2019 Public Hospital Operation Report Released: Tertiary Hospitals Report Negative Surplus for the First Time, Urgent Need for DRG Implementation

The content and data cited in this report are authorized by Beijing Neusoft Wanghai Technology Co., Ltd. Reproduction without permission is prohibited.

On October 20, 2019, the Global Hospital Lean Operations Forum themed “Intelligent Transformation” and the 2nd HIA International Big Data Summit were held in Qingdao, Shandong Province. Numerous industry experts convened to engage in in-depth discussions on topics such as big data, Diagnosis-Related Groups (DRG), value-based healthcare, and lean hospital operations management under the context of healthcare reform. As one of the highlights of the conference, the “2019 HIA Hospital Operations Analysis Report” was officially released at the forum.

DRGs Will Drive the Healthcare System’s Transition to Value-Based Care

Professor Guo Qiyong, Director of the Institute of Hospital Management at China Medical University and Dean of the Neusoft Wanghai Product and Data Research Institute, first provided an interpretation of DRG and value-based healthcare at the forum that day.

Professor Guo Qiyong, Director of the Institute of Hospital Management at China Medical University and Dean of the Neusoft Wanghai Product and Data Research Institute

According to Deloitte’s “2019 Global Health Care Outlook” report, the annual growth rate of global health care expenditure was 2.9% from 2013 to 2017, and is projected to rise significantly to 5.4% from 2018 to 2022. By then, global health care spending in 2022 is expected to reach $10.059 trillion (i.e., $1,005.9 billion). Meanwhile, government spending on health care is declining. According to forecasts by The Economist, the share of global health care expenditure in GDP decreased from 10.3% in 2015 to 10.1% in 2019.

As China rapidly transitions into an aging society and experiences declining birth rates, the growth rate of active employees has fallen below that of retirees in most years in recent times. The basic medical insurance system has long faced a structural deficit, with expenditures outpacing revenues, resulting in significant financial pressure. Although the government has consistently increased healthcare spending—raising the national fiscal budget for healthcare from RMB 319.1 billion in 2008 to RMB 1.5291 trillion in 2018, and increasing the share of healthcare expenditure in total fiscal spending from 5% in 2008 to 7.3%—it is an indisputable fact that the basic medical insurance fund remains in deficit.

Taking Liaoning Province as an example, in 2018, only Shenyang and Dalian among its 14 prefecture-level cities maintained a balance in their medical insurance funds, while the remaining 12 cities experienced deficits after November. In fact, this situation reflects the current reality in more than half of China’s regions.

For this reason, Diagnosis-Related Groups (DRG) have garnered increasing attention over the past two to three years. Unlike traditional payment models, DRG implements diagnosis-based reimbursement. This shift in payment methodology will drive changes in clinical practice, requiring healthcare institutions to reduce medical costs while ensuring quality of care in order to achieve better financial outcomes.

Professor Guo Qiyong believes that the implementation of DRG will drive the transformation of the healthcare system from a traditional model to a value-based care model, thereby meeting the needs of three key stakeholders: national regulatory authorities, payers (government or insurance companies), and healthcare institutions.

First, the operation of medical institutions will become more lean. The core of DRG implementation is clinical pathways, which can standardize and engineer medical processes, thereby enabling hospitals to better control costs. The efficient operation of hospitals can enhance performance, ensuring that medical staff receive due compensation for their efforts.

For payers, DRGs enable more precise control over cost settlement, ensuring payment is made only for effective treatment pathways and medications. This does not imply that payers should indiscriminately reduce payments; rather, it emphasizes the rational and efficient use of funds to guarantee sustainable operations while maintaining cost controllability.

For China, where basic medical insurance is predominantly government-funded, DRG can effectively mitigate the significant waste and deficits plaguing the system. For commercial insurers, the implementation of DRG provides a basis for developing more targeted insurance products, thereby promoting the growth of the commercial insurance sector.

For government health agencies represented by the National Health Commission, Diagnosis-Related Groups (DRG) can address issues in healthcare quality control, thereby providing better medical services to the public. The refinement of clinical pathways helps improve healthcare quality, while the diagnosis-based payment model incentivizes healthcare institutions to enhance their care standards. In regions where DRG has already been implemented, regulatory authorities require healthcare institutions to bear the costs of readmission or retreatment within a specified period. Under such circumstances, healthcare institutions have strong incentives to improve healthcare quality.

