WuXi AppTec Fires on All Cylinders: Surpassing RMB 10 Billion Revenue and RMB 250 Billion Market Cap

WuXi AppTec

New Drug R&D and Production Service Provider

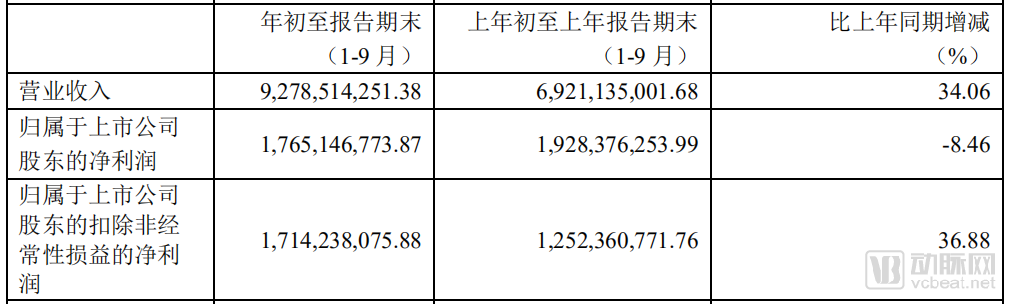

In the first three quarters of 2019, WuXi AppTec’s revenue reached RMB 9.279 billion, a year-on-year increase of 34.1%. With the release of the quarterly report, it is virtually certain that WuXi AppTec’s total revenue for 2019 will exceed RMB 10 billion. Meanwhile, after deducting non-recurring gains and losses, the company’s net profit amounted to RMB 1.714 billion in the first three quarters, representing a 36.88% increase from the same period last year. The net profit growth rate even surpassed the revenue growth rate, indicating that WuXi AppTec is not only continuously enhancing its revenue-generating capability but also becoming increasingly profitable. In addition, WuXi AppTec’s total workforce exceeded 20,000 employees, including more than 1,000 individuals holding doctoral or equivalent degrees. These milestone figures signify that 2019 marked a new starting point for WuXi AppTec.

WuXi AppTec: Selected Financial Data for the First Three Quarters of 2019

WuXi AppTec: Key Performance Highlights for January–September 2019

●Operating revenue increased by 34.1% to RMB 9.279 billion.

●Gross profit increased by 30.6% to RMB 3.66 billion. Gross margin was 39.5%.

●EBITDA reached RMB 2.914 billion, a year-on-year increase of 7.3%.

●Adjusted EBITDA reached RMB 3.006 billion, a year-on-year increase of 41.0%.

●Adjusted Non-IFRS net profit attributable to shareholders of the listed company increased by 38.0% to RMB 1.842 billion.

●Net profit attributable to shareholders of the listed company amounted to RMB 1.765 billion, a year-on-year decrease of 8.5%. The decline was primarily due to a loss of RMB 45 million from changes in the fair value of the company’s investments during the reporting period, compared with a gain of RMB 669 million from such changes in the same period last year.

●Diluted adjusted Non-IFRS earnings per share increased by 17.7% year-on-year; diluted earnings per share decreased by 22.5% year-on-year.

Mr. Hu Zhengguo, Co-CEO of WuXi AppTec, stated, “In the first three quarters of 2019, the Company’s total revenue and adjusted Non-IFRS net profit maintained an accelerating growth trend. On one hand, the Company continued to expand its new customer base and increase penetration among existing customers; on the other hand, it strengthened conversion between upstream and downstream service departments, further enhancing platform synergies. During the reporting period, the Company added more than 900 new customers, with over 3,700 active customers, and all business segments achieved steady development.”

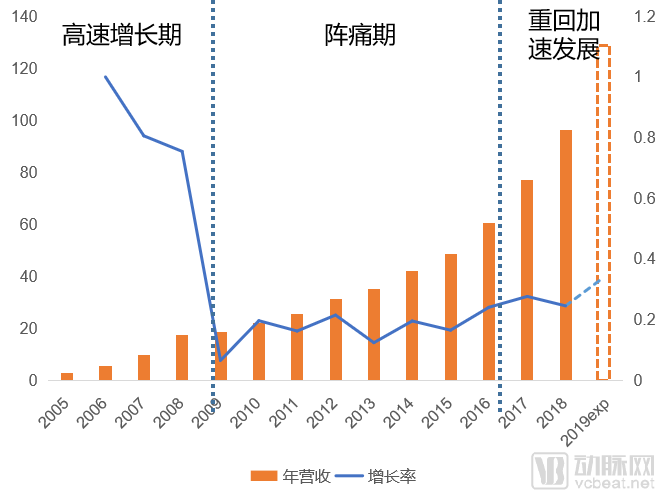

Looking back on WuXi AppTec’s 19-year history, we can clearly identify three distinct phases of development: a period of explosive growth from 2000 to 2008; a phase of growing pains from 2009 to 2014; and a return to rapid growth from 2015 to the present. Today, WuXi AppTec is rapidly restructuring through vertical integration and horizontal expansion. With an almost impeccable track record thus far, the company is playing a much larger game.

