China's Rheumatoid Arthritis Biologics Market: High Unmet Demand Calls for Lower Originator Prices and Accelerated Biosimilar Launches

Biologics have emerged as a rapidly advancing sector in the pharmaceutical industry in recent years, with a key application being the treatment of autoimmune diseases, including rheumatoid arthritis and ankylosing spondylitis. However, the market performance of originator biologic agents in China has been underwhelming, even for Humira, which has ranked as the world’s top-selling drug for seven consecutive years.

RA and AS Have High Incidence Rates in China but Lack Effective Curative Treatments

Rheumatoid Arthritis (RA) is an autoimmune disease characterized primarily by erosive arthritis. Patients with RA ultimately develop joint deformities and loss of function, and may also suffer from comorbidities such as pulmonary diseases, cardiovascular diseases, malignant tumors, and depression. Epidemiological surveys indicate that the incidence of RA in China is 0.42%, with a total affected population of approximately 5 million. Ankylosing Spondylitis (AS) is a chronic inflammatory disease that primarily affects the sacroiliac joints, spinal facet joints, paraspinal soft tissues, and peripheral joints, and may be accompanied by extra-articular manifestations; severe cases can lead to spinal deformity and ankylosis. Preliminary surveys suggest a prevalence of around 0.3% in China. Currently, the pathogenesis of both RA and AS remains unclear, precluding a complete cure. Instead, management focuses on treat-to-target strategies to control disease activity, reduce disability rates, and improve patients' quality of life.

The use of biologic DMARDs can effectively control the disease.

According to China’s treatment guidelines for rheumatoid arthritis (RA) and ankylosing spondylitis (AS), pharmacological regimens primarily include four categories of medications: nonsteroidal anti-inflammatory drugs (NSAIDs), disease-modifying antirheumatic drugs (DMARDs), glucocorticoids, and herbal medicines. Among these, DMARDs are classified into synthetic DMARDs and biologic DMARDs. Although glucocorticoids possess potent anti-inflammatory and immunosuppressive effects that can rapidly alleviate patients’ conditions, their significant adverse effects associated with long-term use have led clinicians to rarely employ them in treatment over extended periods. In contrast, biologic DMARDs, as targeted therapies, demonstrate considerable clinical advantages. Trial data indicate that monotherapy with TNF-α inhibitor biologic DMARDs or their combination with conventional synthetic DMARDs can effectively alleviate symptoms, with most RA or AS patients achieving clinical remission or low disease activity within 3 to 6 months. Furthermore, biologics exhibit a relatively high safety profile and fewer side effects in clinical practice.

Current Status and Causes of Biologic Products in China

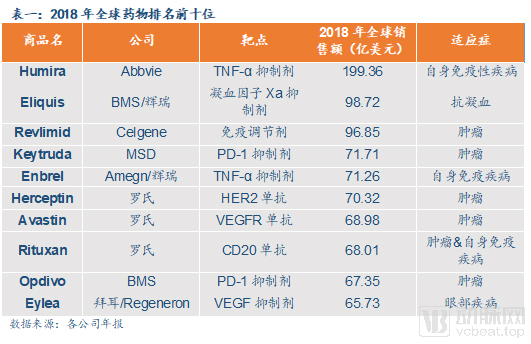

Current Situation: Biologics occupy multiple spots among the top 10 drugs globally, yet their sales remain sluggish in the Chinese market.

Among the top ten global pharmaceutical products in 2018, three were related to autoimmune diseases: AbbVie’s Humira, Pfizer’s Enbrel, and Roche’s Rituxan. All three drugs are indicated for rheumatoid arthritis (RA) and ankylosing spondylitis (AS). Notably, Humira ranked first for seven consecutive years, with sales of $19.9 billion, surpassing the second-place product by $10 billion. Enbrel and Rituxan ranked fifth and eighth, respectively, with sales of approximately $7.1 billion and $6.8 billion.

However, a review of the domestic biologics market reveals that sales of these originator products have been lackluster; even Humira, the global “blockbuster king,” has encountered sluggish sales in China.

Reason: High treatment costs and other factors have suppressed the sales performance of originator products.

As can be seen from the aforementioned sales figures, there remains a substantial gap between the sales revenue of these originator biologics, which have been marketed in China for many years, and that of domestically produced biosimilars. The primary reasons are reflected in the following aspects:

Reason 1: The treatment cost of the original research product is expensive.

