Pharmaceutical Retail Industry Panorama: Prescription Diversion Drives Long-Term Growth Amid Saturation and Intensified Competition

Recently, Ping An Securities released the report “Panoramic View of the Drug Retail Industry,” which outlines the current state and future trends of the industry from three key dimensions—pharmaceuticals, pharmacies, and personnel. By integrating the characteristics of each element, the report presents a comprehensive overview of the sector and includes case studies analyzing the strategic layouts of several leading enterprises. To provide further insights and reference for the industry, VCBeat has organized and published the report with authorization.

The report includes the following key points:

Pharmaceuticals: Industry Concentration Continues to Rise, with Prescription Outflow Driving Long-Term Growth

In 2018, China’s pharmaceutical retail channel achieved sales of RMB 391.9 billion, accounting for 22.9% of total terminal pharmaceutical sales. Due to the significant competitive advantages of medium-to-large chain enterprises and against the backdrop of increasingly stringent industry regulation, industry concentration has continued to rise, with the CR10 reaching 17% and the CR100 reaching 31% in 2017. Policy-driven separation of prescribing from dispensing is a long-term trend; the resulting market size for outpatient prescription outflow is nearly RMB 300 billion, which could contribute over 50% incremental growth to the pharmaceutical retail market.

Pharmacies: The number of pharmacies across China is approaching saturation, with structural adjustments driving an increase in the chain store rate.

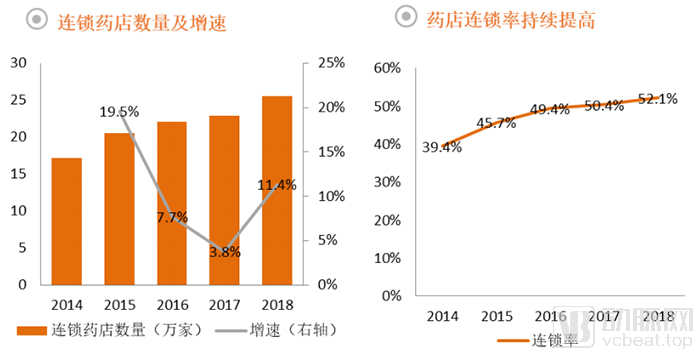

In 2018, the total number of pharmacy outlets in China reached 489,000. Since 2010, the market has gradually become saturated, with the growth rate declining from over 5% to 0–3%. The average number of people served per pharmacy was 2,850, approaching the World Health Organization’s recommendation of 2,500 people per outlet. Given the significant competitive advantages of chain pharmacies over independent ones, the growth rate of chain pharmacies has outpaced the overall industry growth in this mature, stock-competition market. From 2014 to 2018, the chain pharmacy penetration rate increased from 39.4% to 52.1%.

Licensed Pharmacists: Significant Shortage of Licensed Pharmacists; Remote Prescription Review Helps Address the Gap

China has 468,000 registered licensed pharmacists, equating to 3.4 licensed pharmacists per 10,000 people. This figure still falls significantly short of the standard of 6.2 licensed pharmacists per 10,000 population published by the International Pharmaceutical Federation (FIP). According to data from November 2016, the staffing rate of licensed pharmacists in retail pharmacies was only 51%, meaning approximately half of all pharmacies lacked a licensed pharmacist, with an estimated shortage of 200,000 licensed pharmacists. To address this shortage, many provinces have introduced remote prescription review as a solution, which will effectively mitigate the lack of licensed pharmacists and support the development of the pharmaceutical retail sector.

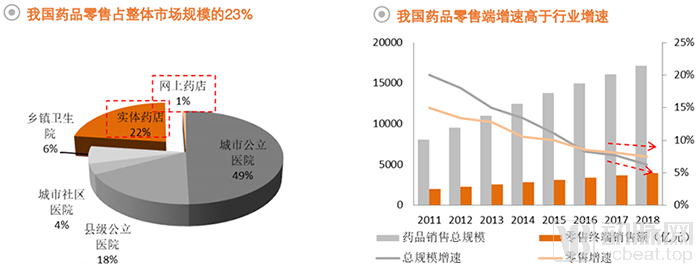

Retail is one of the important channels for pharmaceutical sales terminals in China. According to statistics from Menet, China's pharmaceutical sales scale reached 1.7131 trillion yuan in 2018, with retail channel sales amounting to 391.9 billion yuan, accounting for 22.9%, a year-on-year increase of 7.5%. Among them, physical pharmacies achieved sales of 382 billion yuan, accounting for 22%, while online pharmacies recorded sales of 9.9 billion yuan, representing 1%.

