Heart Failure: The Final Frontier in Cardiovascular Disease Driving a Trillion-Yuan Market Opportunity

In 2018, the cardiovascular sector accounted for $87.1 billion in total financing, making it the highest-funded subsector within the medical device industry. (Data source: Silicon Valley Bank, Trends in Healthcare Investments and Exits 2019) Similarly, the cardiovascular sector has remained a popular focus for mergers and acquisitions in recent years.

It is evident that the cardiovascular device sector continues to be viewed favorably due to its immense potential.

This field has spawned numerous successful companies, particularly in the coronary stent and artificial heart valve markets, each of which boasts a global market size exceeding RMB 100 billion. These two segments currently represent the subsectors within high-end medical devices with the highest rates of domestic production in China.

Due to the rapid iteration of medical devices, companies in the industry continue to maintain high R&D investment to enhance product competitiveness. Once established players have built substantial competitive moats, it becomes significantly difficult for new entrants to break into the market.

So, which sub-sector will drive the growth of the cardiovascular market in the next phase? Judging from the active frontier technologies and corporate strategic directions in recent years, the heart failure market is highly likely to give rise to multiple tracks valued at tens or even hundreds of billions of yuan, thereby fueling the next round of growth in the cardiovascular market.

Academician Ge Junbo, Chairman of the Chinese Society of Cardiology and President of the China Cardiovascular Health Alliance, commented that heart failure is known as the “final battlefield” in the treatment of heart disease. He noted that although humanity has made significant progress in the treatment of most cardiac conditions, heart failure (HF) remains an exception, as its prevalence continues to rise and survival has improved only marginally.

Why is heart failure treatment considered the final battlefield in cardiovascular medicine? And how much incremental market space will heart failure bring?This article will analyze the existing pain points in the heart failure market from the perspectives of pathogenesis, diagnosis, and treatment, and outline potential solutions.

# Why Heart Failure Is Poised to Become the Largest Cardiovascular Market After Coronary Artery and Valvular DiseasesFirst, we need to clarify what heart failure is. Heart failure is a condition characterized by impaired cardiac pumping function, which leads to slowed blood flow, venous and pulmonary congestion, and other manifestations of declining cardiac function.

If we imagine the heart as a mechanical pump, it continuously pumps blood to supply nutrients to tissues and organs throughout the body. When the function of this “pump” is impaired due to various reasons—specifically, when cardiac systolic function declines—the heart fails to draw venous blood back into its chambers and is also unable to effectively pump blood out from the heart.

From an etiological perspective, many cardiac diseases and chronic conditions can lead to heart failure; these include arrhythmias, hypertension, pulmonary diseases, and autoimmune disorders.

From the clinical manifestations of heart failure, patient symptoms mainly present as dyspnea, fatigue, and fluid retention.

The heart failure market has a large patient population and will continue to grow.

In 2018, there were 10 million heart failure patients in China. Worldwide, approximately 23 million people suffer from heart failure.

It is more common in the elderly, and nearly all cardiovascular diseases eventually lead to heart failure. Improvements in medical care have extended the survival of patients with chronic conditions such as heart disease, diabetes, and obesity, while China’s accelerating population aging has rapidly expanded the at-risk population for heart failure.

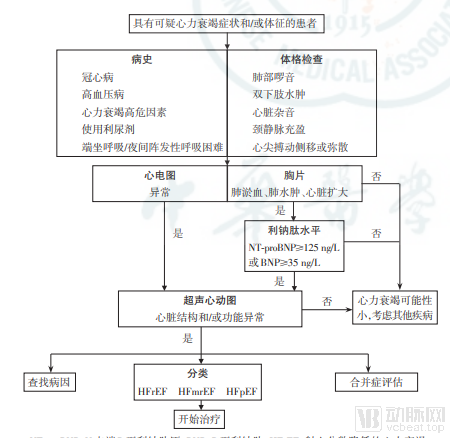

Although the causes of heart failure are diverse, its diagnosis is not difficult.