In the traditional healthcare system, the interests of the three parties are not aligned; whereas in the value-based healthcare system, government health agencies, payers, and healthcare providers have reached a consensus on cost reduction, possessing both the incentive and the means to identify therapeutic outcomes that matter most to patients, thereby ensuring patient benefit.

As the central vehicle for value-based healthcare, hospitals’ core competitiveness will lie in their ability to reduce operational costs through lean operations within the new system, thereby achieving sustainable operations at the most appropriate cost while ensuring that service quality does not decline. Data drives value-based healthcare. Professor Guo Qiyong stated that hospitals need to implement data analytics in the future, improve processes based on data, and adjust personnel structures to successfully deliver value-based healthcare.

Meanwhile, Professor Guo Qiyong also emphasized that physicians should conduct diagnosis and treatment with a patient-centered and disease-centered approach, rather than adopting a DRG mindset that views medical care solely from a cost perspective. In the clinical process, it is essential to select the most effective treatment options that best benefit the patient, while simultaneously taking into account diagnosis-related group (DRG) payment systems to avoid overtreatment.

DRGs cannot cover all diseases; only a certain proportion of common and frequently occurring conditions can be managed using the DRG model. For instance, during the spring peak season for influenza, determining the cost of treatment and the reimbursement rate requires large-scale statistical analysis to draw scientific conclusions. This approach facilitates more refined management of medical insurance and ensures more effective national investment.

In addition to healthcare institutions needing to shift their mindset, Professor Guo Qiyong believes that patients also need to change their thinking. People should pay more attention to their health, rather than waiting until they are critically ill, as is often the case now. A typical example is the sharp increase in hospital admissions for acute pancreatitis after long holidays; if patients exercised modest dietary control, such occurrences could be significantly reduced.

From the perspective of value-based healthcare, the largest portion of most people’s lifetime medical expenses is incurred during end-of-life care. Initially, patients may have been responsible for paying 90% of these costs out-of-pocket. Following healthcare reforms, this proportion has decreased significantly, but it still remains at approximately 50%. For the majority of individuals, such treatments are part of a painful process and offer limited clinical value. Shifting the paradigm to redirect these expenditures toward disease prevention and health maintenance would yield greater value and substantially improve quality of life.

Proactive prevention and regular health screenings are more effective than reactive measures. Only by raising individual health awareness and increasing understanding of healthcare expenditures can societal health be ensured.

Interpretation of the “2019 HIA Hospital Operations Analysis Report”: Tier-3 Grade-A Hospitals Record a Negative Surplus for the First Time

Since 2015, Neusoft Wanghai has annually produced and released the Hospital Operations Analysis Report. Drawing on 16 years of continuous experience in hospital management and operations, and leveraging extensive, detailed operational data from hospitals, the report incorporates insights from senior experts to conduct multi-level, multi-dimensional analyses and summaries of hospital operations for the year. It serves to support hospital operational management and offers significant reference value. With the establishment of the Health Information Alliance (HIA) in early 2019, this analysis report will continue to uphold the alliance’s philosophy of “Sharing, Innovation, and Development” to empower its members.

Professor Guo Qiyong provided an interpretation of the “2019 HIA Hospital Operations Analysis Report.” The report analyzed the current state of hospital operations in China based on statistical data from previous years published by the National Health Commission.