Data source: Menet, Ping An Securities Research Institute

Prior to 2015, driven by factors such as the expansion of medical insurance coverage and rapid macroeconomic growth, the growth rate of the pharmaceutical retail channel lagged behind the overall growth rate of pharmaceutical sales, although the gap between the two gradually narrowed.

Around 2015, healthcare reform entered a critical phase, with policies such as caps on the drug-to-revenue ratio, elimination of drug markups, and controls on adjunctive medications being implemented. These measures impacted hospital drug sales, leading to a significant slowdown in growth. In this context, some manufacturers shifted their focus to retail channels, and the outflow of prescriptions brought new incremental growth to pharmaceutical retail. Consequently, since 2016, the growth rate at the pharmaceutical retail end has exceeded the overall growth rate of the pharmaceutical sales industry.

Industry Concentration Continues to Rise, with Leading Companies Demonstrating Strong Revenue-Generating Capabilities

Data Source: Statistical Analysis Report on Pharmaceutical Circulation Operations, NMPA, Ping An Securities Research Institute

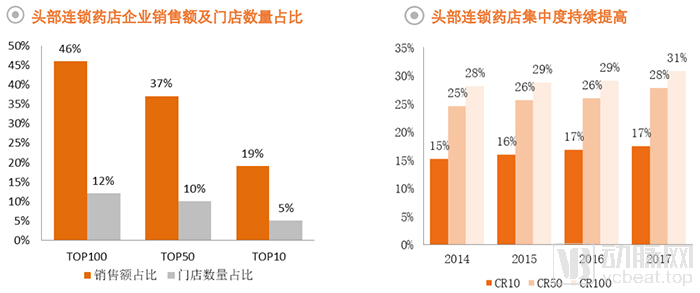

As shown in the figure above, in 2017, the top 100 chain pharmacy enterprises in China accounted for 12% of the total number of stores, while their revenue share reached 46%. The top 10 chain pharmacy enterprises accounted for 5% of the total number of stores, with a revenue share of 19%, indicating that leading enterprises have stronger revenue-generating capabilities per store.

Furthermore, the CR10, CR50, and CR100 of chain pharmacies increased year by year from 2014 to 2017, indicating a continuous rise in industry concentration.

However, the market concentration of the top three chain pharmacies in the United States is 77%, while that in Japan is 17%. In China, the concentration of the top three chain pharmacies stands at only 7.4%, indicating that the market remains relatively fragmented from this perspective.

Retail pharmacy sales categories: Chinese patent medicines account for a relatively high proportion.

Data Source: 2017 Statistical Report on Pharmaceutical Operations and Distribution, Ping An Securities Research Institute

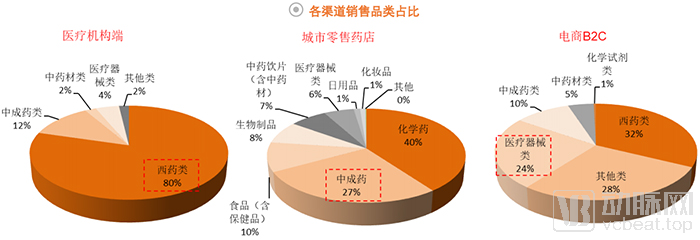

The sales distribution of various drug categories across different terminals in China exhibits distinct characteristics.

For example, the medication structure in medical institutions is dominated by Western medicines. Western medicines account for 80% of the medications used in medical institutions, followed by proprietary Chinese medicines at 12%. The category of Western medicines here includes chemical drugs, biological products, blood products, vaccines, and others.

Among the product categories sold in retail pharmacies, proprietary Chinese medicines (PCMs) account for a significant share. Due to the large number of over-the-counter (OTC) PCMs and their ability to meet patients’ needs for self-diagnosis and treatment, PCMs perform well in retail pharmacy sales. Their share in retail pharmacies reaches 27%, significantly higher than their proportion in medical institutions.

