Analyzing the Four Core Competitive Advantages of New-Generation Pediatric Chain Clinics: Leading Brands Expand into Home-Based Family Healthcare Services

Recently, Probe Capital released the report "New-Style Pediatric Chain Clinics," authorized for publication by VCBeat. Through its analysis of the pediatric healthcare services market, interpretation of policies on socially operated medical institutions, and examination of development trends in pediatric healthcare services, the report provides insights into the competitiveness model and future direction of new-style pediatric clinics.

Key Highlights of the Report:

1. Respiratory diseases remain a major cause of illness in pediatrics. Etiological studies have shown that viral infections account for a significant proportion of acute respiratory tract infections in children in China, particularly upper respiratory tract infections;

2. On the demand side, demographic structure, the two-child policy, and shifting social awareness have driven robust demand for pediatric medical services; on the supply side, pediatric care is predominantly provided by the public healthcare system, with a severe shortage of pediatricians; on the payment side, out-of-pocket payments dominate pediatric healthcare expenditures, creating opportunities for the development of private medical service institutions;

3. Pediatric clinics in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, as well as in emerging first-tier cities including Chongqing, Hangzhou, Wuhan, Kunming, Nanjing, and Changsha, are undoubtedly key areas of interest for capital investors; most pediatric medical institutions that have secured financing are located in these regions. Compared with first-tier cities, central cities with large population bases and conservative fertility attitudes—such as those in the Sichuan-Chongqing region, Wuhan, and Zhengzhou—but characterized by rapid economic growth, relaxed household registration (hukou) policies, and strong middle-class consumption power, may also see the emergence of large-scale pediatric chain medical institutions requiring lower investment and achieving break-even in a shorter period.

4. Development Logic of Pediatric Clinics: Leveraging common pediatric diseases and child healthcare as entry points to horizontally expand into high-margin, high-retention pediatric specialty services, while vertically extending into family medical services.

Below is an excerpt from the report:

Pediatric Disease Types: Respiratory Diseases Remain the Leading Pediatric Conditions

Based on incidence rates, pediatric clinical diseases can be broadly categorized into common diseases, specialized diseases, and rare diseases. Common pediatric diseases are predominantly respiratory disorders. Specialized diseases include conditions within pediatric dentistry, pediatric ophthalmology, pediatric endocrinology (e.g., growth and development), pediatric otorhinolaryngology, and pediatric rehabilitation. Rare diseases include albinism, galactosemia, hemophilia, dwarfism syndromes, and retinoblastoma.

Child health care is an interdisciplinary field at the intersection of pediatrics and preventive medicine. Its primary mission is to study the patterns of growth and development across various pediatric age groups, as well as their influencing factors, so as to promote favorable conditions and mitigate adverse ones through effective interventions. Service offerings include monitoring children’s physical growth and psychosocial development, pediatric nutrition, health promotion, and the prevention and management of pediatric diseases.

Children's Hospital of Fudan University conducted a study on outpatient visit data from its hospital information system between 2009 and 2018, revealing that the spectrum of diseases among pediatric patients was predominantly composed of common illnesses, with an upward trend in specialized conditions.

Respiratory, digestive, and neurological diseases remain the most common conditions treated in internal medicine outpatient clinics. Endocrine disorders, such as precocious puberty and short stature, are showing an upward trend. Patients with these conditions are typically of preschool or adolescent age and require multiple visits. Furthermore, due to enhanced public health education and increased parental awareness of precocious puberty and short stature, the number of outpatient visits for these conditions has risen significantly.

Among pediatric surgical conditions, trauma and fractures remain the most prevalent, followed by pediatric tumors, inguinal hernia, congenital heart disease, and anorectal disorders as common surgical diseases.

Ranking of Outpatient Visits for Internal Medicine Conditions

Ranking of Surgical Disease Consultation Volume

Ranking of Surgical Disease Consultation Volume

Source: “Trend Analysis of Characteristics and Medical Services in a Single-Center Pediatric Outpatient Clinic in Shanghai from 2009 to 2018”

Based on a comprehensive review of survey data from various hospitals across different regions, respiratory diseases remain the predominant conditions in pediatrics. Etiological studies indicate that viral infections account for a significant proportion of acute respiratory tract infections in children in China, particularly in cases of upper respiratory tract infections.