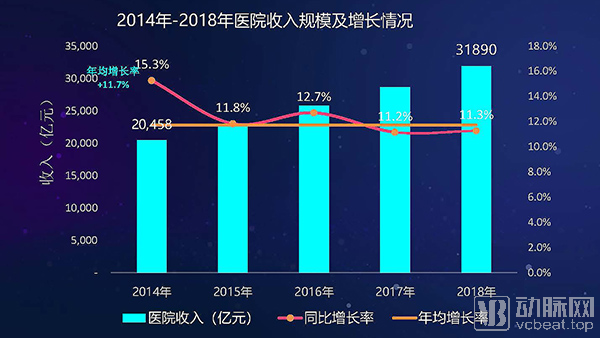

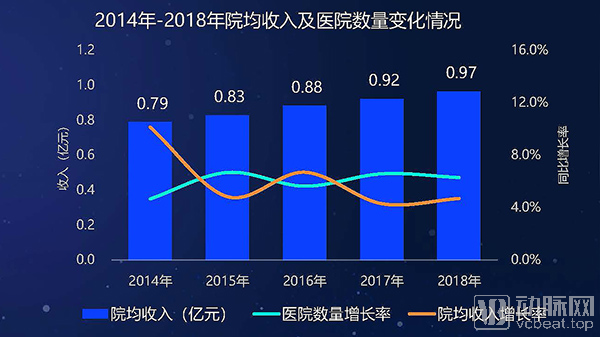

From 2014 to 2018, the overall revenue scale of hospitals in China maintained rapid growth, with an average annual growth rate of 11.7%. However, this growth rate has shown a slowing trend in recent years. The total number of hospitals has continued to grow steadily, exceeding 30,000 in 2018. The growth in average revenue per hospital has also slowed, with its increase in recent years being lower than that of the number of hospitals.

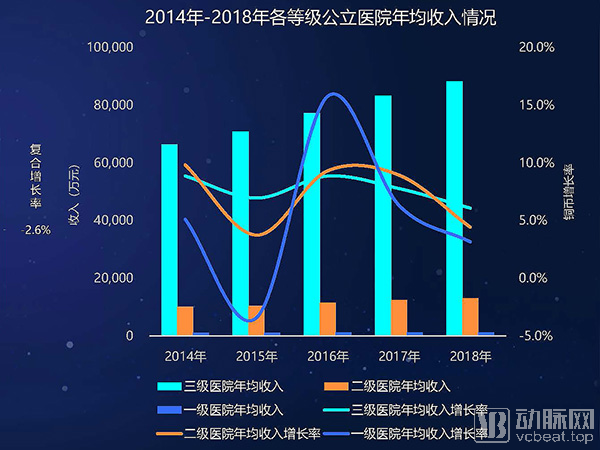

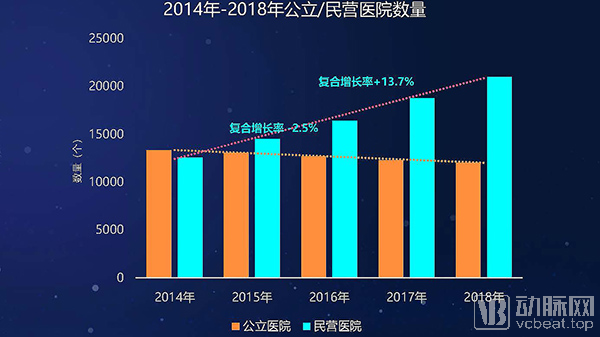

Comparison of Revenue Scale Between Public and Private Hospitals: The total number of public hospitals has been decreasing year by year in recent years, with an average annual decline rate of 2.6%. The revenue growth rate of hospitals at all levels has slowed down, with the growth rate in 2018 being around 5%.

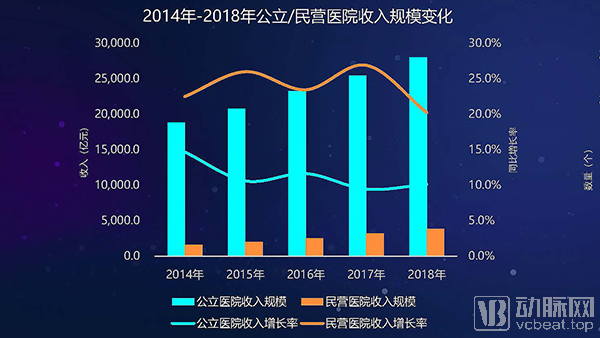

In recent years, the revenue of public hospitals has been significantly higher than that of private hospitals; however, the share of public hospital revenue has declined year by year, falling below 90% in 2017, with its growth rate maintaining at around 10% in recent years. As policies for socially operated medical institutions have shifted from equal treatment to preferential support, private hospitals have achieved rapid development in recent years, particularly exhibiting a faster growth rate in total revenue scale, with a compound annual growth rate (CAGR) of 24.7%.

Overall, in 2019, the total revenue of hospitals grew rapidly. While the number of public hospitals declined, their total revenue increased; meanwhile, both the number and total revenue of non-public hospitals exhibited rapid growth.

