Digital Health Sees a New IPO Surge: Five Companies Reveal Key Industry Trends

Yuanxin Technology

Internet Medical Service Provider

Weimai

Digital Health Service Platform Provider

Medlinker

Chronic Disease Management Platform Provider

PINGAN GOOD DOCTOR

Internet Medical Health Platform

In 2019, after three years of stagnation, the U.S. digital health sector saw a resurgence, with five companies completing their initial public offerings (IPOs) this year.

Digital healthcare applies modern computer and information technologies to medical processes, addressing issues of cost and service efficiency within healthcare systems. The United States entered the digital healthcare sector relatively early. Since 2012, a large number of digital healthcare companies have gone public, including telemedicine provider Teladoc, healthcare advisory services firm Evolent Health, healthcare communications system provider Vocera Communications, health information company Castlight Health, cloud-based intelligent clinical operating system supplier NantHealth, and digital health media company Everyday Health. However, the IPO boom subsided after 2016, until this year, when five digital healthcare companies broke the deadlock.

Among the five companies that went public this year, closing data from October 23 (U.S. time) showed that the stock prices of Change Healthcare, Phreesia, and Health Catalyst remained stable or rose, while those of Livongo and Peloton fell by more than 20%. This mixed performance indicates that although the new wave of IPO enthusiasm has brought surprises to the industry, corporate performance in the capital market still requires further business progress to sustain it.

In China, the corresponding sectors of internet healthcare and mobile healthcare have entered a phase of rapid development since 2014. After exploring various business models, a number of unicorn companies have emerged, with many enterprises reaching Series C and Series D funding rounds. In the past two years, numerous guiding and regulatory policies have been successively introduced, bolstering confidence in the industry. However, among domestic companies, only PINGAN GOOD DOCTOR has completed an initial public offering (IPO).

So, why were these five companies able to break the deadlock and successfully complete their IPOs? What insights can they offer to domestic enterprises? VCBeat (WeChat ID: vcbeat) provides an analysis based on data from multiple sources.

Let’s first take a look at the basic profile of each company:

Basic Information of Five Listed Companies; Latest Stock Prices Are Closing Prices on October 23 (U.S. Time) in USD; Graphic by VCBeat

Change Healthcare is a healthcare technology company that connects healthcare providers, patients, and payers through data- and analytics-driven solutions to enhance efficiency within complex workflows. Its users include insurance companies, employers, hospitals and health systems, physicians, pharmacies, laboratories, and patients.

Phreesia is a SaaS provider. Its SaaS-based Phreesia Platform offers healthcare organizations a robust suite of solutions to manage patient intake and provides integrated payment solutions to ensure secure processing of patient payments. The platform also enables life sciences companies to engage in targeted, direct communication with patients.

Livongo is a digital health company focused on chronic disease management. It combines hardware devices, AI-driven data analytics, and professional health coaches to help individuals manage chronic conditions by providing personalized information and guidance. Its solutions include diabetes management, hypertension management, diabetes risk and weight management, and behavioral health management.

Health Catalyst is a healthcare big data company that provides data and analytics technologies and services to healthcare organizations, enabling them to achieve measurable improvements in clinical, financial, and operational performance. Its solutions include cloud-based data platforms, analytics software, and expert professional services.

Peloton is an internet fitness company that integrates fitness equipment, web-based software, and health and wellness content through a subscription platform. It sells connected fitness devices such as stationary bikes and treadmills, and provides members with immersive workout classes via subscription.

Among these five companies, Change Healthcare, Phreesia, and Health Catalyst provide software and data analytics services to relevant institutions within healthcare systems, with a focus on technological innovation. Although Livongo and Peloton also rely on digital technologies to deliver their core functionalities, their products target consumer-end users, placing greater emphasis on business model innovation overall.

According to the closing data on October 23 (U.S. time), the share prices of three technology companies—Change Healthcare, Phreesia, and Health Catalyst—remained stable or rose compared with their IPO prices, with the highest gain reaching 46%. In contrast, the share prices of two business-model-driven companies, Livongo and Peloton, fell by more than 20%. This may be because the core competencies of technology-innovation companies are not easily replicated and deliver more direct benefits to users, whereas business-model innovation companies face easier imitation of their operations, leading to greater competition.

