BeiGene Responds to J.Capital Research's Short Seller Report in Investor Conference Call

Recently, Chinese innovative pharmaceutical company BeiGene (06160.HK, BGNE.NS) faced a short-selling ambush by the investment research firm J. Capital Research. In its published report, the latter directly accused BeiGene of “fabricating over $154 million in revenue in Q4 2017, an exaggeration of 133%.”

At 7:00 a.m. Beijing time on September 9, BeiGene held a conference call, with all senior executives in attendance, providing detailed responses to each of the allegations raised by J. Capital Research.

• Meeting Time: 7:00 AM (Beijing Time), September 9, 2019. The following is the transcript of the meeting:

Ladies and gentlemen, good day! Welcome to BeiGene’s conference call. Today’s call is hosted by Dr. Heng Liang, Chief Financial Officer and Chief Strategy Officer of BeiGene.

Dr. Heng Liang:Good morning, everyone. Thank you for joining today’s conference call. Before I begin, I would like to remind you that we will be making forward-looking statements during this call. The Company’s business operations are subject to certain risks, which have been discussed in our filings with the U.S. Securities and Exchange Commission (SEC) and The Stock Exchange of Hong Kong Limited, as outlined in our forward-looking statements slide. Accordingly, we will not address every point raised in the short-seller report today. This should not be construed as an admission that any unaddressed items are factual. We have no intention of commenting publicly on certain claims that are demonstrably false.

Also in attendance today were Mr. John V. Oyler, Founder, Chairman and Chief Executive Officer of BeiGene; Dr. Wu Xiaobin, General Manager of China Region and President of the Company; Mr. Scott Samuels, Head of Legal Affairs; and Mr. Dan Maller, Vice President of Finance and Accounting. We would now like to invite Mr. John V. Oyler to speak first.

Mr. John V. Oyler, Founder, Chairman, and Chief Executive Officer of BeiGene

(Image source: Internet. Please contact us for removal if there is any copyright infringement.)

We founded BeiGene in 2010 with the goal of developing innovative oncology medicines and making them accessible to patients in need around the world to the greatest extent possible. From day one, we have been committed to building a global company and upholding the highest global standards.

We are committed to adhering to the highest standards of quality, compliance, and transparency in everything we do, as demonstrated in our laboratory research, clinical development, manufacturing processes, financial controls, and compliance procedures.

We recognize that combating cancer requires tremendous effort. Our company now employs more than 2,700 people across 10 offices on four continents. We are conducting clinical trials in over 30 countries and regions, including 26 Phase III or potentially registrational trials. These clinical studies involve 13 pipeline products, six of which were independently developed by BeiGene’s scientists. We expect to announce data from up to 10 Phase III clinical studies by the end of 2020.

Regarding recent developments, the purpose of today’s meeting is to address concerns arising from certain factually incorrect and misleading statements contained in the recent report published by the short-selling firm J. Capital. While I do not personally know anyone at J. Capital, I am well acquainted with the team that has built our company.

First, our other co-founder, Dr. Wang Xiaodong, is someone I hold in the highest regard, both as a scientist and as an individual. I am also very familiar with Dr. Wu Xiaobin. From the day we began considering his appointment, I received more recommendations for him than for anyone else. He is renowned in this industry for his integrity, and the three words most frequently used to describe him are “open, honest, and transparent.” Most of you here today are also acquainted with our CFO, Dr. Liang Heng, who is a remarkably honest, prudent, and humble individual. For those of you who may not know him, I encourage you to ask others on today’s conference call about him.

I am incredibly fortunate to be surrounded not only by a group of exceptional leaders but also by individuals who are profoundly honest and principled. They were under no obligation to join BeiGene; they had many other options. They chose BeiGene because they believe we are at a unique moment and position, with the potential to make a profound impact on patients. I personally stake my reputation on the integrity of our team.

We are committed to making a lasting and profound impact in the fight against cancer. We recognize that there are no shortcuts on this path, and we remain steadfast in our commitment—both past and future—to operating our company in accordance with the highest standards of quality and integrity.

