Rock Health Q3 2019 Digital Health Funding Report: $1.3B Raised with Behavioral and Women's Health in Spotlight

Talkspace

Mental Health Telemedicine Service Provider

Quartet Health

Mental Health Service Platform Operator

Beta Bionics

Developer of Integrated Bionic Pancreas System

Change Healthcare

Intelligent Medical Network Service Provider

Health Catalyst

Medical Data Development Service Company

Livongo

Chronic Disease Management Service Provider

Phreesia

Patient Registration Automation Service Provider

Peloton Interactive

Intelligent Fitness Service Provider

Pear Therapeutics

Developer of Digital Healthcare Solutions

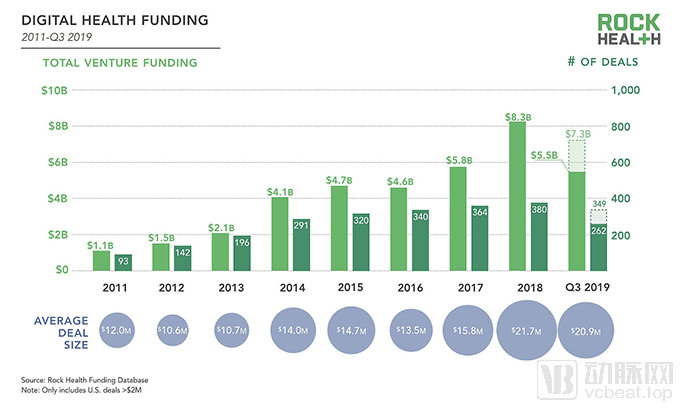

Recently, Rock Health released its financing and investment report for the third quarter of 2019, which VCBeat (WeChat ID: vcbeat) has translated as usual. In Q3 2019, the digital health industry secured $1.3 billion in funding. This represents a slowdown compared to the $2 billion raised per quarter during the first half of the year. Including the total from the first half, digital health companies raised a cumulative $5.5 billion in 2019, positioning the year to become the second-highest on record for industry funding. As in 2018, mega-rounds continued to shape the overall landscape this year. In this quarterly market update, we will discuss the public market performance of five digital health IPOs (with mixed early results), as well as two hot investment sectors: behavioral health and women’s health.

Digital Health Funding Levels Stabilize After 2018 Peak

Venture capital investment in digital health remains near historic highs. Startups in this sector are poised to raise $7.3 billion by the end of this year—1.3 times the 2017 level, but still below the record $8.3 billion set in 2018.

As with the broader venture capital industry, mega-round financings are shaping funding trends in the digital health sector. Investors are concentrating their bets on a select few companies: the average financing amount in the industry reached $20.9 million in 2019, a 32% increase from 2017 and on par with the $21.7 million average in 2018. Meanwhile, we anticipate that the number of financing deals in the digital health sector will decline by 5%–10% in 2019 compared to 2018. This may mark the first year-on-year decrease in the number of financing deals since Rock Health began tracking these trends in 2011.

Image from Rock Health

Mega-Deals and Capital Concentration Are the Trend

To date, there have been nine financing rounds exceeding $100 million in 2019. This figure is roughly comparable to the record 11 mega-financing rounds seen in 2018. Two such large-scale financing events occurred in the third quarter of 2019:

In September, Capsule, an online pharmacy offering same-day delivery in New York City, completed a $200 million funding round to expand its services nationwide. Capsule’s national expansion plan has further intensified competition in the online prescription market. Amazon entered the pharmacy business by acquiring PillPack in 2018. It will compete with pharmacy giants CVS and Walmart, which also provide online pharmacy services.

Beta Bionics, the developer of an automated bionic pancreas, completed two rounds of financing this year: a Series B round in January and a Series B2 round in July. Each round raised $63 million, bringing the total amount raised in its Series B financing to $126 million. The funds will be used for final product development, Phase III clinical trials, submission of clinical reports, and the commercial launch of the iLet Bionic Pancreas System. Beta Bionics’ products are primarily designed to create a closed-loop insulin delivery system for patients with type 1 diabetes. Its competitors include not only startups such as Bigfoot, but also industry giants like Medtronic and Dexcom.

