financing. Intelligent devices rarely involve core medical applications, and R&D and promotion in the consumer-facing (2C) segment are also resource-intensive, resulting in low investor interest. Meanwhile, the financial services sector remains limited in scale due to the low overall share of commercial insurance payments in China.

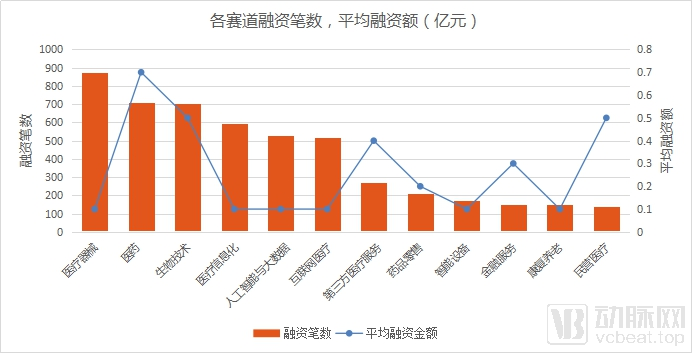

Number of Financing Rounds and Average Financing Amount by Sector, Chart by VCBeat

In terms of the number of financing events, medical devices, pharmaceuticals, and biotechnology have been the most active sectors. The number of financing deals is directly correlated with the number of companies in each sector; the more companies within a sector, the higher the number of financing events. However, the average financing amount across different sectors follows distinct patterns.

As shown in the chart above, the average financing amount for most sectors is below RMB 30 million, with pharmaceuticals, biotechnology, and private healthcare being the highest. Both the pharmaceutical and biotechnology sectors require substantial R&D investment, characterized by long development cycles and a certain risk of failure, which further increases corporate R&D costs. The average financing amount in the private healthcare sector is also relatively high. As previously mentioned, private hospitals incur high costs, requiring significant capital for expenses such as facility rent, medical equipment, recruitment of high-end talent, marketing and promotion, and chain expansion.

Next, we will explore the future of the industry by analyzing investment and financing trends across various sectors and each specific track.

The pharmaceutical and medical device sector experienced rapid growth in 2015–2016, attracting more investors, with more frequent financing events and a steadily rising total amount of funding. Prior to this period, the sector faced several pain points: 1. Low level of drug innovation. 2. Low proportion of domestically produced medical devices. 3. Lengthy review and approval cycles for drugs and medical devices, which reduced the remaining patent term available after new drugs were approved and launched on the market.

In 2015, the State Council issued the Opinions on Reforming the Review and Approval System for Drugs and Medical Devices, officially ushering in a new era of reform in this area. From that year onward, the pace of reform in the review and approval of drugs and medical devices accelerated. In 2017, the issuance of the Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices further emphasized incentives for innovation.

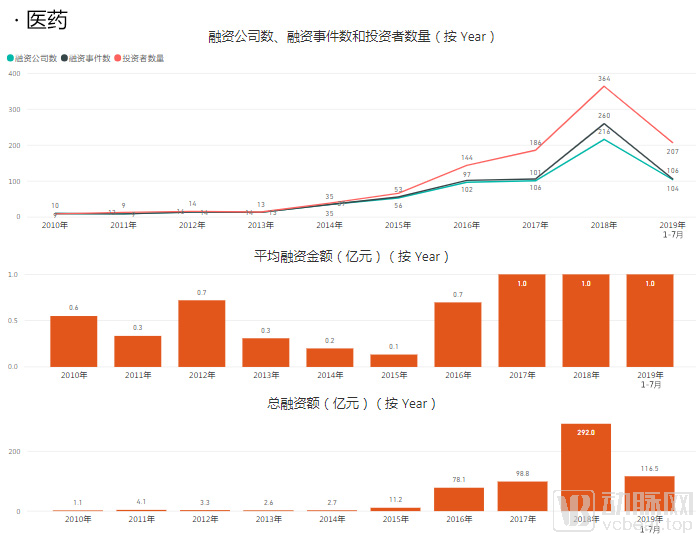

Trends in Financing within the Healthcare Sector, Chart by VCBeat

The pharmaceutical sector gradually gained momentum in 2014, entered a boom phase in 2016, and saw a surge in the number of funded companies, financing deals, and investors, with total financing volume increasing several-fold, peaking in 2018.

Since 2012, a wave of global patent expirations for branded drugs has occurred, with numerous blockbuster patented medicines from multinational pharmaceutical companies continuing to lose exclusivity in the subsequent years. This trend presents a significant opportunity for China’s domestic pharmaceutical industry, which is predominantly focused on generic drugs. On one hand, Chinese pharmaceutical companies have engaged in the research and development of generics and follow-on innovations for a batch of off-patent drugs with high clinical usage. On the other hand, the government has continuously encouraged the development of innovative drugs, leading to the establishment of a number of enterprises primarily dedicated to new drug R&D.

In 2015, the comprehensive reform of drug and medical device review and approval was officially launched. The accelerated pace of these reforms bolstered capital market confidence in the pharmaceutical sector, leading to a surge in financing activities in 2016.

Within two years following the reforms to the review and approval system for drugs and medical devices, a batch of innovative drugs received priority market approval, essentially resolving the backlog in drug evaluations and stimulating the establishment of more pharmaceutical companies. Coupled with the need for additional capital infusion by a cohort of new drug R&D enterprises established in the early stages, the healthcare sector witnessed a peak in financing activity in 2018. Brii Biosciences, founded in 2018, secured $260 million in Series A financing at its inception, which was designated for the development of infectious disease therapeutics.

Among other companies that have secured substantial financing, I-Mab Biopharma focuses on the research and development of innovative biologics in the fields of oncology immunology and autoimmune diseases. Its pipeline in China includes four core candidate drugs, which are expected to be launched sequentially starting in 2021. Henlius adopts a product development strategy combining biosimilars with innovation, starting with biosimilars and gradually developing innovative monoclonal antibody products. The company’s first blockbuster product, Hanlikang® (rituximab), has received marketing approval from the National Medical Products Administration (NMPA), becoming the first domestically produced biosimilar to be approved for market launch. The sequential approval and launch of a batch of pharmaceutical products indicate that the pharmaceutical sector is entering a period of harvest for its R&D achievements.

During this period, key innovative pharmaceutical companies such as Beta Pharma and Innovent Biologics were established, successfully launched blockbuster innovative drugs, and ultimately went public on the secondary market through initial public offerings (IPOs).

Based on the financing data from the first seven months of this year, the total financing amount and the number of financed companies are expected to decline slightly, while the number of investors will not decrease. In the future, the volume-based procurement (VBP) policy for drugs will increase the market concentration of generic drug manufacturers and pharmaceutical distributors, while innovative drugs will continue to receive policy support.

