Hansoh Biopharma Lists on HKEX with Mission to Deliver Affordable Therapies for Chinese Patients: Exclusive Interview with CEO Dr. Scott Liu

Henlius

Innovative Biopharmaceutical Company

On September 25, 2019, Henlius rang the bell for its listing on the Hong Kong Stock Exchange. The IPO was priced at HK$49.6 per share, with a total issuance of 64.6954 million shares, raising approximately HK$3.2 billion (equivalent to about RMB 2.9 billion). The opening price on that day was HK$47.45.

After nearly a decade of development, Henlius welcomed a series of positive developments in 2019. First, Hanlikang® (Rituximab Injection), the first biosimilar approved in China, received marketing approval in February. Several other blockbuster products, HLX02 and HLX03, successively had their New Drug Applications (NDAs) accepted by the National Medical Products Administration (NMPA) and were included in the priority review program. Notably, HLX02 became the first “Chinese-made” trastuzumab to have its marketing application accepted by the European Medicines Agency (EMA). In mid-September, Henlius announced a strategic collaboration with KG Bio regarding HLX10 (an anti-PD-1 monoclonal antibody), further expanding its overseas market presence. The company’s listing on the Hong Kong Stock Exchange marks another significant milestone for Henlius, reflecting recognition from the secondary market.

On the eve of the company’s IPO, Dr. Liu Shigao, President and CEO of Henlius, granted an exclusive interview to VCBeat. During the interview, Dr. Liu stated that Hanlikang, the company’s first product launched this year, has already benefited numerous lymphoma patients, while the development of other candidates in its pipeline is progressing steadily. Meanwhile, Henlius’ anti-PD-1 monoclonal antibody HLX10 is at the forefront of domestic efforts in developing combination therapies involving anti-PD-1 antibodies. Combination regimens with high response rates may help HLX10 achieve superior therapeutic efficacy. Looking ahead, Henlius will continue to deepen its long-term commitment to both biosimilars and innovative drugs, while closely monitoring other emerging directions in tumor immunology.

Reflecting on the past decade, Liu Shigao summarized it with the phrase “favorable timing, advantageous location, and harmonious people.” “Favorable timing” refers to catching the wave of rapid development in China’s innovative drug sector over the past ten years; “advantageous location” signifies Henlius’ steadfast adherence to its core philosophy of “affordable innovation, trustworthy quality”; and “harmonious people” embodies the sense of mission and determination that every Henlius employee must possess, embracing the spirit of “if not me, then who?”

The H shares offered under the Hong Kong Public Offering were oversubscribed, with a total of 25.1353 million Hong Kong Offer Shares subscribed for, representing approximately 3.89 times the initial total of 6.4696 million Hong Kong Offer Shares available for subscription under the Hong Kong Public Offering.

When asked why the company chose to list on the Hong Kong stock market, Liu Shigao gave a straightforward answer: “In 2018, the Hong Kong Stock Exchange introduced regulations allowing pre-revenue biotechnology companies to list in Hong Kong. We made preparations for an HKEX listing at that time. Now, going public is simply the natural next step.”

Regarding commercialization, Liu Shigao expressed even greater confidence: “Following Hanlikang, we have two additional biosimilars already submitted for marketing approval, and we plan to submit applications for new indications of Hanlikang in the future. These biosimilars are all at the forefront of the domestic market and will capture a significant share.”

