Escalating Battle: Global Landscape and Product Pipeline of Oligonucleotide Therapeutics

Ribo Life Science

Small Nucleic Acid Drug Developer

Biogen

New Drug Developer

In 2026, China's small nucleic acid drugs officially entered the "capital meta-year.", the track's popularity continues to rise.

The successful listing of Ribo Life Science marks the official entry of small nucleic acid drugs into China's capital market, injecting a boost into the industry; just days later, China Biologic Products made another significant move, acquiring Hergy Bio, a domestic siRNA innovative drug company, for a total price of 1.2 billion yuan. This action undoubtedly adds fuel to the explosive growth of this emerging track.

As the third major drug form following small molecule drugs and antibody drugs, small nucleic acid drugs have become a core track in global biopharmaceutical innovation due to their unique advantages of precise targeting and broad therapeutic spectrum.As the attention from China's capital market continues to deepen, what is the state of play in the more mature global market?

01 Tripartite Powerhouse

The current global small nucleic acid drug market is showing distinct"Tripartite Dominance" Pattern: Alnylam, Ionis, SareptaThree companies have long occupied a dominant position in the industry by virtue of their technical barriers and commercialization advantages.

As of the end of 2025, a total of 19 small nucleic acid drugs have been approved for marketing worldwide, mostly developed by these three pharmaceutical companies. Relying on their early technical accumulation, mature delivery platforms, and extensive clinical experience, they have built insurmountable competitive barriers, deeply dominating the global research and development direction and commercialization process of small nucleic acid drugs.

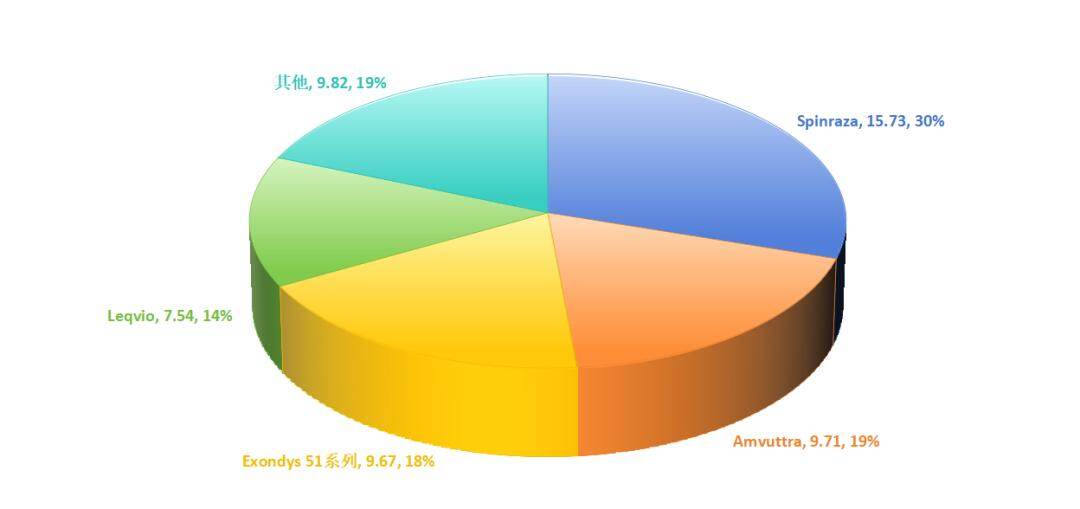

In terms of market share, the global sales of small nucleic acid drugs reached 5.247 billion US dollars in 2024. Among them, Spinraza (Nusinersen), co-developed by Ionis and Biogen, accounted for 30% with sales of 1.573 billion US dollars; Amvuttra (Vutrisiran) from Alnylam accounted for 19% with sales of 971 million US dollars; the series of drugs for treating Duchenne Muscular Dystrophy (DMD) from Sarepta achieved sales of 967 million US dollars, accounting for 18% of the total sales.

Figure: 2024 Global Small Nucleic Acid Drug Landscape (USD billion), Source: Jinduan Research Institute

Antisense oligonucleotides (ASO) and small interfering RNA (siRNA) are the two mainstream technological approaches for small nucleic acid drugs at present. Both core mechanisms involve targeting mRNA to regulate gene expression, achieving precise disease treatment, and each has structural and mechanistic differences.