Pediatric Medical Services Market: Dominated by the Public System, with a Severe Shortage of Pediatricians

According to Frost & Sullivan’s forecasts, the mid-to-high-end segment of the private pediatric healthcare market has demonstrated particularly robust growth. From 2001 to 2014, the mid-to-high-end segment of China’s private pediatric healthcare market grew at a compound annual growth rate (CAGR) of 20.5%, while the low-end segment recorded a CAGR of 15.3% during the same period. From 2014 to 2020, the CAGRs for the mid-to-high-end and low-end segments of China’s private pediatric healthcare market are estimated at 24.2% and 16.4%, respectively.

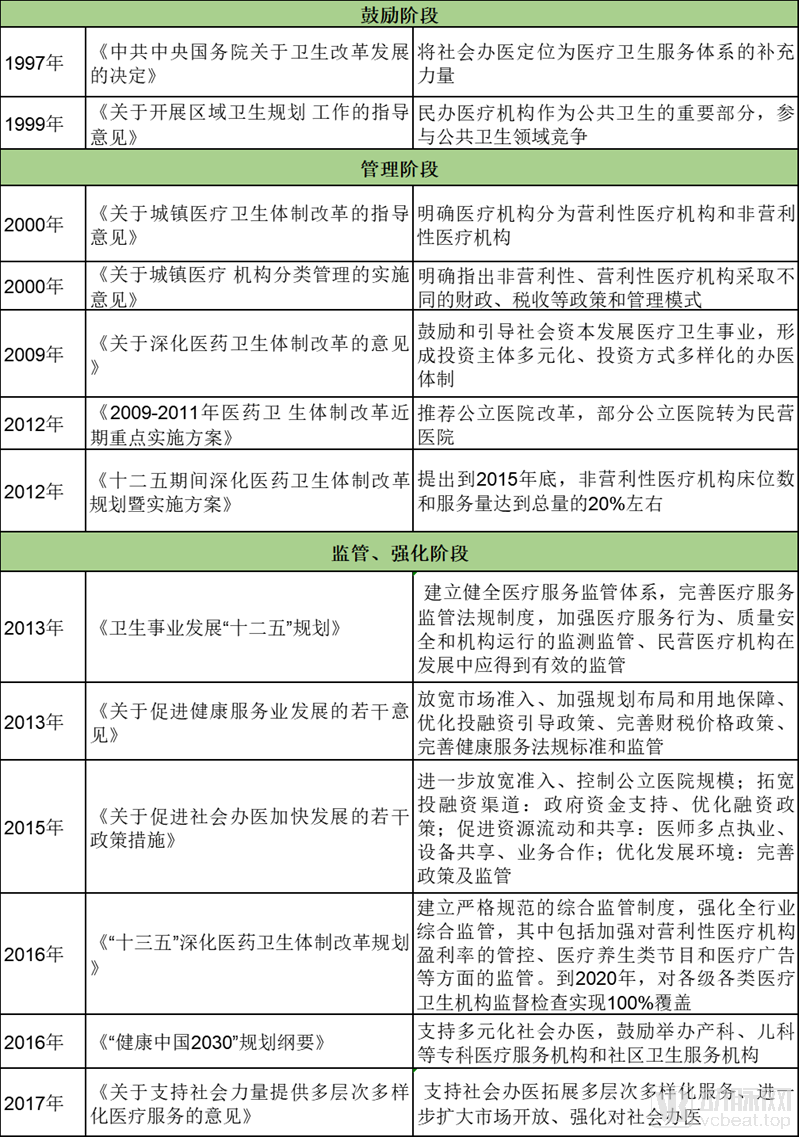

Favorable Policies for Socially-Operated Healthcare Drive Continued Expansion of the Private Pediatric Medical Industry. Over the past three decades, China’s policies promoting socially-operated healthcare have evolved significantly, with regulatory and supervisory mechanisms gradually maturing. This has laid a solid foundation for the development of private pediatric medical service institutions. Key measures include encouraging social capital to establish specialized pediatric medical institutions, promoting multi-site practice for physicians to enhance mobility and alleviate the shortage of medical professionals in private pediatric facilities, and fostering the training of pediatric talent.

Relevant regulatory and supervisory mechanisms are also gradually maturing.

