Health Insurance TPA Takes Off: Dozens of Companies Secure Funding as Redpoint, Qiming and Other Top VCs Rush into a Trillion-Yuan Blue Ocean

Sequoia Capital China, in a highly specialized niche of the healthcare industry, has once againAction Taken。

This July, Sequoia Capital China led a RMB 50 million Series A financing round for Yuanxin Huibao Technology; in August, it also led a RMB 100 million angel financing round for Nuanwa Technology.

Not only Sequoia, but also dozens of investment institutions, including Star VC, BV Baidu Ventures, and Qiming Venture Partners, have invested in companies operating in the health insurance TPA (Third-Party Administrator) sector.

Health insurance TPA is a niche segment within the health insurance industry. According to data from VCBeat, more than half of this year’s financing and investment activities in the health insurance sector have been concentrated in the health insurance TPA segment. This trend aligns, to some extent, with the assessment of investment institutions: as the health insurance market continues to expand, TPAs will be the first to reap the dividends. “In the rapidly expanding health insurance market, TPA companies that provide services centered around payers will quickly break through,” said Huang Shengxuan, Managing Director at Sunshine Ronghui Capital, in an interview with VCBeat.

VCBeat interviewed more than ten senior industry insiders, including Peng Xuan, CEO of Yuanxin Huibao Technology; Lu Min, CEO of Nuannuo Technology; and Ji Chunhui, founder of Yingshi Health, on issues such as the definition, business models, pain points, prospects, and market size of third-party administrators (TPAs) in the health insurance sector. Opinions varied among the interviewees, with significant disagreements on certain topics.

However, there is a tacit consensus among all:

Health Insurance TPA Takes Off。

Image source: VCBeat

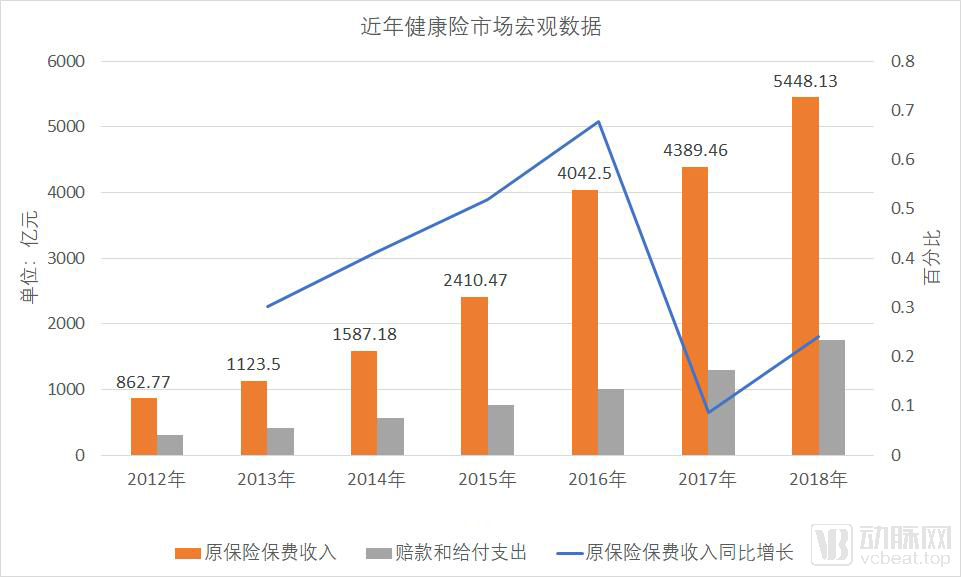

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), domestic health insurance premium income amounted to only RMB 86.277 billion in 2012. From 2013 to 2018, the health insurance market achieved a compound annual growth rate (CAGR) of 35.95%, with premium income reaching RMB 544.813 billion in 2018. Based on this growth trajectory, the health insurance market size is projected to surpass the trillion-yuan mark by 2021 at the latest.

