Three Types and Four Models: Current Status Report on China's Integrated Medical and Elderly Care Industry

Taikang Community

Chain养老机构

In 2018, the average life expectancy in China was 77 years. With the increase in life expectancy, the elderly population has grown, and the proportion of disabled and semi-disabled seniors has gradually risen. Over the next three decades at least, China’s elderly population will continue to climb, peaking around 2050. While addressing the daily care needs of the elderly, there is also a growing demand for medical services, rehabilitation, and related care.

Integrated medical and elderly care is not a simple addition of healthcare and eldercare services; rather, it integrates medical treatment, rehabilitation, health preservation, and wellness into a unified system. This approach achieves deep integration and coordinated development between medical and elderly care resources, thereby maximizing the utilization of social resources. The integrated medical and elderly care industry essentially possesses the five key attributes required of a pillar industry: scale of development, market prospects, technological intensity, industrial interconnectedness, and economic benefits.

According to the forecasts in Analysys’ “Special Analysis Report on China’s Integrated Medical and Elderly Care Market 2018,” China’s integrated medical and elderly care market is projected to reach RMB 5.7 trillion in 2020. The market encompasses four major segments—medical care, nursing, elderly care, and rehabilitation—and includes, but is not limited to, telemedicine services, medical nursing, personal care, health management, smart hardware, and health supplements.

According to the projections in the “White Paper on China’s Elderly Care Industry” released by the Chinese Academy of Social Sciences in 2016, the scale of China’s elderly care industry is expected to reach RMB 13 trillion by 2030. The “Report on the Development of China’s Aging Industry (2014)” predicts that the market size of integrated medical and elderly care services is poised to reach RMB 106 trillion by 2050, accounting for 33% of the country’s total gross domestic product (GDP).

Accelerating Pace of Population Aging

By the end of 2018, China's population aged 60 and above reached 249.49 million, accounting for 17.9% of the total population, among which those aged 65 and above numbered 166.58 million, representing 11.9% of the total population. During the 13th Five-Year Plan period, the elderly population aged 60 and above in China increased by an average of approximately 6.4 million per year, reaching around 255 million by 2020, or about 18.5% of the total population.

Meanwhile, the number of elderly individuals with disabilities and partial disabilities is increasing, with the population of disabled seniors rising year by year. In 2015, there were approximately 40.63 million elderly people with disabilities or partial disabilities, and 11.358 million held disability certificates. According to projections by the National Working Committee on Aging, by 2020, China will have over 42 million disabled seniors and more than 29 million aged 80 and above, collectively accounting for 30% of the total elderly population.

According to internationally recognized indicators, when the proportion of the population aged 65 and above in a country or region exceeds 7%, it is considered an aging society; when it exceeds 14%, it enters an aged society; and when it surpasses 20%, it becomes a super-aged society. The characteristics of aging in China include a rapid progression: it took only 25 years to transition from an aging society to an aged society, whereas France took 115 years, the United Kingdom took 45 years, and the United States took 69 years to undergo the same transition.

The degree of misalignment between China’s stage of population aging and its stage of socioeconomic development is unprecedented in human history. For instance, when the proportion of the population aged 65 and above reached approximately 12%, China’s per capita GDP was less than USD 10,000. In contrast, when Germany, the United States, and Japan reached the same level of population aging, their per capita GDPs were as high as USD 18,000, USD 29,000, and USD 38,000, respectively. The reality of “getting old before getting rich” poses significant challenges to China’s economic and social development.

The proportion of medical expenses for the elderly accounts for nearly one-third.

Healthcare expenditures for the elderly increase with age. By enhancing health management for this population, achieving effective chronic disease management, and ensuring early detection and treatment of diseases, we can shift healthcare spending upstream. Allocating more resources to “preventing potential diseases, treating minor ailments, and promoting wellness” will significantly reduce overall healthcare costs.

According to the National Health Services Survey, the consultation rate, hospitalization rate, and prevalence of chronic diseases among the elderly population aged 65 and above are significantly higher than those in other age groups. In 2003, 2008, and 2013, the two-week consultation rates for the population aged 65 and above were 28.1%, 30.3%, and 26.4%, respectively; the hospitalization rates were 8.4%, 15.3%, and 19.9%, respectively; and the prevalence rates of chronic diseases were 538.8‰, 645.4‰, and 539.9‰, respectively, with hypertension, diabetes, and heart disease accounting for a relatively high proportion.

According to statistics from relevant domestic and international sources, per capita medical expenditure for the elderly is generally 3–5 times that of the non-elderly population. The Statistical Bulletin on the Development of China’s Health and Hygiene Undertakings in 2018 shows that individuals aged 65 and above accounted for 29.2% of total hospital admissions. Among retired seniors hospitalized for more than three consecutive months, they represented only 2.1% of total admissions at Grade A tertiary hospitals, yet accounted for as high as 21% of total inpatient bed-days, with their medical insurance expenditures reaching 16.4% of total medical insurance fund outlays.

