Orphan Drug Investment in Rare Diseases: Is the Hype Premature?

Data from EvaluatePharma’s “Orphan Drug Report 2019” shows that orphan drugs will account for one-fifth of global prescription drug sales in 2024, with sales projected to reach $242 billion, and the players dominating this orphan drug market will primarily be large biopharmaceutical and biotechnology companies.

Investment and financing in the field of rare diseases and orphan drugs are equally robust. In 2018, the total value of investments and mergers and acquisitions (M&A) in rare diseases and orphan drugs within the global biopharmaceutical sector reached $16.45 million, with total financing even surpassing that of the neuroscience sector. (Data source: Trends in Healthcare Investments and Exits 2019)

The rare disease market is often described as a market characterized by “market failure.” However, data suggest that although the total number of patients with rare diseases is relatively small, the potential of this specialized market should not be underestimated. In China’s orphan drug market, uncertainties surrounding market size, pricing, and reimbursement have made it a hotly debated topic whether domestic orphan drugs will emerge as a new focal point for pharmaceutical investment.

On September 20, 2019, the 8th Rare Disease Summit was held in Shenzhen. During the pre-conference workshop, investors, rare disease drug developers, commercialization enterprises, and other stakeholders engaged in discussions on the topic, “Can Orphan Drugs Become the New Hotspot for Pharmaceutical Investment in China?”

VCBeat (WeChat ID: vcbeat) has compiled the highlights from it.

First, Yan Zhiyu, CEO of Shufang Pharma, analyzed the commercial opportunities and challenges for orphan drugs in the Chinese market from three perspectives: demand, supply, and payment.

Regarding patient needs, Yan Zhiyu summarized the plight of rare disease patients in a single word: “difficult.”

A vast number of rare diseases remain untreatable in China due to a severe scarcity of available medications. Globally, there are an estimated 6,000 to 7,000 recognized rare diseases, yet only about 1,000 have approved therapeutic options. While many treatments for these 1,000 conditions have been approved abroad, there is a significant disparity between international and domestic availability, as numerous drugs have not yet entered the Chinese market.

Even when treatments are available, significant challenges remain in terms of payment. Orphan drugs are characterized by their high prices; prior to 2018, only four orphan drugs had been included in China’s national medical insurance negotiations.

The challenges faced by rare disease patients extend beyond medication and health insurance coverage; diagnosis poses another significant hurdle. In China, most diagnosed cases are identified by specialists, yet these represent only the tip of the iceberg among the country’s total rare disease population, with a substantial number of patients remaining undiagnosed or misdiagnosed.

In China, specialists in rare diseases may be even rarer than the patients themselves. In other words, a patient may need to visit multiple healthcare facilities before finding a specialist capable of providing an accurate diagnosis, effective treatment, and management. During this process, many patients remain undiagnosed, resulting in significant patient attrition.

In addition, follow-up and disease course management for rare diseases are also challenging. Many patients are unable to receive continuous and effective treatment.

Therefore, on the demand side, we can see a huge unmet need.

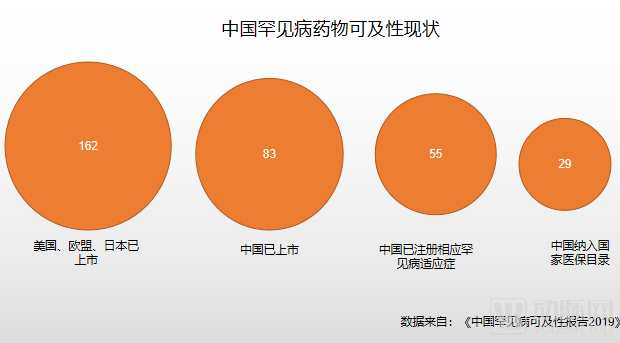

On the supply and demand side, 621 orphan drugs have been approved globally, but only 282 are available in China.

The 2019 “Report on the Accessibility of Rare Disease Drugs in China” revealed a significant gap: among 162 drugs for treating rare diseases, only 83 were marketed in China. Of these 83 marketed drugs, many were available under other indications; only 55 were specifically approved for the indications corresponding to these 121 diseases, representing another substantial disparity. Although the national medical insurance negotiation mechanism has made considerable progress since 2018, only 29 of these drugs have been included in the National Reimbursement Drug List.

Therefore, from a supply perspective, the market is far from achieving the necessary equilibrium.

Fortunately, on the payment front, the Chinese government is paying close attention to rare diseases. With the introduction of the first “List of Rare Diseases,” accelerated drug approval processes, and policies such as clinical trial exemptions being rolled out one after another, policy barriers are gradually disappearing.

Although there are significant unmet needs in the field of rare diseases from the patient perspective, and barriers to approval and reimbursement are gradually breaking down, challenges such as the lack of a commercial insurance system, high out-of-pocket costs for patients, and scarce medical resources still bring considerable uncertainty to investments in rare diseases.