When it comes to market trends, capital is undoubtedly the most sensitive. Faced with the rapid growth of health insurance and a trillion-yuan blue ocean, investment institutions have flocked in. Dozens of companies have announced completed financing rounds, dozens of investment firms have participated, and billions of yuan have been poured in—almost unnoticed,Health Insurance Has Become a Hotspot。

In fact, the surge in popularity of health insurance follows an inherent logic.

As out-of-pocket health expenditures rise, the population ages, urbanization accelerates, the middle-income group expands, and the number of people with chronic diseases grows, the current capacity of social security provision is far from meeting the rapidly growing demand for health protection among the public.

For the government, improving the efficiency of medical insurance fund expenditures and implementing cost containment measures have been the main directions of healthcare reform in recent years. To alleviate the pressure on medical insurance, the government has repeatedly introduced policies to encourage the development of commercial insurance, emphasizing the need to “develop commercial health insurance to serve as a supplement to the medical security system.”

With the rapid growth of health insurance, health insurance TPAs have naturally risen in prominence, marking a turning point in their trajectory.。

TPA, short for Third Party Administrator, is commonly translated as a third-party service provider. It refers to an arrangement in a health insurance plan where the insurer retains the core obligation of bearing risk and claim liabilities, while delegating part or all of the non-core administrative and management tasks to other entities specializing in such services.

The entity that accepts delegated management responsibilities is a third party added to the traditional chain of relationship between insurers and insureds—the Third-Party Administrator (TPA). This TPA can be either a specialized TPA organization or a traditional insurance company. The TPA provides administrative services such as claims management and member enrollment for captive groups or newly established managed care plans, typically without assuming any risk.

Abroad, the TPA (Third-Party Administrator) model for health insurance has become relatively mature. Taking the United States as an example, the U.S. adopts a market-driven managed care insurance model, primarily achieving the integration of medical fund management and healthcare services through Health Maintenance Organizations (HMOs). Unlike traditional health insurance, where insurers and healthcare providers are separate, HMOs not only underwrite insurance business but also possess their own stable medical resources. As a type of health insurance organization that closely integrates insurers with healthcare institutions, HMOs unify the roles of healthcare service providers and payers of medical insurance funds.

In India, the Indian model is a TPA (Third-Party Administrator) model under the supervision of statutory regulatory bodies. TPAs establish their own healthcare service networks, which consist of medical institutions such as hospitals, general practitioners, diagnostic centers, and pharmacies. Leveraging these healthcare service networks and professional management capabilities, TPAs provide insurers with a range of services, including medical management and claims processing. Insurers pay TPAs a certain percentage of service fees based on the number of policies and the scope of services covered.

For health insurance TPA companies in China, the industry is still in its early stages. Traditional business lines primarily include claims processing, coordination of medical expense settlements, and reimbursement administration, while emerging business lines encompass risk control, product development, healthcare service network construction, and health management.

TPA service providers, which operate between policyholders and insurance companies, have emerged in response to pain points within the health insurance industry. Wang Guangying, Managing Partner at Pugongying, stated: “It is precisely because the pain points in health insurance are so significant that TPA has become so popular.”。

In the traditional operation of health insurance, issues such as information asymmetry, low levels of specialization, high loss ratios, and limited profitability are prevalent. Since health insurance accounts for a relatively small share of total social healthcare expenditure, insurers lack sufficient leverage over healthcare providers. This hinders commercial insurance companies from establishing high-quality medical service networks necessary for effective control and intervention in healthcare costs.

Furthermore, insurance companies, after comprehensive consideration, are reluctant to handle tedious operations such as market research, channel management, customer relationship maintenance, underwriting, and claims adjustment on their own. Thus, Third-Party Administrators (TPAs) have emerged “in response to demand.” By participating in health insurance operations as independent entities, TPAs can effectively address these issues.

Health insurance TPA (Third-Party Administrator) service providers in China have largely developed since 2012, initially focusing primarily on handling miscellaneous tasks outsourced by commercial insurers. Gu Bing, General Manager of Beijing Financial Street Insurance Brokerage Co., Ltd., stated, “Traditional TPAs essentially handle the tedious and labor-intensive tasks outsourced by health insurers. Their main functions include processing invoice reimbursements, data governance, cost-control management, and providing treatment and claims settlement recommendations to insurers within the limits of coverage.”