Currently, medical institutions providing pediatric healthcare services are primarily public hospitals (general hospitals, specialized hospitals, and maternal and child health hospitals), private hospitals (mainly specialized hospitals), and community clinics (predominantly pediatric clinics). Among these, the market for pediatric healthcare services is showing an expansion trend.

On the demand side, demographic structure, the two-child policy, and shifts in social awareness have driven strong demand for pediatric medical services.

From 2008 to 2014, the number of pediatric outpatient and emergency visits increased from 275 million to 465 million, representing a compound annual growth rate (CAGR) of 9.1%. With the rapid increase in newborns, the CAGR for pediatrics is expected to rise further. Following the implementation of the universal two-child policy, the CAGR for pediatric outpatient and emergency visits is conservatively estimated at 12.15%. In 2017, the number of pediatric outpatient and emergency visits was approximately 542 million, and it is projected to reach 670 million by 2019.

There are three primary drivers behind the rise in per capita pediatric healthcare expenditure: the sustained growth in per capita disposable income, the persistently high proportion of healthcare spending within household budgets, and the growing popularity of intensive parenting practices.

With the development of China's economy, per capita disposable income in China has also been growing rapidly. Compared with 2011, it increased by 50% in 2015, with a compound annual growth rate (CAGR) of 10.8%. Although the growth rate has slowed down since 2013, it remains on a steady upward trend, providing a guarantee for pediatric healthcare expenditure.

On the supply side, pediatric medical services are predominantly provided by the public healthcare system, and there is a severe shortage of pediatricians.

In China, the medical institutions currently providing pediatric care are primarily public hospitals (including pediatrics departments in general hospitals, specialized hospitals, and maternal and child health hospitals), private hospitals (mainly specialized hospitals), and emerging pediatric clinics. These different types of pediatric medical institutions have distinctly differentiated positioning and characteristics.

China’s public pediatric healthcare system remains the primary provider of children’s medical services, accounting for nearly 90% of all outpatient and emergency visits nationwide. According to the Health Statistics Yearbook, the number of pediatric consultations in general hospitals reached nearly 220 million in 2016, while admissions to specialized hospitals (including both public and private institutions, predominantly public) totaled 1.7804 million in the same year, with consultation volumes showing a slow upward trend. Notably, these figures and their growth rates were achieved against the backdrop of a slowing growth rate in newborn births; following the implementation of the two-child policy, there was a significant increase in the number of pediatric consultations.

With the increasing number of pediatric patients, there is a shortage in the supply of public pediatric medical services. In terms of the number of institutions in recent years, the overall quantity of maternal and child health hospitals has remained relatively stable; as specialized healthcare institutions providing maternal and child health services, their numbers have basically stabilized following policy implementation. The qualification review for general hospitals (Level II and Level III) is also stringent, resulting in a largely stable count. The number of specialized pediatric hospitals has grown from 60 in 2005 to 117, yet they still account for a small proportion and are predominantly publicly owned.

Number of Pediatric Medical Institutions (Public), Including Private Children’s Hospitals in the Count of Pediatric Hospitals Source: Wind

There are 118,000 licensed (assistant) pediatricians in medical institutions across China. The number of licensed (assistant) pediatricians per 1,000 children aged 0 to 14 is 0.53, compared to 1.46 in the United States. According to the White Paper on the Current Status of Pediatric Resources in China, there is currently a shortfall of 86,042 pediatricians in China relative to the target of achieving 0.69 licensed (assistant) pediatricians per 1,000 children by 2020. Currently, the number of pediatricians per 1,000 children is 0.57 in urban areas and 0.47 in rural areas.

The scarcity of pediatricians is partly due to the elimination of pediatrics as an undergraduate major in medical schools, replaced by a general clinical medicine program, with pediatrics becoming just one course within that curriculum. This change has led to reduced enrollment in pediatrics and a corresponding decline in supply. Additionally, pediatricians face significant constraints in their academic and career development. For instance, after pediatrics was removed from the national discipline catalog, pediatricians have had to compete with adult-care specialists for grants from the National Natural Science Foundation of China. A survey conducted by the Pediatric Branch of the Chinese Medical Doctor Association found that pediatricians’ average workload is 1.68 times that of non-pediatric physicians, yet their income amounts to only 76% of that earned by adult-care specialists.

