Will Convenience Stores Reshape the OTC Drug Retail Landscape? Insights from Suning, Watsons, and Mannings' Entry into Pharmaceutical Sales

Not long ago, the General Office of the State Council issued the “Opinions on Accelerating the Development of Circulation to Promote Commercial Consumption,” which mentioned accelerating pilot programs for streamlining approval procedures for the retail of Class B over-the-counter (OTC) drugs. The new policy has brought fresh business opportunities for chain convenience stores, but has caused concern within the retail pharmacy industry. Already struggling with sluggish growth under the dual pressures of the “4+7” volume-based procurement program and pharmaceutical e-commerce, the pharmacy sector now appears poised to face yet another wave of competition.

VCBeat’s analysis suggests that selling medications in convenience stores still faces numerous challenges under current conditions and is unlikely to significantly impact the pharmaceutical retail market in the near term. The key points are as follows:

1. Convenience stores have been retailing Class B over-the-counter (OTC) drugs since 1999. Although many attempts were made during this period, most of them ultimately came to nothing;

2. The introduction of new policies in Beijing in October 2018 sparked a new wave of application surges, but apart from Wumart, most convenience stores only dabbled briefly;

3. There are many challenges for convenience stores to enter the pharmaceutical retail market, such as issues with medical insurance payment, pharmaceutical care services, and operational management;

4. The market share that convenience stores can capture is only about RMB 40 billion, accounting for just 4.4% of the total pharmaceutical market;

5. Japan’s mature drugstore industry owes its success to capturing nearly the entire over-the-counter (OTC) medication market, whereas the market segment accessible to convenience stores in China is significantly smaller, making it difficult to sustain a stable customer flow;

6. Drugstores in Japan, South Korea, and Hong Kong, China should be referred to as “pharmacies that sell non-pharmaceutical products.” Pharmaceuticals primarily serve to drive foot traffic, while non-pharmaceutical products are the main source of profit.

As early as June 1999, the “Measures for the Classified Administration of Prescription Drugs and Over-the-Counter Drugs (Trial)” stipulated that other commercial enterprises approved by the provincial drug regulatory authorities or their authorized drug regulatory departments may retail Category B over-the-counter drugs.

In the subsequent years, various regional chain convenience stores also made attempts in this area, but with limited success. For instance, Hebei Guoda Chain Commerce, Wuhan’s Zhongbai Convenience Supermarkets, Chengdu’s wowo Convenience Stores and Hongqi Chain, and Fujian’s Yitai Chain Convenience Stores all tried selling Class B over-the-counter (OTC) drugs within their convenience stores or supermarkets. Most of these initiatives eventually faded from public view, with some explicitly announcing their discontinuation.

In November 2018, the Department of Market Order under the Ministry of Commerce released the “Guiding Opinions on Classified and Graded Management of Retail Pharmacies Nationwide (Draft for Comments),” which clearly categorized retail pharmacies into three classes. Class I pharmacies are permitted to sell Class B over-the-counter (OTC) drugs; Class II pharmacies may sell OTC drugs, prescription drugs (excluding prohibited and restricted medications), and traditional Chinese medicine (TCM) decoction pieces; Class III pharmacies may sell OTC drugs, prescription drugs (excluding prohibited medications), and TCM decoction pieces. Therefore, the primary competitors for convenience stores selling pharmaceuticals are limited to Class I pharmacies, while competitive relationships with Class II and Class III pharmacies are not significant.

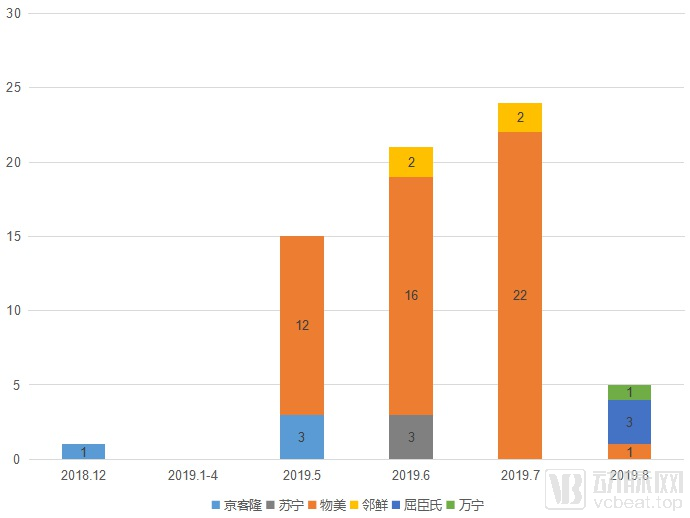

The “Several Measures to Further Promote the Development of Convenience Stores,” jointly issued by seven Beijing municipal departments in October 2018, served as the catalyst for the new wave of convenience stores selling pharmaceuticals. The Measures stipulated that restrictions on food and drug operations should be relaxed; chain convenience stores could apply to retail Category B over-the-counter (OTC) drugs in accordance with relevant standards, and enterprises applying for Class II medical device operation filing could centrally assign quality management personnel at their corporate headquarters. Following the issuance of this document, Jingkelong became the first chain convenience store to obtain a Drug Operation License in December 2018 after the promulgation of the new regulations.