However, driven by rapid market growth and technological advancements, health insurance TPAs are ushering in an era of large-scale innovation.。

Regarding the actual market size of traditional health insurance TPAs, Peng Xuan, CEO of Yuanxin Huibao Technology, provided a conservative estimate:3 billion。

He believes that within the next three years, the market size of internet health insurance, represented by million-yuan medical insurance, will reach RMB 50–60 billion. Of this amount, 40% will be allocated to distribution channels, leaving approximately RMB 30 billion in net premiums. Ten percent of these net premiums will go to TPA providers, resulting in a market size of RMB 3 billion.

However, if we broaden the conceptual scope of health insurance TPA, Wang Yanhua, General Manager of Miao Jiankang’s Miao Bao Division, provided her own estimate regarding the potential market size for health insurance TPA:Over RMB 100 Billion。

Wang Yanhua stated, “I believe the future market size for Third-Party Administrators (TPAs) will be substantial. According to documents issued by the China Insurance Regulatory Commission (CIRC), health services can account for 20% of health insurance premium income. If the health insurance market reaches a trillion yuan in the future, the TPA market within the health insurance sector would amount to 100–200 billion yuan.”

The document on which Wang Yanhua’s estimates are based is the “Administrative Measures for Health Insurance (Draft for Comments)” issued by the China Insurance Regulatory Commission in 2017. The document states that insurance companies may integrate health insurance products with health management services to provide health risk assessment and intervention, as well as services such as disease prevention, health examinations, health consultations, health maintenance, chronic disease management, and wellness and healthcare. The costs allocated to these services shall not exceed 20% of net premiums. Services exceeding this limit shall be priced separately, excluded from insurance premiums, and the prices for health management services shall be explicitly stated in the contract.

From an initial market size of RMB 3 billion to a potential market exceeding RMB 100 billion in the coming years, against the backdrop of such broad prospects for health insurance TPA, stories of innovation are being told one after another.

During interviews with numerous companies in the industry, VCBeat observed an intriguing phenomenon: many firms widely regarded by outsiders as standard health insurance TPA (Third-Party Administrator) enterprises promptly denied being TPAs, preferring instead to describe themselves using labels such as “health insurtech company,” “innovative payment solution provider,” or “integrated end-to-end health insurance service provider.”

“It is evident that the industry’s understanding of health insurance TPA (Third-Party Administrator) remains largely confined to traditional TPA services, such as receipt-based reimbursement and underwriting. ‘Traditional health insurance TPAs are claims-oriented. However, if we broaden the concept, any third-party service provider supporting commercial insurance companies can be considered a TPA. Our focus lies in the incremental market for health insurance, specializing in innovative and customized solutions. By implementing comprehensive risk control and cost containment throughout the entire process, we deliver core value to insurance companies,’ said Ji Chunhui, founder of Inshi Health.”

Based on their respective understandings of health insurance, the three companies reported the proportion of their health insurance TPA businesses.

“TPA business accounts for about 60% of our total business,” said Peng Xuan, CEO of Yuanxin Huibao Technology. This proportion stands at 30% for Nuanwa Technology and 100% for Yingshi Health.

According to Wang Yanhua of Miao Health, 50% of their revenue this year comes from the insurance sector.

If categorized according to the clinical care pathway, the business operations of health insurance TPA providers can be divided into three categories:

At the front end of diagnosis and treatment, with access to extensive medical and insurance data and strong technical capabilities, it supports insurers in product development, risk control, and other business operations.

In the midstream of healthcare delivery, it possesses a medical service network that provides convenient access to care, premium medical services, direct hospital billing, and health management.

The backend of diagnosis and treatment can provide services such as medical care surveys, invoice reimbursement, claims filing, and claims assessment.

Traditional Third-Party Administrators (TPAs) have primarily focused on the downstream segments of diagnosis and treatment, with established players such as Shangbaotong and MSH China representing this sector.

The former is a third-party administrator under the Shenci Group, specializing in providing direct billing health services to corporate clients and insurance companies. Established in 2005, Shangbaotong’s primary business areas include health insurance claims processing, direct-payment medical networks, and collaborative mutual insurance programs.