The attrition of pediatricians is driven by two main factors. On one hand, the low volume of medication prescribed in pediatrics results in relatively low income despite a heavy workload, particularly in a healthcare system where revenue generation has not yet fully decoupled from pharmaceutical sales. On the other hand, communication in pediatrics is inherently complex; pediatricians frequently interact with multiple anxious family members of young patients, exacerbating the common challenges associated with doctor-patient communication.

On the payment side, pediatric medical care is primarily paid out-of-pocket, creating opportunities for the development of private healthcare service providers.

China’s medical insurance system has resulted in significant inadequacies in healthcare coverage for children. Basic pediatric medical care is subject to high deductibles, and certain services are excluded from reimbursement. Pediatric preventive care, a core component of child health services, is not covered by insurance. Furthermore, in some underdeveloped regions, pediatric outpatient and emergency services are also excluded from coverage. Generally, children enrolled in basic medical insurance are eligible for three types of benefits: outpatient and emergency care, hospitalization, and special outpatient diseases.

The basic medical security system provides insufficient coverage for children with critical illnesses, resulting in a severe "Matthew effect." Medical care for children with critical illnesses is characterized by a high proportion of cross-regional consultations, numerous out-of-pocket expenses, and significant gaps in post-diagnosis treatment.

Development of Private Pediatric Chain Service Institutions

Pediatric clinics, as representatives of primary healthcare for children, primarily provide general outpatient services and child health care, with most equipped with clinical laboratories. Some clinics offer specialized medical services, such as pediatric traditional Chinese medicine, family practice, lactation consultation, and adolescent gynecology. Pediatric medical institutions holding outpatient clinic licenses may be configured with day surgery units to perform minor outpatient and day-case surgical procedures.

Development History

In recent years, substantial social capital has flowed into the private pediatric healthcare sector. As early as 2013, Warburg Pincus and its partner institutions announced the completion of a $100 million investment in Amcare USA. In October 2014, Raybo Pediatrics opened its first clinic in Shanghai and subsequently completed its angel-round financing. WellNovo followed suit, also opening its first clinic in Shanghai in 2015. Since then, service-oriented pediatric chain clinics have successively emerged across major tier-1 and new tier-1 cities throughout China.

Not only in pediatric clinics, but also in the specialized fields of child developmental behavior and pediatric rehabilitation, Changhe Dayun holds the exclusive mainland China copyright agency for the Chinese version of the Griffiths Developmental Assessment Scales. Currently, it operates Beijing Changhe Dayun Pediatric Clinic and Shenzhen Changhe Dayun Pediatric Rehabilitation Outpatient Department, in addition to the acquired Shanghai Dayun Home Educational Institution.

Fan Xiaoqia, a pediatric massage brand, was established in 2014. Its first offline store opened in April 2016, and within a year and a half, it operated 15 directly-owned Fan Xiaoqia stores in the Beijing area.

New Century Healthcare is the first listed company in China with pediatric medical services as its core business. Its development offers a glimpse into the broader landscape of women’s and children’s healthcare services in China. Positioned in the high-end segment of pediatric and obstetric-gynecological care, New Century Healthcare currently operates three hospitals and two clinics in Beijing, as well as one women’s and children’s hospital each in Tianjin, Chengdu, Qingdao, and Suzhou.

According to the annual report, its business achieved steady growth in 2018, with revenue reaching RMB 616 million, a year-on-year increase of 14.8%; medical service income reached RMB 569 million, a year-on-year increase of 15.8%. Among these, the pediatric business generated revenue of RMB 466 million, a year-on-year increase of 13.0%; the obstetrics and gynecology business generated revenue of RMB 102 million, a year-on-year increase of 30.5%. The company achieved an EBITDA of RMB 151 million, a year-on-year decrease of 12.3%. Adjusted net profit was RMB 132 million, a year-on-year increase of 15.0%; adjusted EBITDA increased by 13.6% year-on-year. In 2018, the total number of outpatient visits at New Century Healthcare reached 231,786, a year-on-year increase of 15.5%. Among these, pediatric outpatient visits increased by 10.9% year-on-year from 178,618 in 2017 to 198,003. The number of inpatient visits was 9,730, a year-on-year increase of 15.4%.

