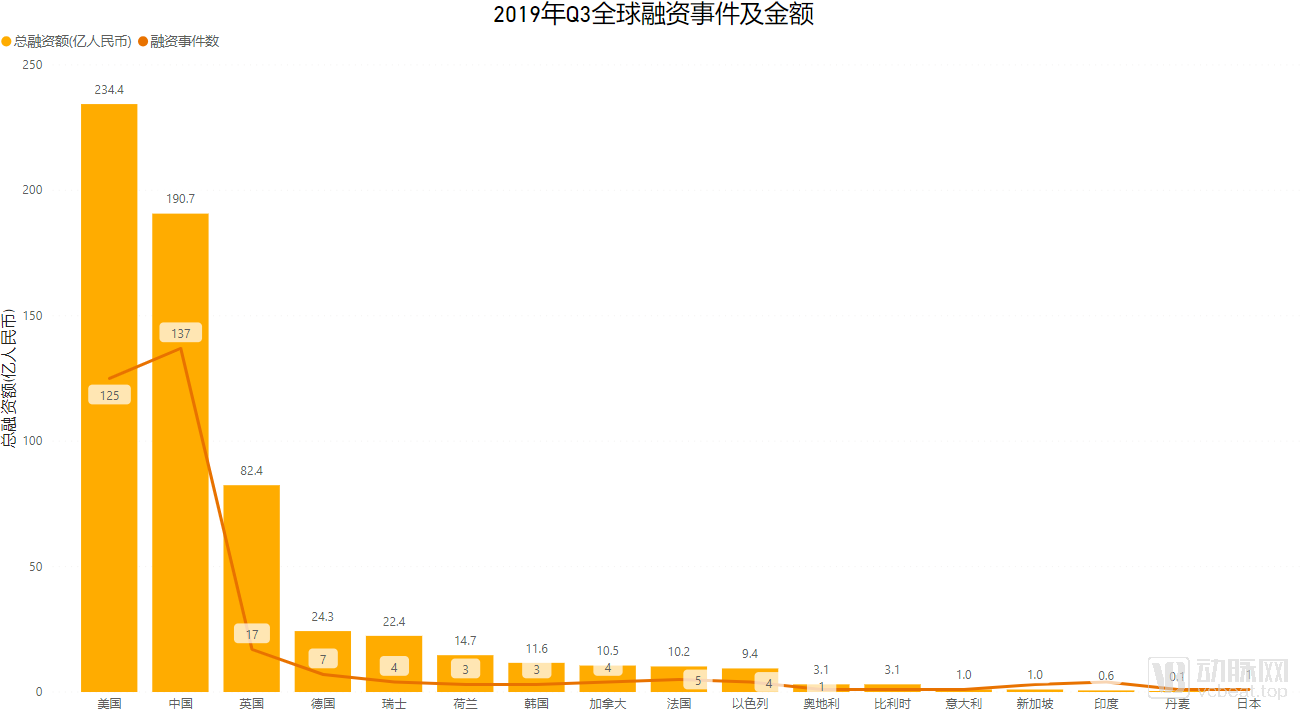

China Surpasses US in Healthcare Financing Deals: 137 vs 125 in Q3 2019

HongShan

Business Consulting, Enterprise Management Consulting Investment Institutions

In the third quarter of 2019, a total of 323 financing deals occurred in the global healthcare industry, with the total amount reaching RMB 62 billion (approximately USD 8.74 billion). Among these, China recorded 137 financing deals, and the United States recorded 125. (Financing deals with undisclosed rounds and undisclosed amounts are excluded.)

Based on an analysis of 323 financing events and in-depth mining of over 15,000 domestic and international financing data points from the past decade, we have drawn the following conclusions:

1. China leads the world in the number of financing events, with the gap in total funding between China and the United States narrowing; the competition continues, yet significant differences remain.

2. Amid a cooling venture capital market, the healthcare industry has been relatively less affected by fluctuations in the broader investment climate.

3. Biotechnology remained the hottest sector both domestically and internationally in Q3 2019, with the most frequently funded categories including gene therapy, cell therapy, immunotherapy, and molecular therapy.Most companies that received cross-investment from star institutions this quarter were biotechnology firms. In China, health insurance performed particularly strongly.

4. In the third quarter of 2019, Chinese healthcare startups faced increasingly difficult fundraising conditions, with investors exercising greater caution in their decision-making.In Q3 2019, both the total financing amount and the number of financing deals in China declined by more than 25% year-on-year.

5. The optimal fundraising window for healthcare companies is 10–20 months after closing their current financing round, with the 30-month mark serving as a critical juncture that determines whether they can secure the next round of funding.

6.In the third quarter of 2019, a total of 853 investment institutions worldwide participated in investment projects.The number of institutions declined in tandem with the quarterly decrease in financing deals;Meanwhile, mature investors are more active and invest more frequently, while novice investment institutions are relatively cautious.

*For the purpose of statistical analysis, we adhere to the following principles when processing investment and financing data:

1. The financing events covered in this report include only venture capital investments from the angel round up to, but excluding, the initial public offering (IPO); they do not include IPOs, private placements, donations, mergers and acquisitions, or other such events.

2. Merge angel round, seed round, and seed VC into the angel round; merge all rounds containing “A” into Series A; merge all rounds containing “B” into Series B; merge all rounds containing “C” into Series C; and merge all rounds above Series C but below IPO into Series C+.

3. All monetary amounts in the charts and tables of this report are denominated in Renminbi (RMB), with foreign currencies converted into RMB using the average exchange rate for the year in which the event occurred.

4. The 2019 data in this report is current as of September 25, 2019. Any data released after this date is excluded from the statistical scope of this report and will be dynamically updated on the soon-to-be-launched VCBeat Investment and Financing Report channel.

5. Financing amounts in the millions, tens of millions, or hundreds of millions are uniformly categorized as 1 million, 10 million, or 100 million, respectively. Financing events with undisclosed rounds and undisclosed amounts are excluded from the statistics in the charts below.