I regret that this incident has briefly distracted us from our mission of fighting cancer for patients. We are using today’s opportunity to address the allegations raised in the report. It is evident that the report contains numerous misleading assertions and malicious speculations. We welcome your questions during the Q&A session later in this conference call. In addition, Dr. Liang Heng and I will attend Morgan Stanley’s conference in New York on Tuesday (the 10th) U.S. time, and we look forward to seeing you there. Now, I will invite Dr. Wu Xiaobin to speak.

Dr. Wu Xiaobin, General Manager of BeiGene China and President of the Company

(Image sourced from the internet; please contact us for removal if there is any copyright infringement)

Thank you! Hello to all our online friends, and thank you for participating in today’s conference call. I would like to respond to some absurd allegations regarding our product sales made in the short-selling report.

First, I would like to take a minute to share my perspective from a more personal standpoint. BeiGene remains steadfast in its pursuit of the highest standards of quality and compliance. I believe BeiGene is a unique company, dedicated to bringing innovative medicines with significant potential to patients worldwide, regardless of their location. It is a profound honor for me to have the opportunity to work alongside an unparalleled team at BeiGene.

Prior to joining BeiGene, I served as the General Manager for China at two of the world’s top three multinational pharmaceutical companies over a period of nearly 20 years, leading the pharmaceutical businesses of Bayer (Germany) and Pfizer (US) in China. Consequently, I have consistently upheld global standards in quality, compliance, ethics, and operational excellence, while also accumulating extensive experience in ensuring the accuracy of sales data in China.

In fact, our entire sales process in China is straightforward and clear:

• This slide clearly illustrates how revenue from imported drugs is generated in China. First, for foreign companies, Celgene ships the products to BeiGene. Upon receipt, BeiGene records them into inventory.

• Next, BeiGene sells its products to distributors—in this case, China Resources Pharmaceutical. It is a highly reputable company and ranks among the top three distributors in China. China Resources Pharmaceutical is listed in Hong Kong and collaborates with many multinational corporations. Once BeiGene sells its products to China Resources Pharmaceutical, we will recognize the revenue.

• Subsequently, our distributor network distributes the products to major hospitals and pharmacies, which constitutes market sales.

• Our product sales to distributors are all final, except for returns due to product defects. Since the fourth quarter of 2017, the total value of returns attributable to product defects has not exceeded $200,000.

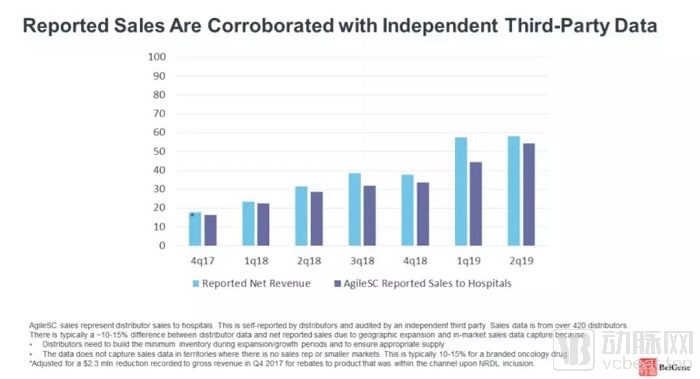

• We will obtain real-time information on product circulation throughout the distribution channel and continuously monitor this data.

• CR Pharmaceutical generally holds one month’s inventory of BeiGene’s currently commercialized products, a fact that we confirmed with CR in the second quarter of 2019.

• As is standard practice across the industry, we also closely monitor relevant information from distributors to the final point of sale, namely hospitals and pharmacies. While these data have certain limitations as they do not cover every hospital and pharmacy, they provide transparency at the hospital and pharmacy levels. The data reveal highly consistent pharmaceutical distribution patterns, which align with my prior expectations.

We stand by the accuracy of the data we report.