Physicians typically suspect heart failure based on signs observed during the physical examination, such as a weak and rapid pulse, abnormal heart sounds, pulmonary edema (including findings on auscultation), distended jugular veins, and lower extremity edema.

For precise diagnosis, chest X-rays can reveal an enlarged heart and pulmonary edema. Electrocardiography (ECG) determines whether the cardiac rhythm is normal. Echocardiography uses sound waves to generate images of the heart and is one of the best methods for evaluating cardiac function, including pumping capacity and valvular function. Other modalities, such as radionuclide imaging, magnetic resonance imaging (MRI), computed tomography (CT), and cardiac catheterization with angiography, can be used to identify the underlying causes of heart failure. In addition to imaging studies, blood tests are required to measure B-type natriuretic peptide (BNP). BNP is a substance secreted by cardiomyocytes in response to stretch stimulation and can be used for the diagnosis and prognostic assessment of heart failure.

These diagnostic devices and methods are readily available in hospitals, with low diagnostic costs.

Diagnostic Algorithm for Chronic Heart Failure. Image source: "2018 Chinese Guidelines for the Diagnosis and Treatment of Heart Failure"

From a therapeutic perspective, physicians often focus on treating the underlying causes of heart failure, modifying lifestyle factors, and managing heart failure through pharmacotherapy, surgery, or other interventions.

Congestive heart failure is primarily caused by impaired cardiac systolic function; once it occurs, the priority should be to actively identify the underlying causes and implement etiology-specific treatment.

Secondly, efforts should be made to reduce cardiac load as much as possible, including rest, a low-salt diet, appropriate use of sedatives, and activity restriction. For patients with severe heart failure, a strict low-salt diet and fluid intake control are adopted to alleviate fluid retention. Meanwhile, medications should be administered based on the principle of “enhancing myocardial contractility, promoting diuresis, and vasodilation.” For example, diuretics help the kidneys excrete salt and water by increasing urine output and reducing blood volume; ACE inhibitors and angiotensin II receptor blockers can dilate blood vessels and promote renal excretion of excess water; aldosterone antagonists directly block the effects of aldosterone, helping to inhibit fluid retention and thereby reducing cardiac load; digoxin can increase myocardial contractility, slow down an excessively rapid heart rate, and alleviate symptoms in patients with systolic dysfunction, among other benefits.

Based on the above description, it is not difficult to find that,The efficacy of heart failure medications is limited to the symptomatic relief level.As a chronic degenerative disease, heart failure cannot be completely cured.

Among the treatment options for advanced heart failure, heart transplantation is currently recognized as the only effective intervention for patients with end-stage heart failure. However, the severe shortage of donor hearts has significantly limited the availability of this procedure, thereby spurring the emergence of several players in the artificial heart sector, such as Thoratec (a subsidiary of Abbott), Medtronic, and Tongxin Medical.

Although the etiologies and treatment strategies for heart failure are well established, the five-year mortality rate among patients with all types of heart failure remains as high as 30–70% despite intensive therapy with current pharmacological and device-based interventions.

Therefore, heart failure is also known as the final battlefield in the field of cardiovascular medicine.

Unlike many other diseases, where high mortality rates are attributed to unclear pathogenesis and low diagnostic rates, the diagnosis and treatment of heart failure are well established. Nevertheless, mortality and readmission rates for heart failure remain persistently high.

The reason is that after diagnosis, patients cannot return to normal life even with treatment; they constantly oscillate between stable disease and acute exacerbations of instability.Precisely because of the risk of acute exacerbations, patients require repeated hospitalizations. With each exacerbation necessitating admission, myocardial damage worsens, life expectancy is correspondingly reduced, and mortality rates remain high.

As the condition progresses, the heart becomes increasingly weakened, treatment becomes more complex, and heart failure enters its terminal stage, where traditional cardiac therapies and symptom management strategies are no longer effective. The only remaining options are heart transplantation or the use of an artificial heart.