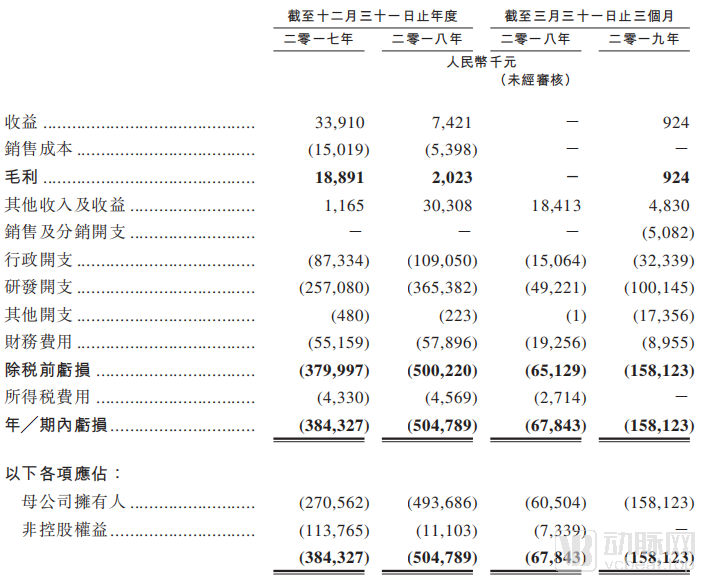

Like most pre-profit biopharmaceutical companies listing in Hong Kong, Henlius has seen its R&D expenses grow steadily over the past few years in line with the progress of its product pipeline, with full-year R&D investment reaching RMB 365 million in 2018. “R&D investment is a long-term and continuous process. Our R&D plans have been progressing smoothly; while we may make minor adjustments and slightly increase research funding each year based on actual circumstances, there will be no significant fluctuations overall,” said Liu Shigao.

As Hanlikang rolls out across China, Henlius is expected to see its total losses gradually decrease in the near future. Reportedly, Hanlikang has already achieved a high market share among new patients, and local medical insurance authorities have shown a relatively positive attitude toward its inclusion in the national reimbursement drug list. It can be said that Hanlikang, having been on the market for half a year, is holding its own against the originator drug.

Henlius chose to prioritize biosimilars as its lead products, primarily based on the conditions of the domestic pharmaceutical market: “We did not prioritize first-in-class innovation because the current payment capacity in the domestic market cannot yet bear the costs associated with such highly innovative products.”

The failure rate of innovative drugs is exceptionally high, particularly for First-in-Class agents. Typically, breakeven is achieved only by allocating the costs of failed drug candidates to the few successful new products, a dynamic that drives the high pricing of First-in-Class innovative drugs. Such exorbitant prices are unaffordable even for patients in some developed countries, let alone those in emerging markets.

“Therefore, we believe that a more feasible strategy at present is to start with biosimilars, build core capabilities for a full-scale biologics industry platform, and then gradually transition from lower-risk innovations such as fast-follow or BioBetter products to novel innovative drugs. As an innovative pharmaceutical company based in China, we aim to prioritize serving Chinese patients by providing them with high-quality, cost-effective biologics,” said Liu Shigao.