VCBeat reviewed the development history of WuXi AppTec and summarized five key decisions it made during its growth:

1. In the early stages of development, bypass the highly competitive clinical CRO sector and focus on expanding preclinical CRO and CMO/CDMO businesses;

2. Once the business matures, decisively list on the secondary market to seek capital support;

3. Halt lateral expansion when growth stagnates, and consolidate existing businesses;

4. Decisively returned to the domestic capital market amid its strong performance, maximizing market capitalization through a “one-into-three” listing;

5. Make precise forecasts for the future, pursue vertical integration and horizontal expansion, and build a CRO group with comprehensive industry coverage.

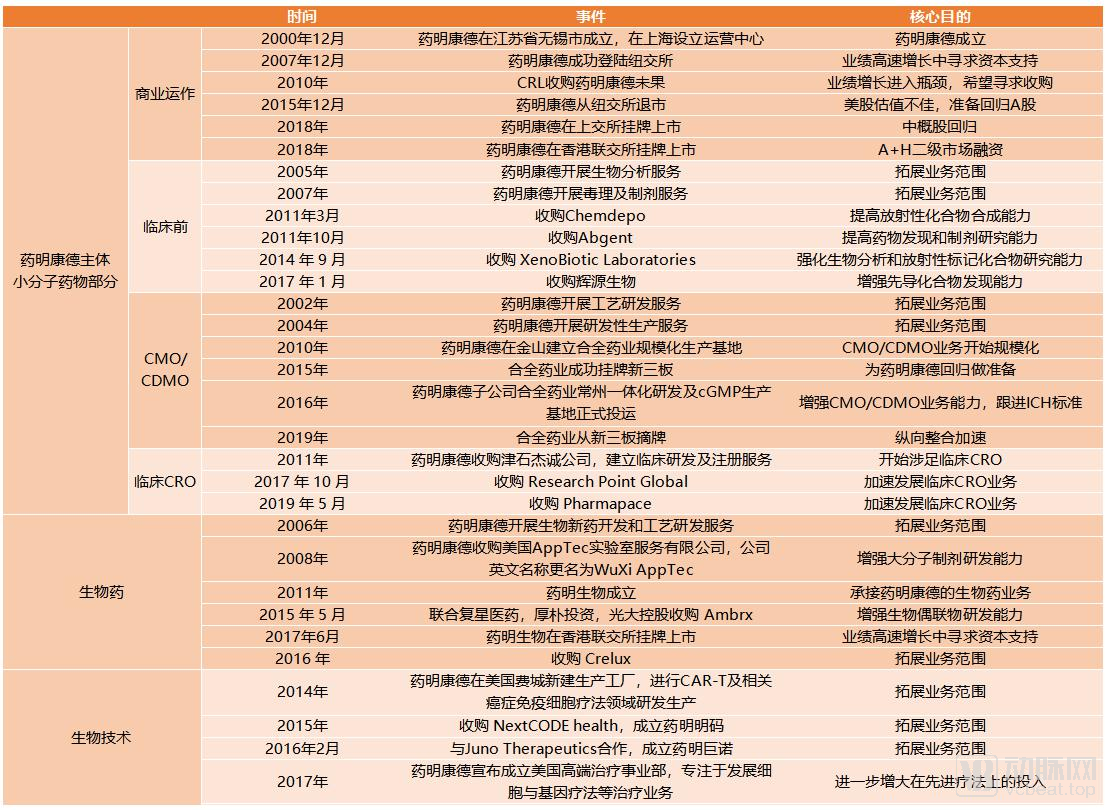

WuXi AppTec: Milestones

In December 2000, Li Ge returned to China to launch a startup, leveraging his years of accumulated expertise in small-molecule drug R&D, and WuXi AppTec was officially established in Wuxi.

Another major event occurred in 2000: Charles River Laboratories International (CRL), a leading global preclinical CRO, went public in the United States. Major players in the CRO sector, including Quintiles (now IQVIA), Covance, and PPD, primarily focus their businesses on clinical trial outsourcing services, with little involvement in preclinical drug development. In contrast, CRL is one of the few CROs that provide preclinical solutions centered on laboratory services.