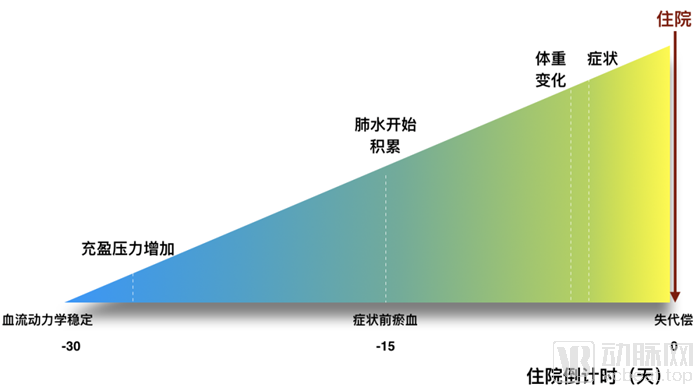

Rome Was Not Built in a Day: Prior to each acute exacerbation of heart failure, the heart releases numerous signals. Changes in filling pressure occur first, leading to cardiac dilation. Under the influence of a vicious cycle, pulmonary edema begins to develop; as fluid gradually accumulates in the lungs, patients become aware of overt symptoms. However, in the early stages of deterioration, the heart lacks nervous system feedback to perceive the decline. Patients typically only recognize the problem when pronounced symptoms such as dyspnea and weakness manifest. By this time, however, the heart has often been deteriorating for several tens of days and has sustained severe damage, necessitating emergency hospital care. This delay contributes to high rates of hospitalization and mortality.

High rates of readmission and mortality impose a substantial economic burden. In the United States, annual healthcare expenditures for this condition exceed $31 billion, with more than half attributed to hospitalization costs. Data show that heart failure patients in China are hospitalized an average of 2.4 times per year, with an average annual length of stay of 22 days. The average annual medical cost per patient is nearly RMB 29,000, which exceeds China’s annual per capita disposable income.

Heart transplantation can offer new hope to patients with end-stage heart failure. However, in the United States, where private insurance systems are relatively well-developed, the average cost of implanting an Abbott LVAD exceeds $170,000, while pump replacement costs approximately $90,000. This financial burden is unaffordable for most patients.

To reduce mortality and readmission rates in heart failure management, in addition to artificial heart replacement at advanced stages, heart failure can be managed after diagnosis to prevent disease progression and extend patient survival.

Because cardiac muscle lacks sensory innervation, patients only become aware of the condition when symptoms worsen.As shown in the figure above, if patients lack heart failure management warning devices, by the time they self-perceive worsening symptoms, the optimal window for medication adjustment has already been missed. The interval from the onset of physiological deterioration to the emergence of clinical symptoms is only 20 to 30 days. When patients become aware of the deterioration, it has already persisted for too long, causing irreversible damage and necessitating hospitalization for treatment or even emergency resuscitation.

Statistics show that approximately 20% of heart failure patients die within one year of diagnosis, and about 50% die within five years, with survival rates lower than those for many types of cancer.

In other words, for most patients who have not yet reached the late stage, the primary challenge in heart failure is not the initial diagnosis, but rather the management of recurrent deterioration after diagnosis.

Given the significant unmet needs in heart failure management, numerous physicians and companies have attempted over the past few decades to address early warning and management through various methods and parameters. In 1995, Dr. Rich published an article on managing heart failure patients via telephone follow-up, igniting enthusiasm for remote patient management. Despite extensive involvement from many healthcare institutions and enterprises, no highly effective solution has yet emerged.

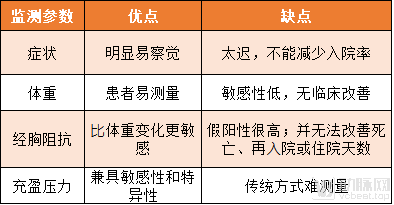

Core parameters monitored in heart failure follow-up management include symptoms, body weight, transthoracic impedance, and filling pressures.

Symptoms are the easiest to assess. As heart failure worsens, patients develop edema, fatigue, poor sleep quality, and increased nocturnal urination. However, by the time symptoms appear, irreversible damage has already occurred. Monitoring symptoms is often too late to reduce hospital admissions.