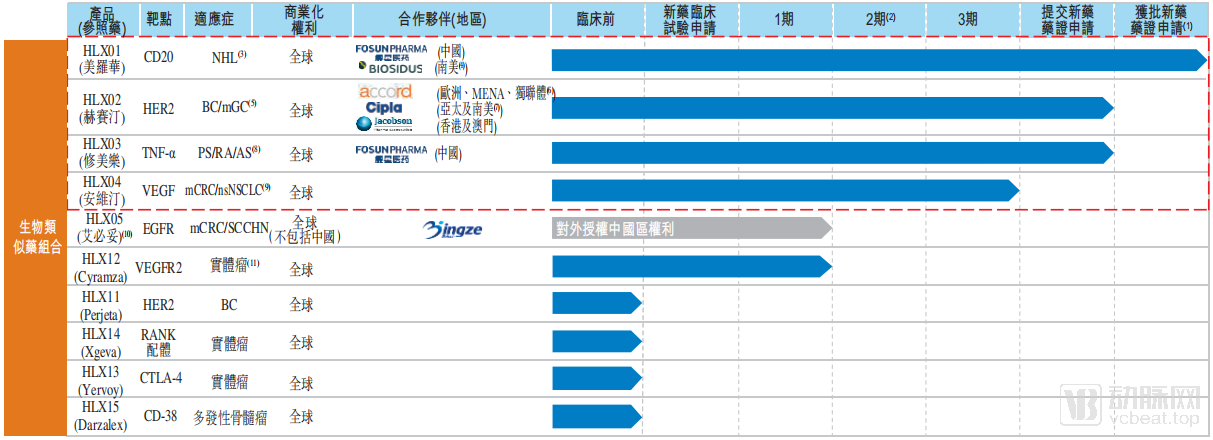

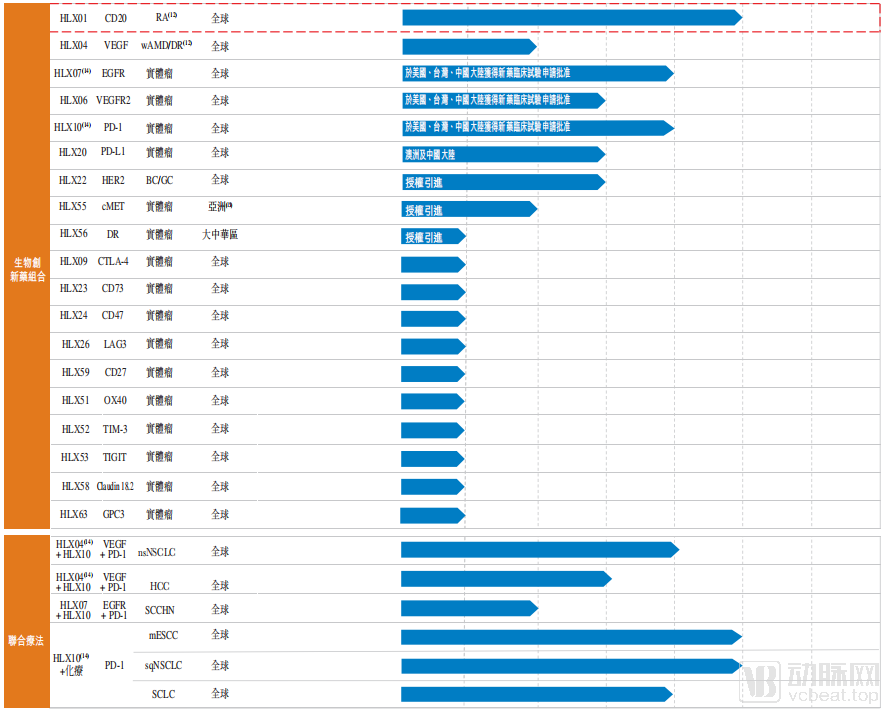

Henlius currently has as many as 10 biosimilar products in its pipeline. In addition to rituximab HLX01 (brand name: Hanlikang), which has already been launched, several other products are poised to rapidly enter the commercialization stage.

Among them, the New Drug Applications (NDAs) for HLX03 (adalimumab injection) and HLX02 (trastuzumab for injection) have been accepted by the National Medical Products Administration (NMPA) and are now included in the priority review program. In addition, the Company has sequentially initiated multiple clinical trials globally on various tumor immuno-combination therapies involving HLX10 in combination with its proprietary products, including HLX04 (a bevacizumab biosimilar) and HLX07 (an anti-EGFR monoclonal antibody), as well as in combination with chemotherapy.

In addition to “affordable innovation for patients,” “trusted quality” is undoubtedly another vital component of Henlius’s core philosophy. The company’s stringent standards for product quality have become a key competitive barrier in the biosimilars industry. Henlius’s manufacturing processes not only meet China’s Good Manufacturing Practice (GMP) standards but also comply with the production requirements set by regulatory authorities in the United States and the European Union. The company’s Xuhui manufacturing site has successfully undergone multiple on-site inspections and audits by EU Qualified Persons and international commercial partners.

Regarding biosimilars, Liu Shigao believes that “compared with generic chemical drugs, biosimilars present significantly higher technical challenges and capital barriers. There are only five or six well-known biosimilar companies globally. The state imposes extremely stringent quality requirements on biosimilars; key quality attributes such as purity, impurities, biological activity, and immunological activity must be highly similar to those of the originator product, with no statistically significant differences in any quality attribute. This is indeed very challenging, particularly during production scale-up, where moving from small-scale trials of a few liters to final industrial-scale production of thousands of liters is highly prone to issues. Therefore, the development of biosimilars is a process with exceptionally high technical difficulty.”