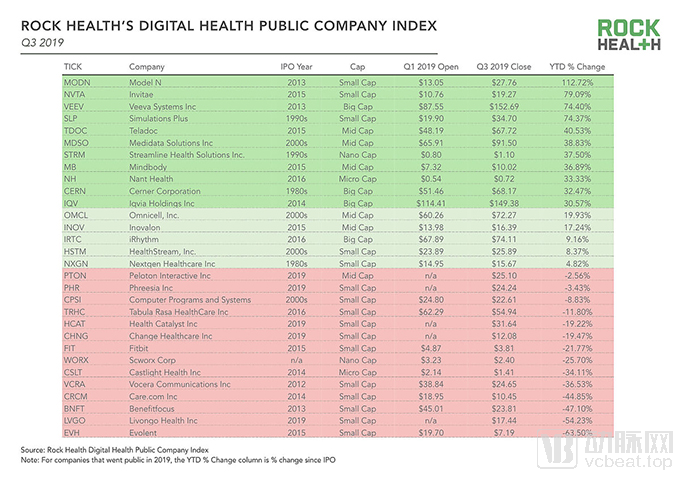

IPOs in the digital health sector are booming—five companies have gone public this year, with another one set to list soon.

As capital flows toward companies with mature business models, exit activity in this sector is also heating up. Five digital health companies have gone public so far in 2019: Livongo, a chronic disease management platform; Health Catalyst, which provides data and analytics technology services to healthcare organizations; Phreesia, which helps healthcare organizations manage patient intake processes; Change Healthcare, which offers revenue cycle management, payment management, and health information exchange solutions; and Peloton, which delivers real-time, on-demand fitness classes through stationary bikes, treadmills, and applications within its service network.

Image from Rock Health

The early public market performance of these IPOs has been mixed. Health Catalyst’s stock price on October 1 was approximately 20% lower than its closing price on the first day of trading, following a more than 20% increase in the preceding weeks. Livongo’s share price declined after its inaugural earnings report; although its revenue grew by 156%, surpassing Wall Street expectations, its losses also exceeded analysts’ forecasts. The stock prices of Phreesia and Change Healthcare remained relatively stable, largely fluctuating within 10% of their respective offering prices. Peloton’s stock broke below its IPO price on its listing day, September 26, which was viewed as a signal of cooling sentiment in the 2019 healthcare IPO market.

At last week’s Rock Health Summit, Rock Health staff and attendees speculated about which company would follow Peloton in completing an initial public offering (IPO). As of today, all 700 participants got it wrong—the answer is Progyny, the fertility benefits management company that has just filed its IPO prospectus. This is no coincidence, as we are witnessing increased investment in women’s health. We are also seeing this trend in investments within the mental and behavioral health sectors.

The behavioral health sector attracted substantial funding in 2019, while investment in the women’s health sector also increased.

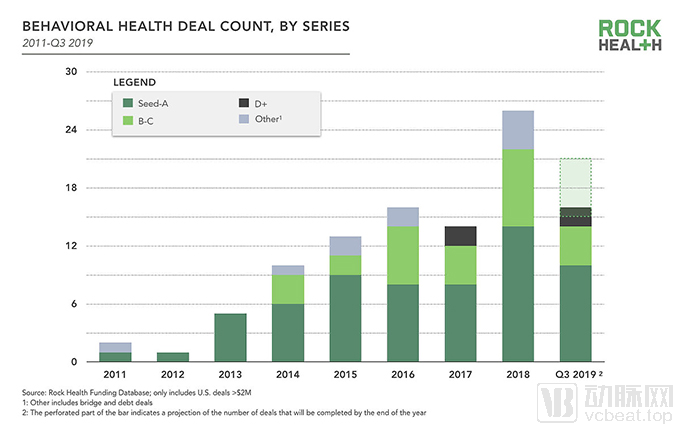

Digital behavioral health is showing signs of becoming a mature investment sector: increased investment activity, larger funding rounds, more late-stage companies, and a consistently robust pipeline of early-stage innovation. We define behavioral health as encompassing solutions that address a spectrum of needs, ranging from basic mental wellness to disease treatment—including companies like Calm and Headspace, which offer relaxation and meditation solutions, and Akili Interactive Labs, which provides digital therapeutics—as well as platforms delivering behavioral healthcare, such as Lyra Health. Given the alarming rise in suicide and depression rates in the United States in recent years, this is a field with substantial demand. Fifty percent of Americans report that these common mental health conditions have affected them at some point in their lives.