Source: VCBeat Knowledge Base

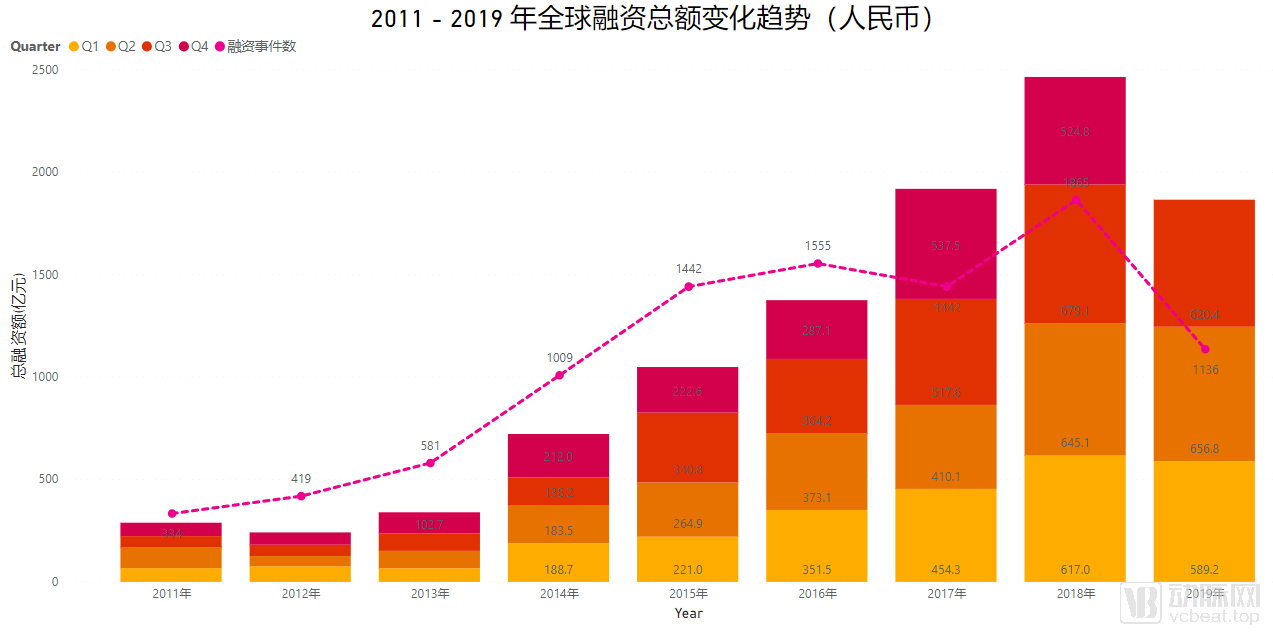

Historical financing data shows that Q3 is often the most active quarter for fundraising, with the amount accounting for about 28% of the full year. In Q3 of 2018, a total of 464 financing events occurred in the healthcare industry, with the financing amount reaching as high as RMB 67.9 billion (approximately USD 10.2 billion), setting a new record for single-quarter financing amounts over the years.

However, the anticipated financing peak did not materialize in the third quarter of this year. As of September 25, 2019, a total of 323 financing deals occurred in the healthcare sector during the third quarter of 2019, with a total financing amount of RMB 62 billion (approximately USD 8.74 billion), representing a decline compared to both the same period last year and the second quarter of this year. Based on this trend, the total global healthcare financing in 2019 is unlikely to surpass that of 2018; instead, it will most likely experience a slight decline, accompanied by a reduction in the number of financing deals.This also means that total global healthcare financing may experience its first decline since 2012.

Source: VCBeat Knowledge Base

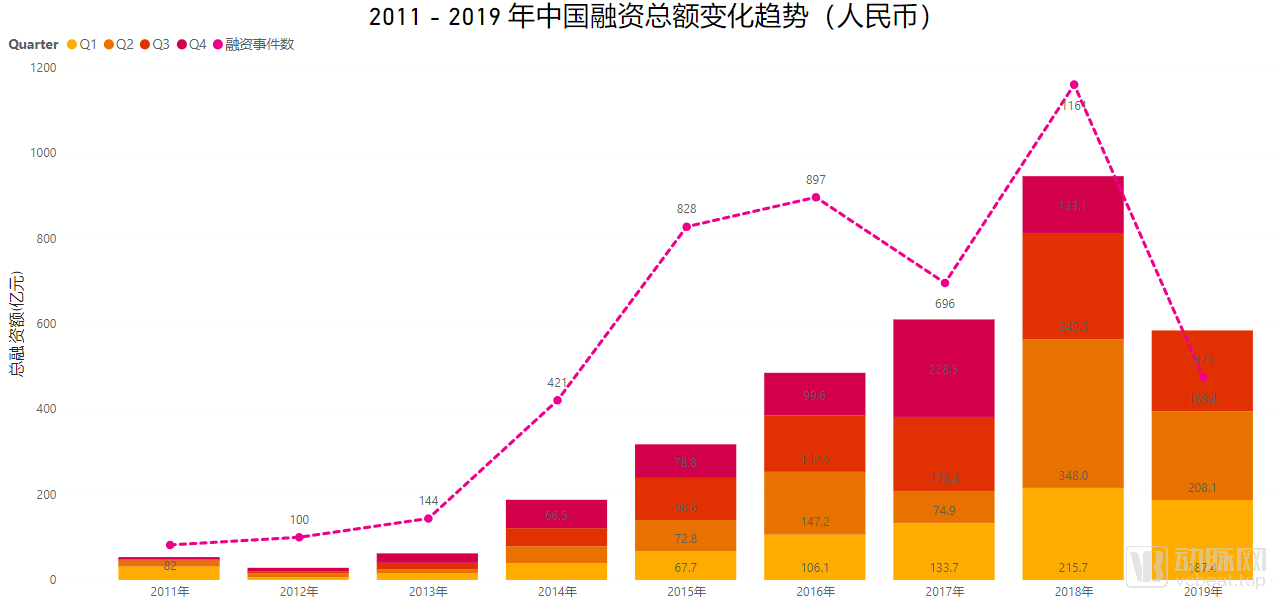

In recent years, the impact of China’s healthcare industry financing volume on the global scale has gradually increased. In 2014, China’s healthcare industry financing accounted for only 24% of the global total; this figure reached 37% in 2018 and stood at 31% in 2019 (as of Q3).

The decline in China’s global share was primarily driven by a 25% year-on-year drop in total financing to RMB 18.93 billion in Q3 2019, bringing the cumulative total for the first three quarters to RMB 58.4 billion, down 28% year on year. Even more pronounced than the decrease in financing amounts was the drop in the number of financing deals: there were 136 deals in Q3 2019, representing a nearly 50% year-on-year decline.The underlying reason may be that investors are exercising greater caution, while Chinese healthcare startups continue to face increasing difficulties in securing financing.

Top 10 Global Healthcare and Medical Financing Deals in Q3 2019

Data Source: VCBeat Knowledge Base

While the total global healthcare financing in 2019 may have experienced a slight decline compared to 2018, the volume is still expected to remain at a high level, exceeding RMB 230 billion (approximately USD 32.3 billion). Meanwhile, the market continues to feature companies with outstanding performance. The top 10 companies in terms of fundraising capability this quarter each secured over USD 100 million, with the three highest amounts all raised by European companies.Four U.S. companies and one Chinese company made the list.

Babylon HealthFounded in 2013, the company raised less than $7 million in its Series A and B financing rounds in 2016 and 2017. In just three years, it secured a $550 million Series C round, marking exponential growth.Its formidable revenue-generating capability is inseparable from Babylon’s three core labels: artificial intelligence, digital health, and chronic disease management.

This UK-based digital health startup is committed to democratizing healthcare by leveraging artificial intelligence to make medical services convenient and affordable for everyone. Babylon Health has established partnerships with Tencent, TELUS, and Samsung. The company currently serves 4.3 million users globally and has conducted over 1.2 million digital consultations.

Babylon’s AI Doctor is a telemedicine app recently launched by Babylon Health, providing users with round-the-clock medical consultation services. For instance, when users describe their symptoms or physical condition within the app, the AI doctor can provide health assessments and offer recommendations on whether to seek hospital care or purchase over-the-counter medications. Additionally, the app offers services such as health tracking and medication delivery.

Ranked SecondBioNTechIt is a biopharmaceutical company. The company’s fundraising in 2018 was already quite impressive: it secured $270 million in Series A financing in January 2018, followed by a $425 million strategic investment from Pfizer in August. In less than a year, the company raised another $325 million in Series B financing this July.

BioNTech’s personalized mRNA technology has established three therapeutic platforms: cancer immunotherapy, infectious disease vaccines, and protein replacement therapies. The CAR and TCR platforms developed by BioNTech are rapid and flexible, enabling the isolation of T-cell receptors (TCRs) from a patient’s individual T cells in as little as 11 days. The company has developed a broad and diverse portfolio of immune receptor candidates, including more than 160 functional, experimentally validated TCRs targeting over 20 different tumor antigens, and more than 60 types of T cells with modified antigen epitopes.