Currently, national incentives for innovative drugs have extended from the approval stage to the market ramp-up phase. For instance, the National Reimbursement Drug List (NRDL) announced this year initially identified 128 drugs eligible for negotiation-based inclusion, many of which are new drugs approved by the National Medical Products Administration (NMPA) in recent years, including major domestic innovations. Upon successful negotiation, these newly included drugs can rapidly achieve significant market uptake. It is expected that investment enthusiasm for innovative drugs will remain strong in the future.

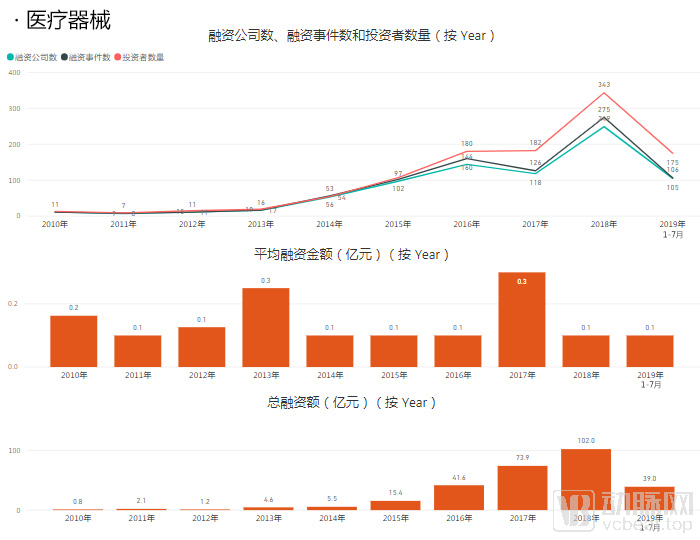

Financing Trends in the Medical Device Sector

As can be seen from the chart above, the medical device sector gradually entered a growth phase from 2013 to 2014. At that time, the industry was facing opportunities for import substitution. On one hand, imported medical devices, especially high-end equipment, came with high prices and service fees, leading to elevated healthcare costs, making localization an inevitable trend. On the other hand, years of upgrading in domestic manufacturing capabilities allowed Chinese-made devices to capture significant market share in low-value consumables such as syringes and blood collection tubes, as well as in certain repair consumable markets, laying the foundation for the industry’s breakthrough from the mid-to-low-end market into the high-end segment.

Breaking into the high-end market: Independent innovation is a key pathway. Since 2013, the Chinese government has continuously increased its support for innovation in domestically produced medical devices. In 2014, following the implementation of the Special Approval Procedure for Innovative Medical Devices, the number of products entering this special approval channel has grown steadily each year. Bolstered by internal and external advantages—including industrial foundation, market demand, and policy support—the medical device industry has also become a focal point for capital market investment.

In the following years, low- and mid-end medical devices rapidly expanded in county-level markets, benefiting from the implementation of the tiered diagnosis and treatment policy. The accelerated review and approval process for innovative medical devices encouraged domestic companies to increase their R&D investment in innovation, thereby stimulating more enterprises to enter the field of innovative medical devices. In 2017, the “13th Five-Year” Special Plan for Health and Medical Science and Technology Innovation reiterated the priority development of medical imaging equipment, medical robots, novel implantable devices, new biomedical materials, and in vitro diagnostic technologies and products. During this period, although the number of financing events declined slightly, the total financing amount continued to rise, driven by higher average financing amounts due to the high costs associated with innovative R&D.

A review of companies that have secured substantial financing reveals the following: United Imaging Healthcare independently develops and manufactures high-end medical products covering the entire spectrum of diagnostic imaging and therapy, while providing innovative healthcare IT solutions. The company is progressively establishing a global R&D, manufacturing, marketing, and service network, and raised RMB 3.333 billion in its Series A funding round in 2017. Ankon Technologies’ magnetically controlled capsule gastroscope robot has obtained Class III medical device registration certification, holds nearly 100 domestic and international technical patents, and its products have been adopted by numerous medical institutions in China, with gradual expansion into overseas markets. New Horizon Health leverages innovative biotechnology to develop early screening technologies for colorectal cancer and lung cancer, and has currently launched a series of home-based early screening products for colorectal cancer.

It must be acknowledged that the medical device sector has witnessed rapid development over the past decade. Based on financing data from the first seven months, the number of financing deals and participating investment firms in the medical device track this year may remain on par with last year; however, the total financing amount is likely to experience a certain decline.

In the future, import substitution in niche sectors such as high-end medical equipment, high-value consumables, and in vitro diagnostics will continue, while the R&D capabilities for independently innovated medical devices will steadily improve. The shortage of equipment in primary healthcare institutions still needs to be further addressed through new deployments or upgrades, thereby driving greater penetration of mid- to low-end devices. With the aging population and heightened public awareness of health management, simple and easy-to-use home medical devices will present more opportunities. Furthermore, with the rise of third-party medical services, medical device companies are expanding their industrial scope and may evolve into integrated entities offering both medical devices and third-party medical services.

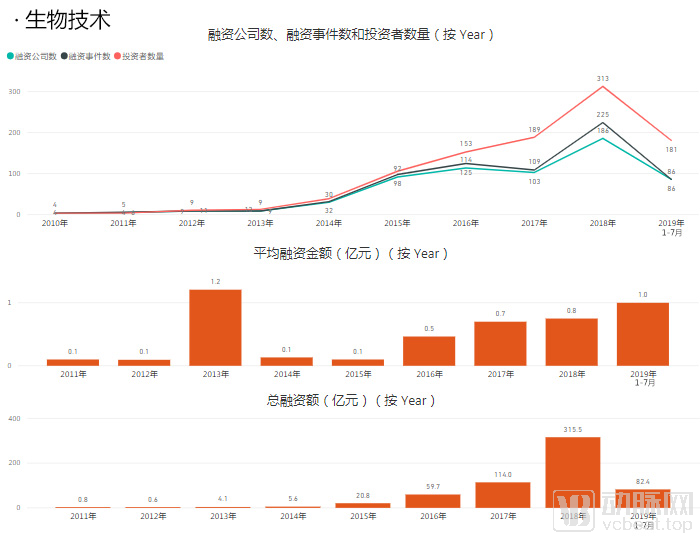

Biotech Sector Financing Trends, Chart by VCBeat

In terms of financing, the biotechnology sector began to gradually gain momentum in 2014 and entered a period of rapid growth in 2015. As early as 2012, the Chinese government designated the bioindustry as a strategic emerging industry. With a large number of highly skilled professionals returning to China to start businesses, a wave of biotechnology companies focused on medical applications was established. Encouraged by policies supporting innovation, the capital market has maintained strong interest in biotechnology, with enthusiasm continuing to rise in the subsequent years.