Excluding patient assistance programs (PAPs), the annual cost of originator biologics for patients exceeds RMB 100,000, reaching as high as RMB 220,000. In contrast, domestically produced biosimilars are significantly more affordable, with the most expensive option, Etanercept, costing less than RMB 100,000 per year, at approximately RMB 80,000. Given that rheumatoid arthritis requires lifelong medication, the prohibitive treatment costs have deterred the majority of domestic patients from using originator products.

The Patient Assistance Program (PAP) for the originator product offers substantial discounts but has a narrow scope of eligibility. When accounting for PAP, the annual cost for patients using the originator product decreases significantly, with a maximum reduction of up to 68%. However, on one hand, the stringent eligibility criteria for PAP limit its actual applicability to a small patient population; on the other hand, even after PAP subsidies, the out-of-pocket costs remain difficult for most patients to afford.

Reason 2: The originator product failed to be successfully included in the National Reimbursement Drug List

In early 2017, TNF-α inhibitors (generic name: recombinant human type II tumor necrosis factor receptor-antibody fusion protein for injection) were included in the updated National Reimbursement Drug List of China, meaning that the annual cost for patients using domestically produced biosimilars would further decrease. Additionally, after these domestically produced biosimilars were covered by national medical insurance, their annual cost became more affordable for many patients who had previously been treated with nonsteroidal anti-inflammatory drugs (NSAIDs), thereby facilitating a shift in their treatment regimens.

In contrast, the originator product has been excluded from the National Reimbursement Drug List (NRDL). Although it is covered by certain provincial basic medical insurance or critical illness insurance schemes, its impact remains limited due to restricted geographic coverage and a small patient population. Moreover, many patients still struggle to afford the annual out-of-pocket costs even after reimbursement. Consequently, the actual sales performance has been negligible.

Reason 3: Insufficient Staffing in the Sales Team for the Originator Product

For pharmaceutical companies, the size of the sales team directly influences hospital formulary inclusion, which is subsequently reflected in product sales figures. In China, biosimilar manufacturers, benefiting from earlier market entry and ample time for strategic planning, have either established their own sales teams or adopted a hybrid model combining in-house teams with third-party agencies to expand hospital coverage and boost sales. In contrast, originator manufacturers rely solely on smaller in-house sales teams, resulting in significantly reduced coverage and promotional efficiency.

Overall, the high cost of treatment has raised the financial barrier for patients to choose originator products, limiting access for the vast majority of patients and serving as the primary reason for the sluggish sales of originator products in the Chinese market. Meanwhile, after domestic biosimilars were included in the National Reimbursement Drug List, the price gap between them and originator products widened further, thereby solidifying the industry position of domestic biosimilars. Additionally, leveraging their advantage in sales force size, domestic biosimilars have continuously expanded their hospital coverage, which not only stabilizes their own market position but also constrains the market share of originator products.

Forecast of Future Trends in China's Biologics Market

The “2018 Treatment Guidelines for Rheumatoid Arthritis” indicate that the utilization rate of biologic DMARDs in North America is 50.7%, whereas a rheumatology and immunology registry study in China shows that the utilization rate of biologic DMARDs in China is only 8.3%. It is estimated that the market size of the biologic agents sector in China will reach RMB 30 billion, with the market size of TNF-α inhibitors in China expected to reach RMB 20 billion. However, according to 3SBio’s annual report, Etanercept (Yisaipu) achieved sales of RMB 1.111 billion in 2018, accounting for approximately 60% of the market share. Based on this, the domestic market size for biologic agents is estimated to be less than RMB 2 billion. This demonstrates that there remains substantial unmet demand in China’s biologic agents market, which is the primary reason why both originator manufacturers and Chinese domestic manufacturers are vying to capture share of the domestic biologic agents market.

Trend 1: If existing originator biologics are included in the National Reimbursement Drug List, their sales may increase significantly

On March 13, the National Healthcare Security Administration released the “Work Plan for Adjusting the National Reimbursement Drug List in 2019 (Draft for Comments)” for public consultation, marking the official launch of the 2019 adjustment process. Following the failure of medical insurance negotiations in 2017, original-equipment biological product manufacturers urgently need to determine how to formulate new negotiation strategies. Although successful negotiations depend on many factors, price reduction has become a de facto prerequisite for inclusion in the reimbursement list. For high-priced products such as biologics, the market generally predicts that price cuts could reach 50% or even higher.