ASO is a single-stranded nucleic acid structure, typically 18 to 30 nucleotides in length, and functions through three pathways: binding with the nuclease RNase H to degrade target mRNA, regulating the splicing pattern of pre-mRNA, and occupying the target mRNA to inhibit translation; siRNA, on the other hand, is a double-stranded nucleic acid structure, approximately 20 to 25 nucleotides long, with the core mechanism being the formation of an RNA-induced silencing complex (RISC) by binding with intracellular nucleases, which then specifically degrades target mRNA. The differences in technical characteristics also determine their respective advantages in application.

As the leader in RNAi therapy research and development, Alnylam is undoubtedly the "front-runner" among the three giants.`, whose efficient R&D system and technical iteration capabilities have built up core competitiveness.`

Alnylam was founded in 2002 and spent the first 15 years of its existence focusing on the drug development pathway for small nucleic acid drugs, during which time it had a relatively low profile. It wasn't until 2018, when the U.S. FDA approved its first drug, ONPATTRO (for the treatment of hereditary transthyretin-mediated amyloidosis, hATTR), followed by the subsequent approvals of Lumasiran, Givosiran, Inclisiran, and Vutrisiran, that the company rose to become a star enterprise in the small nucleic acid field.

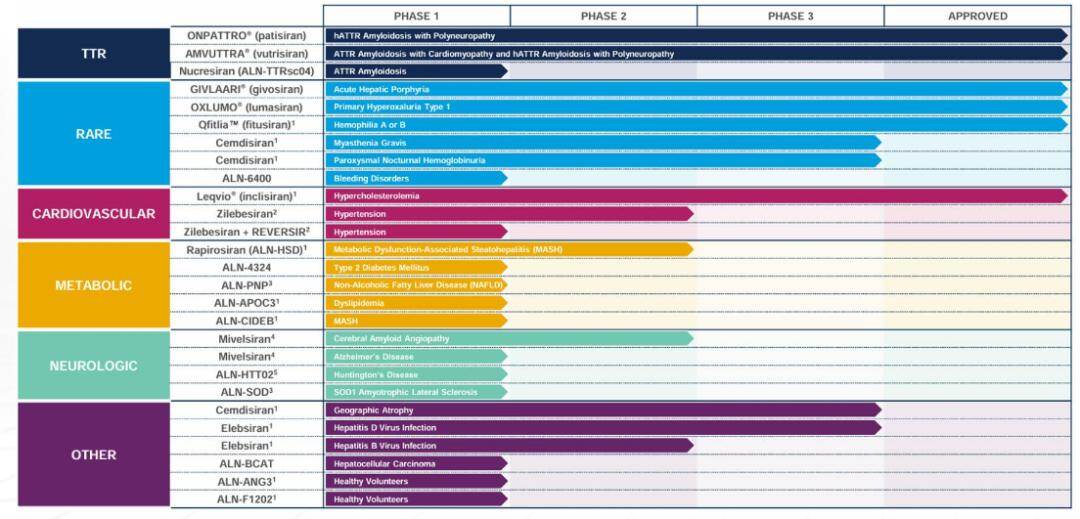

As a pioneer in the GalNAc delivery system, Alnylam has achieved rapid product iteration through this core technology platform and successfully obtained approval for six siRNA drugs by 2025, covering multiple therapeutic areas including rare diseases, cardiovascular, and metabolic conditions.

Figure: Overview of Alnylam's R&D pipeline, Source: CICC Securities

More notably, Alnylam’s clinical translation efficiency demonstrates a significant advantage — the cumulative conversion rate from Phase I to Phase III is as high as 64.3%, more than 10 times the industry average of 5.7%. This highly efficient R&D system allows it to maintain a leading position in competitive fields. The company has explicitly stated its goal to solve RNAi delivery challenges for all major tissues by 2030, extending its therapeutic focus from rare diseases to broader areas such as chronic conditions and neurological disorders.

