Healthcare Services Sector: Four IPOs and Sixteen Funding Rounds Completed — How Much Room Is Left for Growth?

Compared with the booming innovative drugs, innovative medical devices, and the more diverse exit mechanisms brought by the STAR Market, the healthcare services industry in 2019 appeared relatively low-key.

On the one hand, the overall external financing environment is relatively sluggish, making it more difficult for enterprises to secure funding. On the other hand, capital is increasingly flowing toward leading companies that either demonstrate significant high-growth potential or have already validated their business models.

However, as the recipient and implementation setting for medical activities, the capacity of healthcare services to meet patient demand is significantly inadequate. This is particularly evident in large public hospitals, which are operating beyond their capacity, leading to a "the strong get stronger" dynamic. Although these institutions are striving to improve the quality of medical care and operational efficiency, they still have a long way to go before achieving a balance among clinical outcomes, service experience, and cost.

As a supplement to public hospitals, encouraging private medical practice has become a visible trend in the development of the healthcare industry. New types of clinics and specialized hospitals with distinctive features in brand operation, product design, service capability, operational models, and management standards are constantly emerging. They are strategically positioning themselves in areas that are less accessible to public hospitals, characterized by differentiation or relative marginality, such as women’s and children’s health, medical aesthetics, ophthalmology, dentistry, and rehabilitation, thereby forming an avoidance-based market positioning.

Generally, when selecting their market niches, these enterprises differentiate themselves from public hospitals by establishing departments, projects, workflows, and products based on patient needs. They aim to provide more convenient and accessible services, as well as enhanced medical care, while maintaining greater flexibility in marketing management.

Driven by capital, leading chain brands have emerged in certain niche sectors. However, this asset-heavy model exhibits strong regional characteristics, and the burden of managing “chains” has become a common complaint among startups. Leveraging digital tools to optimize workflows and enhance efficiency, expanding business operations horizontally and vertically, and evolving organizational management models have quickly become a consensus within the healthcare services sector.

How are companies in the healthcare services sector evolving? How can they successfully implement chain-operation models? Why do some enterprises manage to go public and achieve phased success? What new business models are quietly emerging, and how can companies develop new revenue streams? VCBeat (WeChat ID: vcbeat) has compiled and analyzed these issues.

Next, you will learn about:

1. In the medical services sector, which niche segments are most favored by investors;

2. What conditions should a good clinic or hospital meet?

3. In the healthcare services sector, high-quality assets suitable for securitization;

4. Why Are Companies with Annual Revenues Exceeding RMB 1 Billion and Profits Surpassing RMB 100 Million So Rare?

5. Analysis of New Healthcare Service Models and Specialized Medical Cases.

Healthcare services are not currently in high demand; in the long term, it is a counter-cyclical industry.

The flow of capital serves as a barometer for the level of interest in a given sector.