In the pharmaceutical e-commerce sector, medical devices account for a significant share. Medical devices constitute 24% of B2C e-commerce sales, second only to Western medicines. This category primarily includes home-use medical devices such as electronic blood pressure monitors and wheelchairs, as well as family planning products.

Prescription Outflow Drives Long-Term Growth, with Market Size Approaching RMB 300 Billion

Data Source: Menet, Ping An Securities Research Institute

Data Source: Menet, Ping An Securities Research Institute

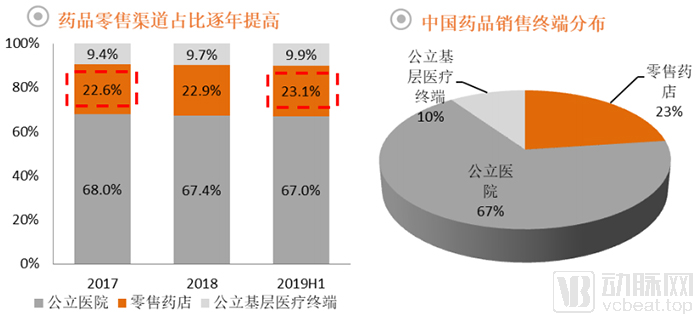

Over the past three years, public hospitals have restricted the "drug-to-revenue ratio" and abolished drug markups, making prescription outflow a major trend. Data from various sales terminals aligns with this trend: over the past two years, the share of drug sales through the public hospital channel declined from 68% to 67%, while the share through the retail pharmacy channel rose from 22.6% to 23.1%. Our grassroots research on large domestic chain pharmacies indicates that the proportion of prescription drug sales has been increasing by approximately 2 percentage points annually.

Currently, among the three major sales channels for pharmaceuticals in China, retail pharmacies account for only 23%, while public hospitals account for 67%, with medication expenditures reaching RMB 1.15 trillion. Assuming that 50% of pharmaceuticals in public hospitals are prescribed in outpatient settings, and half of these outpatient prescriptions are dispensed externally at pharmacies, the resulting market value would reach RMB 287.5 billion, driving an incremental growth of over 50% in the pharmaceutical retail market.

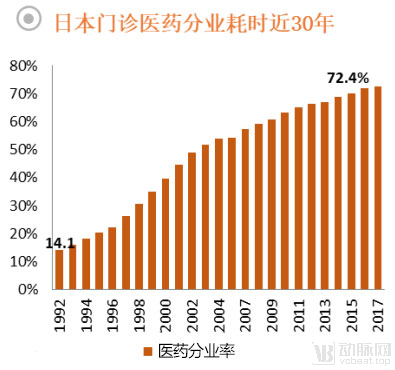

However, the outflow of prescriptions is a long-term process. Japan began promoting the separation of prescribing and dispensing in the 1990s, and it took nearly 30 years to achieve a separation rate of 72.4% by 2017. It is expected that China will also require a considerable amount of time to fully implement the separation of prescribing and dispensing.

Note: Prescription Outflow Rate = Number of prescriptions dispensed at pharmacies / Number of outpatient prescriptions issued by medical institutions.

Data Source: Menet, Ping An Securities Research Institute

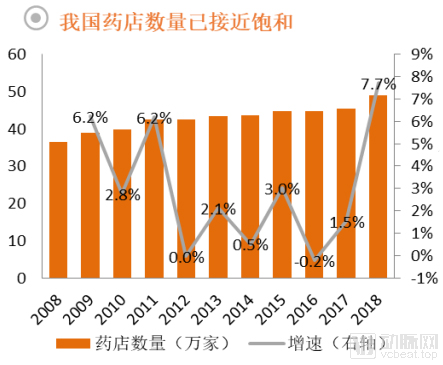

Amid the overall rapid growth of the pharmaceutical retail industry, the number of pharmacies has continued to increase. In 2018, China had 5,671 retail pharmacy chains, with 255,000 chain-affiliated stores and 234,000 independent retail pharmacies, bringing the total number of pharmacies nationwide to 489,000.

The number of pharmacies has approached saturation, with growth slowing down.