In terms of industry distribution, six biotechnology companies made the list. This is primarily because biotech firms require greater upfront capital and investment, leading to generally higher valuations. Particularly after going public, their stock prices often exceed their initial IPO prices. The high investment returns realized upon exit at this stage have made the biotechnology sector a top choice for investment institutions.

China'sSinotechRanking among the Top 10 financing deals in Q3 2019 by virtue of its RMB 1.1 billion+ Series C round completed on September 6, this transaction stands as one of the largest financing projects in China’s medical device distribution sector in 2019. Committed to becoming “China’s leading digital supply chain comprehensive service provider for medical devices,” Guoke Hengtai delivers all-encompassing “digital supply chain ecosystem platform services” to medical device manufacturers, distributors, end-user hospitals, government regulatory authorities, and other stakeholders.

Source: VCBeat Knowledge Base

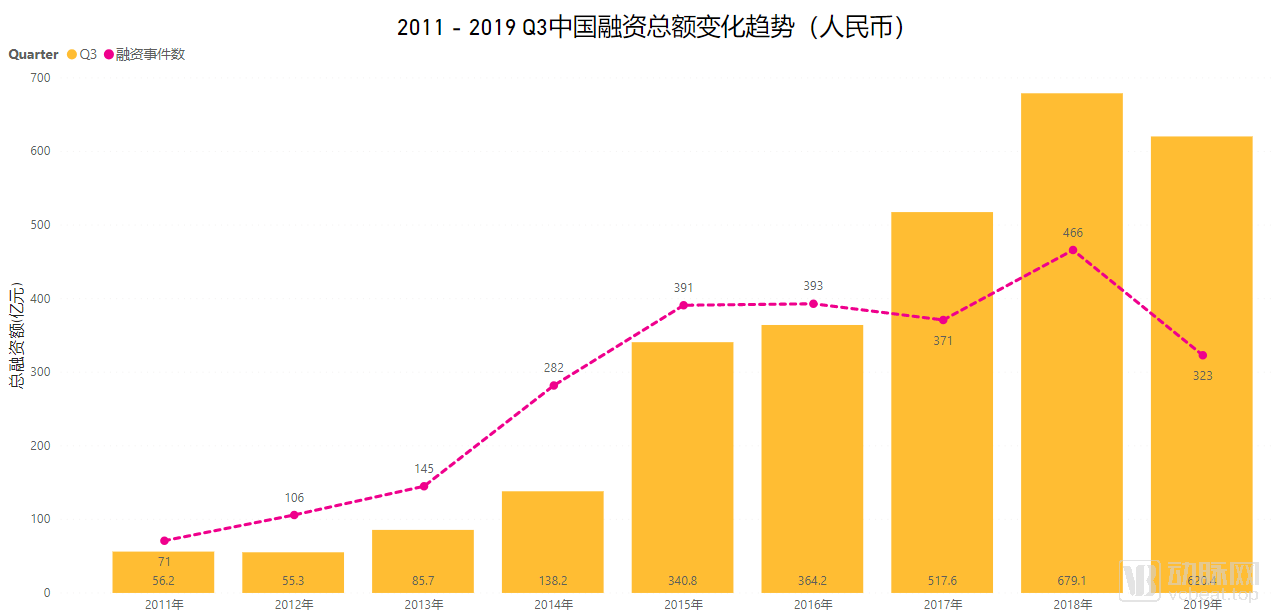

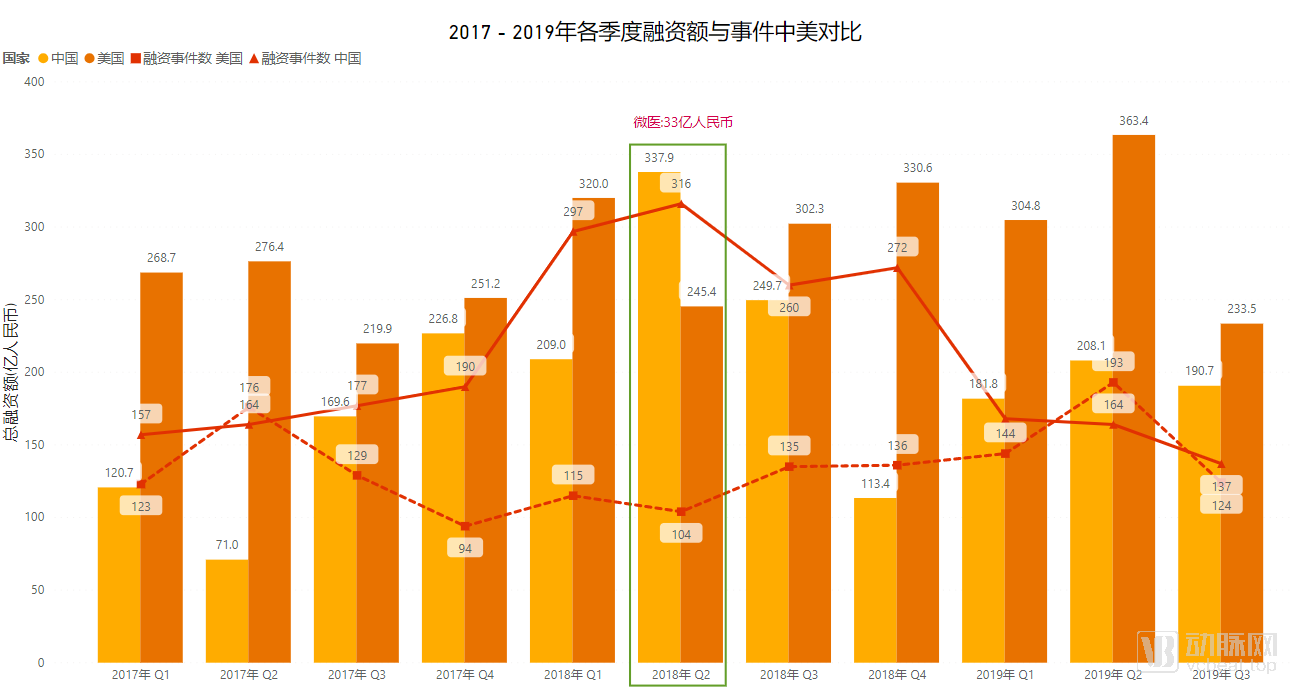

A review of global financing totals and deal counts shows that China and the United States have consistently ranked as the top two countries over the past decade. In the third quarter of 2019, the combined financing volume in these two countries accounted for 68% of the global total, while their share of deal numbers reached as high as 81%. The evolving trends in healthcare venture capital investment in China and the United States will be a key focus for the industry in the coming years.

Data Source: VCBeat Knowledge Base

The United States has long led in total venture capital investment in the healthcare and medical industry. In recent years, China has been steadily narrowing the gap with the United States. In the third quarter of 2019, China surpassed the United States in the number of financing deals, with 137 transactions compared to 125 in the United States, while also reducing the disparity in total financing amount.

In the second quarter of 2018, China’s funding volume once led the United States by nearly RMB 10 billion, primarily driven by WeDoctor’s raise of over RMB 3.3 billion for its internet healthcare service platform, as well as a wave of financing rounds for biopharmaceutical companies including CStone Pharmaceuticals, I-Mab Biopharma, Genor Biopharma, and Brii Biosciences.