Biotechnology is widely applicable in the medical field, with multiple subsectors receiving key support from national industrial planning. These include modern biological therapies such as immunotherapy and gene therapy; stem cells, biomedical materials, and regenerative medicine; molecular subtyping of major diseases and precision medicine; next-generation clinical omics technologies such as gene sequencing, along with bio-big data cloud computing and biomedical analytics; development of major biological products including novel vaccines and antibodies; drug design and new drug R&D; and biomedical engineering and medical devices.

Among biotechnology companies that have secured substantial financing, Mingma Bio is an integrated platform for genetic R&D applications and genetic big data empowerment, leveraging precision medicine big data to improve human health. It has launched products such as preconception carrier screening for genetic diseases and newborn genetic screening. Ascentage Pharma is dedicated to developing innovative drugs in the therapeutic areas of oncology, hepatitis B, and aging-related diseases, with a focus on R&D of small-molecule targeted cancer therapies. Its investigational Class 1 new drug, APG-2575, has completed dosing of the first patient in its Phase I clinical trial in China. Burning Rock Biotech specializes in providing next-generation sequencing (NGS) products and services with the highest clinical value for precision oncology. Its business currently covers three major segments: testing for cancer patients, early cancer screening and detection, and an ecosystem for tumor genomics big data.

Based on the financing trends observed in the first seven months, the number of financing deals and the total amount raised may decline this year, yet the number of investors is not expected to decrease. In the healthcare sector, precision medicine has become a major trend, with biotechnology serving as a key enabler; consequently, investor interest in this field remains strong.

It is worth noting that, as biotechnology companies listing on the Hong Kong Stock Exchange are no longer subject to profitability requirements, and since the launch of the STAR Market this year, its fifth set of listing criteria also imposes no profitability requirements on enterprises with strong scientific research capabilities. Indeed, several biotechnology companies have carried out initial public offerings (IPOs) on either the Hong Kong Stock Exchange or the STAR Market this year. Consequently, biotech firms now have more avenues for going public and broader channels for raising capital.

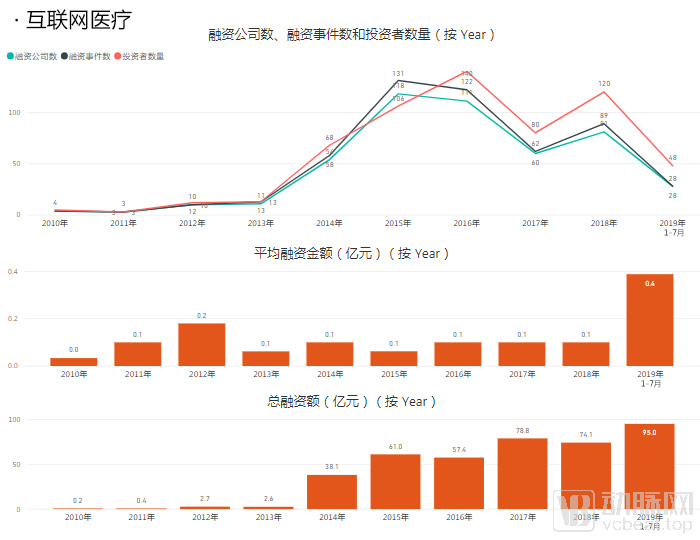

After penetrating the consumer sector, the internet has gradually entered the healthcare field, aiming to address various pain points of traditional medical services through innovations in processes and business models. These innovations have progressively covered the three major segments of healthcare, pharmaceuticals, and insurance, spanning from appointment scheduling and consultations to online diagnosis, medication delivery, and insurance coverage.

Financing Trends in the Internet Healthcare Sector, Chart by VCBeat

Internet healthcare entered a period of explosive financing growth in 2014, with the establishment of numerous new enterprises and several companies securing substantial funding. This year was dubbed the “Year One of Internet Healthcare.” In the following two years, Wuzhen Internet Hospital, The First Affiliated Hospital of Zhejiang University School of Medicine Internet Hospital, and others were successively established. Furthermore, Yinchuan City in Ningxia Hui Autonomous Region provided policy support to the internet healthcare industry, encouraging enterprises to build internet hospitals, which led to the collective settlement of 15 internet hospitals at the Yinchuan Smart Internet Hospital Base. Subsequently, other regions across China emulated Yinchuan’s model, sparking a nationwide boom in the construction of internet hospitals.

However, the industry cooled down in 2017, with a sharp decline in the number of financing events. That year, a draft for public comment of the “Administrative Measures for Internet Diagnosis and Treatment (Trial)” was leaked. The draft stipulated that approvals previously granted to internet hospitals, cloud hospitals, and network hospitals should be revoked by the local health and family planning administrative departments at or above the county level within 15 days after the issuance of these Measures, plunging the industry into an environment of uncertainty.

However, a turning point emerged in 2018. In April 2018, the landmark policy “Opinions of the General Office of the State Council on Promoting the Development of ‘Internet + Healthcare’” was issued, encouraging and supporting internet-based healthcare, which led to a rapid industry recovery.

Among companies in the internet healthcare sector that have secured substantial financing, WeDoctor has established a data-driven digital health network. Last year, WeDoctor completed a $500 million Pre-IPO funding round, entering the final sprint phase before its public listing. Medlinker, which evolved from a physician social networking platform, initially focused on hepatology and has since expanded its internet hospital services to other specialties, now covering multiple disease areas including HIV, endocrinology, oncology, and orthopedics.

As leading players gradually emerge, financing activity in the internet healthcare sector has declined since the beginning of this year. However, the total financing amount in the first seven months has already surpassed that of the entire previous year, primarily because JD Health was spun off from JD.com to operate independently and completed a Series A funding round of up to $1 billion.

From an industry perspective, following the certainty brought by policy changes last year, the internet healthcare sector has entered a fast track this year, with an increasing number of internet hospitals being established. As internet hospitals are capable of diagnosing and prescribing for common diseases and follow-up visits for chronic conditions, serving as a critical link between medical care and pharmaceutical services, they will become a standard component for internet healthcare enterprises.

Furthermore, the business ecosystem of internet healthcare is receiving increasing attention. Online consultation is merely a basic function; whether a closed loop integrating medical care, pharmaceuticals, and insurance can be established, and whether more targeted health management services can be provided, are key areas of extensive exploration within the industry.

On August 30 this year, the National Healthcare Security Administration released the “Guiding Opinions on Improving Price Management and Medical Insurance Payment Policies for ‘Internet+’ Medical Services,” clarifying numerous issues such as price item management for internet-based medical services and the scope of medical insurance coverage. Subsequently, as provincial-level healthcare security authorities formulate their respective implementation rules, the payment framework for internet-based healthcare will be further refined, potentially ushering in further development for the industry.