Investment and Financing Data in the Digital Behavioral Health Sector:

Financing: In the third quarter of 2019, a total of 16 digital behavioral health companies secured financing, with the total amount reaching $416 million, accounting for 8% of the total digital health financing during the same period. Looking back to 2012, there was only one financing deal in the digital behavioral health sector that year. In 2016, this number rapidly increased to 16, and has since remained at or above this level.

Financing Scale: To date, the average digital behavioral health financing amount in 2019 was $26 million, representing a 73% increase from 2018 levels. However, total digital health financing decreased by 4% compared to 2018.

Late-Stage Financing: Since 2016, 30%–40% of behavioral health financing has gone to Series B or later stages. Meanwhile, 60% of companies remain in the early stages, indicating that emerging enterprises continue to thrive.

In 2019, four behavioral health companies raised $50 million or more in financing:

Talkspace ($50 million): Talkspace’s telebehavioral health platform connects patients with licensed therapists;

Quartet ($60 million): Its platform enables healthcare institutions to collaborate on developing treatment plans and provides patients with gatekeeper-like review support.

Pear Therapeutics ($64 million) is a clinically validated digital therapeutics company. It has two products on the market, targeting substance use disorder and opioid use disorder, respectively;

Calm ($88 million): This unicorn company, valued at $1 billion, primarily offers applications for sleep, meditation, and relaxation.

Image from Rock Health

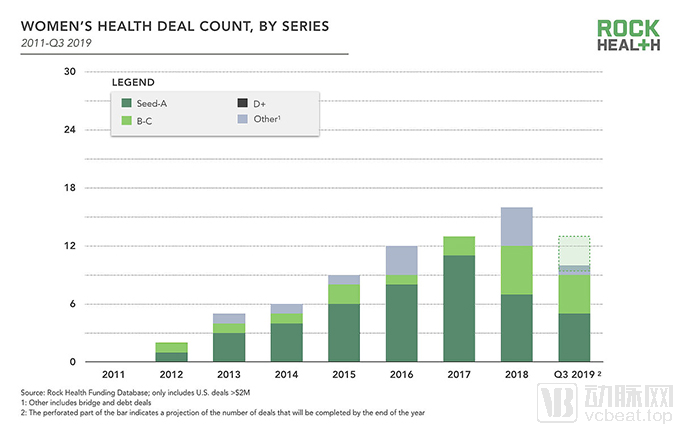

Financing in the field of women's health is also booming:

Increased Financing: The women’s health sector completed 16 financing rounds in 2018, with the total amount raised increasing by 812% compared to 2014. This trend mirrors that of the behavioral health sector two years prior. In 2016, the behavioral health sector also secured a comparable level of funding. Throughout the third quarter of 2019, a total of 10 women’s health companies completed $177 million in financing.

Late-Stage Financing: In 2018, 30% of women’s health companies secured Series B or later-stage financing, marking the first time that such a high proportion of companies in this sector had reached late-stage funding. This trend continued in 2019.

Image from Rock Health

The three largest financing rounds in the women's health sector from 2019 to date include:

Nurx ($52 million): This online healthcare provider offers contraception, at-home HPV testing, and HIV pre-exposure prophylaxis (PrEP).

The Pill Club ($51 million): Provides online prescription and delivery services for birth control and contraception;

Cleo ($27.5 million): Provides online virtual services, offering guidance on preconception care and postpartum recovery for women.

As women increasingly become the primary healthcare decision-makers and providers, women’s health is emerging as a significant investment sector. “Let this be the moment when investors stop calling women’s health a niche market,” said CNBC’s Krystal Falch, commenting on the investment boom in women’s health. Startups are addressing the comprehensive health needs of women across contraception, menstrual health, pregnancy, fertility, gynecology, and menopause.

Some of the best-funded startups in this field are establishing direct-to-consumer (D2C) connections with patients through remote prescription models. We are also encouraged to see employers investing in women’s fertility, maternal, and child healthcare. Although the initial intent was to optimize revenue and expenditures, this trend also reflects society’s growing emphasis on women’s health. We believe that the women’s health industry has only scratched the surface. With the emergence of digital diagnostics and biomarkers, new solutions may delve deeper into relevant areas of women’s health, particularly those related to fertility, such as therapies for endometriosis and polycystic ovary syndrome (PCOS).