Chain Convenience Stores That Obtained the "Drug Operation License" After Beijing's New Policy

As of August 2019, six convenience store brands had obtained the relevant qualifications to sell pharmaceuticals in Beijing. After Jingkelong opened its first pharmacy-enabled convenience store, no additional registered stores emerged from January to April 2019. It was not until May 2019 that Wumart made an aggressive entry into the pharmacy convenience store sector, applying for the necessary licenses for 12 of its stores in the first month alone and rapidly expanding to 51 locations over the following four months. Apart from Wumart, other convenience store chains adopted a more cautious approach to pharmaceutical retail; Jingkelong and Linxian each launched operations in only four stores.

Suning Xiaodian, which partnered with Fosun Group in April, entered the convenience store pharmaceuticals market in June. In August, Watsons and Mannings applied for relevant qualifications for three and one of their respective convenience stores. Suning, Watsons, and Mannings have already entered the pharmaceutical retail sector through online pharmaceutical e-commerce or pharmacy supermarkets. As a new scenario in pharmaceutical retail, selling medicines in convenience stores has naturally attracted the interest of these chain convenience store operators. However, they have not yet made in-depth strategic deployments and are currently only conducting pilot trials in a select number of stores.

On the surface, it appears that convenience stores selling pharmaceuticals will deliver a new blow to retail pharmacies already in crisis. However, careful analysis reveals that convenience stores still face numerous challenges to overcome as they enter the pharmaceutical retail sector.

First, medical insurance coverage is limited, requiring consumers to pay out of pocket.

Consumers must pay out of pocket for medications at convenience stores, whereas pharmacies accept medical insurance payments. Intuitively, consumers are more inclined to purchase medications from pharmacies that allow medical insurance coverage.

Theoretically, there is an opportunity for convenience stores to integrate their information systems with the national medical insurance network. However, the National Healthcare Security Administration (NHSA), which is currently cracking down on the sale of non-pharmaceutical products in pharmacies, appears to lack the bandwidth to promote such integration for convenience stores. Although the NHSA has given the green light to new healthcare access channels such as internet-based medical services, given the regulatory challenges associated with convenience stores, it is unlikely that they will receive medical insurance support in the short term.

Second, the abundance of pharmacies and specialized pharmaceutical services renders convenience store drug sales uncompetitive.

The lack of professional pharmaceutical care services may be a critical weakness for convenience stores entering the drug retail market. Although Class B over-the-counter (OTC) drugs are the safest category among pharmaceuticals, consumers still prioritize related pharmaceutical care services when making purchases, rather than focusing primarily on speed and convenience. Given the cost constraints faced by convenience stores and the limited number of licensed pharmacists in China, it is impractical for convenience stores to hire pharmacists solely for the purpose of selling medications.

From a convenience perspective, convenience stores do not appear to be more accessible than retail pharmacies. Although there are as many as 5 million convenience stores of various sizes across China, only 120,000 meet the relevant standards and are eligible to apply for permission to sell pharmaceutical products. In contrast, China has a total of 489,000 retail pharmacies. This means that the coverage of pharmacies is significantly higher than that of convenience stores authorized to sell medications. Therefore, whether in terms of meeting patients’ medication needs or overall accessibility, retail pharmacies hold a clear advantage over convenience stores.

Third, convenience stores need to adapt to the low-frequency consumption pattern of pharmaceuticals.

When Jingkelong opened its first convenience store with pharmaceutical operations, a relevant official from the Beijing Chaoyang District Commission of Commerce stated that only “chain convenience stores operated within large commercial districts or major shopping malls, and with a pharmaceutical sales area of no less than 20 square meters,” were eligible to apply for permission to sell medicines. For a convenience store of approximately 100 square meters, it is quite difficult and challenging to carve out a dedicated 20-square-meter zone for pharmaceutical sales through simple adjustments without disrupting the existing product layout.