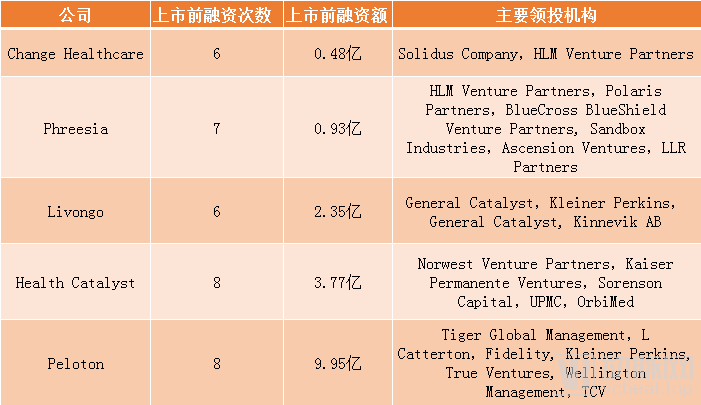

Several companies underwent numerous pre-IPO financing rounds, ranging from six to eight, with a high frequency of fundraising. For instance, Health Catalyst completed eight financing rounds over eight years, while Peloton secured eight rounds within just four years of its establishment. Once a viable business model is established, capital naturally steps in promptly to meet funding needs during the rapid growth phase.

Pre-IPO Financing of 5 Companies (Amount: USD); Data Source: Crunchbase; Chart by VCBeat

Meanwhile, repeat investments are common in the financing rounds of these companies; it is not unusual for a single institution to participate twice. Taking Health Catalyst’s investors as an example, Norwest Venture Partners participated in six out of eight funding rounds, Sequoia Capital invested four times, and Kaiser Permanente Ventures invested three times. In addition, General Catalyst and Kinnevik AB each led two funding rounds for Livongo, while Tiger Global Management led two funding rounds for Peloton. The phrase “helping them get on the horse and accompanying them for part of the journey” aptly describes these persistent investment institutions.

Another interesting phenomenon is that among Health Catalyst’s investors, its client, the University of Pittsburgh Medical Center (UPMC), also emerged. UPMC invested in Health Catalyst on two separate occasions, likely reflecting its confidence in the tangible benefits derived from Health Catalyst’s services.

The Rock Health Q3 2019 Financing Report shows that the digital health industry secured $1.3 billion in funding in the third quarter of 2019, bringing the total financing for the field to $5.5 billion for the year. This makes 2019 poised to become the second-highest funded year on record for the sector, although the number of financing events may decline. So far in 2019, there have been nine financing deals exceeding $100 million, which is roughly comparable to the record 11 large-scale financing events seen in 2018.

Based on this year’s financing trends in the digital health sector and the funding records of the aforementioned five companies, we believe that capital markets have never been stingy with investments in digital health; rather, they favor enterprises with core competitive advantages. Once these companies establish a solid footing and demonstrate sustainable business models, capital will continue to increase its commitments. When rapid corporate growth and frequent financing rounds are met with strong confidence and repeated investments from institutional investors, creating such a virtuous cycle, an initial public offering (IPO) becomes a natural progression.

What Are the Competitive Advantages of These Companies? In terms of core business and user base, Change Healthcare, Phreesia, and Health Catalyst primarily focus on B2B services, while Livongo and Peloton are mainly oriented toward B2C markets. Each company possesses distinct core competencies, which, based on information disclosed in their prospectuses, can be summarized as “letting data speak.”

Consider the following background: According to data from the U.S. Centers for Medicare & Medicaid Services (CMS), total U.S. healthcare spending amounted to $3.6 trillion in 2018 and is projected to reach $6.0 trillion by 2027, accounting for 20% of GDP.

Rising healthcare costs are driven by inefficiencies and substantial waste, partly attributable to extensive manual and time-consuming administrative processes. Research from the U.S. National Academy of Medicine estimates that approximately 30% of healthcare spending in the United States was wasted in 2018, amounting to roughly $1.1 trillion. Furthermore, a study published in the Journal of the American Medical Association (JAMA) estimated that about 27% of total healthcare waste (i.e., $300 billion) is related to administrative complexity. A significant portion of these excess expenditures is associated with complex billing procedures, non-standardized practices, and poor communication between front-office and back-office operations, leading to increased costs, errors, and inefficient use of provider time. As healthcare expenditures continue to rise, employers and healthcare systems have shifted a greater share of these costs onto patients.

In this context, leveraging data analytics and automation to address these complex, communication-deficient processes has become a critical task for cost reduction and efficiency improvement in healthcare systems, with technology companies naturally assuming this responsibility.

In their IPO prospectuses, Change Healthcare, Phreesia, and Health Catalyst all demonstrated strong performance in enhancing efficiency and reducing costs for participants in the healthcare system.

Since 2016, Change Healthcare’s clinical-based claims payment solutions have saved insurance clients over $4 billion annually, enhancing payment accuracy while improving provider satisfaction. Large national payers using Change Healthcare’s virtual card solution saved $10 million in 2017.