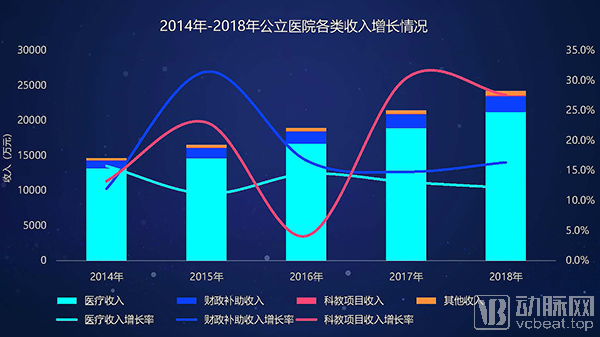

In terms of revenue composition, public hospitals have experienced rapid annual growth in medical service revenue in recent years, with the growth rate remaining above 10%. However, the proportion of fiscal subsidy revenue has been increasing year by year. The growth rate of fiscal subsidies rose from 7.7% in 2014 to 9.5% in 2018, surpassing the growth rate of medical service revenue. Additionally, revenue from scientific research and education projects saw a significant increase in 2017.

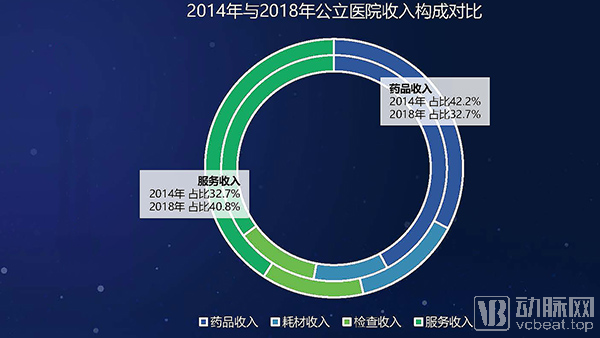

Over the past five years, service revenue in public hospitals (the portion of medical income excluding revenue from pharmaceuticals, consumables, and diagnostic tests/examinations, primarily comprising treatment, surgical, and nursing revenues) has experienced substantial growth. In 2018, service revenue surpassed pharmaceutical revenue, reaching RMB 86.55 million and accounting for 40.8% of total revenue. Although the absolute volume of consumable revenue remains relatively low, its proportion is rising rapidly; in 2018, consumable revenue grew by 19.7%, marking the fastest growth rate among all revenue categories.

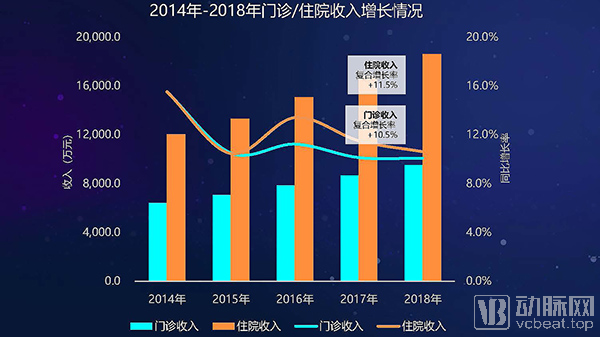

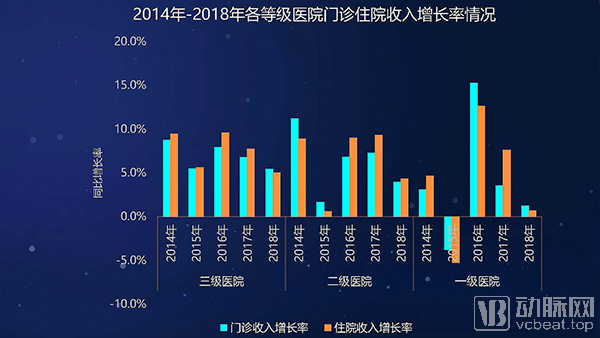

Among hospitals’ average annual medical revenue, the ratio of outpatient revenue to inpatient revenue remains balanced, with inpatient revenue growing slightly faster than outpatient and emergency revenue in recent years. This pattern—faster growth in inpatient revenue than in outpatient revenue—is also observed across public hospitals of all tiers.

Since 2016, the growth rate of outpatient revenue in secondary hospitals has increased significantly, while that in tertiary hospitals has declined. Professor Guo Qiyong believes this reflects the success of national policies regulating tiered diagnosis and treatment, with a substantial increase in outpatient visits at community health centers and secondary hospitals, and a relative decrease at tertiary hospitals.