Most products sold in convenience stores are fast-moving consumer goods (FMCG), which cater to high-frequency consumer demand. Shoppers often pick up everyday items on impulse while browsing these stores. In contrast, pharmaceuticals represent low-frequency demand; it is highly unlikely that consumers would casually purchase a box of medication to “take over time” during a routine convenience store visit. This consumption pattern is inherently incompatible with the operational model of convenience stores. Furthermore, FMCG typically have an inventory turnover cycle of 2–3 weeks, whereas pharmacies generally experience a turnover cycle of 8–12 weeks. For convenience stores to enter the pharmaceutical retail market, they must not only designate specific areas for drug sales but also adapt to the distinct sales methods and rhythms associated with medications. These factors pose significant challenges for convenience stores seeking to expand into pharmaceutical retail.

“Targeting a Market Worth Hundreds of Billions” is a phrase frequently cited in reports on convenience stores selling pharmaceuticals. The retail pharmacy market was projected to reach RMB 400 billion in 2019, and this figure is often used as a benchmark to gauge the market potential for convenience stores entering the drug retail sector. However, even if convenience stores overcome various challenges and successfully enter the pharmaceutical retail market, the addressable market will fall far short of the “hundreds of billions” mark, as restrictions limiting them to Class B over-the-counter (OTC) drugs significantly shrink this potential.

In China, drugs are classified and regulated as either prescription or over-the-counter (OTC) medications based on factors such as drug type, specifications, indications, dosage, and route of administration. Furthermore, OTC drugs are subdivided into Class A and Class B categories according to their safety profiles, with Class B drugs exhibiting a higher level of safety. However, the market share of Class B drugs remains very limited within the overall pharmaceutical market.

In the "2018 China OTC Drug Enterprises and Products List" released by the China Non-Prescription Drug Association (CNPA) at the end of 2018, 295 best-selling over-the-counter (OTC) drugs were announced, among which only 92 belonged to Class B OTC drugs. Based on this, it is estimated that Class B OTC drugs accounted for approximately 31% of the total OTC drug market. The CNPA mentioned in an event that the total size of China's OTC drug market in 2017 was RMB 280 billion. Therefore, it is inferred that the overall market size of Class B OTC drugs in 2017 was approximately RMB 87.3 billion, accounting for only 4.4% of the total pharmaceutical market.

In reality, the market accessible to convenience stores for pharmaceutical sales is smaller than RMB 87.3 billion. The market space that convenience stores can compete for is limited to the out-of-hospital segment, primarily corresponding to the current market size of retail pharmacies. According to monitoring data from relevant institutions, China’s medical retail terminal market totaled RMB 366.4 billion in 2017, of which the pharmaceutical market accounted for RMB 268.8 billion. Over-the-counter (OTC) drugs represented 49.81% of retail pharmaceutical sales, amounting to RMB 134 billion. Further applying the 31% share of Class B OTC drugs, the actual market size accessible to convenience stores is only RMB 41.54 billion, equivalent to 11.3% of the retail pharmacy market and 2.1% of the overall pharmaceutical market.

Compared with the convenience store market, which is valued at RMB 200 billion, this RMB 40 billion segment is highly attractive. However, for retail pharmacies, prescription drugs and Class A over-the-counter (OTC) medications still constitute the primary source of their revenue, making it difficult for convenience stores to undermine the foundational position of retail pharmacies in the market.

Given the high difficulty of capturing share in the existing market, chain convenience stores may find new entry points under the new policy. Among Class B over-the-counter (OTC) drugs, in addition to products with strong pharmaceutical attributes such as aspirin, glycerin enemas, and ibuprofen cream, a significant portion possesses certain health supplement characteristics, such as various vitamin tablets, donkey-hide gelatin (Ejiao) products, and motherwort paste. These products have the potential to create new markets through convenience store promotions, being marketed to consumers in the form of health supplements.

At this juncture, retail chains specializing in health and beauty products, such as Watsons and Mannings, may find certain opportunities. They have already cultivated a highly loyal customer base through their existing service offerings and possess considerable familiarity with the sale of health supplements. Their store sizes and locations also comply with the relevant requirements for licensing qualifications. Through appropriate training, sales associates can gain an understanding of the target demographics, indications, and contraindications of the pharmaceutical products stocked in-store, thereby enabling them to recommend suitable medications to consumers with corresponding needs.

When discussing the sale of medications in convenience stores, it is impossible not to mention Japan, China’s neighbor. Japan’s mature drugstore and cosmetics store system has long been regarded as the future direction for retail pharmacies in China. Japan began implementing the separation of prescribing and dispensing in the 1980s, and over the following three decades, the prescription fulfillment rate (an indicator of the efficiency of prescription outflow) rose rapidly, from 11.3% in 1989 to 70% in 2015.