Data Source: China Pharmacy, Ping An Securities Research Institute

Although the total number of pharmacies has shown an overall upward trend, the growth rate began to slow down after 2010, dropping from over 5% to between 0% and 3%. Starting in 2015, policy reforms in the pharmaceutical industry led to increasingly stringent regulation of the drug retail sector. Local drug administrations conducted unannounced inspections to verify whether licensed pharmacists were on duty, whether storage conditions at pharmacies were appropriate, and whether distribution processes complied with regulations, resulting in penalties for a number of non-compliant pharmacies. The pressure for compliance surged, leading to the first year-on-year decline in the number of pharmacies that year. In 2018, the number suddenly increased, likely due to overheated transactions in tier-1 markets in the preceding two years, which spurred small and medium-sized pharmacy chains to aggressively open new stores. At this point, the number of pharmacies had nearly reached saturation.

Guangdong Province has the largest number of pharmacies in China. In 2018, the number of pharmacies in Guangdong reached 54,000, which was 18,000 more than that in Shandong Province, the second-ranked province. The number of pharmacies is influenced not only by population size but also by economic conditions, healthcare-seeking behaviors, and policies. Generally, residents in economically developed areas are more likely to have employee basic medical insurance and tend to visit hospitals directly when ill, whereas patients with lower reimbursement rates under schemes such as the New Rural Cooperative Medical Scheme are more inclined to purchase medications at pharmacies. As China’s most populous province with a large influx of migrant workers, Guangdong has a significantly higher number of pharmacies than other provinces. In contrast, Beijing and Shanghai have fewer pharmacies due to regulatory restrictions on the minimum distance between pharmacy locations.

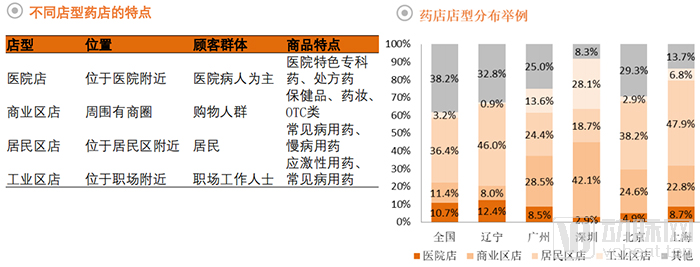

Analysis of Pharmacy Locations: A High Proportion of Pharmacies Are Located in Residential Areas

Data Source: First Pharmacy Financial Intelligence, Ping An Securities Research Institute

The location of a pharmacy determines its customer traffic and plays a pivotal role in sales. Based on location, pharmacies can be categorized into hospital-based pharmacies, commercial district pharmacies, residential area pharmacies, and industrial zone pharmacies.

Hospital-affiliated stores are currently the most popular store format. Leveraging their proximity to hospitals, these stores benefit from stable customer traffic and are well-positioned to capitalize on the ongoing trend of prescription outflow, yielding significant advantages. Major medium-to-large chain pharmacies are aggressively expanding their presence in this segment.

Meanwhile, stores in commercial and residential areas have also experienced rapid growth. As China’s urbanization rate has risen, many new residential communities have been developed in recent years, leading to a corresponding increase in stores located in these areas. Stores in commercial districts have established themselves in newly built satellite cities and small-to-medium-sized central business districts (CBDs).

Nationwide, stores in residential areas account for the highest proportion at 36.4%, followed by those in commercial districts at 11.4% and hospital-based stores at 10.7%. Stores in industrial zones represent a smaller share, at only 3.2%.

The proportions of various store formats vary significantly across different regions, primarily driven by local industrial structures and demographic characteristics. For instance, in Shenzhen, an emerging hub for manufacturing and economic activity, the share of stores located in commercial and industrial zones is notably higher than in other regions.

Most Provinces’ Pharmacies Are Still Growing, with Significant Regional Variations in Competitive Landscapes

In most provinces, the number of pharmacies continues to grow, rising from 447,000 in 2016 to 489,000 in 2018.

The three provinces with the largest increase in number were: Liaoning (3,722 entities), Zhejiang (2,873 entities), and Henan (2,765 entities). The three provinces with the highest growth rates were: Guizhou (16.7%), Liaoning (16.5%), and Jiangxi (16.1%).

At the same time, however, the number of pharmacies has declined in provinces and municipalities including Xinjiang, Hubei, Sichuan, Chongqing, and Jilin.

