From Product Distribution to Import Substitution: How China's IVD Industry Achieves a Blue Ocean Breakthrough

This year marks the 70th anniversary of the founding of the People’s Republic of China. On the eve of National Day, VCBeat has specially curated a “Series on Medical Innovation,” aiming to highlight the achievements made by the healthcare industry under the national initiative for independent innovation, through our coverage and analysis of new technologies and products across various medical fields.

In Vitro Diagnosis (IVD) refers to diagnostic procedures performed by testing blood, body fluids, or tissue samples after they have been collected from the human body. Currently, more than 80% of clinical disease diagnoses rely on IVD.

Due to the relatively late start of China’s in vitro diagnostics (IVD) industry, international brands hold significant advantages in technology, brand recognition, and product quality. Consequently, the IVD sector is predominantly dominated by foreign brands, with foreign-funded enterprises accounting for nearly 56% of the Chinese market.

An in vitro diagnostics (IVD) practitioner once told VCBeat that, at the outset of their venture, tertiary hospitals were largely closed off to domestic brands and held local products in low regard. However, with policy guidance and improvements in product quality, hospitals’ acceptance of domestically produced products has been steadily increasing.

Looking back at the development journey of domestic in vitro diagnostic (IVD) brands, local enterprises have traversed a tortuous yet progressive path. In the 1990s, the first generation of domestic IVD companies started as distributors before embarking on independent innovation and capturing the mid-to-low-end market with cost advantages. To date, domestically produced IVD products have achieved an 80% market share in certain niche segments.

In the early days, the localization of in vitro diagnostic (IVD) products followed a path akin to “saving the nation by an indirect route,” whereby companies first acted as distributors for foreign products to accumulate capital before investing in independent research, development, and manufacturing.

Currently, the import substitution of in vitro diagnostics (IVD) coincides with technological iterations within the industry, enabling domestic companies to leverage their technical advantages to overtake competitors on the curve. For instance, in the cutting-edge field of molecular diagnostics, the overall technical level of Chinese enterprises is not significantly different from that of their overseas counterparts.

In vitro diagnostics (IVD) is hailed as the “eyes” of physicians. The development of the IVD industry is closely linked to public health, particularly in disease prevention and precision diagnosis. Improving the relatively backward state of domestic medical diagnostic technologies, breaking the monopoly of imported products, and revitalizing national industries can be regarded as a way to serve the country through industrial advancement.

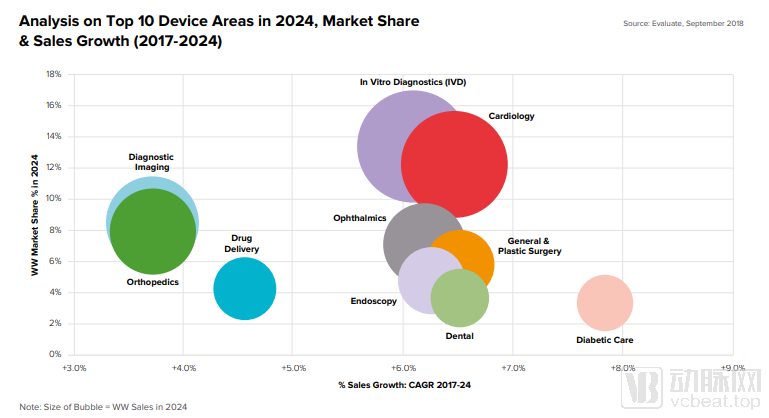

Beyond generating substantial social benefits, the import substitution of in vitro diagnostics (IVD) and their localization are key to securing industrial leadership in the high-end frontier of life sciences. As one of the pillar industries of the economy, medical devices include IVD as the largest subsector, which has long held the top position. The global IVD market size is projected to reach $79.6 billion in 2024. In terms of both market share and compound annual growth rate (CAGR), IVD ranks among the leading segments within the broader medical device industry.

Data source: EvaluateMedTech® World Preview 2018, Outlook to 2024

According to statistics, China's in vitro diagnostics (IVD) market reached approximately RMB 60 billion in 2018. Undoubtedly, domestic enterprises are essential to tapping into this vast blue-ocean market.

China accounts for approximately 20% of the global population, yet its in vitro diagnostics (IVD) market represents less than 5% of the global market. According to statistics from China Industry Information Network, the per capita consumption of IVD products in China is $4.6, which is below the global average of $8.5.