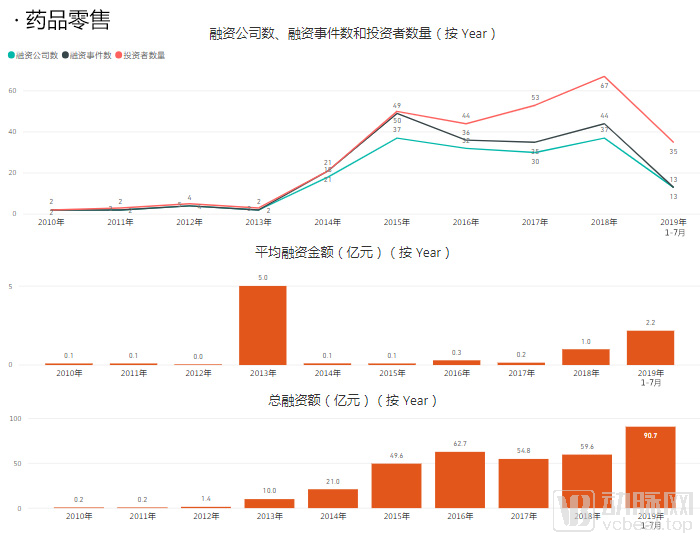

Financing Trends in the Pharmaceutical Retail Sector, Chart by VCBeat

Financing in the pharmaceutical retail sector entered an active phase in 2014, directly driven by the rise of pharmaceutical e-commerce. While e-commerce had already achieved significant success in the general consumer sector, its expansion into the pharmaceutical retail industry was heavily influenced by policy, given the strict regulatory controls on medicines. In 2014, the China Food and Drug Administration (CFDA) released the “Administrative Measures for the Supervision and Management of Online Food and Drug Operations (Draft for Comments),” which permitted internet-based enterprises to sell prescription drugs upon presentation of a valid prescription, in accordance with regulations on classified drug management. The release of this draft spurred a large number of pharmaceutical companies to enter the e-commerce space.

In 2016, the number of online pharmacies in China reached 678, a year-on-year increase of 72.5%, marking the entry of pharmaceutical e-commerce into a phase of rapid development. After 2016, the business models of pharmaceutical e-commerce had taken shape, primarily comprising B2C, B2B, and O2O models. The industrial landscape of pharmaceutical e-commerce gradually took form, with a cohort of representative enterprises emerging in their respective niche sectors.

Among enterprises that have secured substantial financing, Dingdang Kuaiyao has established an integrated online-to-offline (O2O) retail model characterized by “direct supply from pharmaceutical manufacturers and online ordering with store-based delivery,” leveraging its self-operated offline pharmacies and in-house professional pharmaceutical team. Miaoshou Doctor, through its Yuanxin Grand Pharmacy brand, covers 66 cities across China, operating more than 200 directly managed hospital-adjacent pharmacies and specialized Direct-to-Patient (DTP) pharmacies. Its subsidiary, Miaoshou Internet Hospital, provides online follow-up consultations, health education, and O2O medication delivery services to support these offline pharmacies, thereby forming a comprehensive post-diagnosis management system.

However, pharmaceutical e-commerce still faces a major challenge: the sale of prescription drugs has never been formally incorporated into relevant policies, despite prescription drugs accounting for approximately 85% of the total pharmaceutical market size. In 2018, the China Food and Drug Administration (CFDA) released the Administrative Measures for the Supervision of Online Drug Sales (Draft for Comment), which further stipulated that “drug retailers operating as part of a retail chain enterprise are prohibited from selling prescription drugs online.”

The good news is that the newly revised Drug Administration Law will take effect on December 1 this year, lifting restrictions on the online sale of prescription drugs. In the coming period, regulatory authorities will also formulate measures for the supervision of online drug sales. It is widely believed within the industry that pharmaceutical e-commerce will usher in new development opportunities. Judging from the financing situation in the first seven months of this year, the number of financing events has shown a downward trend. The total financing amount still includes JD Health’s $1 billion funding round; excluding this deal, the remaining financing amount is less than half of last year’s figure. However, with the liberalization of laws regarding the online sale of prescription drugs, the sector is expected to enter another period of heightened activity.

Given that the online sale of prescription drugs requires interoperability between sales networks and healthcare institutions’ information systems to ensure the authenticity of prescriptions, industrial convergence has become a major trend. On one hand, physical pharmacies are integrating with online platforms, enabling pharmacies to broaden their sales channels while platforms expand their service offerings. On the other hand, pharmaceutical e-commerce companies are merging with internet hospitals to secure authentic prescriptions for safety and regulatory compliance, while internet hospitals can provide patients with a more comprehensive range of cost-effective medications.

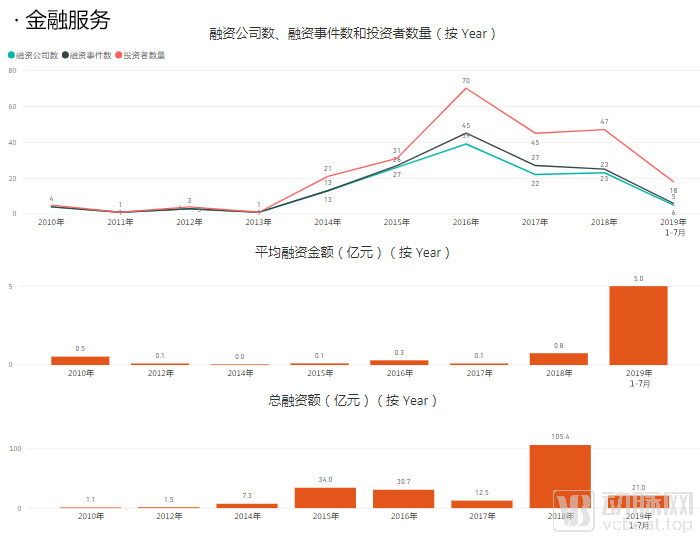

Financing Trends in the Financial Services Sector, Chart by VCBeat

Since 2014, the financial services sector has entered a period of heightened activity. This year witnessed an acceleration in the digitalization of the insurance industry. The internet’s influence on insurance permeates every stage of the value chain, including product development, sales, underwriting, claims processing, customer service, back-office operations, and risk control. Traditional insurance marketing channels—such as direct sales, bancassurance, and telemarketing—face limitations in growth potential and high channel costs. The internet has expanded insurance distribution channels, offering inherent advantages for selling standardized insurance products. It drives significant traffic volume and enables precision marketing based on user personas within specific scenarios.

Furthermore, the continuous development of big data and internet-based healthcare helps address challenges such as cost containment, distribution channels, and product innovation. Internet-based healthcare can be integrated with internet insurance to build an integrated industrial ecosystem encompassing users, products, channels, and data. Leveraging the array of resources brought by the internet, the financial services sector remains consistently active.