From the outset, WuXi AppTec made the right first move by bypassing clinical trials and instead focusing on early-stage drug discovery and late-stage manufacturing, partnering with international pharmaceutical companies.At that time, clinical CRO giants such as Quintiles and Covance had long been eyeing the Chinese market and entered it in 1997–1998. For the newly established WuXi AppTec to compete with these CROs, which had developed over decades, would undoubtedly have been akin to striking a stone with an egg. The environment for new drug development in China was still largely undeveloped at the time; for CRO companies to survive, they needed to seek collaborations with international pharmaceutical companies.

What followed is a familiar story: Li Ge sketched more than 20 chemical drug template molecules on an airplane and asked his laboratory staff to attempt their synthesis. A few months later, Li Ge brought the developed small-molecule templates to a U.S. pharmaceutical company, immediately capturing the attention of its head of R&D and successfully establishing a collaborative partnership.

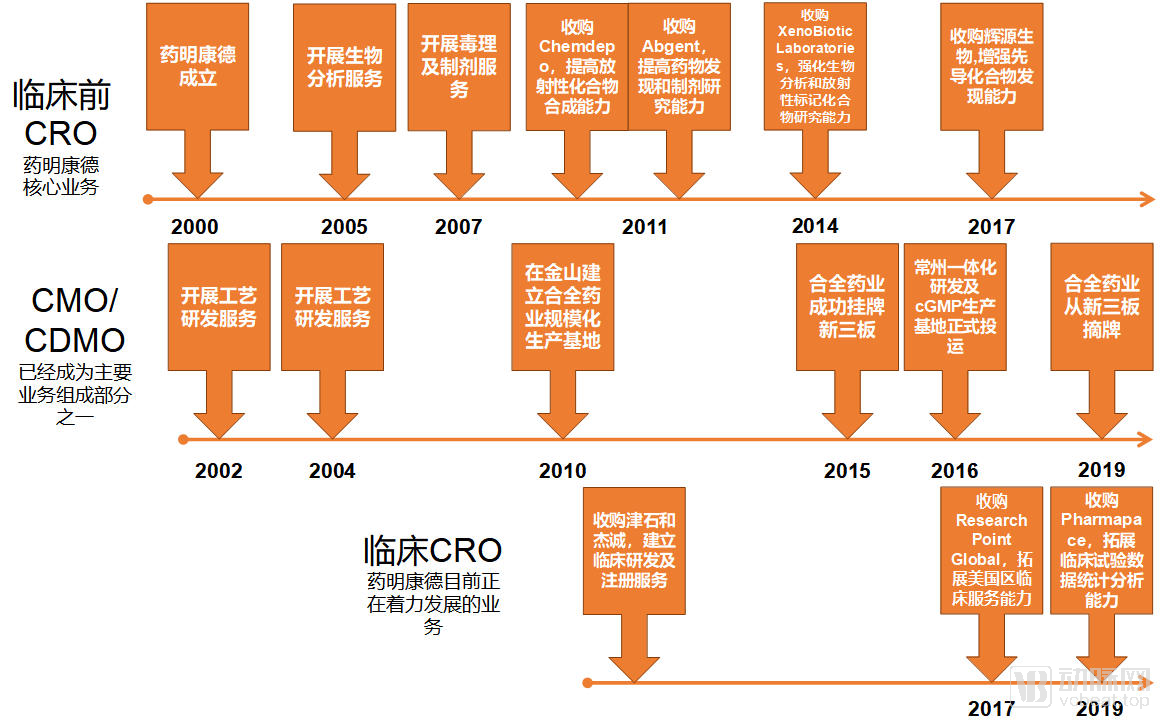

Subsequently, WuXi AppTec gradually expanded its presence in the preclinical R&D sector. By 2007, the company had covered the entire process of early-stage drug development and process development and manufacturing, thereby basically perfecting its industrial chain structure. The small-molecule CRO industry steadily transitioned from its start-up phase to maturity.

At this juncture, WuXi AppTec made its second critical decision: to pursue an initial public offering (IPO) decisively at a pivotal stage of corporate development, thereby securing capital support for further growth.This also marked the first time WuXi AppTec demonstrated its keen business acumen. In subsequent series of business operations, WuXi AppTec’s strategies were virtually flawless.

WuXi AppTec and Its Subsidiaries’ Listing and Fundraising Journey

2007 marked WuXi AppTec’s first period of remarkable success. In August 2007, WuXi AppTec listed on the New York Stock Exchange, issuing 13.19 million shares at a price of $14 per share. Following its IPO, the company’s stock price rose rapidly, reaching a peak of $45.65 within just over two months. That year, WuXi AppTec’s annual revenue exceeded $100 million for the first time, with a net profit of $33.9 million and a net profit margin surpassing 25%.