The latter, established in 2001, is the largest third-party administrator (TPA) in China’s high-end health insurance sector, with services spanning marketing, claims processing, risk control, and IT system support.

As technology empowerment drives growth and the health insurance market expands,An Increasing Number of Innovative Players Are Entering the Health Insurance TPA Arena, its business has expanded upstream from the backend of diagnosis and treatment to the midstream and frontend, and it is even capable of delivering integrated, closed-loop services to the industry.

“China’s health insurance market is still very young, with service experience continuously accumulating, and the industry faces a pressing need for growth and iteration,” said Qu Yuqi, CFO of Medlinker. Addressing the pain points of high out-of-pocket expenses for patients and limited access to high-quality services, Medlinker, founded in 2017, aims to start from the payment side by aggregating the needs of self-paying patients and integrating the upstream and downstream segments of the healthcare value chain. Medlinker’s founder, Zhang Xiaodong, previously served as COO of SPH Cloud Health.

Jianyibao, also founded in 2017, is engaged in the integration of “health insurance + pharmaceuticals.” Founder Zhang Shengming previously held marketing and sales roles at multinational pharmaceutical companies and has experience in the insurance industry, where he participated in and led the development and operation of numerous insurance products tailored for individuals with chronic diseases. To achieve a more effective and innovative combination of insurance and pharmaceuticals, Zhang conceived the idea of starting his own venture. In October 2018, Jianyibao secured tens of millions of yuan in Series A financing from BV Baidu Ventures.

Furthermore, in recent years, a wave of innovative enterprises has emerged in the market, including Nuohui Medical, which provides health insurance solutions for critical illnesses, and Yingshi Health, which leverages technology platforms to enable customized health insurance and comprehensive risk control management throughout the entire process.

However, among the numerous players, Yuanxin Huibao Technology and Nuanwa Technology stand out. The former, spun off from Yuanxin Technology, is a comprehensive health insurance service provider that mainly offers specialized drug services, online consultations, pharmaceutical benefits, and claims investigation services. It has mature solutions in areas such as actuarial pricing of products, risk control, user acquisition, and retention. The latter, spun off from ZhongAn, has accumulated extensive internet operational concepts and technologies in the health insurance sector. Shortly after their establishment, the two companies secured RMB 50 million and RMB 100 million in financing, respectively, led by the star venture capital firm Sequoia Capital China.

The successive entry of star venture capital firms and leading internet insurance companies seems to herald a major transformation in this industry.

Taiping Insurance, Huaxia Insurance, Pacific Insurance... These traditional insurance giants may never have imagined that their development would one day depend on the trivial business outsourcing vendors of the past.

With technological innovation and the rapid growth of the health insurance market, health insurance TPA (Third-Party Administrator) services have undergone rapid iterative upgrades, evolving from traditional claims-based TPAs to resource-based and technology-driven TPAs. This evolution has given rise to two distinct phases—1.0 and 2.0—although the boundary between these two stages is not entirely clear-cut.In the current Phase 2.0, TPAs have gained sufficient leverage over insurance companies.。

The so-called Health Insurance TPA 1.0 era dates back to 2014. Prior to this, the health insurance market was relatively small in scale, with TPA services primarily focused on claims processing and other areas, requiring minimal technological support.

The so-called “TPA 2.0” era in the health insurance sector began in 2015, when new forms of resource-driven and technology-driven Third-Party Administrators (TPAs) emerged in the market. The year 2015 is widely regarded by the industry as the inaugural year of the health insurance boom. At that time, major insurance companies began to prioritize their health insurance businesses, establishing dedicated teams to explore the health insurance market, developing a range of vertically segmented health insurance products, and initiating efforts to integrate health insurance with medical services and health management.