Hospital investment is a capital-intensive industry, requiring substantial financial input for infrastructure, equipment, and personnel. According to the fundraising project disclosures by New Century Healthcare, significant capital expenditure and extended construction periods constitute barriers to entry in this sector.

After five years of development, the pediatric healthcare services industry has gradually exhibited regional characteristics, with leading players emerging. The following section will analyze and discuss the major mature business models and competitive advantages.

Competitive Advantage Analysis

First, site selection models and standardized design and renovation.Community-based healthcare institutions, which rely on a foundational patient flow, are heavily dependent in their early development on the maturity of site-selection models. Their understanding of local demographics, resource distribution, and even cultural norms and customs largely determines the success rate of regional expansion; hence, domestic chain healthcare providers in China predominantly exhibit a trend toward regionalization.

Pediatrics is no exception. Mature chain pediatric healthcare service providers can leverage local macroeconomic data and proprietary scoring models for new clinic site selection, while optimizing clinic design and renovation based on user feedback, thereby enhancing user experience and engagement.

Second, barriers to medical talent.Constrained by China’s physician training and healthcare management systems, high-quality medical talent remains predominantly within the public sector. However, private healthcare institutions offer more competitive compensation and greater professional autonomy, exerting a certain appeal to physicians employed in the public system. The rise of physician groups and independent physician practices serves as compelling evidence of this trend. In regions with favorable regulatory environments and advanced economic development, there have been numerous cases of pediatricians from tertiary Grade A hospitals establishing their own outpatient clinics.

For chain brands, offering reasonable physician incentive mechanisms, safeguards for practice environments, comprehensive career and academic advancement pathways, along with decent income and relatively autonomous work arrangements, holds certain appeal for experienced physicians with established reputations and influence. These physicians will constitute the core talent pool for clinics. Junior physicians, considering factors such as future professional development and title evaluations, tend to exhibit lower motivation in the early stages; however, as the industry matures, they can serve as a supplementary workforce, forming a structured talent pipeline.

Third, barriers in management systems.There are currently few professional medical institutions that adopt a chain operation model for pediatric clinics to achieve rapid expansion. The primary reason is that the insufficient management capabilities and operational experience of new entrants may be one of the main factors constraining their expansion.

As a business model that prioritizes service quality, pediatric chain clinics differ significantly from highly standardized, equipment-dependent medical service providers such as ophthalmology and dental clinics. Participants in this sector must develop management and operational models tailored to external market conditions by integrating their own managerial characteristics during practical development. New entrants cannot expect to achieve growth and expansion in the short term by simply replicating the management and operational models of other companies.

Fourth, brand barriers.Brand awareness is a crucial component of brand equity, serving as a metric for gauging consumers’ recognition and understanding of a brand’s connotations and value. Brand awareness reflects a company’s competitiveness and can sometimes constitute a core competitive advantage. This is particularly evident when parents are selecting medical services, where the brand’s intrinsic meaning, trustworthiness, and the associated community culture become paramount.

The primary clientele of pediatric clinic chains consist of children and their parents. These consumers possess innate, organic channels for social dissemination and tend to base their purchasing decisions on brand familiarity, trust, and cultural affinity. Cultivating such consumer loyalty requires time; once established, it is highly resistant to switching, posing a significant challenge for late entrants in the industry.

Business Model Analysis

First, the offline model for implementing internet-based healthcare

The healthcare industry is characterized by inefficiency, numerous pain points, significant growth potential, and a long-tail structure, which underscores the substantial value that the internet can bring to this sector. However, the inherent characteristics of the healthcare industry also make it difficult for the internet to disrupt it: public hospitals hold significant influence, and the closed nature of the state-run system conflicts with the openness of the internet; the healthcare industry is subject to multi-party regulation and strict administrative approvals; and since it involves life and health, the general public tends to be cautious, making trust mechanisms critically important.

China’s internet healthcare sector has evolved from mobile health to physician groups, and from appointment scheduling to lightweight online consultations. While multi-faceted attempts have been made in the online space, it remains challenging to ensure controllable medical quality and guaranteed patient safety through online consultations alone. Consequently, internet companies are increasingly targeting the offline segment—a critical closed loop in the service industry—by establishing offline clinics and leveraging online channels to drive patient traffic to these physical facilities. The pediatric sector is no exception.