Source: VCBeat Knowledge Base

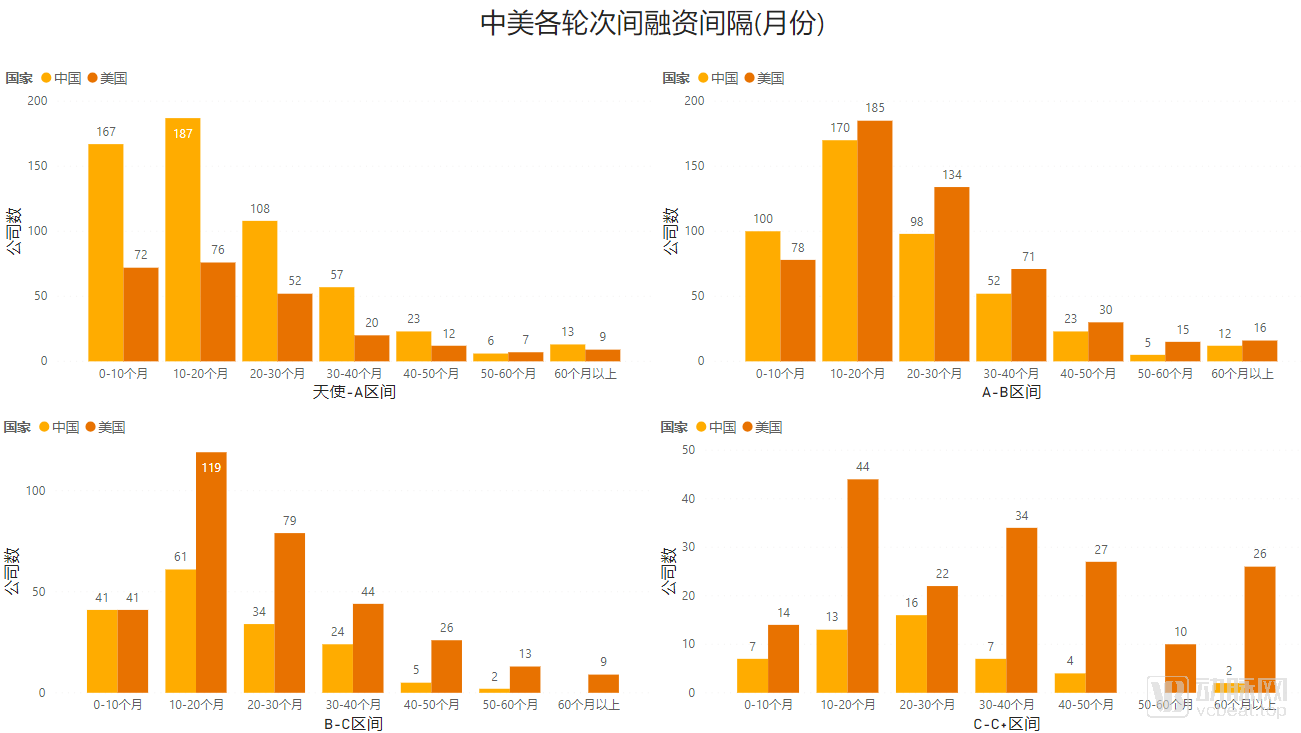

VCBeat’s comparative analysis of financing intervals between Chinese and U.S. companies reveals:

(1)The financing intervals in China and the United States are comparable.From the angel round to Series A, most companies secure their next round of funding within the first 20 months; from Series A to Series B, 75% of companies complete financing within 30 months; and from Series B to Series C, approximately 70% of companies do so within 30 months.

(2)U.S. companies exhibit a more dispersed financing cycle, whereas Chinese companies show a more concentrated one.This trend is particularly evident in the A-to-B and B-to-C funding rounds: From Series A to Series B, 24% of U.S. companies still secured financing after 30 months, compared to only 20% in China; after 40 months, 11% of U.S. companies successfully raised funds, whereas only 8% did so in China. From Series B to Series C, 28% of U.S. companies completed financing within 30 months, compared to just 23% in China; after 40 months, 14% of U.S. companies advanced to Series C, while only 9% did so in China.

Excluding companies that no longer have financing needs,For most healthcare startups in China, the first 30 months post-financing may be the critical juncture determining whether a company can secure its next round of funding, with the period between 10 and 20 months representing the optimal window for achieving the highest success rate in fundraising.After more than 30 months, the likelihood of securing financing smoothly is relatively low; for U.S. companies, however, many have missed the optimal fundraising window yet still managed to successfully close their next funding round.

According to statistics from the VCBeat knowledge base, there are 440 companies in China that have not announced a new round of financing 30 months after completing their Series A funding, and 57 companies that have not announced financing 30 months after completing their Series B funding. Additionally, 103 companies are currently in the critical period of 10–20 months post-Series B completion, with market attention focused on potential financing announcements from these firms.

Data Source: VCBeat Knowledge Base

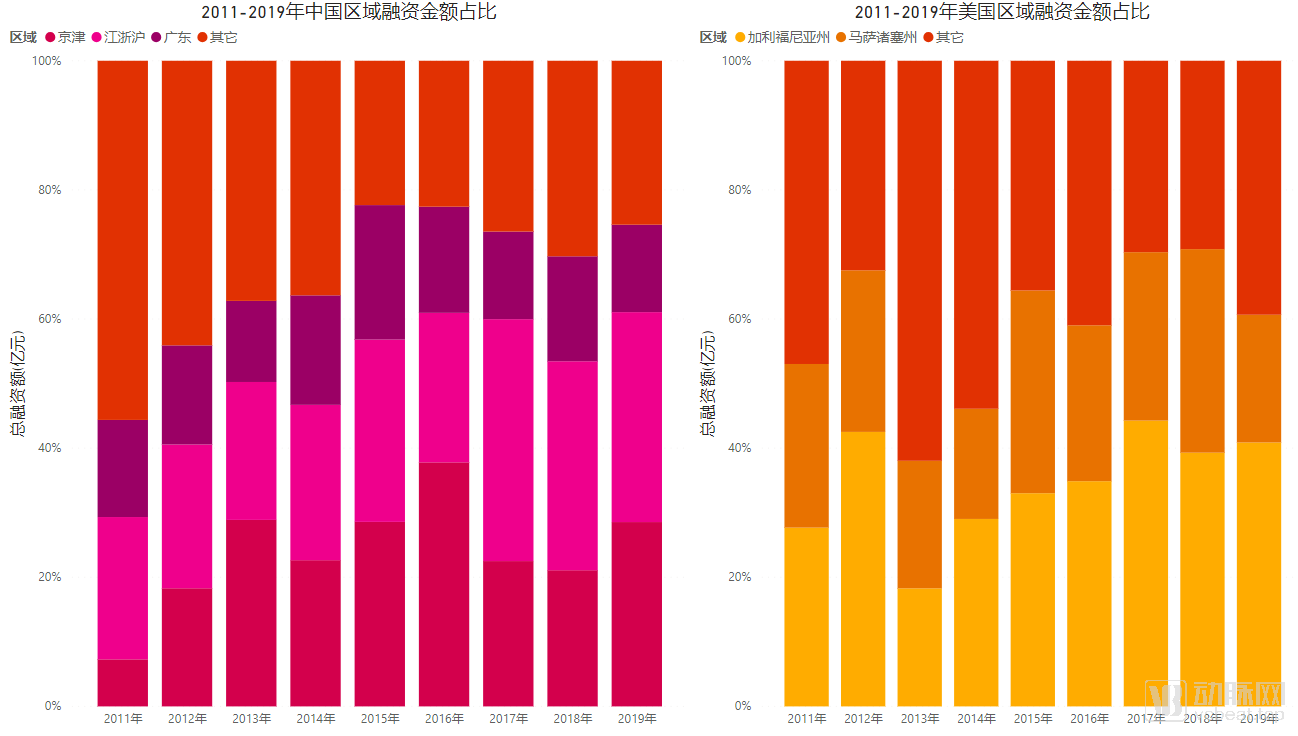

The Jiangsu-Zhejiang-Shanghai region, the Beijing-Tianjin area, and Guangdong are the three most active regions for venture capital investment in China’s healthcare industry. In Q3 2019, these three regions accounted for a total of 118 financing deals, representing 75% of the total financing amount nationwide. Among them, the Jiangsu-Zhejiang-Shanghai region had the highest share, capturing 32.5% of the national financing amount. In the United States, 60% of financing deals occurred in California and Massachusetts, totaling 85 deals. Of these, California saw 56 deals, with its financing amount accounting for 40% of the U.S. total.