During the process of separating medical services from pharmaceutical sales, Japan’s terminal drug market underwent gradual changes. A distribution pattern comprising dispensing pharmacies and drugstore chains gradually took shape, with each assuming distinct functions. Dispensing pharmacies are responsible for selling medicines covered by health insurance and prescription drugs, while drugstore chains primarily sell over-the-counter (OTC) medications, cosmetics, daily chemical products, and other general consumer goods.

Dispensing pharmacies in Japan are equivalent to retail pharmacies in China. The outflow of prescriptions has created substantial market opportunities for Japanese dispensing pharmacies. In 2017, 811 million prescriptions were dispensed outside hospitals in Japan, with the total value of filled prescriptions reaching JPY 7.9 trillion. The sales revenue of Japanese drugstores amounted to JPY 6.8 trillion in 2017, with pharmaceuticals contributing 32% of this figure, while the remainder comprised cosmetics, daily sundries, and other products. This indicates that the over-the-counter (OTC) drug market in Japan was approximately JPY 2.2 trillion. The ratio of prescription drugs to OTC drugs was roughly 4:1, which is relatively close to the overall ratio in China.

Japan’s mature drugstore industry benefits from a clear market division driven by the outflow of prescriptions. Dispensing pharmacies sell prescription drugs, while drugstores handle over-the-counter medications.Therefore, for China, if it follows Japan’s development model, retail pharmacies will not transform into drugstores carrying cosmetics and daily necessities; rather, they will evolve toward dispensing pharmacies, taking over prescriptions flowing out from hospitals, while large chain convenience stores will move in the direction of drugstores, incorporating the over-the-counter (OTC) drug market. However, judging by the current revenue structure of domestic retail pharmacies, OTC drugs still account for a significant share of their income, and hospitals have yet to identify appropriate mechanisms for prescription outflow. Thus, while Japan’s terminal market structure—comprising dispensing pharmacies and drugstores—is indeed one of the developmental directions for China, establishing a pharmaceutical separation system similar to Japan’s still appears to be a distant goal.

Japan’s 2009 “Amended Pharmaceutical Affairs Law” bears some resemblance to China’s recent policy allowing convenience stores to sell medicines. The Amended Law streamlined the existing regulatory framework for drug sales, categorizing pharmaceuticals into prescription drugs, over-the-counter (OTC) drugs (Class A OTC), and general-use medicines (Class B OTC). For general-use medicines, the requirement for licensed pharmacists was relaxed, permitting registered sales personnel to handle sales (thus, convenience stores in Japan do not need licensed pharmacists to sell Class B OTC drugs). Despite this deregulation, convenience stores have failed to capture a significant share of Japan’s pharmaceutical retail market over the past decade. In light of this precedent, it is likely to be challenging for convenience stores in China to establish a strong foothold in the pharmaceutical distribution sector.

Pharmacies and convenience stores also differ fundamentally in nature.In Japan, South Korea, Hong Kong (China), and other regions, drugstores are not convenience stores that sell pharmaceuticals; rather, they are pharmacies that generate profits primarily from non-pharmaceutical products.The business logic of the drugstore industry is to attract customers into stores through essential products like pharmaceuticals, and then generate profits by selling non-pharmaceutical products. Pharmaceuticals account for a certain proportion of total turnover but yield slim margins, primarily serving as a traffic driver. The drugstore industries in South Korea and Hong Kong, China, operate under the same model.

However, this model has yet to reach a consensus in China. The sale of non-pharmaceutical products by pharmacies covered by medical insurance has long been an ambiguous issue, with policies fluctuating repeatedly. Relaxing regulations would allow consumers to purchase non-pharmaceutical items using medical insurance funds, thereby increasing the financial burden on the system; conversely, tightening regulations would reduce pharmacy profits and hinder the development of retail pharmacies. Amidst this hesitation, the growth of China’s retail pharmacy sector has stalled at this critical juncture.

In December 2018, as Jingkelong began selling pharmaceuticals, Watsons also opened its first offline pharmacy on the Chinese mainland in Foshan. Offering a comprehensive range of products—including prescription drugs, health supplements, food items, dermocosmetics, and personal care products—the store presented the image of a mature health and beauty retailer. While this move by Watsons may have been somewhat impulsive, it might have already discovered a strategy to break through the competitive landscape of retail pharmacies on the mainland, making its first strategic move on this grand chessboard.