During this period, online mutual aid platforms such as Waterdrop emerged. By focusing on crowdfunding for critical illnesses as an entry point, the company expanded into health insurance and health protection services, including the Waterdrop Insurance Mall and Shuidichou (Waterdrop Crowdfunding). This model leverages social networks as a channel for user acquisition, with the viral nature of social dissemination providing significant advantages over traditional insurance sales methods. In March and June of this year, within a span of just three months, Waterdrop completed its Series B financing round of RMB 500 million and its Series C financing round of RMB 1 billion, respectively.

In 2017, the China Insurance Regulatory Commission (CIRC) issued the “Notice on Regulating Product Development and Design Practices of Life Insurance Companies,” launching a stringent crackdown on the industry practice of packaging insurance products as wealth management products for sale. Consequently, overall activity across the sector was adversely affected.

However, the financial services sector has regained momentum this year. It should be noted that, as shown in the chart above, total financing reached a peak last year due to Ping An HealthCare Technology’s $1.15 billion (approximately RMB 7.6 billion) Series A funding round. However, Ping An HealthCare Technology primarily provides management services for medical insurance and health administration systems, commercial insurers, healthcare institutions, and pharmaceutical distribution channels, without engaging directly in insurance business itself; thus, it represents a special case. Excluding this financing amount, the total financing in the first seven months of this year has already approached two-thirds of last year’s total, directly illustrating the heightened activity in the sector since the beginning of the year.

This year, Miao Health also completed a C-round financing of 500 million yuan. By empowering the insurance industry with health technology, Miao Health has transitioned from building a mobile health management platform to diversifying its business operations. Its services now cover smart hardware connectivity, out-of-hospital health big data tracking, health behavior intervention, insurance services, and offline health management, thereby establishing a closed-loop online-to-offline (O2O) health management ecosystem.

Amid the overarching trend of healthcare cost containment under medical insurance, commercial health insurance has significant room for growth. However, with technological advancements and industrial convergence, the financial services sector has long transcended the traditional boundaries of insurance. In the future, efficient collaboration between payers and service providers will be key to forming a closed-loop industry ecosystem. Whether through internal coordination among various business units within an enterprise, partnerships with external resources, or the introduction of strategic investments, these are all important pathways to facilitate the formation of such a closed loop.

Model innovation has injected vitality into the healthcare industry, while technological innovation serves as the intrinsic driving force propelling its overall progress. In recent years, the advent of digital transformation has expanded the reach of healthcare informatization. The widespread application of artificial intelligence and big data has made precision medicine more accessible and extended its integration into health management scenarios.

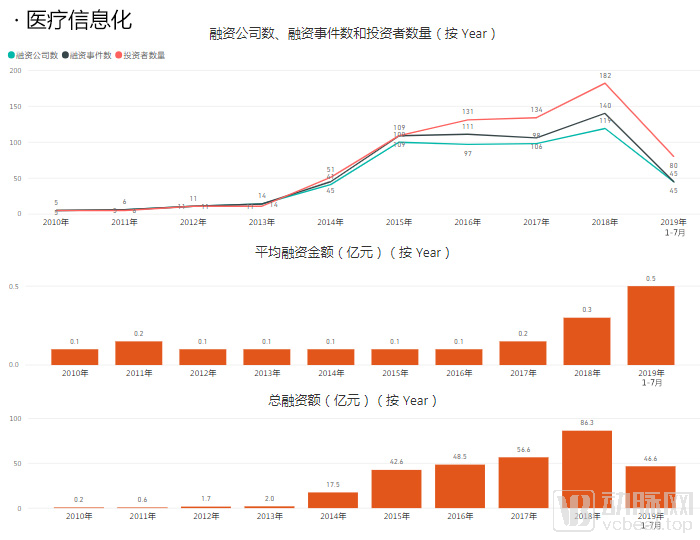

Financing Trends in the Healthcare IT Sector, Chart by VCBeat

From the perspective of financing trends, healthcare informatization entered a phase of rapid development in 2014, with an increasing number of investors entering the market and both the average deal size and total financing amount rising steadily.

Medical informatization involves various clinical departments and operational processes within healthcare institutions, ranging from initial patient registration, fee collection, and medication dispensing management to the application of departmental subsystems. These subsystems are interconnected to form a comprehensive system, incorporating big data analytics and advanced Clinical Decision Support Systems (CDSS) to assist clinical practice. With the advancement of information technology and the promotion of tiered diagnosis and treatment, informatization not only functions within hospitals but also provides robust support for collaboration among medical consortia and other healthcare institutions. Furthermore, the extension of informatization beyond hospital premises enhances patients’ healthcare experience and strengthens the interoperability and sharing of patient information.

Among companies that have secured substantial financing, Xinyi International is a provider of medical cloud application solutions. Through its integrated “cloud technology + cloud services + cloud specialties” business model, it delivers multi-dimensional medical cloud application services covering diagnosis and treatment, teaching, scientific research, and management to governments, healthcare institutions at all levels, and industry partners. Neusoft Wanghai offers solutions for performance supervision of public hospitals, hospital equipment management, and smart finance to governments, medical groups, medical consortia, and hospitals. Taimei Medical Technology provides information system solutions for pharmaceutical R&D collaboration, data, imaging, and pharmacovigilance to healthcare institutions.

This year, the National Health Commission released the "Graded Evaluation Standard System for Hospital Smart Services (Trial)," which establishes detailed evaluation criteria for the level of informatization in hospitals at Level II and above. The system evaluates smart services from two perspectives: the functionalities provided by hospitals and the perceived effectiveness by patients. Smart services are categorized into Levels 0 to 5, with specific indicators defined for each level. According to the CHIMA "Survey on Hospital Informatization Status in China (2017–2018)," 42.36% of hospitals in China have formulated comprehensive informatization plans, with tertiary hospitals demonstrating a significantly higher rate of such planning compared to hospitals below the tertiary level.

Medical informatization serves as a critical foundation for enhancing hospital management standards and clinical capabilities. According to statistics from CHIMA, there remains significant room for improvement in the level of informatization construction among hospitals in China. Furthermore, the national government has established an evaluation system to assess the extent of informatization development, indicating that such construction will remain an essential requirement in the future. For tertiary hospitals, which already possess relatively comprehensive informatization systems, the high volume of patients necessitates urgent improvements in healthcare professionals’ work efficiency and patient care experiences. Consequently, leveraging technologies such as big data and cloud computing to update and iterate existing systems represents the future direction.