A comparative analysis reveals that California has consistently maintained its dominance in U.S. healthcare venture capital investment. Leveraging its renowned biotechnology industry cluster and abundant medical resources, Massachusetts has surpassed the more economically developed New York State to become the second-largest state for healthcare venture capital investment in the United States; however, its total volume still lags significantly behind that of California.

In China, venture capital investment in the healthcare industry is more concentrated, with development across the three major regions being relatively more balanced and showing a stronger correlation with the level of economic development.In recent years, the Jiangsu-Zhejiang-Shanghai region has seen its influence in the healthcare industry grow steadily. Since 2017, its total financing volume has comprehensively surpassed that of the Beijing-Tianjin region, and it is expected to become China’s largest healthcare industry cluster in terms of venture capital investment scale.

Source: VCBeat Knowledge Base

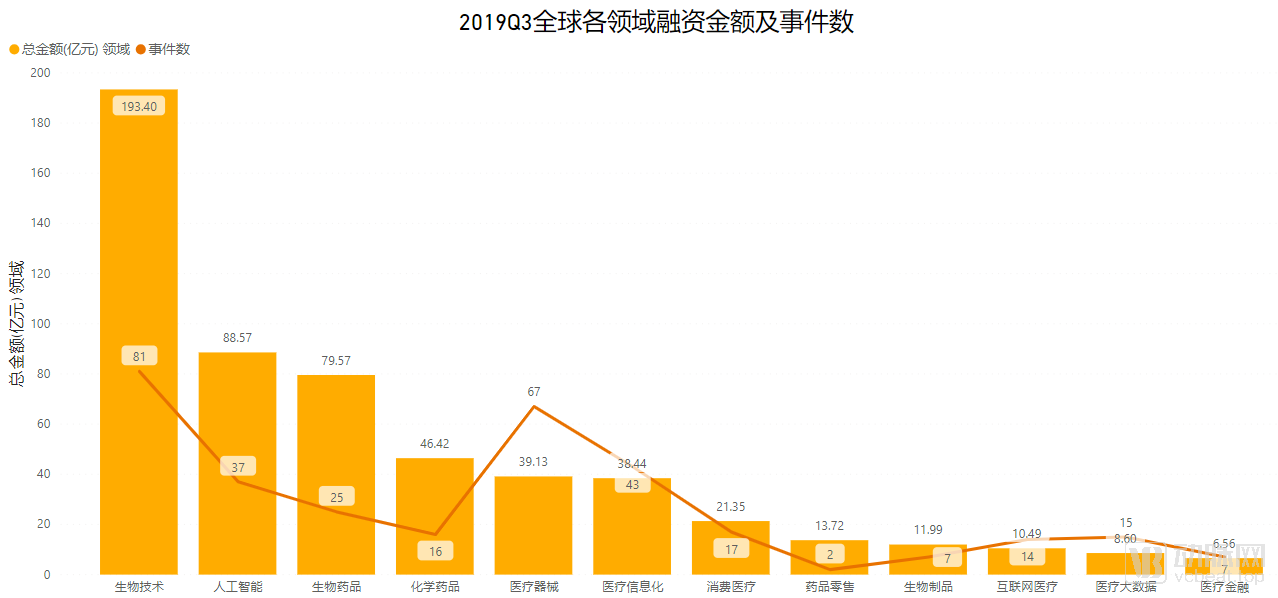

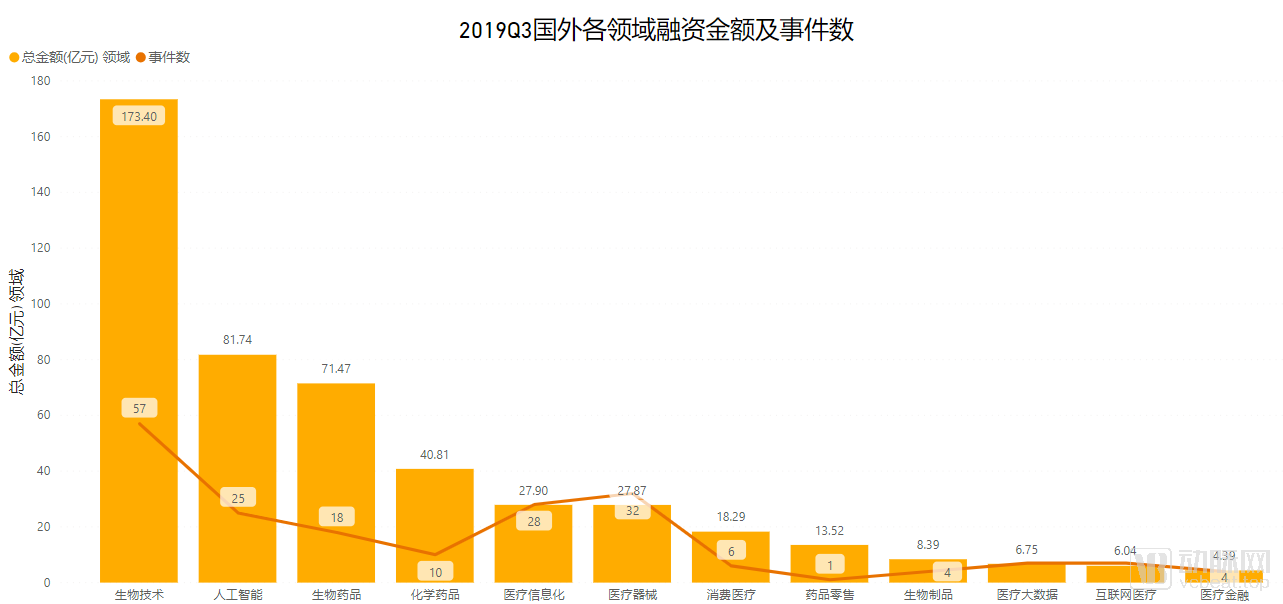

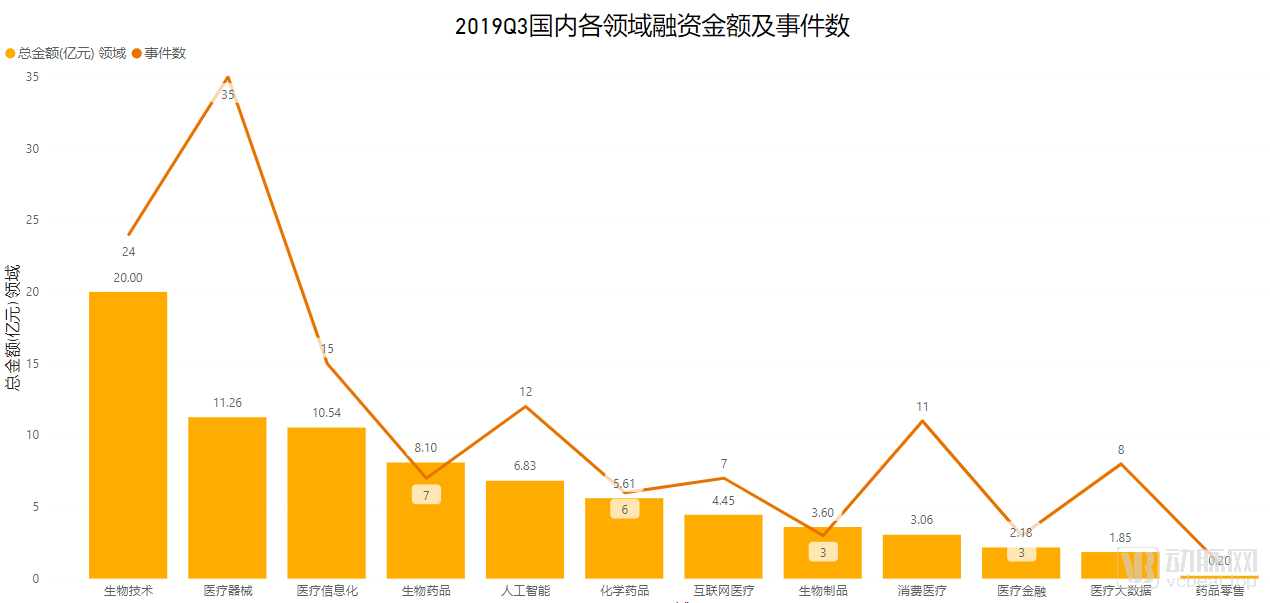

Globally, biotechnology remains the hottest investment sector,81 financing deals, with a total amount of RMB 19.34 billion, accounting for 31% of the total financing in Q3 2019. The pharmaceutical sector (biological drugs + chemical drugs + biological products) and artificial intelligence ranked second and third, respectively.

Source: VCBeat Knowledge Base

Abroad, biotechnology, artificial intelligence, and biologics emerged as the three hottest subsectors in the third quarter of 2019.Among these, the biotechnology sector abroad witnessed 57 financing events, with a total funding amount of RMB 17.3 billion, surpassing the combined total of artificial intelligence and biopharmaceuticals, which ranked second and third, respectively.Immunotherapy, cell therapy, targeted therapy, and gene technology have become the hot keywords for overseas financing projects this quarter.

Source: VCBeat Knowledge Base

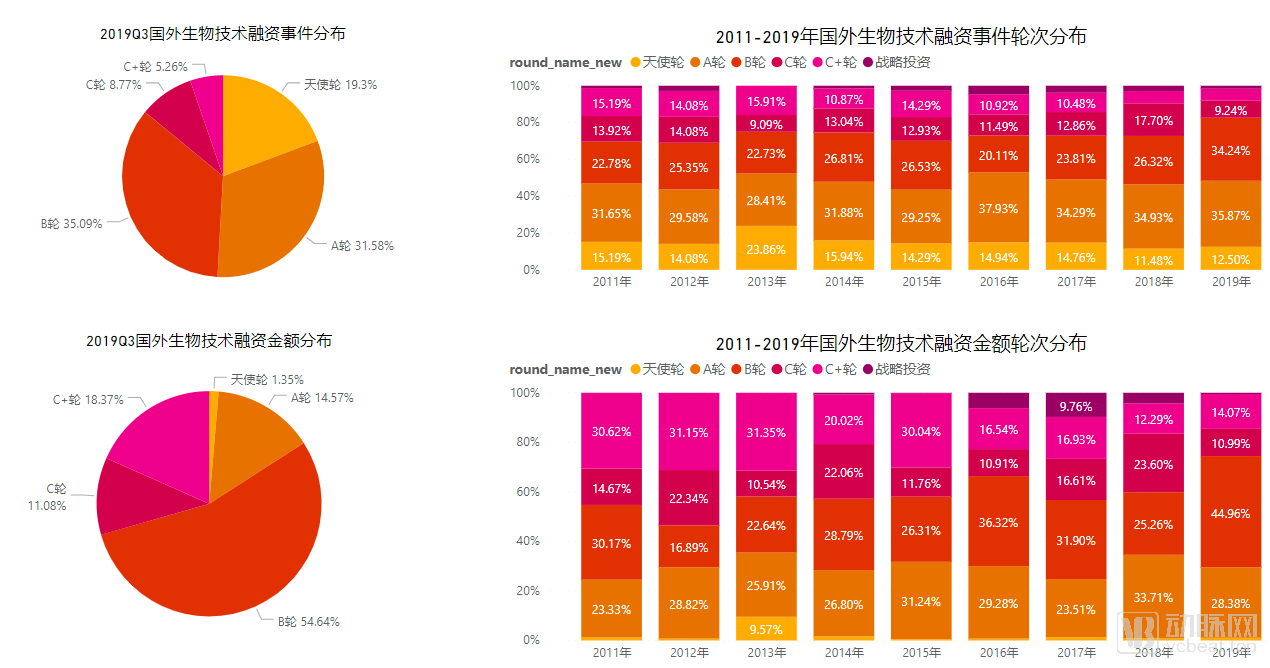

2019 also marked the year with the highest proportion of Series B financing in the global biotechnology sector, reaching 54.64%, while the share of Series A financing decreased by 10%. This was partly attributable to Europe’s largest private biopharmaceutical companyBioNtechOver RMB 2 billion in financing, and a well-known company in early cancer screeningFreenome, Emerging Cell Therapy CompanyAchilles TherapeuticsOn the other hand, it also reflects the trend of delayed project maturity in the overseas biotechnology sector.