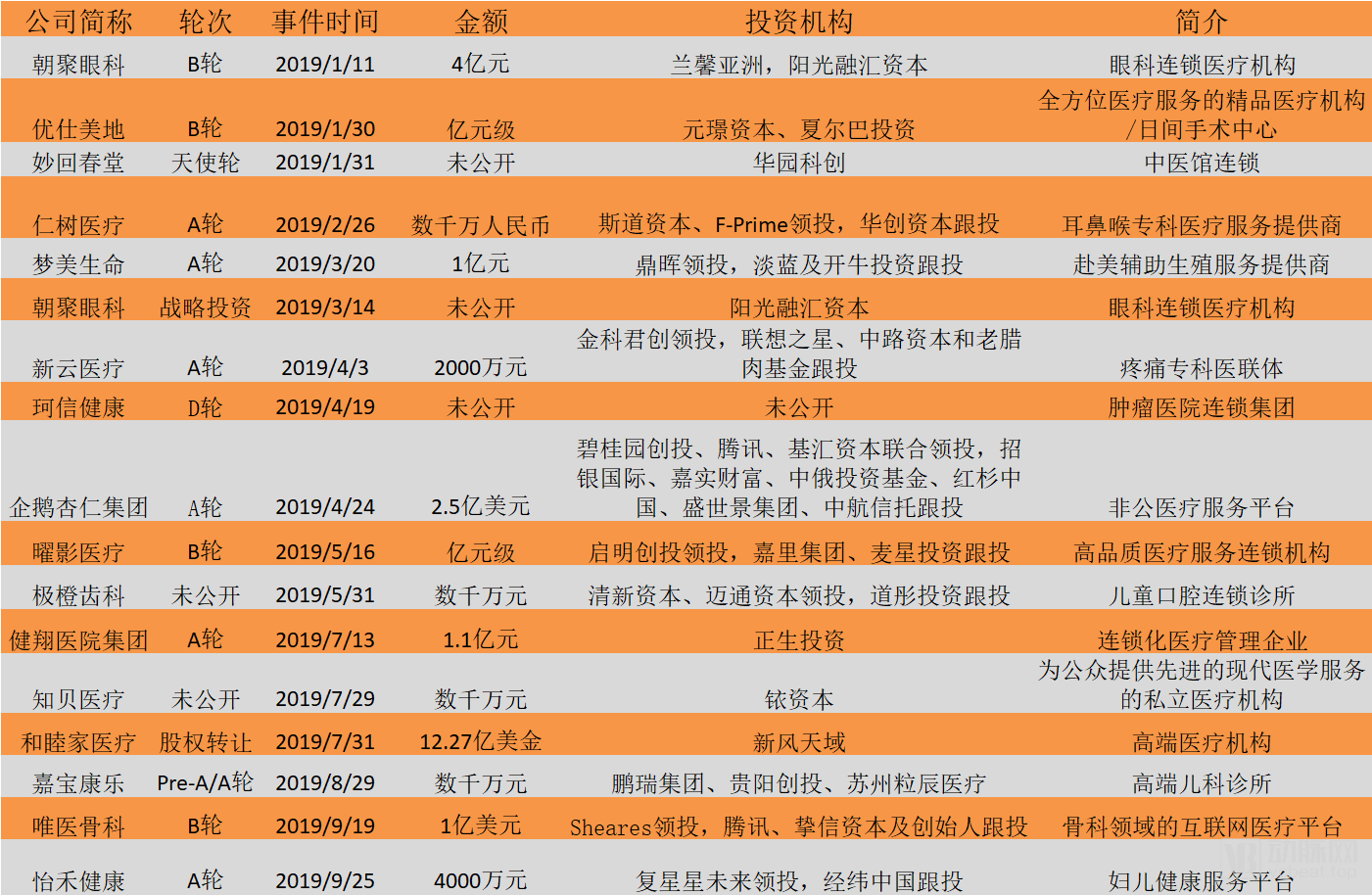

A review of financing data in the medical services sector through October shows that 16 companies with physical facilities completed a total of 17 financing rounds, indicating that this segment is not a hot area for investment within the broader healthcare industry. Notably, Chaoju Eye Care, Usmile, Mengmei Life, Penguin Almond, United Family Healthcare, Jianxiang Hospital Group, United Family Healthcare, and Weiyi Orthopedics all closed deals worth RMB 100 million or more.

It can be observed that the majority of companies securing financing this year are innovative leaders in their respective sectors and business models. These companies are primarily concentrated in specialties such as pediatrics, ophthalmology, obstetrics and gynecology, otolaryngology, pain management, orthopedics, reproductive medicine, and oncology. These specialties generally exhibit characteristics such as meeting essential patient needs (e.g., pediatrics, pain management, obstetrics), high scalability (e.g., ophthalmology, stomatology), or high average revenue per user (e.g., oncology, assisted reproductive technology).

In terms of revenue scale, the reporter learned that the compound annual growth rates (CAGR) for specialized hospitals in aesthetics, rehabilitation, ophthalmology, and dentistry all exceeded 20%, indicating rapid revenue growth. It is precisely due to these favorable revenue performances that there has been a proliferation of new clinics in these sectors.

It is worth noting that, impacted by the continued decline in birth rates, the revenue growth of obstetrics and gynecology hospitals has slowed significantly compared to previous years. Consequently, many pediatric clinics are generally introducing new service offerings and integrating additional resources to expand their target patient populations and service portfolios.