As a result of the successful execution of our commercial strategy, we have been able to sustain our revenue growth. We have also continued to expand our commercial team in China, which now comprises more than 600 employees. This represents a significant increase since we took over the commercial operations for Celgene’s portfolio. Our hospital coverage has expanded, and there have been substantial additions to both medical insurance reimbursement listings and approved indications. I am very proud of the work we have done and the achievements we have made at BeiGene. Next, I would like to invite Dr. Liang Heng to speak.

Dr. Heng Liang, Chief Financial Officer and Chief Strategy Officer of BeiGene

(Image sourced from the internet; please contact us for removal if there is any copyright infringement)

I will address the other allegations contained in the report. The report includes numerous erroneous statements, factually inaccurate information, and baseless speculation, even concerning fundamental facts such as incorrect data on management stock sales and miscalculations of the floor area of our R&D building. This not only demonstrates their lack of understanding of our business but also reveals their deficiency in conducting basic equity research analysis and performing essential due diligence to verify facts.

For those who have conducted in-depth investigations and broader physician surveys, it is still difficult to predict sales figures, let alone base allegations that our management fabricated 60% of sales on the purported results of interviews with only ten oncologists.

Many of the allegations and questions raised in the report could have been resolved simply by giving us a call, but they chose not to do so. Instead, they relied on their imagination to fabricate these baseless accusations. Some involve clearly serious issues, which we will address here. Others are utterly ridiculous; for example, it is claimed that we engaged in related-party transactions merely because the counterparty’s name sounds similar to that of our founder, Wang Xiaodong.

About BeiGene (Guangzhou) Biotech Co., Ltd.

One of the most serious allegations in this short-selling report centers on our Guangzhou entity and its operations, namely BeiGene (Guangzhou) Biotech Co., Ltd. Before I provide a detailed overview of the Guangzhou company’s business, I would like to take a moment to recap our investments and strategic partnerships established in Guangdong Province.

As is well known, Guangdong Province is one of the largest and most affluent provinces in China, accounting for more than 10% of the nation’s GDP. In collaboration with the Guangzhou Development District, we have established a large-scale biopharmaceutical manufacturing base, primarily funded through external capital. This joint venture serves as a production facility, in which BeiGene holds a 95% equity stake, while our partner, the Guangzhou Development District, holds a 5% equity stake in the joint venture entity that operates this production base. It is important to clarify that this 5% stake refers to equity in the manufacturing joint venture, not a 5% royalty or economic interest in our PD-1 monoclonal antibody, tislelizumab.

As many of you are likely aware, establishing a biologics manufacturing facility requires years of dedicated effort, and this work must commence well before commercial supply can be achieved. Our goal is to conduct significant business operations in Guangzhou, and these are tangible realities. We will hold the completion ceremony for Phase I of our Guangzhou manufacturing base in three weeks.

BeiGene (Guangzhou) Biotech Co., Ltd. is the legal entity responsible for providing financial support for the significant development costs of tislelizumab in China and for its post-approval marketing activities.

To fund the expenses of this segment, we must regularly increase our registered capital. Contrary to what the short-selling report claims, our entity, BeiGene (Guangzhou) Pharmaceutical Co., Ltd., is audited by Ernst & Young.

To commercialize tislelizumab in China, we require a drug distribution license. We obtained this license by acquiring a company that already held one, a common practice given the current difficulty in securing such licenses through direct application. Prior to our acquisition, the target company was renamed by its original seller. Upon completion of the merger and acquisition, the company was renamed BeiGene (Guangzhou) Pharmaceutical Co., Ltd. The use of temporary names followed by subsequent renaming is highly common in M&A transactions in China. A similar scenario occurred when we acquired Celgene’s China operations.

The short-seller report also speculated that the $25 million in non-current assets on the books of BeiGene (Guangzhou) Co., Ltd. was used to repurchase Celgene’s inventory. In fact, this payment was made to our contract manufacturing organization, Boehringer Ingelheim, for the expansion of production capacity dedicated to BeiGene, which is a common industry practice. Payments for capacity expansions by contract manufacturers are required, and this is another reason why we are building our own production facilities. We expect this expenditure to be recouped through future reductions in production costs from Boehringer Ingelheim; therefore, it is classified as a non-current asset. This is a specific payment that can be easily verified and has been clearly disclosed in our financial reports.