The average number of people served per pharmacy can, to some extent, reflect the local competitive landscape. In China, each pharmacy serves an average of 2,850 people, which is close to the World Health Organization’s recommendation of 2,500 people per pharmacy.

Shanghai has the most favorable competitive landscape for pharmacies, with each pharmacy serving over 5,000 people on average. This is primarily due to Shanghai’s regulation imposing a minimum distance requirement between pharmacies, mandating that the road-network distance between any two pharmacies be no less than 300 meters. Similarly, Beijing enforces a minimum inter-pharmacy distance of 350 meters.

In populous provinces such as Guangdong and Shandong, the average number of people served per store ranges from 2,000 to 3,000, approaching the national average.

In provinces where the average number of customers served per store is below 2,000, Liaoning and Heilongjiang are old industrial bases that experienced early economic prosperity but now face severe population aging, resulting in a smaller customer base per store. Chongqing is home to two major pharmacy chains, Tongjungge and Heping Pharmacy, with a combined total of over 10,000 stores. This high density has spurred significant activity in the pharmaceutical retail sector, thereby reducing the average number of customers served per store.

Chain Enterprises Hold Significant Advantages as Pharmacy Chain Penetration Continues to Rise

Source: Ping An Securities Research Institute

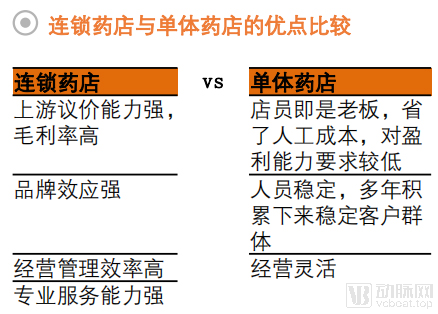

Chain pharmacies hold significant advantages over independent pharmacies, leading to a continuous increase in the pharmacy chain rate in recent years.

First is the cost advantage. Chain pharmacies benefit from large-scale upstream procurement and strong bargaining power, resulting in lower product costs compared to independent pharmacies. This advantage becomes more pronounced as the scale of the chain pharmacy increases.

Next is brand advantage. Chain pharmacies have a large number of stores, which can continuously reinforce their brand image in the minds of customers, and they possess stronger professional service capabilities. Therefore, chain pharmacies have stronger customer acquisition capabilities and significant brand advantages.

Data Source: Statistical Report on Pharmaceutical Operations and Distribution, Ping An Securities Research Institute

Data Source: Statistical Report on Pharmaceutical Operations and Distribution, Ping An Securities Research Institute

In the early years, regulatory oversight of China’s pharmacy sector was relatively lax, driving rapid industry growth. Currently, as the sector enters an era of stringent regulation, compliance costs for pharmacies have risen, making the competitive advantages of chain pharmacies more pronounced.

In 2018, among the 489,000 retail pharmacies, 255,000 were chain stores, resulting in a chain store penetration rate of 52%. From 2014 to 2018, the chain store penetration rate increased from 39.4% to 52.1%. In the medium to long term, the chain store penetration rate is expected to continue rising.

Data Source: Statistical Report on Pharmaceutical Operations and Circulation, Ping An Securities Research Institute

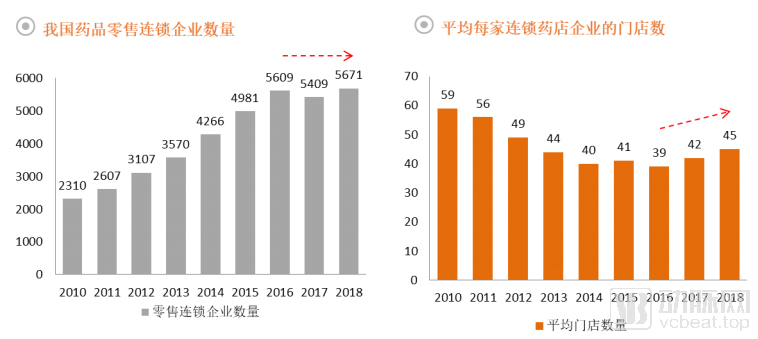

An increase in the chain affiliation rate signifies changes in the number of pharmaceutical retail chain enterprises. Prior to 2016, the number of such enterprises increased year by year, rising from 2,310 in 2010 to 5,609 in 2016. After 2016, driven by a surge in mergers and consolidations among chain operators, the total number of retail chain enterprises ceased to grow. By the end of 2018, there were 5,671 pharmaceutical retail chain enterprises in China, indicating that the number had stabilized.