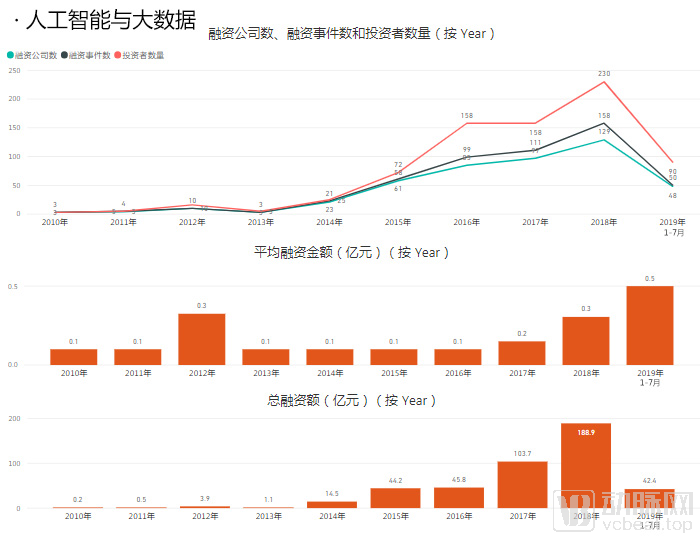

AI and Big Data Financing Trends, Chart by VCBeat

In recent years, industries related to big data in health and healthcare have been incorporated into the national strategic layout for big data. Furthermore, in 2016, the State Council issued the “Guiding Opinions on Promoting the Healthy Development of the Pharmaceutical Industry,” which explicitly called for vigorous development of intelligent medical services and affirmed the application of artificial intelligence (AI) in the healthcare sector. Consequently, the AI and big data sectors have entered a period of rapid growth in recent years.

Artificial intelligence can be applied in various scenarios within the healthcare sector, including AI-assisted diagnosis in medical imaging, drug development, R&D of medical robots, and analysis of healthcare data. Big data analytics in healthcare can provide clinical guidance to physicians in determining treatment plans, selecting drug types and dosages, and supporting public health disease prevention and control efforts.

Among companies that have secured substantial financing, Ping An Health Technology has deployed applications in the healthcare sector leveraging biometric recognition, artificial intelligence (AI), and big data to address challenges across the “three medicals” (healthcare, health insurance, and pharmaceuticals), such as using big data to more accurately identify insurance fraud and abuse. Yitu Healthcare applies AI technology to the diagnosis of various diseases, constructs knowledge graphs based on highly localized datasets, and utilizes algorithms and big data to analyze clinical cases and literature, thereby maximizing their value. All-domain Medical Care integrates AI into radiotherapy products to enhance the quality and efficiency of radiation therapy.

Last year, Ping An Health Insurance Technology completed a $1.15 billion Series A financing round (approximately RMB 7.6 billion), accounting for 40% of the total funding raised that year. Excluding this portion, the total funding amount appears to have declined based on the financing activity observed in the first seven months of this year. While the artificial intelligence and big data sectors appear promising, many practical challenges remain to be addressed.

This year, the National Medical Products Administration (NMPA) released the “Key Points for Approval of Medical Device Software Assisted by Deep Learning in Decision-Making,” establishing specific criteria for the approval of AI-based medical devices and steering the industry toward greater standardization. However, AI products still need to address challenges related to data sources, homogenization, clinical implementation scenarios, and payment mechanisms.

Currently, the storage and utilization of big medical data have expanded from hospitals to pharmaceutical companies, distribution enterprises, and internet healthcare companies. This year, Ernst & Young released a report titled "Realizing the Value of Healthcare Data: A Framework for the Future," which shows that the value of 55 million people's medical data in the UK's National Health Service is £9.6 billion, highlighting the significant value of big medical data. However, in the future, challenges such as ownership, security, privacy, and information silos still need to be addressed in the field of big medical data.

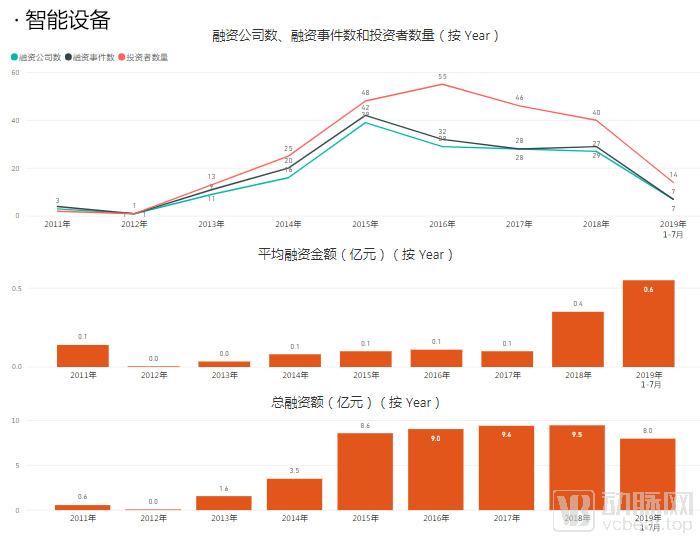

Trends in Smart Device Financing, Chart by VCBeat

In terms of financing trends, smart devices entered an active phase starting in 2013, with the number of financing events peaking in 2016 and declining thereafter.

Market enthusiasm for smart devices has declined significantly. A key reason is that these devices offered overly limited functionality, resulting in low user stickiness. Features such as step counting, sleep monitoring, and activity tracking have become standard, yet the data collected through them offer little additional value. In contrast, patients with chronic conditions and the elderly are populations that stand to benefit more from data collection via smart devices; timely data acquisition facilitates more effective health management interventions by healthcare professionals. However, technologies for wearable devices to monitor vital signs such as blood pressure, blood glucose, and blood oxygen saturation remain immature. Medical device certification requires prolonged clinical trials and is subject to stricter regulatory oversight. Consequently, companies with insufficient technical capabilities have been gradually squeezed out of the market, while those with the ability to build ecosystems have emerged and grown.

Among companies that have secured substantial financing, Zhiyun Health has leveraged its proprietary smart hardware for glucose data transmission to deeply mine big data through a medical engine, building an ecosystem for mobile and digital healthcare. This ecosystem connects patients, physicians, pharmaceuticals and consumables, as well as health management and education, forming a closed-loop system for chronic disease management. Its latest Series C funding round has brought cumulative financing to $100 million. Jingbai Medical is a provider of smart maternal and child health solutions. Its intelligent device products include series of home fetal heart rate monitors, clinical fetal heart rate monitors, and ultrasound fetal monitors, with multiple product lines currently available on the market.

Smart devices can be applied in scenarios such as exercise monitoring, assisted diagnosis and treatment, personalized therapy, and chronic disease management. Currently, technologies for exercise monitoring products are relatively mature, with companies like Huawei and Xiaomi already capturing a significant market share. In the future, there will be substantial market potential for products focused on personalized therapy and chronic disease management. Applications in the medical field will serve as one of the key drivers of market growth, and the boundary between health-oriented and medical-grade products will become increasingly blurred.