Ionis takes ASO technology as its core competitiveness,With its technical characteristics, it occupies a unique position in the small nucleic acid field, especially with a first-mover advantage in targeting treatments for organs outside the liver.

Unlike Alnylam's siRNA drugs, ASO single-stranded nucleic acid molecules can freely penetrate cell membranes, showing lower dependence on delivery systems. Their target organs are not limited to the liver but also cover extrahepatic tissues such as muscles and the central nervous system. This characteristic gives them a natural advantage in treating central nervous system diseases and muscular disorders. As early as 1998, Ionis launched the world’s first ASO drug, fomivirsen. Of the 12 ASO drugs currently approved globally, nine originate from this company, including Spinraza, which targets spinal muscular atrophy and has achieved remarkable sales as the highest-grossing small nucleic acid drug.

In addition, Ionis continues to advance the iteration of chemical modification technologies, from the first-generation fluorine modification, the second-generation 2’MOE modification, to the 2.5-generation cEt and LNA technologies, continuously optimizing drug efficacy, reducing toxic side effects, and further strengthening its technical barriers. Notably, Bepirovirsen, which is under GSK and is expected to become the world's first functional cure for hepatitis B, is an ASO therapy licensed from Ionis. Both of its Phase III clinical trials have achieved key endpoints, with plans to submit a marketing application in the first quarter of 2026, demonstrating the commercial value of Ionis' technology platform.

The third player, Sarepta, focuses on the field of muscular diseases.Establish a solid foothold with a differentiated strategy of "technology deepening + indication focus" to become a leader in the treatment of Duchenne Muscular Dystrophy (DMD).

In 2012, Sarepta shifted its strategic focus to the rare disease field, officially embarking on an innovative journey in small nucleic acid drugs, and gradually growing into a representative company of small nucleic acid therapies in the United States. To date, the company has successfully developed and commercialized four DMD treatment drugs: Exondys 51, Vyondys 53, Amondys 45, and Elevidys. The first three RNA exon-skipping therapies were approved by the FDA in 2016, 2019, and 2021, respectively. However, it should be noted that in 2025, the FDA suspended the shipment of Elevidys due to safety concerns, and the European Medicines Agency also refused to approve the drug for marketing based on efficacy considerations, posing certain challenges to its commercialization process.

Strong product strength drives rapid growth in performance. In 2024, Sarepta's revenue reached $1.9 billion, a year-over-year increase of over 50%. RNA therapy was the core source of income, confirming the commercial viability of its focused strategy. Additionally, the company obtained its first FDA recognition for a gene therapy vector platform technology in 2025, laying the foundation for future pipeline expansion.

02 Blockbuster in the Making

The global small nucleic acid drug market has entered a period of concentrated commercial realization, with growth momentum continuing to be released. In 2024, the global small nucleic acid drug market size reached 5.247 billion U.S. dollars. It is predicted that by 2033, this size will climb to 46.7 billion U.S. dollars, with a compound annual growth rate as high as 25% during this period. However, it is worth noting that currently marketed products are still concentrated in niche areas such as rare diseases, with targets mainly being new types. Market awareness and penetration still require long-term cultivation, and the track has not yet broken through the "niche circle."

From the perspective of the development pattern of the pharmaceuticals industry,A phenomenal "blockbuster product" is often the key driver in propelling a niche market from "niche" to "mainstream.", which can not only break the market ceiling but also attract resources such as capital and technology to accelerate their aggregation, driving the upgrading of the entire industry chain. For small nucleic acid drugs to achieve this leap, they similarly and urgently need a blockbuster product to break the deadlock.

Considering the current pipeline progress and commercial performance, Spinraza, co-developed by Ionis and Biogen, has long ranked at the top in sales. However, its growth momentum is slowing down, with sales showing a declining trend, and the gap with subsequent products is gradually narrowing. By comparison,Alnylam's core product Amvuttra and Novartis' PCSK9-targeted drug Leqvio,With differentiated advantages and strong growth potential, it has become the most competitive "blockbuster seed player."