So, how do investors view the healthcare services industry, and how do they evaluate the quality of potential targets? Lin Zhencheng, Investment Director at Daotong Investment, believes that one must first consider the market size and whether there is a prominent supply-demand imbalance. Secondly, priority should be given to sub-sectors with strong consumer-oriented characteristics. “The choice of sector determines the pace of a company’s growth. Healthcare service companies should not rely on medical insurance reimbursement or compete with public hospitals for resources and patients; this is one dimension. Only after that should one consider whether the business model is easily replicable to achieve chain-based scalability.”

When evaluating an investment target, considerations generally span two dimensions: single-site operations and chain networks. Even a standalone clinic, though small in scale, encompasses all essential functional components. Liu Zeyuan of China Renaissance Capital noted, “For single-site operations, key metrics include the ramp-up period of individual stores and return on investment, which must meet certain operational and financial benchmarks. For chain networks, evaluation focuses on regional distribution, standardization levels, and economies of scale.”

In a nutshell, from an investment perspective alone, a prominent characteristic of high-quality healthcare service entities is their strong counter-cyclical resilience and robust profitability. If they can achieve the scale of institutions such as Amcare, Wuhan Asia Heart Hospital, and Sanbo Brain Hospital, they will attract ample capital attention. However, whether for clinics or hospitals, attracting and retaining patients to achieve profitability requires systematic operations, centered on a set of key factors: market size, conversion capability, patient retention, and repeat visits.

The choice of promising tracks and niche segments determines the size of the market capacity. The design of products and services dictates the strength of conversion capabilities. Optimization of medical processes and efficiency improvements determine patient retention. Physician quality and brand operational capabilities ultimately drive patient repurchase. This constitutes a comprehensive, integrated strategy in which every element is indispensable.

Regarding the future momentum of the healthcare services sector, Liu Zeyuan from iCapital told reporters: “Overall, the healthcare services industry is trending toward recovery, but it is exhibiting a polarized pattern. Early-stage companies that relied on concepts and whose valuations were mismatched with their profits are facing an awkward predicament. In contrast, leading enterprises with strong revenue streams and sustained profitability continue to attract significant investor interest and remain highly sought after.”

Daotong Investment has long maintained a bullish outlook on the healthcare services sector. “The healthcare services industry is relatively resilient to economic cycles, with limited downside risk,” said Lin Zhencheng, Investment Director at Daotong Investment. “Healthcare services constitute the foundational infrastructure of the broader health and wellness industry, as all medical technological innovations ultimately require physical healthcare service entities to facilitate their commercialization and implementation. Therefore, while we closely monitor high-risk innovative technologies, we consistently allocate a certain proportion of our capital to healthcare services projects. Our ultimate goal is to establish an ecosystem-wide portfolio that generates synergistic effects among our invested companies.”

What Are the Characteristics of Listed Companies with Profits Exceeding RMB 100 Million?

In the healthcare services sector, two unavoidable benchmarks in the secondary market are Aier Eye Hospital and Topchoice Medical. Understanding their business models and latest developments offers insights into the industry’s stature and future trajectory.

According to Topchoice Medical’s 2019 semi-annual report, the number of dental outpatient visits reached 1 million. Its operating revenue amounted to RMB 847 million, a year-on-year increase of 24%; the net profit attributable to shareholders of the listed company was RMB 208 million, representing a year-on-year growth of 54%.

Summarizing its model, we can characterize it as the persistent adherence to a “Regional General Hospital + Branch Hospitals” development framework and a group-based replication strategy. Key initiatives include building the “Topchoice Doctor Group,” continuously implementing the CM team-based diagnosis and treatment model, comprehensively advancing the “Dandelion” chain expansion plan, participating in investments in the broader health industry, and sustaining the company’s innovative growth. By establishing academic flagship clinics, addressing physician-related challenges, enhancing service quality, and strategically investing in new enterprises, the company ultimately forms a chained network layout—a progressive and step-by-step development logic.

Aier Eye Hospital’s 2019 Semi-Annual Report shows that it achieved an operating revenue of RMB 4.749 billion, a year-on-year increase of 25.64%; a net profit of RMB 731 million, a year-on-year increase of 33.6%; and a net profit after deducting non-recurring gains and losses of RMB 695 million, a year-on-year increase of 31.93%. Its current business model features a further improved tiered chain system and the gradual implementation of multi-level ophthalmic medical services. While accelerating the construction of its medical network system, Aier Eye Hospital is actively integrating with the international industrial ecosystem to promote clinical translation and innovation in ophthalmology and visual science.