How Do Investors View the Many Uncertainties Surrounding Rare Disease Investment in the Chinese Market?

Ran Ting Qian, Managing Director of Ally Bridge Hongjia Fund, first analyzed capital market preferences for biotechnology companies.

In her view, capital markets’ understanding of companies developing drugs for rare diseases is rapidly expanding.

“Since the beginning of last year, the Hong Kong Stock Exchange has allowed pre-revenue biotechnology companies to go public. This year, Rule 5 of the STAR Market further opened listing pathways for such biopharmaceutical enterprises with no operating revenue. This represents a significant benefit for the broader biopharmaceutical sector, regardless of whether companies are engaged in rare disease therapeutics. It has brought pharmaceutical R&D enterprises, which previously faced considerable challenges in securing funding, directly before capital markets. Naturally, the rare disease segment is one of the key beneficiaries.”

However, she also pointed out that capital markets’ preferences for biotechnology companies have been continuously fine-tuned and evolving.

“We have observed the performance of biopharmaceutical companies listed on the Hong Kong Stock Exchange for over a year. We found that investor preferences remain relatively concentrated, with companies generating revenue or targeting more mainstream diseases demonstrating stronger performance.”

“However, we are pleased to observe that the capital market is composed of highly professional individuals with a strong spirit of learning. In the past, Hong Kong investors long focused on traditional pharmaceutical companies with established revenues and profits. Today, discussions have shifted toward more specialized and segmented areas of pharmaceutical R&D, a progression that has far exceeded our initial expectations. Therefore, I am optimistic about the future acceptance by the capital market of companies developing orphan drugs.”

VCs should have a keener sense of smell than PE funds. So, from the perspective of VC investors, is orphan drug R&D ready?

Xue Wenyu, Managing Director of Morningside Venture Capital, stated that while the firm is interested in the field of rare diseases, it has not designated this area as a primary investment focus. However, last year, Morningside’s U.S. team conducted a review and found that nearly one-third of the European and American biotechnology companies in its portfolio have adopted rare diseases as their R&D direction or possess orphan drug development pipelines.

Why Have We Unintentionally Invested in a Significant Number of Rare Disease Companies?

From the perspective of Morningside Venture Capital’s U.S. team, the investment rationale for orphan drugs is clear. First, Europe and the United States have established a robust ecosystem supporting rare disease drugs from R&D and regulatory approval through to commercialization, along with a mature capital market that fully understands this sector. Second, recent data indicate that rare disease drugs have a higher probability of approval after entering clinical trials, and their review timelines are shorter compared to other indications, implying a higher return on investment.

Third, because rare diseases target a relatively small and well-defined patient population, orphan drug developers may establish their own commercialization teams to market directly to these patients, thereby enhancing corporate value at the commercialization stage.

“Oranges grown south of the Huai River remain oranges, but those grown north of it become trifoliate oranges.” Can these two logics take root in China?

Xue Wenyu pointed out that for Chinese companies developing orphan drugs for the European and American markets, there are two considerations in the current environment: first, whether they have a high-quality pipeline in early-stage R&D to compete with their Western counterparts; and second, whether they can consider expanding overseas for subsequent commercialization.

It is also necessary to consider whether there is overheating in certain rare disease areas.

In European and American markets, the pricing of orphan drugs is the result of negotiations between payers and pharmaceutical R&D companies. Currently, the number of approved therapeutic agents for most rare diseases remains quite limited, leaving payers with little bargaining power and contributing to high orphan drug prices to some extent. However, if five or six drugs targeting the same rare disease indication become available in the future, along with generic versions entering the market after patent and regulatory exclusivity periods expire, payers’ negotiating leverage will increase significantly. At that point, whether the current high-pricing model for orphan drugs can be sustained will warrant close attention.

For pharmaceutical companies targeting China’s rare disease market, the most critical challenge is to establish a viable commercialization pathway amid lowering approval thresholds and a gradually improving policy environment. Although the estimated population of patients with rare diseases in China approaches 17 million, indicating substantial market potential, the actual addressable market for rare disease drugs remains very limited due to various constraints. Realizing the market’s full potential will require the development of a supportive ecosystem and concerted efforts from all stakeholders involved.

Therefore, Xue Wenyu believes that the investment window for orphan drugs in China is opening up, presenting suitable investment opportunities; however, it remains some distance from becoming a major market trend, and investors need to have sufficient patience.

Finally, several investors also noted that the social benefits of investing in orphan drugs cannot be overlooked. There are no perfect investment targets in any market; the rare disease and orphan drug market presents both challenges and opportunities. If a strong tailwind can lift even a pig to flight, a window of opportunity requires sustained exploration and cultivation.