At that time, WuXi AppTec’s revenue structure was highly concentrated, with its top ten customers accounting for over 70% of total revenue and achieving a 100% retention rate. Leveraging its exceptional service capabilities, WuXi AppTec established long-term partnerships with leading pharmaceutical companies such as AstraZeneca, Merck & Co., Eli Lilly, and Pfizer.

A prime example is the collaboration with AstraZeneca in 2006. In August 2006, AstraZeneca announced a $14 million investment over the following two years to partner with WuXi AppTec on projects related to compound synthesis. By June 2008, WuXi AppTec had successfully delivered hundreds of thousands of compounds to AstraZeneca, completing the partnership two months ahead of schedule. Through its high quality and efficiency, WuXi AppTec established a relationship of mutual trust with pharmaceutical companies, marking the first step toward realizing its vision of “making it easy to develop drugs anywhere in the world.”

In 2008, despite the economic crisis and a continuous decline in stock price, WuXi AppTec maintained an annual revenue growth of nearly double. In the same year, WuXi AppTec acquired Apptech, horizontally expanding its business scope into the fields of large-molecule formulations and medical devices.

In its 2008 annual report, WuXi AppTec disclosed that revenue from orders placed by its top ten customers amounted to only RMB 138 million, representing a growth rate of just 38% and accounting for 54% of its total revenue. As the revenue growth from its key clients slowed, WuXi AppTec was compelled to begin cultivating smaller clients. However, the inherent instability of orders from these smaller clients foreshadowed the subsequent slowdown in the company’s overall performance growth.

In early 2009, as the subprime mortgage crisis intensified, WuXi AppTec, listed on the New York Stock Exchange, was also affected. Following the sharp decline in 2008, WuXi AppTec’s stock price hit a low of $3.67. Meanwhile, the company’s growth suddenly slowed. In 2009, WuXi AppTec reported annual revenue of $270 million, representing a mere 6.5% increase from 2008.

Changes in WuXi AppTec's Revenue Growth

2009 was a year of painful reflection for WuXi AppTec. At the end of 2008, WuXi AppTec shut down its biologics manufacturing operations in the United States. Meanwhile, affected by the subprime mortgage crisis, the company experienced a decline in both the volume of orders and the average transaction value for its manufacturing services. Consequently, revenue from WuXi AppTec’s manufacturing services shrank significantly in 2009, dropping from $48.5 million in 2008 to $10.2 million. On another front, growth among key clients continued to slow, with the top ten customers contributing only $144 million in revenue in 2009, while laboratory services grew by less than 25%.

WuXi AppTec’s management team also appeared to recognize its development bottleneck. With its typically keen business acumen, WuXi AppTec made a pivotal decision at this juncture: to sell itself to CRL. On April 26, 2010, CRL announced it would acquire WuXi AppTec for $1.6 billion.

At that time, Tigermed, another representative domestic CRO company, had not yet gone public, so WuXi AppTec could not gauge how the Chinese secondary market would respond to CRO firms. In 2009, WuXi AppTec’s net revenue was $52.9 million. A price-to-earnings (P/E) ratio of 32 times was broadly in line with prevailing valuations in the overseas CRO industry. From this perspective, although the transaction did not yield substantial profits for WuXi AppTec, it was still considered a reasonable deal.

In fact, CRL’s total revenue also declined sharply in 2009, falling from $1.34 billion in 2008 to $1.20 billion, which was lower than the same period in 2007. In its annual report, CRL attributed its downturn to clients’ business restructuring, economic slowdown, and the subprime mortgage crisis. The acquisition of WuXi AppTec was driven by CRL’s recognition of the potential in the Chinese market, with the aim of entering this market through WuXi AppTec and identifying new revenue streams.

The deal ultimately fell through, marking perhaps the biggest misstep in CRL’s 80-year history. Although CRL had recognized the opportunities embedded in the Chinese market, its investors did not endorse the company’s strategic choice. On the day the acquisition was announced, CRL’s stock price plummeted by 16% from $39.77 and continued to decline in the following days, hitting a low of $26.82. In the end, CRL voluntarily abandoned the transaction and paid WuXi AppTec a $30 million breakup fee.

Fortunately, the deal fell through; otherwise, we would not have had the opportunity to witness the spectacle of WuXi AppTec’s three-for-one stock split and listing.