In the early stages, the monitoring parameter for remote physician follow-up was body weight. While this metric is easy for patients to measure, it has low sensitivity. In a 2005 trial publication, Lewin stated that this method had a sensitivity of less than 20%, and that remote monitoring of body weight did not reduce readmissions or mortality.

Another monitoring parameter commonly used in recent years is transthoracic impedance measured by implanted devices, which is used to assess pulmonary fluid and is more sensitive than changes in body weight. However, false-positive rates remain high in the Medtronic SENSE-HF and Abbott DEFEAT-PE clinical trials, and in the Medtronic DOT-HF trial, it even led to an increased rate of heart failure hospitalizations.

In past clinical practice, some remote follow-up results have shown improvements in hospitalization rates and mortality, while others have not, making the findings difficult to replicate. Nevertheless, enthusiasm within the industry remains undiminished, with institutions and enterprises continuously experimenting with different combination strategies. For instance, in 2011, the Veterans Administration spent $1.38 billion on remote management for patients with heart failure and hypertension; in 2013, Medtronic acquired Cardiocomm Solutions, a remote patient management company, and subsequently launched multiple remote patient management platform services (for heart failure).

Overall, monitoring and management based on the aforementioned traditional indicators provide warnings that are both too late and unreliable, and clinical trials have failed to demonstrate a reduction in hospitalizations. Consequently, they cannot yet serve as accurate indicators for heart failure management. The most advanced and authoritative indicator currently recognized by industry experts is cardiac filling pressure, which offers both sensitivity and specificity.

Filling pressures primarily consist of left atrial pressure and pulmonary artery pressure. Due to their early predictive capability and high accuracy, cardiac filling pressures have been widely recognized in recent years as the earliest and most accurate real-time indicators of worsening heart failure.

Approximately 90% of patients hospitalized for heart failure present with pulmonary congestion associated with elevated left atrial pressure (LAP). An increase in left atrial pressure is the earliest indicator of impending heart failure exacerbation, occurring well before the onset of clinical symptoms.

Following the onset of heart failure, decompensation directly leads to an increase in cardiac filling pressure (left atrial pressure, LAP), which subsequently causes an elevation in pulmonary artery pressure (PAP). This results in pulmonary capillary exudation, and cardiac function gradually transitions from a compensated to a decompensated state, manifesting as significant symptoms and signs.

In this process, elevated pressure is an early indicator of decompensated heart failure, and this indicator is not subject to many confounding factors.

By monitoring cardiac filling pressures, prompt medication adjustments upon detection of elevated pressures can interrupt the vicious cycle, preventing irreversible cardiac damage as well as increased hospitalization and mortality rates.

In the heart failure monitoring market, leading players have abandoned symptom-based diagnostic technologies and are instead focusing on solutions centered around left atrial pressure or pulmonary artery pressure monitoring. In the heart failure management market, multiple industry giants have established their presence, while emerging startups with innovative technological solutions are also making their debut.

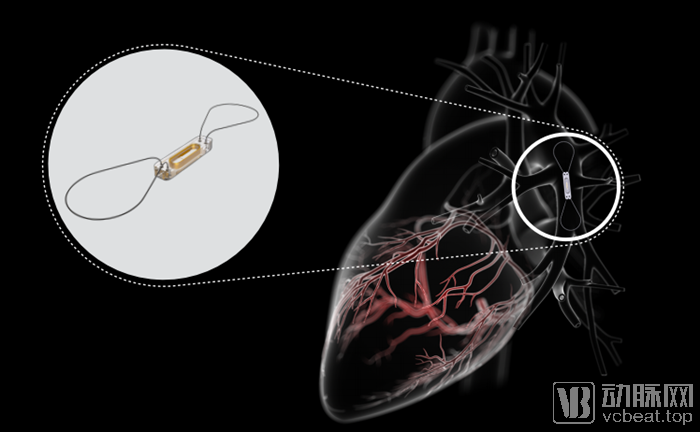

The first to be introduced isAbbott's CardioMEMS Heart Failure System, this is the world’s first and currently only FDA-approved system capable of significantly reducing hospitalization rates and improving quality of life for patients with NYHA Class III heart failure. CardioMEMS involves implanting a device in the pulmonary artery to monitor pulmonary hypertension signals and transmit them to healthcare providers; physicians then guide patients in adjusting their medications based on these data to achieve heart failure management. The CHAMPION clinical trial results demonstrated a 37% reduction in 30-day heart failure-related readmissions and a 58% reduction in all-cause readmissions, while also enabling pulmonary artery pressures to be maintained within target ranges.