After using Health Catalyst’s solutions for one year, Allina Health saved up to $125 million in financial and operational improvement projects. The University of Pittsburgh Medical Center achieved $38 million in clinical, financial, and operational improvements over several years by leveraging Health Catalyst’s solutions. As previously mentioned, the University of Pittsburgh Medical Center likely invested in Health Catalyst because it witnessed tangible results.

Phreesia’s services for streamlining the admission process have directly enhanced healthcare providers’ efficiency and indirectly improved patient satisfaction, as evidenced by quantifiable data. For instance, hospitals using the Phreesia platform have reported high levels of patient approval, with satisfaction rates of 86% among users aged 18–25 and 88% among those aged 26–35.

No matter how dazzling the technology or how flashy the products, nothing is more substantive than being “useful,” especially when these enterprises deliver quantifiable, financial results.

Unlike several tech companies, Livongo and Peloton serve consumer-end users.

However, Livongo adopts a B2B2C sales model, selling its products to employers, insurance companies, government agencies, and labor unions, which then provide the products to their employees or clients. This approach facilitates rapid user base expansion and reduces customer acquisition costs. According to its prospectus, as of June 30, 2019, Livongo had secured 720 clients and served over 192,000 Livongo members with diabetes.

Peloton expands its user base by selling connected bikes, treadmills, and subscription content, while enhancing user stickiness through interactive and social features. Currently, the Peloton platform has 1.4 million members, and as of June 30, 2019, approximately 577,000 connected fitness products had been sold. Peloton’s products are expensive, with bikes priced at $2,245 and treadmills at $4,295, indicating that its loyal users possess strong purchasing power.

From this perspective, the two B2C companies have already accumulated user data at a certain scale. Precise user data signifies substantial development potential, an indicator that has always been valued by investors; consequently, they have secured greater financial support.

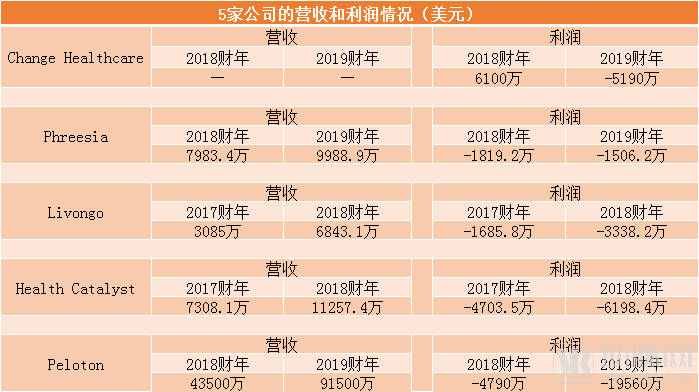

The prospectus reveals that nearly all of these companies are unprofitable. We have compiled statistics on their key financial data:

Data for the Most Recent Two Fiscal Years Disclosed in the Prospectuses of Five Listed Companies (Amount: USD); Chart by VCBeat

Change Healthcare’s core operations are conducted by its joint venture, Change Healthcare LLC, which has achieved profitability. In fiscal years 2019 and 2018, it reported net profits of $177 million and $192 million, respectively. Although Change Healthcare does not consolidate the joint venture’s financial statements and performance—thereby presenting a loss-making position—its underlying performance is in fact highly optimistic.

Furthermore, Phreesia’s losses have begun to narrow, and Health Catalyst’s loss growth has lagged behind its revenue growth, suggesting a positive trajectory. Many technology-driven companies incur high upfront R&D and marketing expenses; however, as their customer base expands, average R&D costs decline. If their solutions can deliver tangible value to clients and build strong word-of-mouth reputation, marketing expenses are also expected to decrease over the long term.

These technology companies have also outlined plans for future growth, with several common themes including: acquiring or making strategic investments in high-quality companies with complementary technological advantages; expanding their customer base and deepening collaboration with existing clients; and optimizing current products by upgrading them with new technologies.

Livongo is somewhat unique in that both its revenue and losses continue to grow. Expenditures are primarily directed toward expanding the customer base, building and operating marketing channels, covering personnel costs, and developing technological solutions—a challenge inevitably faced by high-growth, platform-level digital health companies. Livongo’s proposed solution is to intensify the “development” of existing members while increasing member enrollment, offering them more practical paid solutions and leveraging AI to enhance platform service efficiency. Additionally, Livongo plans to expand internationally to serve the vast global population of patients with chronic diseases.