Against this backdrop, capable health insurance TPA companies have gradually expanded from back-end operations to mid- and front-end services. Today’s health insurance TPAs assist insurers in product development and risk control, leverage technology for intelligent underwriting and claims processing, and build medical service networks that have become a major selling point for health insurance products.The Former Third-Party Player Now Stands in the Industry Spotlight。

“TPAs initially stepped in to handle tasks that commercial insurers were reluctant to undertake. However, with continuous technological innovation, the scope of TPA services has expanded significantly, while their specialization and efficiency have improved markedly. As a result, commercial insurers have become increasingly reliant on TPAs; indeed, without TPAs, many insurance operations would now be unfeasible,” explained Jiang Guanjun, Partner at Milliman, an actuarial consulting firm, regarding the evolution of the health insurance TPA business.

The business evolution of health insurance Third-Party Administrators (TPAs) has been so rapid that it has even outpaced the inherent meaning and understanding of the term “TPA” itself. Companies emerging during the TPA 2.0 phase rarely identify themselves as health insurance TPA firms; for instance, Yiguo Doctor, which boasts a high-quality medical service network, has completely disavowed any association with the TPA model. Instead, these enterprises have focused on addressing the pain points in health insurance products, operations, and services, capitalizing on the opportunities presented by large-scale innovation in the health insurance sector.

It is indeed inappropriate to readily describe the businesses of many companies using the concept of Third-Party Administrator (TPA). For instance, enterprises such as Nuohui Medical, Nuanwa Technology, and Yuanxin Technology are more dedicated to integrating the healthcare industry chain or leveraging technology to empower the sector, thereby providing innovative payment solutions. Compared with traditional health insurance TPAs, these companies prefer to identify themselves as ecosystem players in the “Insurance + Healthcare” model, although a significant portion of their current revenue still comes from insurance companies.

“The core assets of an insurance company are its insurance license and sales network; beyond these, TPA firms can step in to handle other operations.” Wang Guangying, Managing Partner at Pugongying, believes that once TPA companies have scaled up, they can acquire insurance companies in a reverse takeover, a precedent already seen abroad.

The significant transformation in the health insurance TPA business marks, to some extent, an upgrade of the entire industry, namelyThe entire healthcare industry is transitioning from traditional fee-for-service reimbursement models to service-oriented and managed care.。

Insurance products rely on the evolution of Third-Party Administrators (TPAs); both health management and TPA services are indispensable components of health insurance.

While TPAs have addressed the pain points of the health insurance industry, they themselves still face numerous challenges.

“The ceiling for traditional health insurance TPAs is relatively low; most of these companies lack investment in technology and find it difficult to leverage technology to provide genuine, effective support for their operations,” said Lu Min. He believes that next-generation health insurance technology presents high barriers in areas such as data, risk control, and automation. While there are some pioneers in the industry’s digitalization and automation, few companies have truly undergone the rigors of practical application, and the sector will inevitably undergo a process of survival of the fittest. “The overall improvement of the industry is a gradual process,” he stated.

Peng Xuan shares a similar view with Lu Min. He believes that the industry is currently mixed with good and bad players and highly unregulated, giving the impression that anyone can engage in TPA services. “The industry needs several years to mature before quality companies will emerge.”

Although it also has many pain points, there is no doubt thatThe Prospects for Health Insurance TPAs Are Very Clear。

Wang Yanhua believes that a platform akin to Alipay in the financial sector will emerge in the insurance industry. “As contemporary operational services continue to improve, the nature of insurers’ third-party service providers is changing. With operators becoming increasingly technology-driven and platform-oriented, they can move to the forefront and establish themselves as independent brands.”

Health insurance should not be limited to mere coverage; instead, it should provide comprehensive protection grounded in health. Establishing an ecosystem of “insurance + healthcare + health management” not only delivers a better insurance experience for policyholders but also maximizes the value of health insurance.

This ecological integration is precisely the “"A Place to Put One's Skills to Use"“。

Sequoia Capital has made a decisive move in the health insurance TPA sector.

(We extend our sincere gratitude to the following enterprises and institutions for their invaluable assistance during the interviews for this article:Miao Health, Nuanwa Technology, Yuanxin Technology, Yingshi Health, Mingde Actuarial Consulting Company, Yuguo Doctor, Magnesium Health, Pugongying, Beijing Financial Street Insurance Brokerage, Nuohui Medical, Jianyibao, Sunshine Ronghui Capital。)