In 2016, the market size of IVD products in China was approximately RMB 43 billion. It is projected to reach RMB 72.3 billion by 2019, with a compound annual growth rate (CAGR) of 18.7% over the three-year period, indicating rapid development that far exceeds the global CAGR of 4.8%.

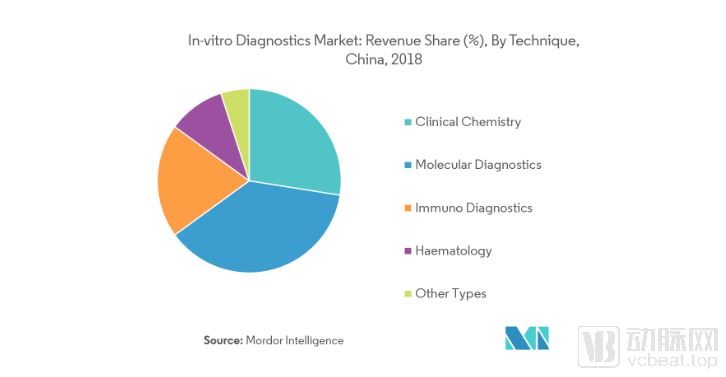

In terms of growth trends within specific segments, the domestic in vitro diagnostics (IVD) market mainly comprises immunoassay, clinical chemistry, and molecular diagnostics. Among these, clinical chemistry and immunoassay dominate the market, collectively accounting for over 60% of the share. However, according to the latest data from Mordor Intelligence, molecular diagnostics is experiencing rapid growth due to its broad range of applications, making it the fastest-growing IVD subsector globally (with an annual growth rate of approximately 12% in recent years). The growth rate of China’s molecular diagnostics industry is roughly twice the global average.

In addition to the growth of the in vitro diagnostics (IVD) industry driven by the release of potential market demand, China’s IVD sector is poised to enter a golden age of development, with significant opportunities for import substitution, fueled by policy initiatives such as tiered diagnosis and treatment and the establishment of “Three Centers” (Stroke Centers, Chest Pain Centers, and Trauma Centers), as well as by technological iterations.

From the perspective of the distribution pattern of core players in the domestic in vitro diagnostics (IVD) market, traditional multinational giants such as Roche, Siemens, and Thermo Fisher Scientific dominate the high-end segment, while enterprises including Mindray, Kehua Bio-engineering, Autobio Diagnostics, Maccura Biotechnology, Dirui Industrial, Leadman Biochemistry, Medcon Biotechnology, and Sinocare have established a firm foothold in the mid-to-low-end IVD market.

Their story of dominating the mid-to-low-end market dates back to the 1990s.

China’s in vitro diagnostics (IVD) industry began in the 1970s. Over the past 50 years, the development of IVD technology in China has undergone a complete transformation—from classic manual methods and workshop-style equipment to standardized, intelligent, and automated management. In the 1970s, the foundation of China’s IVD industry was virtually “zero.” Following the reform and opening-up policy, clinical laboratory centers were established successively across various provinces, rapidly accelerating the domestic development and introduction of IVD products in China.

In the 1990s, a large number of in vitro diagnostic (IVD) manufacturers and import agencies emerged rapidly; however, IVD products were limited to simple imitation and reliance on imports.

Most of the early batch of in vitro diagnostic (IVD) companies initially started as product distributors, including Autobio Diagnostics, Joysun Biotech, and Maccura Biotechnology.

Jiuzhang Biology’s founder, Zou Jianjun, once stated in a speech that Jiuzhang started as a distributor. Due to a lack of market expertise, the company relied on Randox Laboratories (UK) for product knowledge training and guidance on marketing practices. It can be said that Jiuzhang established its market presence before building its manufacturing facilities.

At that time, China’s in vitro diagnostics (IVD) industry was still characterized by a shortage of suppliers, with few companies engaged in biochemical diagnostics. It was not until the period from 2000 to 2015 that the healthcare industry began to expand rapidly.

A large number of enterprises have gradually discovered in the course of their development that independent innovation is the only core competitiveness. However, embarking on the path of independent innovation is no easy feat.

“Giving up the shortcut of making money through agency services was something that even some of our corporate partners couldn’t understand at the time.”

Independent innovation also imposes higher requirements on domestically produced products. Yao Jian’er, founder of Lifei Diagnostics, once stated, “If we are to surpass others and replace competitors in terms of product performance, our products must evolve from their 1.0 version to a 2.0 or even 10.0 version, creating a strong sense of differentiation for customers.”