In many Chinese cities, basic medical insurance does not cover outpatient expenses, with reimbursement available only for inpatient care. This is one of the primary reasons for the rising proportion of inpatient revenue in hospitals’ total income.

In 2018, the revenue of general hospitals exceeded RMB 200 million, with a compound annual growth rate (CAGR) of 10.9%. The revenue of specialized hospitals has grown rapidly in recent years, surpassing that of traditional Chinese medicine (TCM) hospitals. Among these, aesthetic medicine, rehabilitation, ophthalmology, and dental hospitals all achieved CAGRs exceeding 20%, while cardiovascular hospitals also witnessed substantial revenue growth over the past few years. Affected by the continued decline in birth rates, the revenue growth of obstetrics and gynecology hospitals has slowed significantly compared to previous years.

In a cross-regional comparison, Guangdong Province has long led the nation in revenue scale of medical institutions, with its fiscal subsidy revenue also experiencing rapid growth. Provinces ranking high in revenue scale, such as Zhejiang, Jiangsu, and Shandong, have maintained an average annual growth rate of over 10% in recent years.

Professor Guo Qiyong believes that this indicates increased government investment in healthcare and medical services in these regions. Only by developing the regional economy can social development issues and healthcare challenges be resolved. Development is the absolute principle.

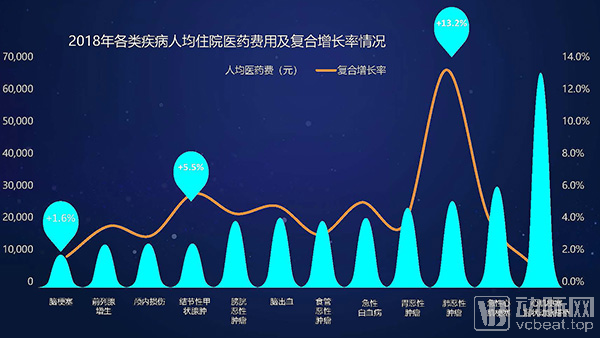

An analysis of changes in average per-capita inpatient medical costs across various diseases reveals that costs for myocardial infarction and coronary artery bypass grafting have remained persistently high, although the rate of cost growth has been gradually slowing. Malignant neoplasms exhibited the highest compound annual growth rate (CAGR) in average per-capita inpatient medical costs, reaching 13.2%. Notably, in 2018, the year-on-year increase in average per-capita inpatient medical costs for gastric and esophageal malignancies was less than 1%. Conversely, average per-capita costs for conditions such as cerebral infarction and lumbar disc herniation declined, indicating that the elimination of drug markups has impacted costs for a range of diseases.

Based on data shared by the HIA Alliance, the report also provides a comprehensive and detailed statistical analysis of hospital costs. Several conclusions were drawn: In terms of personnel expenses, labor costs in surveyed tertiary hospitals have surpassed pharmaceutical costs to become the primary cost driver, although they are showing a downward trend. This is attributed to the implementation of tiered diagnosis and treatment, which has led to an increase in service volume at secondary hospitals, thereby driving up their demand for medical talent.

Due to the continuous restrictions on drug prices imposed by national policies, the growth rate of drug costs in tertiary hospitals has slowed down; drug costs in secondary hospitals have also remained stable over the past two years. Overall, the proportion of drug costs continues to decline.

However, Professor Guo Qiyong also believes that as the state gradually requires all secondary hospitals to implement targeted therapy drugs, and even further extends this practice to community hospitals in the future, the proportion of drug costs may increase.

The cost of medical consumables at surveyed hospitals has shown a trend of rapid growth; however, the proportion of medical consumables in tertiary hospitals has stabilized.

After reconciling hospital revenues and costs, the report reveals a stark fact: the surveyed tertiary hospitals recorded a negative balance for the first time in 2018, indicating they were operating at a loss.

Given the severity of the current situation, the implementation of Diagnosis-Related Groups (DRG) is imminent. China has designated 30 cities as pilot sites. Following a three-step approach of “top-level design, simulation testing, and actual payment,” the initiative aims to ensure the completion of tasks at each stage, with simulated operations launched in 2020 and actual payment implementation commencing in 2021.

All images are sourced from the HIA report. For further information, please contact the HIA Alliance.

https://www.chinahia.com/#/home