As the world's first small nucleic acid drug to achieve annual sales exceeding $1 billion, Spinraza pioneered the commercialization of its category. Since its launch in 2016, its cumulative sales have surpassed $10 billion, with peak sales reaching $2.097 billion in 2019. Its core indication is spinal muscular atrophy (SMA). However, constrained by the limited size of the SMA patient population, the high cost of the product, and competition from Roche's Evrysdi and Novartis' Zolgensma, which have diverted market share, Spinraza’s sales have gradually declined, dropping to $1.573 billion in 2024, putting its leading position under pressure.

Amvuttra, as a core siRNA drug under Alnylam, demonstrates strong growth resilience with its technological advantages and excellent commercial performance. This drug was approved for marketing in 2022, targeting both mutant and wild-type transthyretin (TTR) mRNA, and is used to treat adults with hereditary transthyretin-mediated (hATTR) amyloidosis with stage 1 and 2 polyneuropathy. Its core competitiveness lies in the use of GalNAc delivery technology, enabling subcutaneous injection once every three months, which significantly reduces dosing frequency compared to traditional therapies and greatly enhances patient compliance with treatment.

On the commercialization level, Amvuttra’s growth curve continues to rise. In 2024, the drug’s sales reached $971 million, and it is expected to exceed $2 billion for the full year of 2025, with a significant year-on-year increase. It is poised to become the first single product under Alnylam with annual sales surpassing $2 billion. With the continuous expansion of indications and the deepening of global market penetration, its growth potential still has room for further exploration.

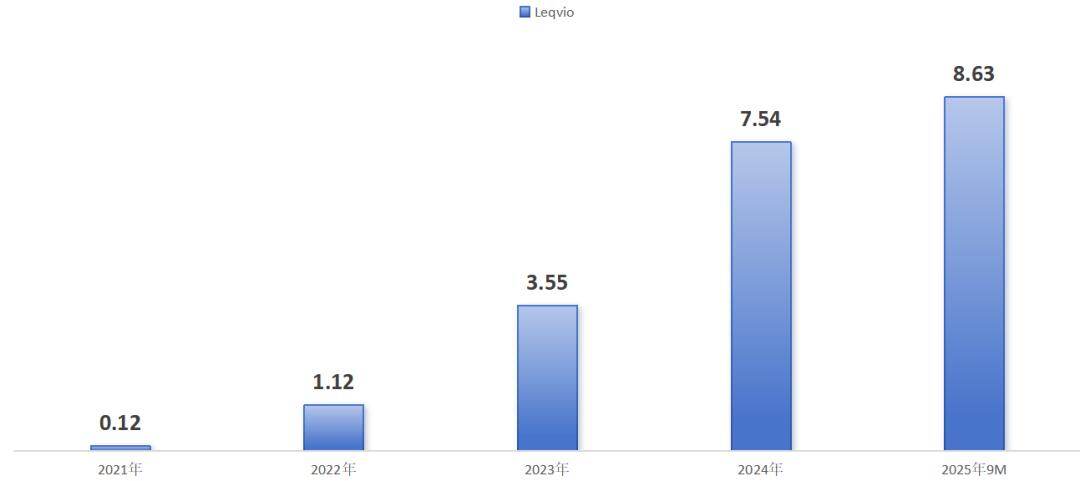

Unlike Amvuttra, which focuses on rare diseases, Leqvio, jointly developed by Alnylam and Novartis, precisely targets the major cardiovascular disease field, naturally possessing a higher market ceiling and greater blockbuster potential. As the world's first siRNA lipid-lowering drug targeting PCSK9, Leqvio was officially approved in 2021. By accurately targeting the mRNA of the PCSK9 protein and inhibiting its expression, it effectively reduces low-density lipoprotein cholesterol (LDL-C) levels in the blood, thereby lowering the risk of cardiovascular disease.

In the first three quarters of 2025, Leqvio sales have reached $860 million, steadily advancing toward the blockbuster drug category. With the continuous progress of its national medical insurance coverage and ongoing market education, its penetration rate is expected to further increase, unlocking greater market value.