As most patents for originator products expired in 2018 or earlier, numerous domestic pharmaceutical companies have initiated clinical trials for biosimilars, posing a significant challenge to the current sales performance of these originator products. Consequently, inclusion in the National Reimbursement Drug List (NRDL) has become a critical strategy for manufacturers of originator biologics to alter the current market landscape. Successful inclusion in the NRDL would drive a substantial increase in drug sales volume, offsetting the adverse effects of price reductions and thereby gradually achieving growth in sales revenue.

From the perspective of current policy guidance, the National Healthcare Security Administration is intensifying efforts to include exclusive innovative drugs in its coverage. Therefore, the likelihood of existing originator products being included in the national reimbursement list remains considerable. However, inclusion in the reimbursement list does not mean that pharmaceutical companies have completed their tasks; how to expand hospital access and further increase sales volume will become the primary issues for pharmaceutical companies to address in the subsequent stages.

Trend 2: Accelerated Clinical Trial Progress of Domestically Produced Biosimilars, with Market Launches Expected to Begin in 2019

The domestic market for biologics holds immense potential, and with the patents of many originator products expiring, it has attracted significant attention from Chinese biopharmaceutical companies. Currently, clinical trials for biologic DMARDs in autoimmune diseases are primarily focused on TNF-α inhibitors and tocilizumab, while research is also underway on biosimilars targeting CD20 monoclonal antibodies, CTLA-4, and other targets.

TNF-α inhibitors under development in China can be categorized into three types based on drug class: 1. Etanercept biosimilars (fusion proteins): In addition to the three pharmaceutical companies with already marketed products, Qilu Pharmaceutical is making the fastest progress, having entered Phase III clinical trials. 2. Infliximab biosimilars: Genor Biopharma is currently conducting Phase III clinical trials. 3. Adalimumab biosimilars: Numerous enterprises are engaged in R&D, with at least 27 companies developing such agents. Among them, Bio-Thera Solutions has made the most rapid progress, filing for marketing approval in August 2018, followed closely by Hisun Pharmaceuticals, Innovent Biologics, and Henlius Biotech, which have also submitted marketing applications.

Tocilizumab Biosimilars: In addition to Jinyu Bio and Bio-Thera Solutions, which have both entered Phase III clinical trials, four other domestic biopharmaceutical companies are in Phase I clinical trials. This indicates that adalimumab biosimilars could be launched and go on sale as early as the end of 2019, while companies are already conducting Phase III clinical trials for other types of biosimilars.

Pricing Strategy: The R&D costs for domestically produced biosimilars in China are significantly lower than those for originator biologics. This allows Chinese manufacturers to maintain substantial profit margins even after reducing prices, similar to the pricing relationship between etanercept and its biosimilars. Furthermore, given the significant supply gap in the domestic biologic market, Chinese pharmaceutical companies can still achieve considerable returns despite price reductions. Consequently, it is expected that domestic pharmaceutical firms will continue to adopt a low-price market entry strategy to capture market share. Meanwhile, if a pharmaceutical company can break through the competition and become the first domestic manufacturer of a specific biosimilar, it will not only enjoy pricing autonomy but also benefit from substantial market growth potential.

Trend 3: Who Will Be the Ultimate Beneficiaries of This Feast?

As major pharmaceutical companies compete to capture the biologics market and diversify their product portfolios, patients are undoubtedly the primary beneficiaries. Since autoimmune diseases cannot be cured and require long-term medication for disease control, an increased variety of available products—particularly as numerous domestic pharmaceutical companies embark on the development of biosimilars—will drive prices down further. This will enable more patients to afford biologic therapies, rather than having to rely continuously on non-steroidal anti-inflammatory drugs (NSAIDs) or glucocorticoids, which carry greater side-effect burdens, for symptom relief.

Faced with a significant market gap, domestic pharmaceutical companies can quickly recoup their relatively low R&D costs and achieve profitability, making them undeniable beneficiaries of this competition. However, in the future, besides enduring the long wait for marketing approval, domestic pharmaceutical companies must also address challenges such as inclusion in the national medical insurance scheme and hospital formulary adoption. Meanwhile, as the number of market participants increases and competitive pressure intensifies, achieving sustained sales growth and maintaining market share will be the next critical challenge for domestic pharmaceutical companies to resolve.

Author: Ryan Partners

Ryan Partners is composed of professionals dedicated to management consulting and research, focusing on vertical industries such as pharmaceuticals and healthcare, fast-moving consumer goods (FMCG), manufacturing, and digital new media. Leveraging specialized expertise and services, the firm provides clients with comprehensive solutions, including global market research, market access strategies, market potential assessments, and other business intelligence offerings.