Growth Slows, Acquisition Attempts Fall ThroughAfter the growing pains, WuXi AppTec has come to realize that it is not yet time for horizontal expansion. Instead, it should continue to consolidate its advantages in preclinical CRO and CDMO services, while securing top-tier clients and expanding channels for smaller customers.In 2010, WuXi AppTec established a large-scale production base for STA Pharmaceuticals in Jinshan, marking the beginning of its scaled expansion of CDMO service capabilities.

Consequently, by the end of 2010, WuXi AppTec’s performance experienced a slight correction. Although it no longer maintained its previous year-on-year doubling growth rate, a growth rate approaching 20% was not considered slow for a maturing enterprise. Manufacturing services began to grow rapidly that year, rising from $20.1 million in 2009 to $39.2 million, nearly doubling. The growth in laboratory services was primarily driven by increased revenue from the top ten customers, with the concentration among these top ten clients returning to 60%.

In the following years, WuXi AppTec consistently adhered to this development strategy, maintaining a growth rate of approximately 15%. Manufacturing services were the primary driver of growth during this period. By 2014, revenue from manufacturing services reached $182 million, accounting for 27% of total business, up from only 7.5% in 2009. Meanwhile, the revenue composition of laboratory services became increasingly stable. Although revenue from top clients continued to grow, its proportion of total revenue declined steadily, eventually stabilizing at around 35%. To date, WuXi AppTec’s overall revenue structure has remained largely unchanged.

However, during this period, overseas secondary markets held a negative outlook on the preclinical CRO industry. Starting in July 2011, multiple foreign brokerages successively downgraded the stock ratings of WuXi AppTec and Charles River Laboratories (CRL), with WuXi AppTec’s rating adjusted from “Buy” to “Hold,” and CRL’s from “Hold” to “Underweight.” The unfavorable sentiment in overseas markets, coupled with the opening of the domestic market, ultimately drew WuXi AppTec back to China.

In August 2012, Tigermed, a leading domestic clinical CRO, was listed on the Shenzhen Stock Exchange. From 2013 to 2014, Tigermed’s price-to-earnings (P/E) ratio remained stable at around 70. In contrast, WuXi AppTec, which was listed in the United States, had a valuation hovering around a P/E ratio of 30. Coupled with the A-share bull market that began in July 2014, WuXi AppTec found itself somewhat restless.

WuXi AppTec, always highly sensitive to business operations, will certainly not let slip the vast domestic market; a compelling drama is beginning to take shape within its strategic plans.

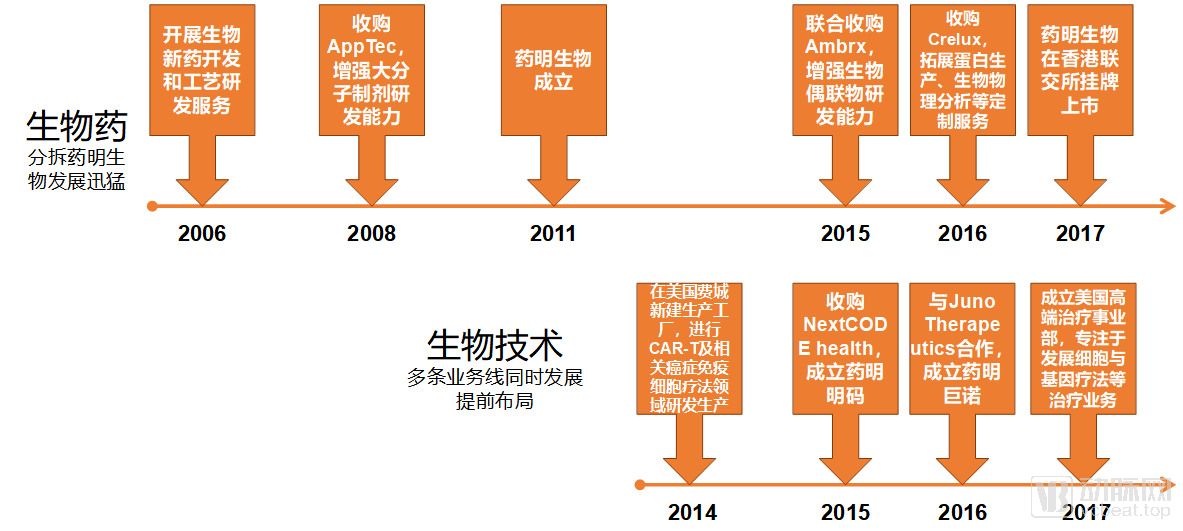

Thus, in April 2015, with WuXi PharmaTech successfully listing on the National Equities Exchange and Quotations (NEEQ), setting a precedent for subsidiaries of overseas-listed companies to be listed on the NEEQ, WuXi AppTec’s “spin-off into three” return process was officially launched.WuXi STA’s listing on the New Third Board was a critical step in the “one-into-three” restructuring and return. First, the funds raised could provide financial support for WuXi AppTec’s privatization process; second, WuXi STA, with its elevated market capitalization, could serve as a guarantor for WuXi AppTec’s acquisition loans.