Market competition between biosimilars and originator drugs has long been a topic of widespread interest. However, the domestic biosimilar market in China differs significantly from those abroad. In foreign markets, mature payment systems have allowed originator drugs to largely saturate their respective markets. Consequently, annual market growth rates for innovative biologics in Europe and the United States are quite limited, with some even registering single-digit figures. In contrast, China continues to exhibit a trend of rapid growth. Although China accounts for a high proportion of new cancer cases globally, medication uptake rates remain generally low, primarily due to the prohibitive cost of biologic agents. Thanks to national medical insurance policies designed to benefit the public and the robust development of the biopharmaceutical industry, prices of biologics in China have declined significantly. The rapid development and regulatory approval of high-quality biosimilars, exemplified by Hanlikang (rituximab), will further foster healthy market competition and provide physicians and patients with more therapeutic options.

“Therefore, the rapidly growing domestic market is different from the slowly growing overseas market. China’s biopharmaceutical market remains a blue ocean, with biological innovative drugs and biosimilars poised for rapid growth,” said Liu Shigao.

For Henlius’s pipeline of innovative drugs and combination therapies, the anti-PD-1 monoclonal antibody HLX10 is undoubtedly the cornerstone product. To date, two indications for HLX10 in combination with chemotherapy have entered Phase III clinical trials, and combination regimens with other key products are being actively advanced.

Following the sequential approval of three domestically produced anti-PD-1 new drugs, competition among Chinese-made PD-1 monoclonal antibodies has gradually shifted from racing to market toward expanding indications. Liu Shigao offers a unique perspective on the future development direction of domestic anti-PD-1 monoclonal antibodies: “The advantages of PD-1 monoclonal antibodies are well known, particularly their broad range of indications. However, the objective response rate (ORR) for PD-1 monoclonal antibodies in most responsive cancer types is quite low, approximately 20%. Yet, when PD-1 monoclonal antibodies are combined with one or more additional small-molecule drugs or monoclonal antibodies, the ORR can reach as high as 60% or even higher. Such an ORR is essential to ensure the effective clinical application of anti-PD-1 monoclonal antibodies.”

“Therefore, anti-PD-1 products that can be combined with a wider range of other drugs to achieve better therapeutic outcomes will be the future winners,” Liu Shigao continued. “Last year, Henlius obtained China’s first IND approval for an anti-PD-1 monoclonal antibody in combination with other monoclonal antibodies, and combinations with other small-molecule drugs are also under efficient development.”

“This is also why leading oncology experts in China, such as Professor Shi Yuankai, Professor Qin Shukui, and Professor Li Jin, are willing to participate in our clinical trials. Because patients can derive tangible benefits from our clinical trials, and these trials can better facilitate the advancement of drug research,” said Liu Shigao.

In addition to progress in combination therapies, Henlius has also established its own strategic layout for international market expansion. In mid-September 2019, Henlius announced that it had reached a cooperation consensus with KG Bio of Indonesia, granting the latter the rights to develop and commercialize HLX10 as a monotherapy and in two combination regimens across ten Southeast Asian countries, with total deal value potentially reaching up to USD 692 million.

“The anti-PD-1 product market in Southeast Asia is expected to be served by only three to five players. However, with a population of 650 million, the region still faces substantial unmet medical needs. Entering the Southeast Asian market in this landscape means we are well-positioned to uncover greater opportunities and bring benefits to the many patients in the region with limited ability to pay,” said Liu Shigao.

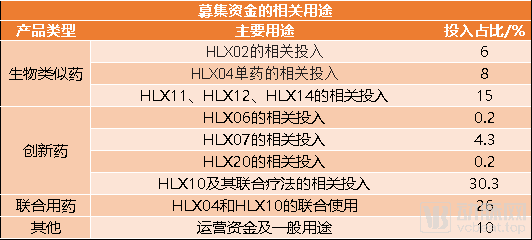

Henlius stated in its prospectus that 90% of the proceeds from this listing will be allocated to product research and development. The largest portion, accounting for 30.3% of the proceeds, will be invested in HLX10 and its combination therapies. Investments in biosimilars will be primarily directed toward overseas clinical trials for HLX02 and related clinical trials for HLX04, with these two drugs collectively representing 40% of the proceeds. Additionally, 15% of the funds will be used for the development of other candidate biosimilars.