In terms of the number of stores operated by retail chain enterprises, a large number of small chain enterprises emerged before 2016, reducing the average number of stores per enterprise from 59 in 2010 to 39 in 2016.

After 2016, the average number of stores per chain pharmacy enterprise bottomed out and rebounded. Unprecedented M&A activity in the industry greatly stimulated small chains’ enthusiasm for opening new stores, leading to an increase in the average number of stores per chain pharmacy enterprise.

In terms of regional differences, the chain pharmacy rates vary significantly across provinces. The highest rates are observed in Shanghai (89.7%), Hainan (74.7%), and Shandong (73.9%), while the lowest are in Tianjin (26.9%), Shaanxi (27.3%), and Xinjiang (32.1%).

Data Source: China Pharmacy, Ping An Securities Research Institute

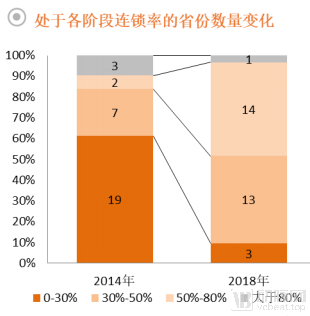

The number of provinces with chain store rates between 0% and 30% decreased from 19 in 2014 to 3 in 2018; the number of provinces with chain store rates between 30% and 50% increased from 7 in 2014 to 13; and the number of provinces with chain store rates between 50% and 80% rose from 2 in 2014 to 14. The increase in the number of provinces with moderate chain store rates has driven up the national chain store rate.

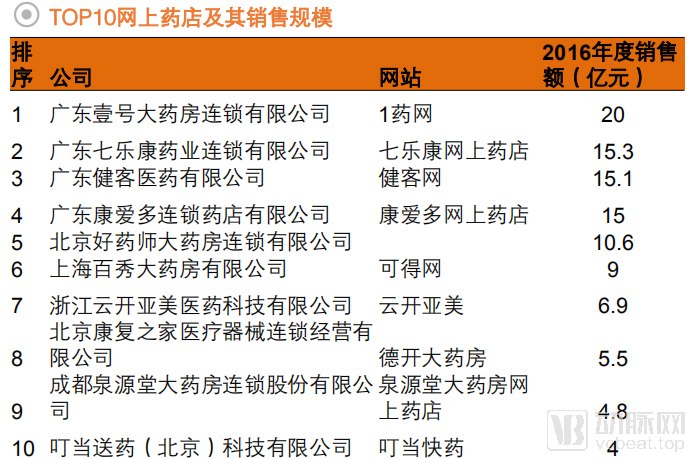

Online Pharmacies: A High-Growth Market Dominated by Giants

Sources: Menet, China Drugstore, Ping An Securities Research Institute

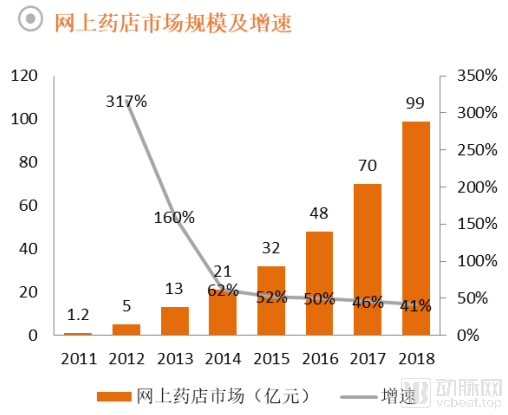

E-commerce has become an indispensable channel in the pharmaceutical retail industry. According to statistics from Menet, China’s online pharmacy market has experienced rapid growth in recent years, with its market size reaching RMB 9.9 billion in 2018, a year-on-year increase of 41%.

Guangdong Province’s relatively open policies and economic environment have fostered the growth of online pharmacies, with the top four online pharmacies in China all originating from Guangdong. The largest by volume, 1 Yao Wang (1 Drug Network), achieved sales of RMB 2 billion in 2016.