Peloton is an even more unique case, with its loss-making scope expanding and the rate of increase in losses far outpacing revenue growth. This is primarily driven by high customer acquisition costs, including those associated with offline physical fitness studios. Peloton’s strategy is to enhance brand awareness and member experience to grow its membership base, maintain high retention rates, and improve the efficiency of sales and marketing expenditures.

Although unprofitable companies have all indicated that losses will persist, they are in fact standouts that have emerged through rigorous trials within the industry and market. Their technologies, products, or business models possess certain barriers to entry, making them not easily imitated or replaced by peers. Future performance will depend on the implementation of their next-phase strategies and agile market response tactics, warranting anticipation.

In China, a group of strong players has emerged in the digital healthcare sector. PINGAN GOOD DOCTOR completed its initial public offering (IPO) on the Hong Kong Stock Exchange last year, becoming the first listed digital healthcare company in China. WeDoctor completed a $500 million Pre-IPO financing round last year and has entered the final sprint phase ahead of its IPO.

As early explorers in digital healthcare, Haodaifu Online, DXY, and Medlinker are also worth watching for their IPO progress, but none of them have announced a corresponding timeline yet.

Digital health enterprises in China are growing rapidly. According to incomplete statistics, a large number of companies, including Miaoshou Doctor, Miao Health, SENYINT, and Weimai, have conducted extensive explorations focusing on different segments of the industry, with strong business performance already demonstrated. These companies also enjoy favorable financing conditions and hold significant future potential.

Miaoshou Doctor: Building an Online-Offline “Doctor-Patient-Drug-Insurance” Closed Loop

Miaoshou Doctor’s medical services span both online and offline channels. Online, the Miaoshou Internet Hospital connects doctors with patients. Offline, Yuanxin Pharmacy has established over 200 directly operated hospital-adjacent pharmacies and professional DTP (Direct-to-Patient) pharmacies across 66 cities in China, covering more than 260 Grade A tertiary hospitals and oncology hospitals nationwide. In addition, the Brand Doctor project delivers online health education content through live streaming, short videos, and articles. These multiple business lines collectively provide services including online follow-up consultations, digital health education, and O2O medication delivery, enabling refined management of specialized diseases and conditions.

This year, Miaoshou Doctors expanded into the insurance sector by establishing the insurtech company Yuanxin Huibao. Focusing on health insurance products for critical and chronic diseases, the company leverages a “healthcare + insurance” service model to deliver more reliable medical and pharmaceutical services to users. Additionally, it utilizes big data to provide insurers with solutions for actuarial pricing, risk control, customer acquisition, and user retention.

At this point, Miaoshou Doctor’s integrated online-offline and in-hospital-out-of-hospital business layout has connected the key links of “medical care–patients–pharmaceuticals–insurance.”

Miao Health: Health Management and Insurance Services Based on Big Data and Artificial Intelligence

Miao Health is a health management company built on big data of health behaviors and artificial intelligence. It operates seven major brands: “Miao Health APP,” “Miao+,” “Miao Cloud,” “Miao Insurance,” “Miao Medical,” “Miao Pharmacy,” and “Canada Health Management Center (China).” By integrating high-frequency health management with low-frequency medical services, it has created an entry-level health platform application that combines “healthcare, medicine, pharmacy, and insurance.” To date, Miao Health has served 4,500 corporate clients, with a cumulative user base exceeding 75 million.

This year, Miao Health launched a series of “CPIC Miao Health” interactive insurance products, shifting the role of insurance from risk bearer to prevention-focused provider. Users can earn corresponding rewards by completing designated health plans, thereby incentivizing them to maintain healthy habits. In this process, Miao Health leverages digital technology as a connector by collecting users’ health behavior data through mobile applications and wearable devices.

In September this year, the first concept store of Miao Health’s Canada Health Management Center (China) opened in Beijing. As a multi-functional complex integrating fitness and exercise, chronic disease rehabilitation, health management, and new retail health products, it combines online operations to explore offline scenario-based service models.

SENYINT: Efficiently Connecting Medical Resources via Cloud Platform

As a provider of medical cloud application solutions, SENYINT leverages its medical cloud platform to deliver solutions for telemedicine, medical consortia, internet hospitals, regional healthcare, integration platforms, and digital hospitals to government entities, healthcare institutions at all levels, and industry partners. To date, SENYINT’s medical cloud platform has reached 80% of Grade A tertiary hospitals in China, covering more than 7,000 hospitals across 31 provinces and over 250 medical consortia nationwide, while serving more than 240,000 primary care physicians.

SENYINT built a telemedicine platform for Guizhou Province, one of the first provinces in China to pilot remote medical services. This initiative enabled all 199 public hospitals at or above the county level in Guizhou to achieve “county-to-county” telemedicine connectivity, and extended telemedicine access to all 1,543 township health centers across the province, achieving “township-to-township” coverage.