Independent Innovation in In Vitro Diagnostics: At the time, companies faced not only a lack of recognition from both internal and external environments but also a series of immediate challenges.

First, the challenge lies in the lack of supporting industrial chain infrastructure; certain key components and upstream raw materials in China’s in vitro diagnostics (IVD) industry are heavily reliant on imports.

In the upstream segment of the in vitro diagnostics (IVD) supply chain, many manufacturers rely heavily on imported raw materials. Key reagents such as enzymes, antigens, and antibodies remain largely monopolized by foreign companies.

Raw materials for in vitro diagnostics (IVD) are the source of technological innovation in the field. Furthermore, the performance limits of these core materials largely determine the upper bound of IVD system performance. Taking immunoassays as an example, their fundamental principle is based on antigen-antibody reactions; thus, high-quality antigens and antibodies determine the overall quality of the final product. Such biological raw materials, including antigens and antibodies, are analogous to chips in the IT industry.

Miao Yongjun, Chairman of Autobio Diagnostics, stated that relying on imported raw materials is akin to having one’s neck held by foreign companies.

This has also compelled domestic companies to commit to the research and development of bioactive materials. A cohort of localized upstream R&D enterprises specializing in biological raw materials has emerged in China.

Second is the shortage of talent; China’s in vitro diagnostics (IVD) industry can be described as severely lacking in skilled professionals. Many companies initially had to cultivate their own teams.

At the inception of Getein Biotech, its founder, Su Enben, transitioned from a medical practitioner to an entrepreneur. When Getein Biotech was established in 2002, it consisted solely of him and two or three assistants at Jiangsu Province People’s Hospital.

As China’s in vitro diagnostics (IVD) industry started relatively late, domestic IVD companies have encountered numerous obstacles in regulatory review and approval. Due to the advanced nature of product innovations and stringent medical approval requirements, innovative products previously required a prolonged period to obtain regulatory clearance. For startups, capital shortages could make it difficult to survive the lengthy approval cycle.

Dai Lizhong, founder of Sansure Biotech, stated in an interview that after leaving his position as a core R&D scientist at Gen-Probe, the world’s largest nucleic acid reagent company, to return to China and start his own business, he gained profound insights into the differences between the in vitro diagnostic (IVD) industries in China and the United States. He noted that the development of biological reagents abroad is governed by clear regulations and frameworks, making many aspects highly predictable. For instance, developing an infectious disease test kit typically takes about five years and requires an investment of $100–200 million. The situation in China is different: the industry is less mature, regulations are less standardized, and with government support, there is significantly greater flexibility in operations.

Fortunately, in recent years, as the in vitro diagnostics (IVD) industry has been designated a key sector for state-supported development, domestic enterprises have received substantial government support in their growth.

On the path of innovation in in vitro diagnostics (IVD), despite navigating countless make-or-break moments, waves of entrepreneurs continue to enter the field. Driven by innovation and sustained by perseverance, and propelled by numerous industry practitioners, domestic products have become an indispensable force in multiple IVD subsectors in China.

Biochemical Diagnostics: Substitution Rate Reaches 70%

In terms of import substitution rates across specific sub-sectors, the biochemical diagnostics sector represents the most mature domain for domestically produced products. As one of the earliest-established sub-sectors within China’s in vitro diagnostics (IVD) industry, biochemical diagnostics has completed its transition from reliance on imports to independent research and development. Domestic brands have achieved significant localization success in the mid- and low-end reagent and instrument markets; however, the high-end market, particularly in tertiary hospitals, remains monopolized by overseas giants. Consequently, import substitution in the high-end immunodiagnostics market has become a key direction for future development.

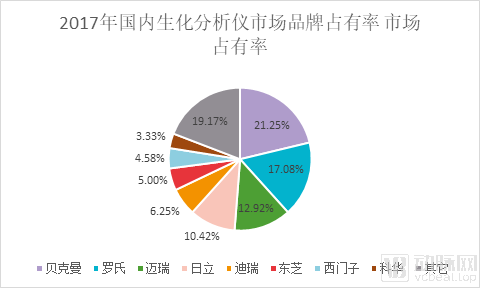

Currently, the domestic substitution rate for biochemical products exceeds 70%. Domestically produced biochemical analyzers have been rapidly adopted and promoted in hospitals below the Grade A Tertiary level. At present, high-quality domestic biochemical manufacturers, such as Dirui, Mindray, and Kehua Bio-engineering, are gradually penetrating high-end domestic markets, including tertiary hospitals.