Figure: Leqvio Sales Overview (USD billion), Source: Jinduan Research Institute

In addition to Amvuttra and Leqvio, there are several late-stage candidates in the global small nucleic acid drug pipeline poised for potential success, further expanding the boundaries of the field. For instance, Arrowhead's Plozasiran was approved for marketing in November 2025 for the treatment of familial chylomicronemia syndrome (FCS); Alnylam's hypertension drug Zilebesiran is currently in Phase III clinical trials, and if successfully approved, it will become the world’s first small nucleic acid antihypertensive drug, opening up an entirely new therapeutic area.

The successive launches and commercial scaling of these promising products will continue to expand the therapeutic landscape of small nucleic acid drugs, drive the field from rare diseases towards more common conditions, and accelerate the global small nucleic acid drug market into a new phase of explosive growth.

03 Changes Are Happening

Although the global small nucleic acid drug landscape dominated by the three giants is relatively stable,The long-coveted MNC has made its move, aggressively entering the field with a "dual-track layout" of "acquisition + cooperation" to accelerate the division of track dividends.

Given the high technical barriers and complex delivery systems characteristic of small nucleic acid drug development, multinational corporations (MNCs) initially focused on collaborating with the "Big Three" as a starting point to steadily accumulate industry experience. However, with the continuous expansion of the global market scale and the accelerated release of commercial potential in the sector, MNCs have begun aggressively intensifying their efforts through a flurry of business development (BD) deals, driving a rapid reshaping of the competitive landscape within the industry.

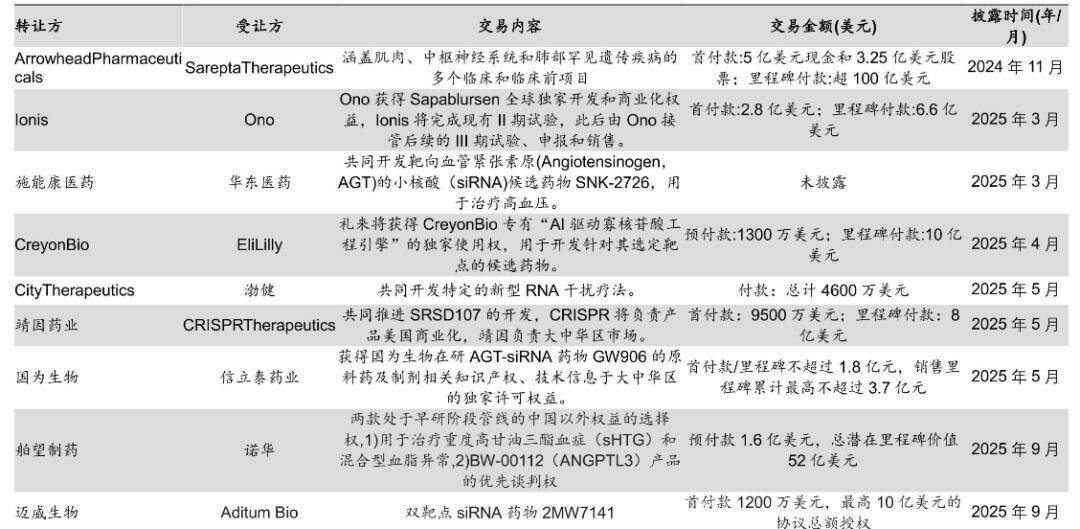

The热度 of the track can be seen from the BD transaction data. According to incomplete statistics, in 2025, there were 23 representative transactions in the global small nucleic acid field, covering diverse forms such as technology platform cooperation, pipeline authorization, and corporate acquisitions. The potential total transaction value exceeded 36.473 billion US dollars, surging over 300% compared to 8.496 billion US dollars in 2023, intuitively demonstrating the MNCs' urgent desire and determination to layout this golden track.

Figure: Overview of Key BDs in the Small Nucleic Acid Drug Field in the Past Year, Source: Tebon Securities

Novartis is undoubtedly the benchmark player among MNCs in the small nucleic acid track., constructing full-dimensional competitive barriers through a series of significant transactions, with clear ambitions for dominance. It has already built a comprehensive pipeline covering various technology types such as RNAi and ASO, encompassing key areas like cardiovascular, neurology, and rare diseases, becoming a core force in reshaping the landscape.