In the third quarter of 2019, Switzerland ranked first in foreign biotechnology financing.Oncology Drug Development CompanyADC TherapeuticsOn July 6, ADC Therapeutics announced the closing of a $103 million expansion of its Series E financing round, bringing the total amount raised in Series E to $303 million. Investors in this round included Auven Therapeutics and AstraZeneca, among others.

ADC Therapeutics, founded in 2011, is dedicated to the development of proprietary antibody-drug conjugates (ADCs) targeting hematologic malignancies and solid tumors. Its ADC products consist of monoclonal antibodies targeting specific antigens linked to PBD dimers via Spirogen Limited’s PBD technology. The company has multiple PBD-based ADC candidates in ongoing clinical trials, with clinical research laboratories located across the United States and Europe.

ADC Therapeutics has four R&D pipelines: ADCT-402, ADCT-301, ADCT-602, and ADCT-601. The company’s lead candidate, ADCT-402 (loncastuximab tesirine), is undergoing Phase 2 studies for relapsed or refractory diffuse large B-cell lymphoma (DLBCL), with plans to submit a Biologics License Application (BLA) to the FDA in the second half of 2020 as a monotherapy for this specific blood cancer.

Moreover, in the two subsectors that saw the most frequent financing activity abroad in Q3 2019—biotechnology and artificial intelligence—an increasing number of companies operate at the intersection of these fields. These companies aim to enhance the R&D efficiency of innovative therapies and the accuracy of cancer screening through artificial intelligence, machine learning, and other technologies, as exemplified by Freenome and Recursion Pharmaceuticals.

On July 24, Freenome, a prominent company in the U.S. early cancer screening sector, announced the completion of its $160 million Series B financing round, with investors including RA Capital, Polaris Partners, and China Renaissance Capital.

Freenome is a biotechnology company that pioneered the most comprehensive multi-omics platform for early cancer detection. By combining deep expertise in molecular biology with advanced computational biology and machine learning techniques, it identifies disease-related patterns from billions of circulating cell-free biomarkers.