Furthermore, in August, Hillhouse Capital and Temasek jointly invested in Aier Eye Hospital. Hillhouse Capital had previously become a shareholder of Aier Eye Hospital through secondary market investments and subscribed to 37.1818 million shares of Aier Eye Hospital at an amount of RMB 1.026 billion during the company’s first private placement since its listing in 2018, ranking sixth among the company’s shareholders. Upon completion of this equity transfer, Hillhouse Capital will hold a 2.57% stake, becoming the fifth-largest shareholder of Aier Eye Hospital.

In October, Aier Eye Hospital Group issued an announcement stating its intention to acquire 28 ophthalmic hospitals from CITIC Industrial Fund and Zhongsheng Pharmaceutical. The tripartite cooperation among Aier Eye Hospital Group, CITIC Industrial Fund, and Zhongsheng Pharmaceutical demonstrates the accelerating trend of capital converging toward leading enterprises.

According to incomplete statistics, the companies that have gone public this year include Jinxin Fertility, EuroEyes, and United Family Healthcare. In addition, Pengai Medical is set to list on the Nasdaq this month, bringing the total to four.

In June, Jinxin Fertility Group was listed on the Hong Kong Stock Exchange. The group owns three major assisted reproductive technology centers, including Chengdu Xinan Hospital, Shenzhen Zhongshan Urology Hospital, and HRC Fertility in the United States. According to a Frost & Sullivan report, Jinxin Fertility ranked third in China’s assisted reproductive services market in 2018, performing 20,958 in vitro fertilization (IVF) oocyte retrieval cycles, with a market share of approximately 3.1%.

Jinxin Fertility’s revenue is primarily derived from the provision of assisted reproductive services, management services, and ancillary medical services. From 2016 to 2018, Jinxin Fertility’s revenues were RMB346.4 million, RMB662.8 million, and RMB922.0 million, respectively, while its profit and total comprehensive income for the same periods amounted to RMB103.7 million, RMB198.6 million, and RMB212.1 million, respectively.

In July, TPG, a global leader in alternative assets, announced that it would sell its equity stake in United Family Healthcare (UFH) to New Frontier Health Corporation. Under the agreement, New Frontier Health will acquire UFH from existing shareholders, including TPG and Fosun Pharma. Following the acquisition, the company will become one of China’s largest listed integrated private healthcare providers. The enterprise value of the company is estimated at approximately $1.44 billion upon completion of the transaction. After the acquisition, New Frontier Health Corporation will be renamed “New Frontier Healthcare Group” and will continue its commitment to delivering high-quality, comprehensive healthcare services in China, with future plans for sustained growth through organic expansion and strategic acquisitions.

United Family Healthcare is one of the few private comprehensive healthcare providers in China with nationwide coverage. It offers lifecycle-spanning medical services centered on general practice, including primary care, family medicine, pediatrics and obstetrics, gynecology, in vitro fertilization (IVF), surgery, orthopedics, oncology, and more. Its service portfolio encompasses primary care, health check-ups and preventive care, consultations, diagnostics, treatment, surgical services, as well as patient-centered management of chronic and acute conditions. As of August, it operated nine hospitals (two under construction) and 14 clinics across four first-tier cities and a number of second-tier cities.

In October, EuroEyes was listed on the Hong Kong Stock Exchange. EuroEyes officially entered China in 2013, with its first clinic established in the Jin Mao Tower in Shanghai. In just six years, EuroEyes Eye Hospital became the first German ophthalmology company to be listed in Hong Kong.

EuroEyes experienced a period of rapid revenue growth in the mainland China market over the past three years. From 2016 to 2018, its compound annual growth rate (CAGR) reached 79.6%, with revenue increasing from €3.76 million in 2016 to €12.11 million in 2018. Meanwhile, its contribution to the Group’s total turnover rose from 12.4% in 2016 to 28.2% in 2018, approaching half the level of the German market.

Recently, Pengai Medical released its prospectus and is scheduled to list on the Nasdaq on the 25th of this month. The prospectus indicates that Pengai Medical was founded in 1997 and is currently positioned as a leading medical aesthetics service provider in China. The Group currently operates 21 medical aesthetics centers (19 of which are wholly owned or majority-controlled), spanning mainland China, Hong Kong, and Singapore.