We have employees at BeiGene (Guangzhou) Biotech Co., Ltd. and maintain an actual office location, as indicated in the figure. Although the construction of our newly registered permanent office address has not yet been completed, it is common practice for a company’s temporary registered address to differ from its primary assets and main office location.

Let me reiterate several other accusations and erroneous statements made in the short-selling report.

• Regarding the inventory of Celgene products:Contrary to what was stated in the report, as Dr. Wu Xiaobin just explained, we hold inventory of Celgene products in China. Since these are imported drugs, we place orders several times a month. For instance, at the end of the second quarter, factors such as timing or the supplier’s stock levels may lead to an increase in procurement volumes from Celgene. Inventory levels may fluctuate significantly between periods, which has also been reflected in our financial statements.

Report.

• Regarding the inventory in Suzhou:The report states that they firmly believe our inventory at the Suzhou facility is related to Celgene’s products. In fact, the inventory recorded on the balance sheet for our Suzhou facility consists of zanubrutinib and pamiparib manufactured by the Suzhou facility itself. When preparing consolidated financial statements, these non-commercialized products are not classified as inventory under U.S. GAAP, as we had not yet obtained approval for the commercialization of zanubrutinib and pamiparib. This is standard industry practice: we present inventory in this manner in accordance with the principles of audit reports prepared under Chinese accounting standards, while making corresponding adjustments for inclusion in the global consolidated financial statements. Our Suzhou facility commenced operations in the second half of 2017. Its operations were audited by a local financial auditing firm until the end of 2017. Contrary to what was claimed in the short-selling report, Ernst & Young did not begin auditing the facility only from the beginning of 2018.

• Regarding the growth trend of gross profit:The short-selling report claimed that the rate of decline in our reported gross profit was inconsistent with price changes, citing this as evidence to support their theory that we were buying back new products from distributors. Among Celgene’s three products, Revlimid experienced the largest price reduction due to its inclusion in the National Reimbursement Drug List. However, this factor was already known at the time we acquired Celgene’s business and had been reflected in our gross margin figures since the fourth quarter of 2017. Therefore, our gross margin trend did not experience any further decline.

• Regarding the Minimum Purchase Commitment:This is also a misconception—that we are required to purchase drugs from Celgene. We are not obligated to purchase any minimum quantity of drugs from Celgene. However, as with all supply agreements, we must submit binding purchase orders. Of the $135 million in purchase commitments disclosed as of June 30, 2019, $114 million relates to commitments to purchase PD-1 from Boehringer Ingelheim over the next ten years. The remaining $21 million represents binding orders for inventory purchases from Celgene.

• Regarding the cash balance of Celgene China:The short-seller report’s claim regarding the cash balance obtained as part of the acquisition of Celgene China is factually incorrect, as it is an inference based on historical data. As part of the merger accounting integration, the upfront cash payment for the PD-1 collaboration was allocated to Celgene’s operations in China. This was clearly disclosed in the financial statements at the time of our acquisition.

Before I invite Mr. Ou Leiqiang to speak once again, I would like to address the issue of alleged “cashing out” by our management. The short-selling report claims that our insiders have sold more than $322 million worth of stock since the company’s IPO in 2016. However, this figure is approximately double the actual amount, as it double-counts both the planned and the actual share sales. If you review our Form 4 filings with the U.S. Securities and Exchange Commission (SEC), you will find that the shares actually sold by management are only half of what the short-selling report alleges.

More importantly, the management team and board members listed in this report sold only about 18% of their total holdings. Our CEO, Mr. Wang Lei, sold merely 16% of his total holdings. After the sale, he still retains a 10% equity stake in the company. It is evident that our CEO and other members of the management team hold substantial equity stakes in the company and will continue to do so. Their interests are aligned with those of investors. They have not “cashed out.”