In China’s in vitro diagnostics (IVD) industry for clinical chemistry, biochemistry analyzers are evolving toward higher throughput in standalone units, modular connectivity, and total laboratory automation (TLA) lines, while biochemical reagents are moving toward more comprehensive test panels at lower prices.

Data sourced from the "Blue Book on the Development of China's In Vitro Diagnostics Industry 2017"

Immunodiagnostics: Import Substitution Underway

The immunoassay market is the primary driver of growth in the in vitro diagnostics (IVD) industry and is often referred to as the “golden segment.” Currently, chemiluminescence technology has largely replaced enzyme-linked immunosorbent assay (ELISA) in the high-end immunoassay sector, with approximately 70% of the immunoassay market now adopting chemiluminescence. The chemiluminescence segment is growing at a compound annual growth rate (CAGR) of approximately 25%.

The chemiluminescence market is largely monopolized by foreign companies such as Roche, Abbott, Beckman, and Siemens, with domestic enterprises accounting for only about 10% of the market. Thus, there is significant potential for import substitution.

There are over 260 chemiluminescence companies in China. Representative enterprises include Snibe, Mindray, Autobio, Maccura, Daan Gene, and Kehua Bio-engineering.

It is worth noting that current projects from imported manufacturers are concentrated on routine thyroid function tests, tumor markers, and hormones. In contrast, domestic manufacturers have successfully addressed the shortcomings of imported brands, achieving breakthroughs in liver fibrosis assessment, specialized oncology tests, and autoimmune detection assays.

Domestic companies such as Snibe, Autobio Diagnostics, and Mindray Medical have achieved breakthroughs in chemiluminescence technology, with Snibe further pioneering direct chemiluminescence technology. Lifeomics’ high-throughput flow cytometry fluorescence technology builds upon chemiluminescence by adding the advantage of multi-analyte panel testing. This technology has already been adopted by customers in top-tier tertiary hospitals, and the import substitution process in the high-end immunoassay market is underway.

POCT: A Late Start, Rapid Development

POCT is one of the fastest-growing segments in the in vitro diagnostics industry, attracting significant attention due to its wide range of product applications.

From a global perspective, the POCT market has exceeded $40 billion, with the United States accounting for approximately 50% and Europe for over 30%. China’s POCT market is still in its early stages of development, with a relatively small scale but significant growth potential. In 2015, China’s POCT market was valued at approximately $740 million, with an annual growth rate of 20%–30%, far surpassing the global average growth rate of 7%–8%.

Currently, the high-end POCT market is monopolized by overseas companies. The implementation of tiered diagnosis policies has created a significant development opportunity for leading domestic brands offering cost-effective solutions positioned in the mid-to-low-end segment.

Driven by the promotion of tiered diagnosis and treatment, primary care hospitals have taken center stage. Leveraging advantages such as miniaturization and point-of-care testing, POCT products have gradually penetrated the market, thereby driving growth in the primary care sector.

Currently, there are many domestic enterprises in the POCT market. Representative companies include Getein Biotech, Mingde Biology, Wondfo, Hotgen Biotech, Lifotronic Technology, Lepu Medical, Weidian Bio, and Aupu Biopharmaceuticals.

POCT sub-segments are typically categorized by disease type: infectious diseases, critical care, cardiac conditions, pregnancy, blood glucose, drug testing, oncology, and others. China’s POCT market is in its growth phase, with domestically produced segments such as infectious disease testing and cardiac markers experiencing relatively rapid growth.

For domestic POCT companies, there is still a long way to go.

Over the first 50 years of in vitro diagnostics (IVD) development, domestically produced IVD products in China emerged from scratch, with industry growth primarily driven by import substitution in the mid-to-low-end market.

Today, domestic in vitro diagnostic (IVD) companies are poised to reap the dual benefits of rapid industry growth and import substitution, particularly in molecular diagnostics, a leading segment within the IVD sector.

Molecular diagnostic technologies enable precise diagnosis of disease-associated genes and allow for the assessment of disease susceptibility prior to onset. They are widely applied in areas such as infectious diseases, blood screening, genetic disorders, and molecular oncology diagnostics.

Molecular diagnostics features high technical barriers and remains in the early stages of market development. Although China started later in this field, the technological gap between domestic companies and their overseas counterparts is relatively small, and the industry is experiencing rapid growth. This presents an opportunity for China’s in vitro diagnostics sector to achieve leapfrog development.

Overall, the molecular diagnostics industry chain is divided into upstream raw materials, midstream reagents and instruments, and downstream hospitals and third-party independent laboratories.