In terms of financing, from 2011 to 2018, Peng Ai Medical received equity investments from Andafu Capital, IDG, and Shanghai Chuangrui Investment (SCI). With the support of capital, Peng Ai achieved leapfrog development from 2016 to 2019.

Pengai Medical’s revenues in 2016, 2017, and 2018 were RMB 585 million, RMB 697 million, and RMB 761 million, respectively, with revenue of RMB 393 million in the first half of this year. The Group recorded a profit of RMB 50.53 million in 2016, but incurred losses of RMB 72.43 million and RMB 253 million in 2017 and 2018, respectively. From 2016 to 2018, its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) amounted to RMB 96.06 million, RMB 112.1 million, and RMB 113.1 million, respectively. In the first half of this year, the Group’s profit reached RMB 80.2 million, representing a year-on-year increase of 374%.

Based on the above analysis, it is evident that these enterprises are primarily concentrated in the fields of dentistry, ophthalmology, and obstetrics, gynecology, and pediatrics. This aligns with the previously discussed strategy of selecting specific sectors first and then establishing a scalable group-based chain model. These companies target mid-to-high-end self-paying and insured patients, excluding those reliant on public medical insurance reimbursement. They have built medical teams ranging from core experts to attending physicians, covering all key specialties. By earning patient trust through high-quality care and superior service experiences, they demonstrate significant advantages in both replicability and average revenue per user (ARPU).

High-end healthcare, represented by United Family Healthcare (UFH), is relatively unique. The premium market for expatriates constitutes a somewhat segmented niche. In theory, high-end providers can avoid direct competition with public hospitals and operate independently of national medical insurance, thereby carving out their own specialized market segment. UFH’s success has validated this approach.

Compared with companies that have the concept of "Internet healthcare," physical hospitals and clinics are not so high in valuation and attention. However, top-tier enterprises with revenues of 1 billion yuan or more and profits of 100 million yuan or more, although extremely rare, are undoubtedly "hot cakes."

Specifically for enterprises, the healthcare services industry has transitioned from a phase of unregulated growth to one characterized by market-driven survival of the fittest. The companies that ultimately survive will be those demonstrating excellence in key areas such as building high-quality physician teams, leveraging digital tools for clinical decision support, standardizing medical processes, delivering patient-centric experiences, optimizing disease-specific and departmental structures, refining pricing and strategic decision-making, reducing supply chain costs, and optimizing labor costs.

Against the backdrop of an aging population, consumption upgrading, and the nation’s new healthcare reforms, enterprises that prioritize “endogenous” growth and have restructured their expansion and operational models will establish new competitive barriers.

New Healthcare Services and Chain Business Models

According to multiple investors and corporate representatives, the overall strategic layout of companies in the healthcare services market during the second half of 2019 was characterized by contraction and a conservative approach. Rather than pursuing large-scale expansion driven solely by capital as in the past, companies focused on strengthening internal capabilities and optimizing the operations of individual facilities and regional markets.

Against the backdrop of continuous major healthcare reforms, pharmaceutical companies, medical device manufacturers, pharmaceutical distributors, and even medical payment and health insurance sectors have all undergone significant transformations and restructuring. In contrast, the healthcare services sector has long been perceived as engaging in a “quiet struggle,” yet subtle changes are already underway. Driven by the industry’s pain points, resources and business models are being restructured. The following are several observable trends:

First, expand departmental and population coverage to deepen service depth and broaden service boundaries.It goes without saying that new high-demand specialties have been added to deepen service offerings and reach a broader patient population, such as expanding from pediatrics to gynecology, from obstetrics and gynecology to higher-margin assisted reproductive technologies, from pediatric care to adult medicine, and from clinics to hospital construction.

This July, Zhibei Medical completed a tens-of-millions financing round led by Irong Capital, upgraded its brand, and announced two major enhancements. The first is the upgrade of multi-disease pediatric diagnosis and treatment services. Zhibei has gradually expanded its range of pediatric diagnostic and therapeutic offerings. In addition to its existing departments of general pediatrics and child healthcare, it has added specialized clinics for various chronic childhood conditions, such as the Pediatric Wheezing Clinic, Pediatric Height Management Clinic, Pediatric Rhinitis/Sinusitis Management Clinic, Day Treatment Clinic for Neonatal Jaundice, Pediatric Hip Dysplasia Screening Clinic, Pediatric Immunization Clinic, Pediatric Behavioral Development Clinic, and Pediatric Optometry and Vision Care.