Data sources: Menet, China Drugstore, Ping An Securities Research Institute

The newly revised Drug Administration Law adopts an open stance toward the online sale of prescription drugs, stipulating that such sales are permitted provided they meet the same standards as offline channels. The National Healthcare Security Administration issued the Guiding Opinions on Improving Pricing and Medical Insurance Reimbursement Policies for “Internet+” Medical Services, explicitly clarifying that medical insurance can cover Internet+ medical services. Compared with the previous prohibition on the online sale of prescription drugs, this policy shift represents a significant relaxation that could shape the future of online pharmacies.

The Good Supply Practice for Pharmaceutical Products stipulates that “newly established pharmaceutical trading enterprises must be staffed with licensed pharmacists.” As pharmacies are classified as pharmaceutical trading enterprises, they are required to employ licensed pharmacists. However, due to the limited number of licensed pharmacists in China, it is not yet possible to fully comply with the staffing requirements set forth in the Good Supply Practice for Pharmaceutical Products.

Data source: Licensed Pharmacist Registration Platform, Ping An Securities Research Institute

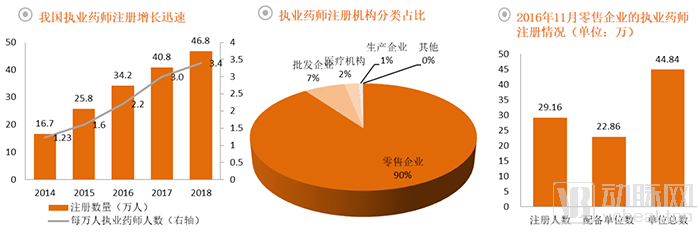

Rapid Growth in the Number of Licensed Pharmacists, Yet a Significant Shortfall Remains

In recent years, under national encouragement and policy guidance, the number of registered licensed pharmacists has grown rapidly, increasing from 167,000 in 2014 to 468,000 in 2018. The number of licensed pharmacists per 10,000 people also rose from 1.23 to 3.4; however, this figure still falls significantly short of the standard of 6.2 licensed pharmacists per 10,000 population published by the International Pharmaceutical Federation (FIP).

Among registered licensed pharmacists in China, 90% are registered with retail enterprises, making them the primary type of employer for licensed pharmacists. According to data from November 2016, the staffing rate of licensed pharmacists in retail pharmacies in China was only 51%, meaning that approximately half of all pharmacies lacked a licensed pharmacist.

Significant Disparities in the Number of Licensed Pharmacists Staffed at Pharmacies Across Provinces

In addition to a long-standing shortage in numbers, licensed pharmacists also face the issue of uneven distribution, with significant disparities in the number of registered licensed pharmacists across provinces. Guangdong Province has the largest number, with 58,000 licensed pharmacists, followed by Shandong Province (37,000) and Henan Province (31,000). The provinces with the fewest registered licensed pharmacists are Tibet (650), Qinghai (1,216), and Ningxia (2,593).

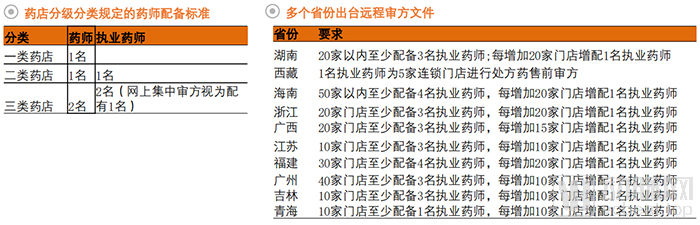

According to the “Guiding Opinions on the Classification and Graded Management of Retail Pharmacies Nationwide (Draft for Comments)” released by the Ministry of Commerce in November 2018, Class II pharmacies are required to have at least one licensed pharmacist, while Class III pharmacies must have at least two. The current number of licensed pharmacists in China is insufficient to meet demand, with an average of 0.93 registered licensed pharmacists per pharmacy nationwide.

Meanwhile, there is a significant disparity in the staffing of licensed pharmacists across pharmacies in different regions. Only Shanghai and Tibet have an average of more than 1.5 registered licensed pharmacists per pharmacy. Guangdong Province, which has the largest number of pharmacies, is slightly above the national average. The two provinces with the lowest staffing rates are Yunnan and Guizhou, where the average number of registered licensed pharmacists per pharmacy is less than 0.5.