Subsequently, in late 2015, WuXi AppTec repurchased its U.S.-listed shares for $3.3 billion, successfully completing its privatization. Following the privatization, the equity stakes held by the four founders increased. Coupled with concerted action agreements with other private equity (PE) firms, the voting rights of the four founders rose to 34.4812%, representing a significant leap from the pre-privatization level.

Consequently, WuXi Biologics’ listing on the Hong Kong Stock Exchange (HKEX) and WuXi AppTec’s dual listings on the Shanghai Stock Exchange (SSE) and HKEX followed naturally. WuXi Biologics went public on the HKEX in June 2017, and its market capitalization surpassed HK$100 billion within 295 days. WuXi AppTec listed on the SSE in May 2018, recording 16 consecutive daily upper-limit gains post-IPO, with its market capitalization exceeding RMB 140 billion. Subsequently, WuXi AppTec also listed on the HKEX in December 2018. The company’s ultimate “one-into-three” strategy was highly successful, driving its total market capitalization above RMB 250 billion.

As its commercial operations progressed, WuXi AppTec’s overall revenue returned to a fast-growth trajectory, achieving a compound annual growth rate (CAGR) of over 25% from 2015 to 2018. During this period, domestic policies provided significant impetus to the CRO industry. On one hand, China launched pilot programs for the Marketing Authorization Holder (MAH) system in 2016, formally integrating CRO companies into the mainstream pharmaceutical ecosystem. On the other hand, China’s accession to the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) in 2017 enhanced communication and collaboration between domestic and international pharmaceutical sectors, thereby expanding market opportunities for Chinese CRO firms.

Prior to its delisting from the U.S. stock market, WuXi AppTec had already begun to further strategize for its future vertical integration and horizontal expansion.

WuXi AppTec: History of Major Business Development

Vertically, the acquisitions of Chemdepo and XenoBiotic Laboratories enhanced its capabilities in radiolabeled compound research; the acquisitions of Shanghai Jingshi and Shanghai Jiecheng expanded its business scope into clinical CRO services. Its Wuxi and Wuhan branches also commenced operations in 2012. In WuXi AppTec’s prospectus, the company projected a trend toward vertical integration in the future development of the CRO industry. Compared with its annual reports during its previous listing on U.S. stock exchanges, WuXi AppTec’s A-share prospectus and annual reports have added a section on “clinical research and other CRO services.”

WuXi AppTec’s preclinical CRO and CMO/CDMO businesses have already reached the forefront in China, and even globally. As of September 30, 2019, the small-molecule CDMO/CMO service projects undertaken by WuXi AppTec involved more than 900 new drug molecules, among which 40 were in Phase III clinical trials and 17 had received marketing approval. By bolstering its clinical CRO capabilities, WuXi AppTec will integrate the entire service chain spanning early-stage R&D, clinical trials, and drug manufacturing, thereby providing customers with one-stop CRO services.

Based on WuXi AppTec’s recent moves, its determination to establish a presence in clinical CRO services has become clear. Following the acquisitions of Jinshi and Jiecheng, WuXi AppTec acquired Research Point Global in October 2017 to expand its clinical research service capabilities in the United States; in May 2019, it acquired Pharmapace to further enhance its data analysis capabilities for clinical trials.Therefore, in the coming years, the development focus of WuXi AppTec’s parent company will inevitably be placed on advancing its clinical CRO operations.

From the results, WuXi AppTec’s clinical CRO business has begun to accelerate its development. In 2018, the growth rate of its clinical CRO segment reached 64%, and in the first half of 2019, the growth rate exceeded 100% compared to the first half of 2018.

Some investors have described STA Pharma’s delisting from the National Equities Exchange and Quotations (NEEQ) as “removing the firewood from under the pot.” In its announcement, WuXi AppTec stated that STA Pharma would not seek to list on any stock exchange, either within or outside China, through an initial public offering (IPO), a backdoor listing, or other means for three years from the date of its delisting.

In reality, the initial purpose of Hequan Pharma’s listing on the New Third Board was to prepare for WuXi AppTec’s return plan. Now that WuXi AppTec has completed its return, there is no longer any significance for Hequan Pharma to remain on the New Third Board. For a long time, WuXi AppTec, the parent company, has held more than 90% of Hequan Pharma’s shares, and all of its CMO/CDMO businesses have been undertaken by Hequan Pharma. From the perspective of WuXi AppTec’s current vertical integration strategy, as a core business component of the parent company, Hequan Pharma is more likely to be merged into the parent company in the future rather than pursuing independent financing and development.