Second, the upgrade of adult diagnostic and treatment services. Zhibei Dermatology has expanded its offerings to include photoelectric medical aesthetics and injectable medical aesthetics, and will place greater emphasis on long-term follow-up management for chronic diseases in the future. In addition to its existing pediatric oral preventive care services (oral health consultations, fluoride varnish application, and pit and fissure sealing), Zhibei Dentistry has developed a clearer business plan for pediatric dental treatment services. The services currently offered by Zhibei include: frenectomy, 3M resin fillings for primary teeth, root canal therapy for primary teeth, crown restoration for primary teeth, simple extraction of primary teeth, extraction of impacted and unerupted teeth, treatment of dental trauma, and early orthodontic intervention for children.

YuXueYuan’s Beijing Honghe Obstetrics and Gynecology Hospital officially opened in September. The hospital features multiple departments, including gynecology, obstetrics, pediatrics, internal medicine, surgery, and dentistry, with a focus on women’s reproductive health and children’s health management. It provides a series of high-quality, continuous medical services covering preconception care, pregnancy, childbirth, postpartum recovery, and parenting.

In its future services, Honghe Obstetrics and Gynecology Hospital, building on the longstanding professionalism and distinctive service model of Yu Xueyuan, remains steadfastly committed to women’s reproductive health and comprehensive child health management. With “integrated obstetrics, gynecology, and pediatrics” as its hallmark, the hospital fully promotes the concept of “Joyful Pregnancy” to achieve integrated health management during the “First 1,000 Days of Life.”

Second, model empowerment to enhance efficiency and reduce costs.The chain model is capital-intensive, particularly in specialized healthcare, which requires establishing offline clinics or hospitals. This entails significant investment and a prolonged ramp-up period. New outlets must address numerous challenges, such as identifying regional markets suitable for the intended service offerings, understanding local consumer preferences, navigating local market competition, negotiating acceptable lease terms (including optimal rent levels), recruiting, training, and retaining medical staff, successfully integrating new facilities into existing control structures and operational systems (including information technology systems), and securing financing or maintaining sufficient capital for new facility investments or acquisitions.

In the dental sector, leading national chains are piloting a new Dental Support Organization (DSO) model. This approach provides dentists and clinics with non-clinical support in administrative and operational management, offering comprehensive management solutions encompassing brand building, operations, dentist training, centralized supply chain procurement, management, and strategic support, and even extending to equity investment and holding.

Meiwei Dental, Huanle Dental, and Malo Clinic are all leveraging this new model to empower their operations and compete in the dental care sector. This marks a shift from merely expanding the number of clinics to focusing on management and brand output. By serving dentists and clinics with innovative work platforms, and by integrating supply chain, informatization, and digitalization services from emerging healthcare enterprise service providers, these companies are collectively helping to improve efficiency and reduce costs. This could signal the true beginning of the healthcare services industry’s transition toward “value-based healthcare.”

Furthermore, Taikang Bybo Dental’s strategic approach aims to validate the “payment + service” model. Taikang promotes the development of dental insurance, bringing customers and payment solutions to major dental chains, thereby unlocking the dormant oral health market.

Third, integrating asset-light and asset-heavy models with online-offline synergy to share core medical resources.Two core challenges have long plagued practitioners in the healthcare services sector: one is customer acquisition and traffic generation, and the other is training, retaining, and serving physicians. The latter, in particular, is of paramount importance to the healthcare industry. A typical approach involves creating an online-offline integration to serve physicians and share medical resources.

As China's leading online-to-offline (O2O) integrated healthcare services group, Penguin Almond has onboarded 450,000 contracted and certified physicians, established close collaborations with 57 prominent physician groups across various specialties, served over 10 million members, processed more than 100,000 monthly service orders on its platform, and connected with over 30,000 hospitals.