This year, SENYINT launched a variety of cloud-based service scenarios, including “Mobile Cloud,” “Cloud Outpatient,” “Cloud Specialty,” “Cloud Consultation,” “Cloud Ward,” “Cloud Follow-up,” and “Cloud Clinic,” covering all stages from pre-diagnosis to post-diagnosis. Meanwhile, its telemedicine business has continued to penetrate deeper into healthcare institutions, extending services from the hospital level down to individual departments to create “department-level cloud services,” thereby facilitating high-frequency interactions between departments.

Weimai: Focused on Localized Internet Healthcare

Weimai is an internet-based healthcare service platform with a strong focus on localization. To date, Weimai has connected nearly 1,000 public hospitals across more than 80 cities in 21 provinces throughout China, with 100,000 doctors providing medical and health services on the platform to over 10 million users.

This year, Weimai has delved deeply into innovative healthcare services, bridging the service loop between in-hospital and out-of-hospital settings as well as online and offline channels to create a “Trusted Healthcare” model. For instance, Weimai partnered with Zhejiang Taizhou Enze Medical Group to launch “Internet + Specialty Care” services. In specialty areas such as obstetrics, pediatrics, oncology, chronic disease management, and orthopedics, they introduced comprehensive, full-cycle health management services. Notably, the one-stop obstetric care initiative—a representative innovation in specialty services—covers five key stages: pre-conception, pregnancy, childbirth, postpartum, and parenting. This model has been implemented across multiple hospitals in Taizhou City, helping these institutions establish a patient-centered care environment for expectant and new mothers.

Furthermore, Weimai’s one-stop maternity care services have been launched in over 20 cities across China, cumulatively providing offline prenatal check-ups, online consultations, and interpretation of prenatal examination reports to tens of thousands of individuals, achieving an overall satisfaction rate of 98%.

Amid this year’s IPO boom in digital healthcare, what key insights or trends can domestic companies draw from the performance of several listed firms? We believe there are several main points:

We observe that among several publicly listed companies, with the exception of Peloton, which markets itself on fitness, all have emphasized in their prospectuses the cost savings delivered to users. Providing targeted, greater savings for users makes them more willing to pay.

Currently, large hospitals in China have completed large-scale informatization, generating multi-dimensional data. A significant number of medical big data companies are involved in informatization platforms and databases, which pertain to the creation and storage of data. However, few enterprises participate in the stages of data processing, cleaning, and analysis. Even among those engaged in data organization and analysis, most focus on physicians’ scientific research and clinical applications. It is hoped that more enterprises will leverage the value of big data and artificial intelligence by focusing on improving the management efficiency of healthcare institutions and reducing costs.

In serving both patients and physicians, many companies in China have already established connectivity among key elements such as patients, doctors, pharmaceuticals, and insurance. This has enhanced the convenience of seeking medical care and improved access to high-quality healthcare services, while also boosting medical efficiency and gradually emphasizing a patient-centric approach. Building on this foundation of connectivity and efficiency gains, it is essential to optimize product and service models based on quantifiable cost control.

The U.S. healthcare system faces waste caused by complex processes in settlement and payment, creating opportunities for digital health companies. In China’s healthcare system, as the government advances cost-containment measures within basic medical insurance and encourages commercial health insurance, scenarios involving commercial insurance payments will become increasingly common. The resulting changes include more business interactions among healthcare institutions, patients, and insurance companies. Consequently, there is a growing need to leverage big data, artificial intelligence, and other technologies to optimize claims processing for insurers, enhance risk control management, and reduce costs.

According to foreign media, most healthcare stakeholders believe that digital health is still in its infancy and is working to define its position within the health ecosystem. Establishing a sustainable profitability model remains an ongoing exploration in this field. Phreesia, Livongo, and Peloton all noted in their prospectuses that they may not be able to achieve or maintain profitability in the future.

Although the outlook may appear somewhat pessimistic, this is an inevitable stage following the emergence of a new field, with some pioneering companies always leading the way through their exploratory spirit. To address this challenge, scaling up through acquisitions and investments is a strategy commonly cited by the aforementioned listed companies. When a company possesses core technologies and receives sustained capital support, acquiring or investing in high-quality projects can complement its existing business, expand its scale, and provide access to additional innovative technologies, customers, and sales channels. Furthermore, this approach generates predictable revenue streams, diversifies income sources, and serves as a means to mitigate financial risks, thereby simultaneously addressing the dual imperatives of “survival” and “innovation.”