Schematic Diagram of the CardioMEMS Pulmonary Artery Pressure Sensor and Its Implantation Site

Endotronix’s SolutionMuch like Abbott’s CardioMEMS approach, the Cordella sensor is implanted into the heart via a catheter, with an external signal receiver that enhances interactive convenience. Patients can monitor parameter changes through the system’s built-in tablet app, while physicians can timely assess patients’ disease status and interact with them via the software platform. Endotronix has raised over $100 million in funding; VCBeat recently reported that the company completed an extended Series D financing round to support FDA-regulated clinical trials for its sensor hardware and the commercialization of its software platform.

Endotronix Products

The second key point to highlight isBoston Scientific's HeartLogic AlgorithmThis is a heart failure management feature available on Boston Scientific’s latest implantable cardioverter-defibrillator, the Resonate ICD/CRT-D. During early research, the R&D team made a significant discovery that changes in heart sounds are highly correlated with the worsening of heart failure. By collecting and processing data from 500 individuals using multiple sensors integrated into the device, they developed an algorithm centered on heart sounds as the core parameter, supplemented by other heart failure-related parameters including heart rate, respiration, transthoracic impedance, and activity level. This algorithm integrates these inputs to output a composite index closely related to left atrial pressure, which indicates the progression of heart failure deterioration. The validity of this algorithm was further validated in a clinical trial involving 400 enrolled patients. The results demonstrated a sensitivity of 70% for predicting acute heart failure decompensation, with a false alarm rate of 1.4 per person per year, and the ability to provide warnings up to 34 days in advance of acute heart failure decompensation events. Based on these clinical outcomes, the product has received FDA approval; however, access to the HeartLogic feature requires patients to have this specific cardiac defibrillator implanted.

HeartLogic was also recently nominated for the 2019 “Best Medical Technology” award by the Galien Awards Committee in the United States.The Prix Galien Award is widely recognized as the highest honor in the pharmaceutical and biomedical industries, aimed at recognizing outstanding contributions to medical and scientific research and innovation, and is hailed as the “Nobel Prize of the pharmaceutical industry.”

Resonate CRT-D and Its HeartLogic Algorithm

In addition to Boston Scientific,Vectorious Medical Technologies has developed V-LAP, a minimally invasive device implanted on the interatrial septum.TM, with a sensor on the left atrial side. In addition to the implant, patients need to wear a belt-mounted device, similar in size to a Walkman and equipped with a switch, which powers the implant and automatically transmits monitoring data to a cloud-based system. Leveraging this technology, Vectorious Medical Technologies secured $10 million in Series B funding last year, with Fresenius participating in the investment.

Currently, V-LAPTMCurrently undergoing registration clinical trials in Europe.

Although CardioMEMS, Cordella, HeartLogic, and V-LAPTMAlthough monitoring of pulmonary artery pressure or left atrial pressure has been achieved, these approaches require invasive implantation and are costly. The new solution will usher heart failure management into an era of non-invasive precision.

Sensible Medical, an Israeli company, has developed Sensivest, a wearable vest that detects pulmonary fluid accumulation using radar wave technology. As heart failure patients often experience fluid retention in the mid-to-late stages of disease progression, Sensivest facilitates heart failure management by noninvasively and quantitatively measuring lung water. This technology has received FDA approval and was recently licensed to Bayer following their interest in the innovation.

A domestic company namedDARMA Tech (commonly abbreviated as DARMA)The company is also developing non-invasive heart failure management devices.