The upstream raw material R&D market is primarily monopolized by foreign enterprises.

In the midstream market, domestic reagents have developed rapidly, while the share of domestically produced instruments remains relatively small. Molecular diagnostic kits, including nucleic acid extraction kits and nucleic acid detection kits, have been largely localized. The number of domestic manufacturers producing nucleic acid detection reagents for common viruses such as hepatitis B virus (HBV), hepatitis C virus (HCV), and human immunodeficiency virus (HIV) far exceeds that of foreign manufacturers. Nucleic acid detection kits for common diseases such as influenza A, B, and C are already quite mature, with many competing manufacturers, and nearly all are domestic brands.

Molecular diagnostic instruments primarily include nucleic acid extraction systems, PCR amplifiers, nucleic acid molecular hybridization instruments, gene chip analyzers, and gene sequencers. In the mid-range instrument segment, where technical barriers are relatively easier to overcome, domestic production has matured for nucleic acid extraction systems, PCR amplifiers, nucleic acid molecular hybridization instruments, and gene chip analyzers, with domestically produced products capturing the majority of the market. Meanwhile, Chinese enterprises are striving to break through in the localization of gene sequencers.

According to incomplete statistics, there were over 1,000 molecular diagnostics-related companies in China in 2017. Currently, 439 companies are engaged in research on PCR technology; 65 companies are researching FISH technology; 6 companies are studying nucleic acid molecular hybridization technology; 98 companies are working on gene chip technology; and 647 companies are focused on gene sequencing technology.

In the past, China’s in vitro diagnostics (IVD) industry started from scratch, with the market predominantly dominated by imported products. Today, numerous Chinese IVD companies have developed the capability to expand their products into international markets. Sansure Biotech, for instance, has achieved remarkable success in exporting its molecular diagnostics and genetic testing products. Its products are now sold in more than 40 countries, including Germany, France, and Singapore, and the company has undertaken a series of public health service projects in nations such as Pakistan, Egypt, and Cuba.

Autobio Diagnostics: Achieving Self-Sufficiency in Raw Materials

As mentioned above, reliance on imported raw materials is one of the pain points in the localization of in vitro diagnostics (IVD) in China. Recognizing shortcomings and striving for improvement has driven many companies to invest in raw material research and development. Currently, Autobio Diagnostics has achieved independent production of more than 400 types of antigens and antibodies, with a self-sufficiency rate of approximately 73%.

Autobio Diagnostics started out as a distributor and small-batch manufacturer, later adopting the integrated operation of reagents and instruments as its development strategy. In 2003, reagent production entered the stage of large-scale manufacturing. In 2013, following the launch of enzyme-linked immunosorbent assay (ELISA) technology and microplate chemiluminescence technology, the company introduced its magnetic particle chemiluminescence product series.

Following its IPO in 2016, Autobio Diagnostics leveraged industry resources to rapidly launch China’s first fully automated magnetic levitation laboratory automation line, the Autolas A-1 Series, and the Autof ms1000 microbial mass spectrometry detection system, further solidifying its technological leadership and position as an industry pioneer.

Snibe: Breakthrough in Direct Chemiluminescence

In 1998, chemiluminescence products had just entered the Chinese market, with fewer than five end-users adopting them and fewer than ten individuals in China familiar with the technology. It was at this juncture that Snibe Co., Ltd. (New Industries Biomedical Engineering) commenced the research and development of its chemiluminescence immunoassay systems. Snibe boasts three specialized technical teams dedicated to the R&D of instruments, reagents, and key raw materials.

As chemiluminescence is a closed system integrating reagents and instruments, it presents significant R&D challenges and high technical barriers. Furthermore, since the development of chemiluminescent immunoassay diagnostics in China started relatively late, foreign companies currently hold 90% of the domestic market share, maintaining a monopoly in the high-end segment, including tertiary hospitals.

Snibe’s products hold approximately a 5% share of the domestic chemiluminescence market. The fully automated chemiluminescence immunoassay analyzer developed by Snibe features 25 reagent positions and 144 sample positions, enabling it to accommodate 144 serum samples simultaneously, with each sample capable of being tested for up to 25 analytes at the same time.

Snibe is also the first Chinese chemiluminescence manufacturer to gain access to the U.S. FDA, currently serving more than 140 countries and regions worldwide with an installed base of over 11,000 units.