Freenome specializes in AI Genomics, leveraging deep learning algorithms to analyze genomic patterns. By detecting hidden correlations imperceptible to conventional medical methods, this technology enables disease prediction, diagnosis, and even localization of pathological sites. Specifically, by analyzing patients’ blood samples, Freenome’s AI system filters cancer-specific signals from immune system markers. Through deep learning analysis, it determines whether a patient has cancer and identifies the precise location of the tumor.

On July 15, biotechnology company Recursion Pharmaceuticals completed a $121 million Series C financing round. Investors included Scottish Mortgage Investment Trust and Intermountain Ventures, among others.

Recursion Pharmaceuticals is a clinical-stage biotechnology company that integrates artificial intelligence, experimental biology, and automation, primarily engaged in large-scale drug discovery and development. By combining experimental biology and automation with artificial intelligence within a massively parallel system, it effectively identifies potential drug candidates for various indications, including genetic disorders, inflammatory diseases, immunological conditions, and infectious diseases. The proceeds from this financing round will support Recursion’s continued expansion of its machine learning-enabled drug discovery platform, as well as the development of new capabilities designed to fundamentally accelerate the identification of new chemical entities and predictive safety pharmacology.

Source: VCBeat Knowledge Base

As a dark horse in the healthcare industry, health insurance may have been the biggest surprise in China’s primary market financing in the third quarter of 2019.

Health insurance is an innovative solution to the current dilemma in healthcare payment. Even though the United States already has a relatively comprehensive health insurance and payment system, public demand for lower-cost care continues to drive transformation in healthcare financing, leading to the continuous emergence of health insurance startups. Currently, the U.S. is home to a large number of industry unicorns, including Clover Health, Humana, and Oscar Health.

In China, the health insurance sector remains a blue ocean. In 2018, ten companies, including Ping An Health Technology, Kangyu, and Yi Hubao, completed angel and Series A financing rounds. Among them, Ping An Health Technology secured over RMB 7 billion in Series A funding, ranking as the number one healthcare financing deal in China for 2018 and single-handedly driving up the total financing volume in the medical finance segment.

Compared to the previous year, the health insurance sector saw more players successfully secure financing in 2019, with both established medical mutual aid platforms and emerging payment technology companies obtaining funding. In the first half of the year alone, six companies, including Waterdrop Inc. and Miao Health, raised over RMB 2 billion. This quarter, five additional health insurance companies sequentially secured financing. On July 8, three enterprises—Yuanxin Huibao, Nuohui Medical, and Zhanlue Data—even simultaneously announced their financing news on VCBeat.

2019 Health Insurance Company Financing List

Company Name | Financing Date | Financing Amount | Financing Round | Investor |

Nuawa Technology | 2019/8/29 | 100 million yuan | Angel Round | Sequoia Capital, Kuanscreen Capital |

Kangyu | 2019/8/22 | Tens of Millions of US Dollars | Series A | Youlun Group, et al. |

Yuanxin Huibao | 2019/7/8 | 50 million yuan | Series A | Sequoia Capital, Qiming Venture Partners |

Nuohui Medical | 2019/7/8 | Undisclosed | Round 2 | Legend Star, BV Baidu Ventures |

Zhanlue Data | 2019/7/8 | Nearly 100 million yuan | Series B | Lingfeng Capital, Paipaidai |

Wukong Insurance | 2019/6/20 | RMB 60 million | Angel Round | 58 Group, Yeepay, Plum Ventures |

Waterdrop Inc. | 2019/6/12 | RMB 1 billion | Series C | Tencent Industry Win-Win Fund, Boyu Capital, and others |

KeyWorld Cloud Health | 2019/5/29 | Not specified | Series A+ | Dilin Corporate Consulting |

Yingshi Health | 2019/5/15 | Unknown | Series B | CICC Hui Cai |

Miao Health | 2019/4/2 | 500 million yuan | Series C | Pacific Insurance’s Investments in the Elderly Care Industry, etc. |

Doubao.com | 2019/3/27 | RMB 95 million | Series C | Benyi Capital, Bojiang Capital, etc. |

Data Source: VCBeat Knowledge Base

Yuanxin Huibao Secures RMB 50 Million in Series A Funding Led by HongShan, Providing Insurers with Solutions for Actuarial Pricing, Risk Control, and User Acquisition. In an interview with VCBeat, Peng Xuan stated that future health insurance will extend beyond mere coverage, evolving toward health management and comprehensive health services.

In terms of business model, Yuanxin Huibao provides policy underwriting services to insurance companies by leveraging its internet hospital platform and drug delivery resources covering nearly 500 Grade A tertiary and oncology hospitals across China. By implementing a multi-layered review process that integrates “online + offline,” “in-hospital + out-of-hospital,” and “system + professional personnel” components, it ensures both the timeliness of underwriting and the compliance of prescriptions at the time of claims, as well as the authenticity of related documentation. This helps insurance companies reduce claims risks and achieve reasonable cost control.

Currently, Yuanxin Huibao has established in-depth collaborations with multiple medical companies and pharmaceutical enterprises, possessing service delivery capabilities in “genetic screening, health check-ups, overseas medical care, online consultations, medication services, and post-diagnosis management.”

Established in November last year,Nuohui Medical, secured Series B financing led by Legend Star, launching health insurance and payment solutions for major diseases that cover medication reimbursement, efficacy guarantees, and medication security.Zhanlue DataSecured nearly RMB 100 million in Series B financing led by Fen Capital, providing enterprise-level big data risk control solutions for insurance companies and insurance intermediaries.

Currently, these companies are still in the early stages of financing. It is expected that their growth will soon bring more innovative payment solutions.