WuXi AppTec's New Business Segment

Horizontally, WuXi AppTec began to make significant inroads into the biologics sector. In 2011, WuXi Biologics was established in Shanghai to take over WuXi AppTec’s biologics business; in the same year, it acquired Abgent to strengthen its research capabilities in biological agents. In 2015, it jointly acquired Ambrx with Fosun Pharma, Hopu Investment Management, and Guangda Holdings, thereby completing its strategic layout in bioconjugates.

WuXi AppTec has also begun to expand into the fields of cell therapy and genetic testing. In 2014, WuXi AppTec built a new production facility in Philadelphia, USA, for the research, development, and manufacturing of CAR-T-related cancer immunotherapies. In 2015, it acquired NextCODE Health, a company specializing in centralized databases of human whole-genome information, and established WuXi NextCODE to focus on the development of genomic big data. In February 2016, it partnered with Juno Therapeutics to establish WuXi Juno, advancing cell therapy technologies. WuXi AppTec itself has been actively expanding its footprint in the biotechnology sector. As of September 30, 2019, WuXi AppTec’s cell and gene therapy CDMO platform was providing services for 24 Phase I clinical trial projects and 9 Phase II/III clinical trial projects.

Following the completion of vertical integration, WuXi AppTec’s various horizontally expanded business lines will operate with relative commercial independence.WuXi Biologics was WuXi AppTec’s first foray into this space, and it elicited a very strong response in the secondary market. WuXi Biologics’ current market capitalization exceeds HK$100 billion, with a valuation approaching that of WuXi AppTec and a price-to-earnings (P/E) ratio as high as 140x. For a rapidly growing company with annual revenue exceeding RMB 2.5 billion and a growth rate still above 50%, this valuation may well be justified.