In terms of offline resources, Penguin Almond has built a leading-scale network of offline clinics, encompassing various formats such as general practice clinics, specialty clinics, surgical centers, and infirmaries. Currently, its 48 offline locations cover eight cities: Beijing, Shanghai, Guangzhou, Shenzhen, Shenyang, Nanjing, Hong Kong, and Chengdu. Meanwhile, facilities in Xi’an, Chongqing, Hangzhou, Wuhan, and other cities are under preparation and will soon commence operations.

As of October 2019, Penguin Almond had provided high-quality online-to-offline (O2O) medical services to more than 10 million patients. Among these services, a total of 502 physicians performed procedures at its shared ambulatory surgery centers, successfully completing over 10,600 surgeries.

It has been reported that there is a significant shortage of qualified physicians in the medical aesthetics sector. United Lige Second Hospital, a leading chain brand in this field, has established a shared surgical center. This asset-light business model for physician services enables faster growth and allows the company to capture the core healthcare service market from a strategic flank. Meanwhile, by partnering with the Meidaifu online platform, the hospital aims to build a more effective doctor-patient communication channel and enhance user stickiness.

Fourth, brand positioning in niche blue-ocean sectors, with continuous optimization of the user experience.In China’s healthcare services market, brand positioning and marketing have long been in an awkward position, characterized by polarization: on one hand, some enterprises lack brand awareness, while on the other, consumer healthcare sectors such as medical aesthetics and dentistry suffer from excessive marketing.

In emerging "blue ocean" sectors such as pediatric dentistry, rehabilitation, ENT and ophthalmology, and aesthetic dermatology, there remains significant room for improvement in patient education. By offering segmented and precise positioning while ensuring the quality of medical services and patient experience, providers can effectively capture their target customer base.

Jicheng Dental has introduced gamified dental care to make dental visits enjoyable for children. Jicheng’s advantage also lies in its pursuit of customer experience, transforming children’s perceptions of oral healthcare and treatment through the concept of “happy dental visits.”

Youfu is dedicated to sports medicine, musculoskeletal rehabilitation, and the diagnosis and treatment of orthopedic conditions, providing professional medical services to sports enthusiasts, orthopedic patients, postoperative individuals, and those in a sub-health state.

Youfu Clinic was the first in China to propose the concept of "holistic care," centered on the principle of "quality medical treatment, quality rehabilitation." Holistic care aims to help individuals with health needs find the most appropriate therapeutic interventions. This approach advocates viewing patients as whole persons, rather than merely addressing specific lesions through surgical means.

The aforementioned examples represent only the tip of the iceberg of new models in the healthcare services sector. Across the entire healthcare services landscape, institutions that typically achieve strong performance are either specialized providers in consumer-driven medical segments—such as dentistry, medical aesthetics, health screenings, obstetrics and gynecology, and ophthalmology—or those addressing essential, high-demand clinical needs, including cardiology, oncology, neurology, pediatrics, and rehabilitation.

Consumer healthcare enterprises must undoubtedly make exceptional efforts on both the supply and demand sides to validate their business models. In addition to possessing certain medical resources, these institutions must also implement robust marketing strategies, as demand is neither entirely inelastic nor constant; strong measures in marketing and operational services are essential for success.

For specialty healthcare providers addressing essential needs, the overall market faces a supply-demand imbalance, which is particularly evident in pediatrics, rehabilitation, and oncology. However, securing supply-side resources remains challenging: there is a general shortage of certain professionals, such as pediatricians, while core resources in fields like oncology and neurology are predominantly concentrated within public institutions. Therefore, building robust reserves of medical resources is key to achieving competitive advantage.

In summary, healthcare service enterprises must innovate their business models and restructure resources in both clinical and non-clinical management and operations, while continuously optimizing internal processes, to achieve competitive advantage in the industry.

Adopting a contraction strategy, optimizing existing resources, improving efficiency and reducing costs, strengthening internal capabilities, deepening regional presence, and expanding nationwide—this may well be the most accurate portrayal of many clinics and hospitals in 2019.

References and Related Materials:

Annual Revenue Nears RMB 800 Million, 21 Stores: Pengai Medical to List on NASDAQ

China's Healthcare: Two Decades of Turbulence—Struggle and Innovation Amidst Macro Trends

900 Clinics, Heavy Investment from KKR: Has the Dental Chain Model Proven Successful in the U.S.?