Given the limited resources of public hospitals, private hospitals and clinics have emerged against the backdrop of healthcare reform, supplementing medical resources, particularly at the primary care level. Meanwhile, certain services spun off from hospitals, such as diagnostic imaging and clinical laboratory testing, have gradually given rise to third-party medical service providers. Healthcare delivery settings are now appearing in increasingly diversified forms.

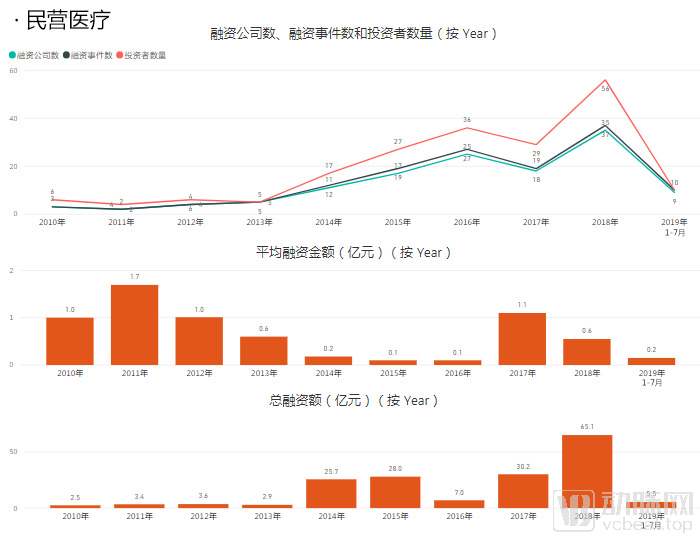

Financing Trends in the Private Healthcare Sector, Chart by VCBeat

Hospitals are characterized by their asset-heavy nature and long investment cycles, necessitating continuous and substantial capital infusion for their development. During the advancement of healthcare reform, the state has frequently introduced policies to affirm, encourage, and support private healthcare provision. Notably, in 2013, the State Council issued Several Opinions on Promoting the Development of the Health Service Industry, which optimized investment and financing guidance policies and encouraged financial institutions to innovate financial products and service models tailored to the characteristics of the health service industry, aiming to address the financing difficulties faced by private hospitals. Since 2014, the private healthcare sector has entered a period of heightened activity, with the number of financing events increasing year by year. Although there was a notable decline in the number of such events in 2017, the total financing amount remained substantial.

Among companies that have secured substantial financing, Taikang Bybo Dental deserves special mention. In 2018, Bybo Dental received a strategic investment of RMB 2.062 billion from Taikang Life Insurance, aiming to create a closed loop integrating dental healthcare services with insurance payment solutions, and striving to achieve a win-win outcome for service providers, payers, and consumers. Earlier, in 2014, Bybo Dental had also obtained a strategic investment of RMB 1 billion from Legend Holdings. Another private healthcare enterprise that has attracted significant funding is Arrail Group, which positions itself as a provider of premium dental care services. In addition, the physician group Bodajialian also secured substantial financing, introducing a strategic investment of RMB 1 billion from New Frontier Health in 2017.

Precisely because the market cultivation cycle for private healthcare is long, making it impossible to “make quick money” or achieve a rapid exit, both capital investors and medical institutions should recognize the critical importance of mutual resource integration. According to statistics from the VCBeat database, strategic investments account for the highest total amount in financing rounds within the private healthcare sector. The aforementioned cases of Taikang Life Insurance investing in Bybo Dental and New Frontier Group investing in Bodajialian are both strategic investments involving the integration of industrial resources.

Financing in the private healthcare sector during the first seven months of this year has been less than optimistic; however, the Hong Kong IPO of Jinxin Fertility and the acquisition of United Family Healthcare by New Frontier Health Group have nonetheless helped bolster industry confidence. Given that public hospitals are predominantly general hospitals with relatively few specialized institutions, differentiated development through specialization represents a promising strategic direction for private healthcare providers in the future. Key specialty areas include dentistry, ophthalmology, assisted reproductive technology (ART), and cosmetic surgery. Furthermore, the emergence of physician groups can cultivate a cohort of professionals who possess both medical expertise and market acumen. By adopting a physician-led model, these groups can also help address the longstanding talent shortages faced by traditional private hospitals.

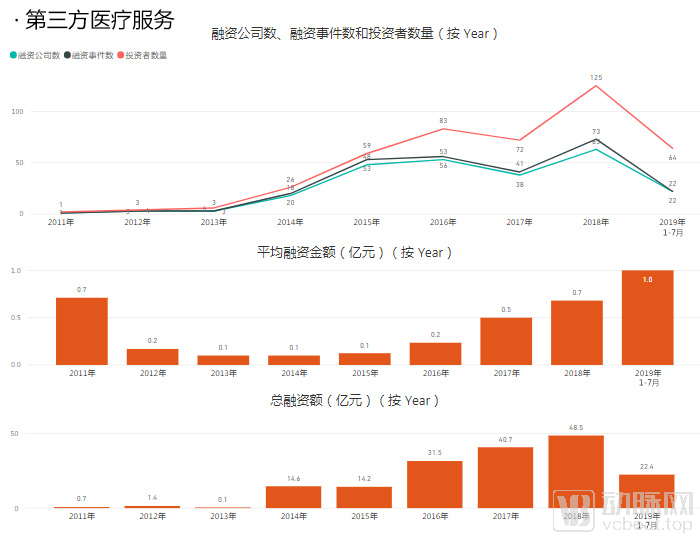

Trends in Third-Party Medical Service Financing, Chart by VCBeat

Third-party medical services are healthcare facilities that have emerged against the backdrop of “tiered diagnosis and treatment plus promotion of privately-run healthcare.” In October 2013, the national government issued the Several Opinions on Promoting the Development of the Health Service Industry, vigorously developing third-party services and guiding the establishment of specialized medical laboratory centers and imaging centers. Starting in 2014, the third-party medical services sector entered a period of active financing. In 2017, the government introduced further policies to encourage the development of ten types of third-party medical service institutions, including: medical imaging diagnostic centers, pathological diagnostic centers, hemodialysis centers, medical laboratories, hospice care centers, rehabilitation medical centers, nursing centers, sterile supply centers, health examination centers, and small- and medium-sized ophthalmic hospitals. In 2018, the sector reached a peak in financing activity.

Due to the limited service radius of healthcare providers, standalone third-party medical service institutions typically face a clear growth ceiling. By adopting a chain-based expansion strategy, these institutions can not only enhance their brand image but also strengthen their bargaining power with upstream and downstream players in the industry chain through economies of scale, thereby achieving a low-cost operational model.