Cui Yutao Yu Xue Yuan Pediatric Clinic: Cui Yutao Yu Xue Yuan Pediatric Clinic features the “Yu Xue Yuan” mobile app for online interaction and offline pediatric clinics, focusing on an O2O health and parenting management system that integrates online and offline services. The online platform includes a pediatric medical record management system, while the offline pediatric clinics primarily focus on child healthcare.

Mommy Knows Pediatric Clinic: Mommy Knows Pediatric Clinic operates the online maternal and child consultation platform “Mommy Knows,” the obstetrician-gynecologist and pediatrician physician group “Yixin Doctors,” and the offline pediatric outpatient center “Yixin Pediatrics.” It adopts an innovative online-plus-offline healthcare service model, leveraging online operations and SaaS solutions to establish offline clinics. Its services feature a significant volume of lightweight consultations and a popular science community. In addition to its self-built and self-operated model, the offline clinics also include a co-operated general practice clinic model.

Zhibei Medical: Zhibei enters the market through online consultations and paid WeChat courses, providing services such as daily family health management, parenting courses for parents, and health consultations via the internet, complemented by offline pediatric healthcare and specialized clinical services.

Second, centered on regionally renowned pediatricians: a clinic-plus-family-doctor model

In recent years, in regions with more open policies such as Beijing, Guangdong, and Shenzhen, there has been a surge in projects where doctors leave the public system to start their own practices, primarily focusing on pediatrics—a specialty marked by prominent doctor-patient conflicts and relatively low physician income. Most pediatricians who embark on entrepreneurial ventures adopt an asset-heavy model of building their own clinics, often providing family doctor services and collaborating with large hospitals to establish green channels for expedited referrals.

Clinics independently established by physicians typically operate under two models: the physician’s personal brand or a standardized chain brand. These clinics demand strong store-operational capabilities, derive their profitability primarily from consultation fees, and target middle-class families with sufficient paying capacity and a focus on the quality of medical services.

Ruibao Pediatrics, positioned in the mid-to-high-end pediatric healthcare market, was founded by renowned physicians in Shanghai. It adopts a service model that integrates offline clinics with digital solutions. By leveraging its physical clinics as the primary entry point and complementing them with the online platform “Q Ruibao,” it offers services such as appointment scheduling, electronic medical records, payment processing, and lightweight consultations. Its operational strategy prioritizes offline services.

Dr. Yu Pediatrics was founded by Dr. Wang Yu, Deputy Chief Physician of the Department of Pediatrics at the First Affiliated Hospital of Chongqing Third Military Medical University. The practice primarily operates through offline outpatient clinics, focusing on differentiated, specialty pediatric medical services across its locations, and adopts a family doctor model that integrates online and offline care.

Weier Nuo Pediatrics adopts the American family doctor service model, advocating a preventive healthcare philosophy that avoids overtreatment. It emphasizes offline clinic operations and comprehensive child health services, promoting an integrated “medical + educational” approach. By implementing an appointment-based system with limited daily patient volumes, it ensures extended consultation time between patients and physicians.

Third, the Family Service Model: A General Practice Outpatient Clinic Centered on and Driven by Specialized Services for Women and Children

Distinct HealthCare: Distinct HealthCare adopts a chain of general practice clinics model, configuring one medical center, one physical examination/day surgery center, N pediatric care centers, and one pediatric dental clinic in each city. The medical centers provide general practice medical services, with referrals to its affiliated specialized service institutions as needed. Distinct HealthCare’s GP clinic chain also offers family doctor services.

Fourth, the Pediatrician Group Model: The Physician Partnership System

The current bottleneck in the development of China’s pediatric sector lies in the scarcity of pediatricians. To address this, some pediatric clinics have adopted the physician group model, striving to maximize the utilization and value of existing medical professionals. These clinics often leverage idle consultation rooms in high-end hospitals to facilitate multi-site practice for contracted physicians. By building online communities of both doctors and patients, they deliver tangible healthcare services through offline physical entities.