Looking back at its layout path, every step has precisely hit the key nodes of the track: In 2019, it acquired The Medicines Company for $9.7 billion, bringing in Leqvio, the world’s first siRNA drug targeting PCSK9, officially opening the door to the small nucleic acid field; In 2023, it spent $1 billion to acquire DTxPharma, obtaining the Falcon lipid nanoparticle delivery platform; In June 2025, it invested another $1.7 billion to acquire Regulus Therapeutics, incorporating farabursen, a microRNA therapy for polycystic kidney disease in Phase III clinical trials, to strengthen its late-stage pipeline capabilities; In the same September, it also reached two major collaborations intensively, partnering with Arrowhead and China's Bowang Pharmaceuticals respectively to develop siRNA drugs, further broadening its pipeline boundaries and global layout.

Not only Novartis, but also MNCs such as Eli Lilly, Boehringer Ingelheim, Novo Nordisk, and Regeneron have entered the field, creating a multi-faceted layout. Boehringer Ingelheim has reached a $2 billion collaboration with Ribo Life Science to jointly develop small nucleic acid therapies in the MASH field, demonstrating recognition of the Chinese company's technology platform. Novo Nordisk is making advances on two fronts: on one hand, it has invested $550 million in Replicate Bioscience’s srRNA technology, and on the other hand, it has acquired Dicerna to target more than 30 hepatocyte targets, deeply cultivating promising areas such as chronic liver disease and obesity. Regeneron has directly shifted its R&D focus; of the 10 new drugs entering clinical trials for the first time in 2024, six are siRNA therapies, showing its strategic emphasis on the small nucleic acid track.

Notably, Chinese companies are emerging as a new force in the global small nucleic acid field by leveraging proprietary delivery technologies, differentiated pipeline layouts, and cost advantages. An increasing number of MNCs are actively seeking BD collaborations with Chinese companies.The Power of China has become the "catfish" breaking the global pattern, injecting new vitality into the industry.。

The successful listing of Ribo Life Science marks a milestone in the rise of China's small nucleic acid drug research and development. As one of the first companies in China to deeply cultivate the small nucleic acid field, Ribo Life Science currently has seven self-developed assets in clinical trial stages. It has built three core technology platforms with independent intellectual property rights—RiboGalSTAR™ (liver targeting), RiboPepSTAR™ (extrahepatic targeting), and RiboOncoSTAR™ (oncology)—achieving "modularization" and "scalability" in the R&D process, and solidifying its technological foundation.

Its pipeline layout combines innovation with commercial potential: the core product RBD4059 is the world's fastest-progressing siRNA drug targeting FXI, overcoming the pain points of traditional anticoagulant therapies with the advantages of long-lasting effects and low risk of bleeding, and is currently advancing in global synchronized development; RBD5044 follows the approval path of Arrowhead's similar drugs, significantly reducing R&D risks. The collaboration with Boehringer Ingelheim in the MASH field is important evidence of its technical platform being recognized by top international pharmaceutical companies; licensing RBD7022 to Qilu Pharmaceutical in Greater China is the optimal allocation for achieving commercial efficiency, demonstrating a mature pipeline operation strategy.

Apart from Ribo Life Science, other Chinese Biotechs such as Jingyin Pharmaceuticals and Bowang Pharmaceuticals have successfully reached international BD collaborations, with the potential to make a mark on the global stage; leading domestic pharmaceutical companies like Hengrui Medicine, Innovent Biologics, and Junshi Biosciences have also crossed over to this field, accelerating efforts to fill gaps in the small nucleic acid sector, forming a tiered development trend.

The intensive moves by MNCs and the strong rise of Chinese pharmaceutical companies have not only driven up the transaction热度 and valuation levels in the small nucleic acid field, but also forced technological iteration, delivery system innovation, and accelerated global market education. As indications extend from rare diseases to common conditions such as obesity, hepatitis B, and cardiovascular diseases, the market ceiling for small nucleic acid drugs continues to rise.The global competitive landscape has officially bid farewell to the "tri-power dominance" and entered a new phase of "heroes vying for supremacy."

This article is based on publicly available information and is intended solely for the purpose of information exchange, without constituting any investment advice.

This article is from the WeChat Official Account"MediShine", Author: Huang Xiwen, 36Kr authorized publication.