Among companies that have secured substantial financing, Yimai Yangguang, a well-known third-party medical imaging diagnostic institution, just completed its Series C funding round worth hundreds of millions of yuan this July. Yimai Yangguang currently operates nearly 80 offline medical imaging centers and will accelerate its business expansion across the entire medical imaging industry chain. Qianmai Medical Laboratory is a third-party testing center that raised over 100 million yuan in its Series C funding round in 2018. It primarily provides routine clinical laboratory tests, pathological examinations, specialized tests, and research-related testing services to medical institutions at all levels.

Since some genetic testing companies also provide testing services to medical institutions or patients, we have included these companies under third-party clinical laboratories within the third-party medical services sector. However, their financing is primarily driven by their testing technologies and capabilities rather than their services; therefore, we do not conduct a separate analysis of these enterprises here.

Based on the financing trends observed in the first seven months, third-party medical services are expected to maintain last year’s momentum this year. In the future, opportunities for third-party medical service providers will not be limited to delivering medical services alone; they can also achieve deeper expansion by extending their reach upstream and downstream within the industry. For more mature third-party medical service providers, horizontal and vertical integration across the industry chain can create new growth drivers.

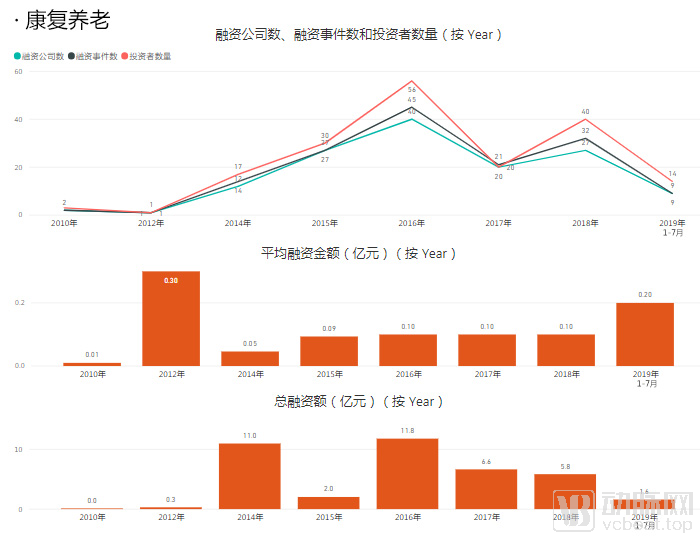

Financing Trends in the Health and Wellness Sector, Chart by VCBeat

The rehabilitation and elderly care sector gradually entered a period of heightened activity after 2012. With the aging of China’s population, the state has introduced a series of incentive policies since 2011 to improve the rehabilitation medical service system and develop the elderly care service industry. Since then, rehabilitation departments within general hospitals have been progressively established and refined, while specialized rehabilitation hospitals and rehabilitation institutions have also emerged. The rehabilitation medical service system comprises rehabilitation departments in tertiary hospitals, rehabilitation departments in secondary hospitals (or specialized rehabilitation hospitals), community rehabilitation centers (outpatient clinics), and home-based rehabilitation services. The primary recipients of rehabilitation medical services include postoperative patients, the elderly, individuals with chronic diseases, and persons with disabilities.

In the early stages of capital entry into the rehabilitation sector, investments were primarily made through the trusteeship of rehabilitation departments in public hospitals or by directly participating in the transformation of secondary-level hospitals. After accumulating management and operational experience, investors began to target specific segments of the rehabilitation industry, such as specialized rehabilitation hospitals or community rehabilitation centers focusing on musculoskeletal rehabilitation, pediatric rehabilitation, and cardiopulmonary rehabilitation, implementing standardized and chain-based expansion strategies. With the widespread application of internet and big data technologies, the rehabilitation industry has undergone intelligent and informatization-driven innovations. While capital values enterprises that address specific links in the rehabilitation care continuum, it places even greater emphasis on integrated solution providers capable of offering comprehensive services encompassing rehabilitation equipment, talent development, management and operations, and informatization infrastructure.

In the elderly care sector, capital from various industries—primarily healthcare, real estate, and tourism—has entered the market, giving rise to diverse models of elderly care services.

Among companies in the health and wellness sector that have secured substantial financing, Neusoft Xikang is dedicated to building an integrated platform for health management, medical care, rehabilitation, and elderly care services, all connected by big health and medical data. By leveraging its own wearable devices and third-party ecosystem products, the company collects personal health and lifestyle information, establishes electronic health records, and provides users with full-cycle services including health interventions, telemedicine, and in-home care. Kangjiu Medical focuses on the integration of medical and elderly care. Supported by its centrally operated nursing homes and rehabilitation hospitals, anchored in local communities, and linked through an IT information platform, it offers seniors a comprehensive elderly care solution that integrates daily living assistance, diagnosis and treatment, healthcare, psychological support, emergency rescue, and post-ICU care.

Over the past two years, activity in the health and wellness sector has declined, with single-business models struggling to attract capital attention. The future of the health and wellness industry will trend toward building large-scale ecosystems, with capital investment focusing on platform-based enterprises. Such companies will not only provide one-stop, full-cycle services to C-end patients but also empower B-end enterprises by aggregating technology, capital, talent, and management resources to serve partners across the healthcare, pharmaceutical, and medical device supply chains.

Gaining data-driven insights into the future stems from our commitment to growing alongside the industry. We welcome enterprise executives deeply engaged in specific sectors, experts and scholars focused on particular fields, and other industry professionals to engage in discussions with us or submit contributions. Meanwhile, innovative companies and projects across various sectors are encouraged to connect with us. Investors and other stakeholders are also invited to reach out for investment and financing matchmaking, or to leverage our platform to showcase high-potential new enterprises and projects.

Note: In the data statistics, amounts in USD, HKD, and other currencies have been converted into RMB using the average exchange rate of the respective year for uniform calculation; the “average financing amount” mentioned in the text refers to the median.

He Qiongfeng from the VCBeat Data Technology Center also contributed to this article.

References:

VCBeat: White Paper on China’s Third-Party Medical Services Industry

Tianfeng Securities: Medical Devices, the Cyclical Starting Point of a Golden Age

VCBeat Eggshell Research Institute: The Leap from Integrated Platforms to Big Data Applications — 2018 Hospital Informatics Construction Report

CITIC Securities: Thematic Report on China’s Private Hospital Industry: Vibrant Colors Adorn the Foreshore, Waves Stir the Distant Sky

VCBeat Eggshell Research Institute: Report on the Competitiveness of the Pharmaceutical E-commerce Industry

VCBeat: 2019 Research Report on the Development Potential of the Rehabilitation Industry

Deloitte: Exploring the “Last Mile” of Healthy Aging – Outlook on the Trend of Integrated Medical and Elderly Care in China

VCBeat: Entering the Era of Value Output, 2018 Medical Big Data Industry Report