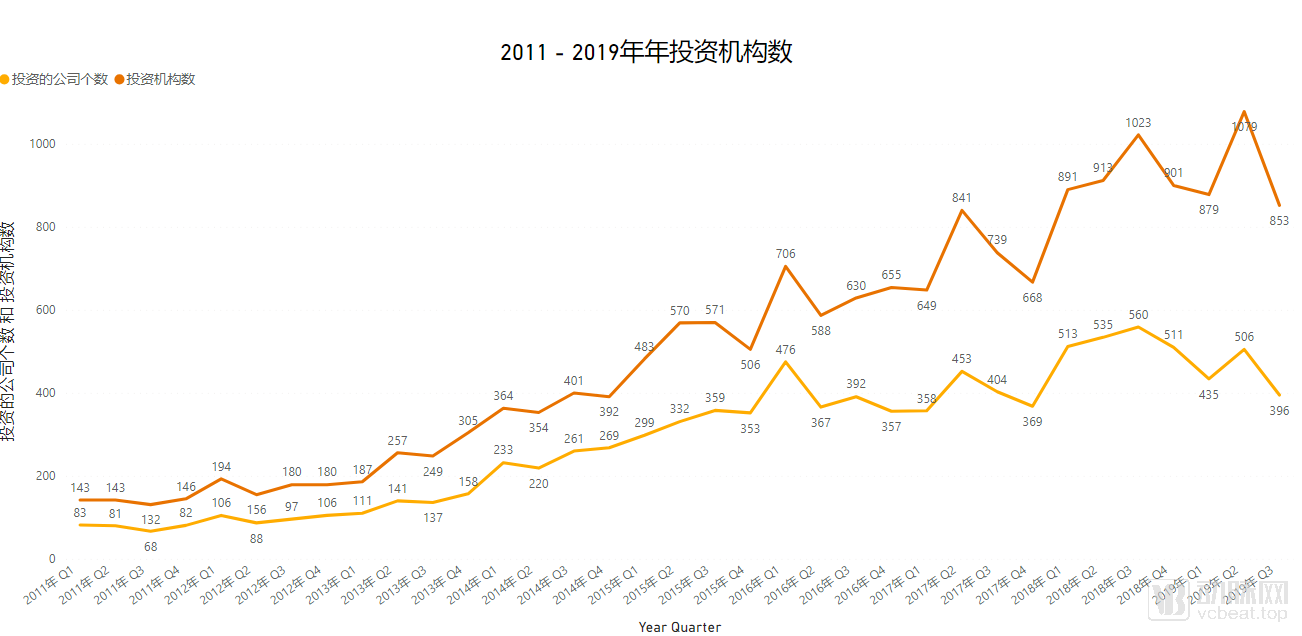

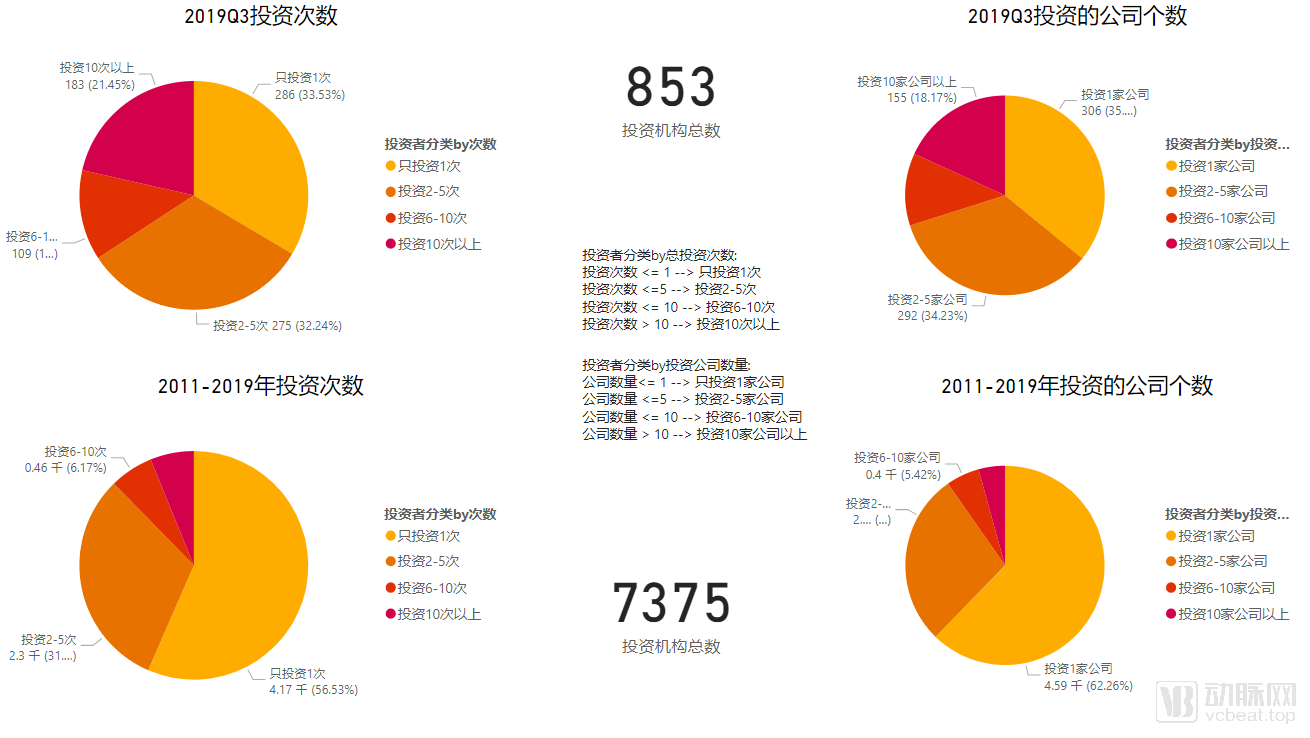

In the third quarter of 2019, a total of 853 investment firms participated in funding globally, marking the lowest level in the past seven quarters. The number of institutions and the number of funded projects showed a positive correlation; as the number of funded projects declined in this quarter, the number of participating investment firms also decreased.

Data Source: VCBeat Knowledge Base

From the perspective of the number of investments made by institutions and the number of portfolio companies, changes in investment firms became more pronounced in Q3 2019. The proportion of institutions that invested only once decreased by 22%, while the share of those investing in just one company dropped by 26%. In contrast, there was a significant increase in the proportion of institutions making more than six investments and those investing in more than six companies.

This shift more intuitively reflects a trend toward investor consolidation, with large institutions possessing substantial strength and abundant resources becoming more active and increasing their investment frequency, while smaller firms or novice investors new to the healthcare sector are adopting a more cautious approach. In the future, healthcare investment firms are likely to become more refined and specialized, potentially raising the entry barriers for investment in the healthcare industry.

Data Source: VCBeat Knowledge Base

Among the most active investment firms in the third quarter of 2019, there were four U.S. companies, three Chinese companies, and one French company.Among them, HongShan China Fund and Perceptive Advisors tied for first place, each with seven investments. Deerfield, Invus, Kurma Partners, OrbiMed, Qiming Venture Partners, and Legend Star followed closely behind, each with six investments.

These companies, which have received cross-investment from several top-tier investment firms, include foreign entities such as Frequency, Oncorus, Kronos Bio, Achilles, and Insilico Medicine, as well as domestic companies such as Yuanxin Huibao, Weiyuan Gene, Gaocheng Biology, and Qihan Biology.Securing support from more than two top-tier investment firms reflects the potential and strength of these startups.

Most of these startups are biotechnology companies with leading hard-core technologies, involving advanced therapeutic techniques such as gene therapy, immunotherapy, and molecular therapy. OverseasFrequencyAimed at developing drugs for hearing impairment using molecular therapy,OncorusFocused on developing oncolytic virus cancer immunotherapy,Kronos Biois the development of anticancer drugs through a small-molecule microarray platform; in China,WeGeneFocused on precision medicine for infectious diseases, it possesses two core technological products: the pathogen metagenomics platform IDseq™ and the pathogen CRISPR rapid diagnostic platform ID-CRISPR™;Gaocheng BiotechLeverage its proprietary single-cell analysis platform to dissect the immune system and develop therapeutic antibody drugs;Qihan BiotechApplying the latest gene-editing technologies to xenotransplantation to address the global shortage of donor organs.

By analyzing investment and financing data in the healthcare industry for Q3 2019, the highlight of this report is the review and comparison of financing trends in the Chinese and U.S. healthcare sectors. While a certain development gap still exists between China and the United States, Chinese healthcare companies continue to grow and expand. In the future, Chinese enterprises should place greater emphasis on product R&D and market expansion, aligning with national policy trends regulating the healthcare industry.

The biotechnology sector will continue to be the primary focus of capital both domestically and internationally. To catch up with the United States, China must secure its footing in this critical strategic arena. A cohort of high-quality biotechnology enterprises has already emerged in China, driving a steady increase in investment and financing within the country’s healthcare sector.

Meanwhile, we observe that against the backdrop of a cooling global venture capital market, investment and financing activity in the healthcare sector has been somewhat dampened, with deal pacing slowing down and institutional investors adopting a more cautious approach to decision-making. In this environment, those healthcare companies with solid foundations, robust technologies, and genuine value, along with mature healthcare investors, remain steadfast. In the long run, the return to intrinsic value remains an enduring theme.

He Qiongfeng from the Data Department and Shi Anjie from the Research Institute also contributed to this report.

For more investment and financing information, please scan the QR code to follow the VCBeat channel.

↓ ↓ ↓