Mingde Biology: Two Women Create the Light of Domestic POCT

In 2008, Dr. Chen Lili and her co-founder, Dr. Wang Ying, jointly established Mingde Bio in the Wuhan Overseas Scholars Pioneer Park. Mingde Bio stands out as a rare example in the healthcare industry of a company founded and scaled to capital market success by two female entrepreneurs.

Mindray Biomedical completed the development of its quantitative detection system and initiated product registration within a short period. In 2012, its immune quantitative analyzer and procalcitonin (PCT) quantitative detection reagents were successfully launched on the market and obtained CE certification and ISO 13485 certification. Notably, the PCT quantitative detection reagent was the first registered product in China to enable rapid, quantitative point-of-care testing, filling a gap in this field domestically.

Currently, Mingde Biology is a domestic leader in high-throughput POCT and a pioneer in the construction of Chest Pain Centers, Stroke Centers, and remote ECG networks. Its business covers nearly 4,000 medical institutions across China, with sales coverage extending to multiple regions including Asia, the European Union, and South America.

Mindray: The Comprehensive Leader in In Vitro Diagnostics

Mindray is known as the Huawei of the medical device industry. In the field of in vitro diagnostics (IVD), Mindray is also an undisputed comprehensive leader. The market share of Mindray’s IVD product lines, such as clinical chemistry and hematology analyzers, ranks among the top of domestic enterprises.

Mindray’s product portfolio primarily covers three major sectors: Patient Monitoring & Life Support, In Vitro Diagnostics (IVD), and Medical Imaging. Currently, 60–70% of the sales revenue from Mindray’s other two product lines is generated overseas, whereas the situation for IVD is the opposite, with more than 70% of its sales revenue coming from the domestic market in China.

It is worth noting that Mindray has been continuously increasing its investment in the coagulation and chemiluminescence immunoassay segments of its in vitro diagnostics (IVD) product portfolio. As is well known, the coagulation testing market has emerged as one of the fastest-growing niches within the IVD sector in recent years, with a compound annual growth rate (CAGR) reaching 30%. However, the localization rate for coagulation analyzers remains low, with the Chinese domestic market dominated by foreign players: Instrumentation Laboratory (IL, part of the Werfen Group) from the United States, Sysmex Corporation from Japan, and Stago Group from France. Other multinational companies, such as Sekisui Medical from Japan and BE Diagnostic from Germany, hold smaller market shares. Currently, PULSOTEC, a member of the Mindray Group, stands out as a leading domestic player in the coagulation market and is poised to deliver further notable achievements in the future.

Wondfo: Comprehensive Product Portfolio

Guangzhou Wondfo Biotech Co., Ltd. was established in 1992. The company is dedicated to the research and development, manufacturing, and sales of rapid point-of-care testing (POCT) products, including reagents and instruments, within the biomedical in vitro diagnostics (IVD) industry. Its main product lines cover pregnancy testing, drug abuse testing, infectious disease testing, and chronic disease testing. Wondfo is the first domestic IVD reagent enterprise to pass the U.S. Food and Drug Administration (FDA) on-site inspection with “zero defects.”

Currently, most POCT companies in China focus on only a single sector. In contrast, Wondfo boasts a comprehensive product portfolio and, since its listing, has advanced through both internal R&D and strategic acquisitions to establish a well-rounded presence across multiple sectors.

Kehua Bio-Engineering: Covering the Entire Industry Chain

As one of China’s first A-share listed, long-established IVD companies, Kehua covers the entire IVD industry chain from a value-chain perspective. This includes R&D and manufacturing capabilities for raw materials, instruments, and reagents; its own distribution channels; a third-party medical service center; and application support and after-sales services.

Kehua’s product portfolio focuses on three key segments: clinical chemistry, immunodiagnostics, and molecular diagnostics. Additionally, the company maintains a distribution business for high-end products authorized by Sysmex and bioMérieux.

Getein Biotech: A Leading Player in POCT

Getein Biotech was founded in 2002 by Dr. Su Enben, a cardiologist at Jiangsu Province Hospital. At its inception, the company consisted only of Dr. Su and a few assistants. Through the team’s relentless efforts, they successfully developed the Full-throughput POCT Fluorescence Immunoassay Quantitative Analyzer and its associated reagents. Currently, Getein Biotech’s product portfolio spans multiple technological platforms, including POCT, clinical chemistry, chemiluminescence, and hematology. Its testing solutions cover a wide range of diagnostic areas, such as cardiovascular diseases, inflammation, renal function, thyroid function, hormones, glucose metabolism, and blood cells.