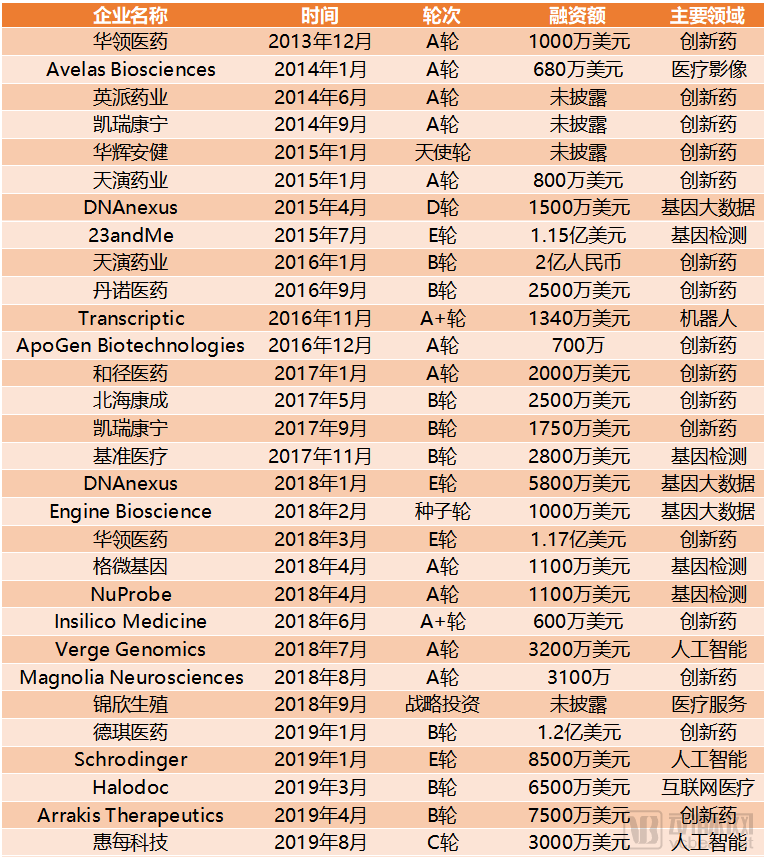

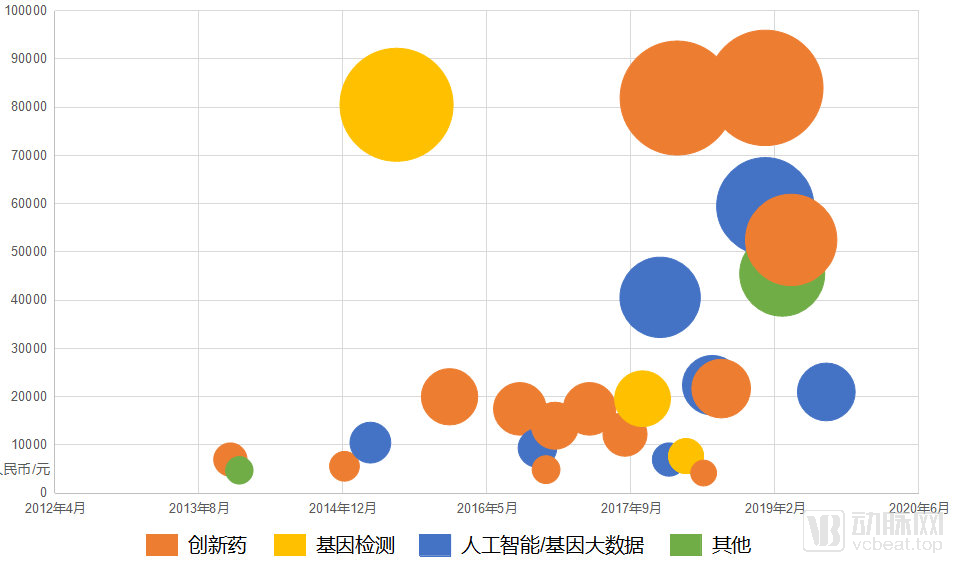

Since investing in Hua Medicine in December 2013, VCBeat has recorded WuXi AppTec’s participation in 30 investment deals. Starting from 2018, WuXi AppTec’s strategic perspective on the industry has undergone a significant shift.

WuXi AppTec's List of External Investments

WuXi AppTec's Distribution of External Investments

From late 2013 to late 2017, WuXi AppTec invested in a large number of startups in a fragmented and decentralized manner. These companies were primarily focused on innovative drugs, with additional involvement in artificial intelligence, genetic big data, and genetic testing. During this period, WuXi AppTec’s first notable success was Hua Medicine, which is now listed on the Hong Kong Stock Exchange. Subsequently, it invested in other innovative drug companies such as Imabio Therapeutics, Caregenics, and Adagene. Throughout this period, WuXi AppTec participated in only one major financing round, namely the Series E funding of 23andMe.

Since 2018, WuXi AppTec’s investment strategy has undergone significant changes. While the number of investments in the innovative drug sector has decreased, the average transaction size has increased. On another front, WuXi AppTec has made deep inroads into artificial intelligence and genomic big data enterprises. Notably, its January 2019 investment in Schrödinger, a U.S.-based AI-driven new drug R&D company, can be seen as reflective of WuXi AppTec’s vision for the future of pharmaceutical research and development.

Schrödinger’s analytical computing software helps accelerate the drug discovery process for new drug R&D professionals. By importing the chemical structures of integrins and small-molecule drugs into Schrödinger’s software, researchers can elucidate potential binding modes of these small molecules. Additionally, Schrödinger’s artificial intelligence platform assists pharmaceutical companies in drug molecule design, significantly shortening R&D timelines and enhancing efficiency for pharmaceutical enterprises.

Recognizing the future potential of artificial intelligence and genomic big data in new drug development, WuXi AppTec has begun to intensify its efforts in this field. Its investments in innovative drugs focus more on cutting-edge therapies, such as Arrakis Therapeutics, a developer of RNA-targeted small molecules, and Magnolia Neurosciences, a company developing novel small-molecule drugs to prevent neuronal death. These companies provide significant support for the growth of WuXi AppTec’s own business. By investing in these technology-driven enterprises, WuXi AppTec continues to solidify its foundation in the small-molecule CRO sector.

Over the past 19 years, WuXi AppTec has risen to the forefront of the global CRO industry, driven by its keen business acumen and precise decision-making. The company continued to deliver rapid performance growth in the first three quarters of 2019. Meanwhile, its horizontal business lines have been progressively expanded, with a cluster of companies led by WuXi Biologics emerging as leaders in their respective sub-sectors, thereby forming a comprehensive business matrix that covers the entire pharmaceutical landscape.

Dr. Ge Li, Chairman and Chief Executive Officer of WuXi AppTec, summarized in the Q3 financial report: “While maintaining accelerated business growth, the Company has continued to build capabilities, expand scale, and further enhance its enabling platform. These investments will help maintain and strengthen the Company’s core competitiveness, laying a solid foundation for future development. WuXi AppTec remains steadfast in empowering global customers to accelerate the development and launch of more innovative and high-quality medicines, thereby advancing our vision of ‘making it easy to make drugs and treat diseases’ for the benefit of patients worldwide.”