Remote Prescription Review Helps Address the Shortage of Licensed Pharmacists

In accordance with the “Guiding Opinions on the Classified and Graded Management of Retail Pharmacies Nationwide (Draft for Comments)” released by the Ministry of Commerce in November 2018, retail pharmacies are categorized into Class I, Class II, and Class III stores. Class II stores are required to have at least one licensed pharmacist on staff, while Class III stores must have at least two licensed pharmacists. Centralized online prescription review is considered equivalent to having one licensed pharmacist on staff.

Data sources: Guiding Opinions on the Classified and Graded Management of Retail Pharmacies Nationwide (Draft for Comments), official websites of provincial medical products administrations, Ping An Securities Research Institute

Assuming that Class I, Class II, and Class III pharmacies in China account for 20%, 30%, and 50% of the total, respectively, a total of 640,000 licensed pharmacists would be required. Currently, however, there are only approximately 440,000 licensed pharmacists registered at pharmacies in China, resulting in a shortfall of 200,000 licensed pharmacists.

To address the shortage of licensed pharmacists, many provinces have proposed remote prescription review as a solution. Currently, approximately half of the provinces across China have issued documents outlining specific implementation guidelines for remote prescription review. This approach will effectively mitigate the shortage of licensed pharmacists.

Leading companies in the pharmaceutical retail industry each have their own characteristics, with some focusing on the national market and others concentrating on specific regions.

Guoda Pharmacy and Laobaixing operate stores in more than 15 provinces across China, making them nationwide chain pharmacies. Furthermore, driven by capital investment, Gaoji Medical has risen from nothing to become the largest chain pharmacy in China within just two years, with its sales volume expected to exceed RMB 20 billion.

According to data from Wind and Ping An Securities Research Institute, the regions covered by Guoda Drugstore include Guangxi, Guangdong, Hunan, Fujian, Zhejiang, Shanghai, Anhui, Jiangsu, Henan, Shanxi, Shandong, Hebei, Tianjin, Beijing, Liaoning, Inner Mongolia, Ningxia, and Xinjiang, with a total of 4,275 pharmacies.

The regions covered by Laobaixing Pharmacy include Guangxi, Guangdong, Hunan, Jiangxi, Zhejiang, Hubei, Anhui, Shanghai, Shaanxi, Tianjin, Beijing, Hebei, Henan, Shandong, Jiangsu, Gansu, and Inner Mongolia, with a total of 3,289 pharmacies.

Furthermore, driven by capital, Gaoji Medical has grown from scratch to become the largest chain pharmacy in China within just two years, with its sales volume expected to exceed RMB 20 billion.

Yixintang, Dashenlin, and Yifeng Pharmacy have their respective strongholds in Southwest China, South China, and Central and East China.

According to data from Wind and Ping An Securities Research Institute, Yixintang’s operational regions include Tianjin, Shanghai, Shanxi, Sichuan, Chongqing, Yunnan, Guizhou, Guangxi, and Hainan, with a total of 5,758 pharmacies.

Dasenlin’s operational regions include Henan, Guangxi, Guangdong, Jiangxi, Fujian, and Zhejiang, with a total of 3,880 pharmacies.

Yifeng Pharmacy’s operational regions include Hubei, Hunan, Jiangxi, Guangdong, Jiangsu, Shanghai, and Zhejiang, with a total of 3,611 pharmacies.

As industry concentration increases, large national and regional pharmaceutical retail chains are gradually taking shape, leading to increasingly fierce competition among retailers. Meanwhile, market competition is further intensified by the continuous improvement of medication standards in primary healthcare institutions, the implementation of national centralized drug procurement policies, rising operational costs for pharmaceutical retailers, and the gradual formation of a consumer base that primarily shops via the internet and mobile devices.

Meanwhile, as the new healthcare reform deepens, a series of policies—including comprehensive public hospital reform, zero-markup drug pricing, the two-invoice system, and reforms to health insurance payment methods—have been rolled out, leading to increasingly stringent industry regulation. Given the broad scope of the new healthcare reform policy framework, its implementation must address various complex situations and may be adjusted based on actual conditions; consequently, certain uncertainties remain within the industry.