Little Apple Pediatrics: An O2O platform centered around a physician group. Its online offerings include a pediatric light-consultation app, a WeChat-based lab report manager, and online private physicians. Offline, it has established regional physician group entities in Beijing, Shanghai, Guangzhou, and Hangzhou, leveraging underutilized consultation rooms in premium hospitals to enable contracted physicians to practice at multiple sites.

Competitive Landscape of Emerging Pediatric Clinics

Pediatric clinics in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, as well as in new first-tier cities including Chongqing, Hangzhou, Wuhan, Kunming, Nanjing, and Changsha, are undoubtedly the focal point of capital attention; most pediatric medical institutions that have secured financing are located in these regions. Compared with first-tier cities, central cities with large population bases, conservative fertility attitudes, yet rapid economic growth, relaxed household registration (hukou) policies, and strong middle-class consumption capacity—such as those in the Sichuan-Chongqing region, Wuhan, and Zhengzhou—may also give rise to large-scale pediatric healthcare chains requiring lower investment and achieving break-even in a shorter period.

Future Development Directions

The Development of Pediatric Clinics:Focusing on common pediatric conditions and child healthcare, we horizontally expand into high-margin, high-retention pediatric specialty services, while vertically extending into family medical services.

Private pediatric clinics are an inevitable outcome of the tiered diagnosis and treatment system and the trend toward decentralizing medical resources. However, revenue generated from basic patient volume is limited, with a clear ceiling. Therefore, while securing high-quality patient traffic, these clinics must develop productization and specialization capabilities to increase average spending per visit and consultation frequency, thereby fully unlocking the hidden value of patient flow.

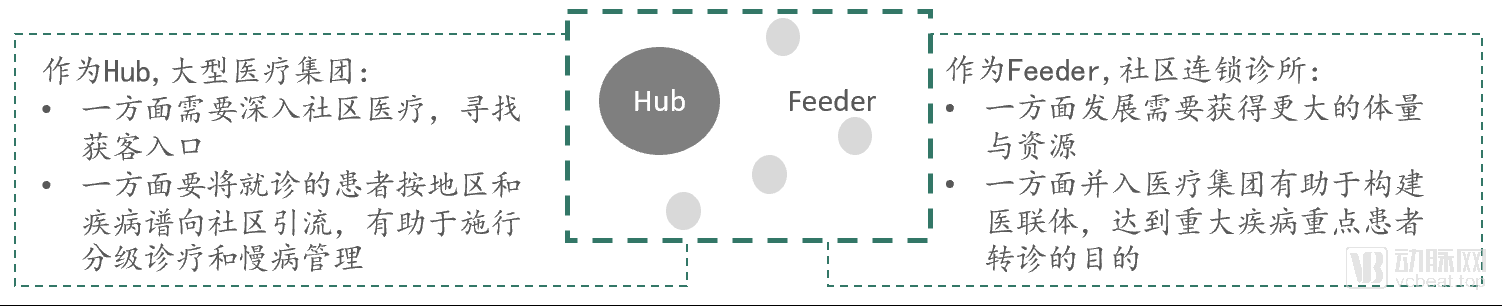

Capital Value of Pediatric Clinics:Consistent with the overarching logic of socially operated healthcare, community medical services serve as the entry point, integrating resources with medical groups to establish regional monopolies or market leadership.

Taking the renowned Singapore-based Parkway Healthcare Group as a case study, it operates dozens of hospitals, medical centers, clinics, imaging centers, and health screening centers in Singapore alone. Parkway manages Mount Elizabeth Hospital, Mount Elizabeth Novena Hospital, Gleneagles Hospital, and East Coast Medical Centre, all of which are JCI-accredited. Additionally, it operates 37 family or community clinics, nine imaging centers, and seven health screening centers. Through its hub-and-feeder model, its business scope encompasses clinic networks, health examination facilities, radiology equipment, laboratories, educational facilities, clinical research institutions, rehabilitation services, corporate insurance, and third-party administration (TPA). This has enabled Parkway to establish an integrated system spanning primary, secondary, tertiary, and quaternary care sectors in Singapore, achieving regional market dominance.

Socialized healthcare delivery has promoted the development of both chain specialty clinics and large medical groups. These two types of healthcare institutions are interconnected, with pediatric chain clinics serving as a component within the broader ecosystem of socialized healthcare. In the future, they will evolve toward a regional monopoly model based on the Hub-and-Feeder structure.