"Ladies and gentlemen, I would like to reiterate that we remain committed to industry standards and operational excellence, and we deeply value the opportunities before us. Next, I invite Mr. Wu Lei to discuss our future investment strategies."

The short-selling report’s claims that our R&D expenditures and clinical development costs are excessively high are factually inaccurate. BeiGene’s R&D investment is indeed substantial. Our pipeline includes six internally discovered drug candidates currently in development, with another poised to enter clinical trials shortly. We are an industry leader in conducting global clinical development, including in China. We boast the largest oncology-focused clinical team in China.

To date, we have enrolled more than 7,000 subjects in BeiGene’s clinical programs. Our clinical trials include costly head-to-head studies, such as our global Phase III superiority trial comparing zanubrutinib with ibrutinib in the treatment of Waldenström’s macroglobulinemia.

We expect to obtain clinical data later this year. We are also conducting two other global Phase III clinical trials of zanubrutinib for the treatment of chronic lymphocytic leukemia (CLL): one is a head-to-head comparison against ibrutinib, and the other is a comparison against BR (bendamustine plus rituximab) regimen. Clinical data from these studies are expected in 2020. The costs associated with these large-scale hematologic oncology trials are generally higher than those of other clinical trials, primarily because we need to purchase ibrutinib for the head-to-head comparison; obtaining this clinical data is essential for achieving global market approval and launch.

Our PD-1 inhibitor also boasts an extensive clinical development program, including six global registrational trials. As many of you have heard me say over the past few years, the key to success in the PD-1 market lies not in being the first to obtain marketing approval, but in achieving broad indication coverage and doing so rapidly. Only with approvals across a wide range of indications can PD-1 inhibitors reach all patients in need at an affordable price.

This slide presents our R&D expenses. Compared with peer companies also conducting Phase III clinical trials, the majority of our R&D costs are associated with clinical development. We have 17 ongoing Phase III clinical trials, and our investment in this area is lower than the global international trend. We stand out among Chinese competitors because we conduct extensive global clinical trials and pursue the highest global standards in all our endeavors. In addition to clinical development, we also make substantial investments in manufacturing, which represents a key strategic capability. These costs are reflected in our R&D expenses until our clinical candidates receive marketing approval.

In addition, we continue to support a preclinical R&D team of more than 300 people. As this team is expanding, we need to acquire additional R&D space to enlarge our R&D center in Changping. The short-selling report alleged that the building we purchased in Changping was acquired at a price above market value, with the intent of channeling benefits to Xiao Dong’s brother through alternative means. First, I wish to clarify that Xiao Dong does not have a brother. Second, regarding the alleged market price of RMB 30,000 per square meter cited in the short-selling report, the actual price we paid was RMB 21,000 per square meter. Therefore, contrary to their claims, we actually secured a favorable deal in this transaction. As you all know, I am someone who enjoys making jokes, but I am not joking about this matter. This is a very serious and malicious accusation.

The short-selling report also questioned our disclosed R&D costs, claiming that our internal quality control was poor because we did not allocate our R&D expenses by project. However, this is not typical practice in our industry. In fact, we have disclosed external expenditures, which are allocated by R&D project. As a company listed on both the NASDAQ and the Hong Kong Stock Exchange, our financial controls are subject to rigorous oversight. We are audited by Ernst & Young, which has issued unqualified opinions on our internal quality control and our consolidated financial statements for 2017 and 2018.

Furthermore, we strictly adhere to the compliance requirements of the Sarbanes-Oxley Act regarding the assessment of internal control management. We take great pride in our robust internal quality controls. Therefore, I firmly disagree with the assertions made in this report. I have full confidence in the work we are doing at BeiGene, and I stand by the accuracy of the data presented in our financial reports. We remain steadfast in our pursuit of high quality and regulatory compliance. I trust in the integrity of our team and am deeply grateful for everyone’s daily efforts, which have enabled us to achieve so much in such a short period. I concur with Xiaobin’s remarks; it is an honor to work alongside such outstanding individuals within our company. Our strength lies in the character of our people and our relentless pursuit of our mission.