DARMA’s core technology is fiber-optic sensor technology. VCBeat has reported on the company’s medical-grade intelligent monitoring solutions and its “image-free cardiac ultrasound” for noninvasive, continuous hemodynamic monitoring. Recent information indicates that DARMA has adopted the multi-parameter combination strategy used by Boston Scientific’s HeartLogic, which leverages the third heart sound as a core parameter. Furthermore, based on noninvasive hemodynamic data, DARMA has developed and refined two additional key parameters. These are integrated with heart sound data to construct algorithms for analysis, enabling accurate assessment of left atrial pressure and thereby facilitating the management of patients with heart failure.

Preliminary clinical results indicate that DARMA’s heart failure product is non-inferior to HeartLogic, the latter of which demonstrated an accuracy rate of 70% in FDA clinical trials.The accuracy of the combined three-parameter assessment using DARMA was 92%.

In terms of technical principles, the DARMA fiber-optic sensor array continuously detects cardiac pulse waveforms from the back to assess hemodynamic information. The product can be designed in the form of a mat or a vest, allowing for seamless application in various settings such as homes, hospitals, and elderly care facilities.It is worth noting that DARMA has also significantly reduced the cost of its heart failure monitoring products, making them affordable for the majority of people.

From the perspective of current market capacity, although China has a large number of heart failure patients, the existing domestic market for heart failure management remains nearly untapped.

According to the "2018 Chinese Guidelines for the Diagnosis and Treatment of Heart Failure," in 2018, there were 10 million heart failure patients and 270 million high-risk individuals in China. If the penetration rate of heart failure management devices reaches 70%, with an average per capita expenditure of RMB 5,000, the total potential market size for heart failure management devices would amount to RMB 50 billion.

From the perspective of market growth trends, cardiac rhythm management (CRM) devices and heart failure (HF) products constitute the largest single segment within the cardiovascular market. In the global medical device market, cardiovascular medical devices account for 12%, making it the second-largest segment after in vitro diagnostics; in China, cardiovascular implantable devices account for only 6% of the medical device subsector. There is still significant room for market growth.

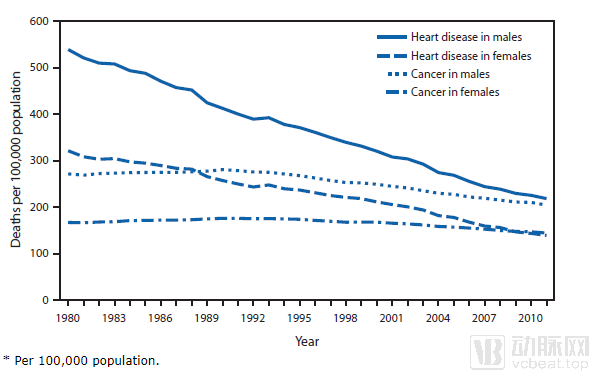

In terms of incidence, cardiovascular mortality in the United States has declined significantly since 1995, whereas in China, both the prevalence and mortality of cardiovascular diseases have continued to rise for many years. According to Cong Hongliang, Director of the Cardiology Department at Tianjin Chest Hospital, “As the final outcome of various cardiovascular diseases, heart failure is currently the only cardiovascular disease whose prevalence, incidence, and mortality are increasing year by year.”

Age-Adjusted Death Rates* for Heart Disease and Cancer,† by Sex — United States, 1980–2011

Changes in Cardiovascular Mortality Among Urban and Rural Residents in China, 1990–2016: Data from the *Report on Cardiovascular Diseases in China 2018*

In the U.S. market, there is a wide variety of products, including both implantable and non-invasive solutions, resulting in intense competition in the heart failure management sector. In contrast, this market remains nearly untapped in China, with few available solutions and existing management methods being prohibitively expensive, thereby limiting patient accessibility.

The primary reason for the limited number of heart failure management products in the domestic market is insufficient market awareness. Currently, major players in the cardiovascular market remain predominantly focused on in-hospital settings, with relatively little attention paid to out-of-hospital and home-based care. Additionally, patients’ understanding of cardiovascular diseases remains inadequate.

With deepening market awareness, the heart failure management market is poised for explosive growth.