As the population ages, the health status of the elderly continues to decline, with increased incidence rates. Their rates of medical consultations and hospitalizations are significantly higher than those of other age groups, leading to greater demand for healthcare services and a corresponding rise in healthcare expenditures.

Rising per capita disposable income and an expanding middle class

The level of economic income fundamentally determines purchasing power; similarly, an increase in the income levels of the elderly will inevitably and effectively drive their demand for daily life care and medical services.

In 2018, the national per capita disposable income of residents was 28,228 yuan, representing a nominal year-on-year increase of 8.7% and a real growth of 6.5% after adjusting for price factors. Among this, the per capita disposable income of urban residents was 39,251 yuan, an increase of 7.8% (hereinafter, unless otherwise specified, all refer to nominal year-on-year growth), with a real growth of 5.6% after adjusting for price factors; the per capita disposable income of rural residents was 14,617 yuan, an increase of 8.8%, with a real growth of 6.6% after adjusting for price factors. According to the results of the Fourth Sample Survey on the Living Conditions of the Elderly in Urban and Rural Areas of China: In 2014, the average annual income of urban elderly people in China reached 23,930 yuan, and that of rural elderly people reached 7,621 yuan, representing increases of 16,538 yuan and 5,970 yuan respectively compared to 2000. After adjusting for price factors, the average annual growth rate of income for urban elderly people was 5.9%, and that for rural elderly people was 9.1%.

Changes in Household Size

The "China Family Development Report" shows that since the 1980s, the trend of shrinking average household size has become more significant, dropping to 3.96 people in 1990 and to 3.10 people in 2010. According to data from the National Bureau of Statistics, the average household size in 2012 was 3.02 people. China has already become a country with a relatively small average family size. Currently, there are over 88 million households in China with elderly members aged 65 and above, accounting for more than 20% of all households nationwide. According to research on the status of disabled elderly in urban and rural areas across China, the number of disabled elderly reached 37.5 million in 2013, and it is projected that this figure will exceed 40 million by 2015.

In stark contrast to the rapidly growing demand for family-based elderly care, families’ capacity to provide such care has been weakened by shrinking household sizes and constrained time resources. Among these, the challenges are most pronounced in rural households with left-behind elderly members and in households where seniors live alone.

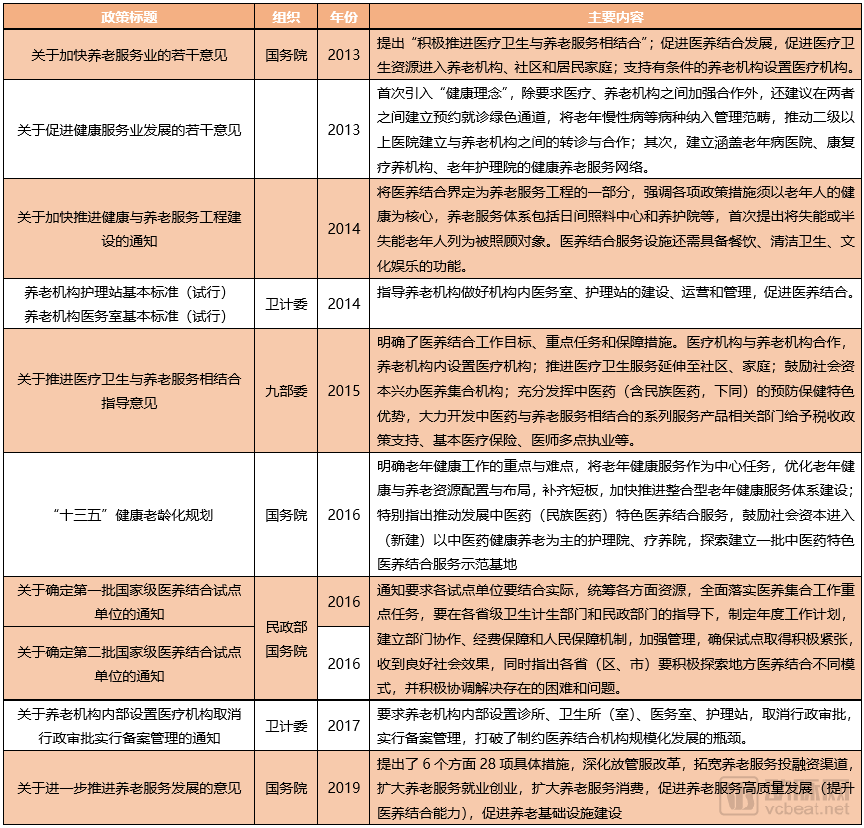

China has basically established a comprehensive framework for its elderly care policy system. The elderly care service industry is developing rapidly, and the quality of elderly care services has been effectively improved. Since the concept of integrating medical and elderly care was first proposed in 2013, related policies have been gradually refined. However, challenges remain in implementation, including difficulties in policy execution, low effectiveness, ambiguous content, and insufficient consideration of urban-rural coordination.

Table 1 Policies Related to the Integration of Medical and Elderly Care Services

The connotation of medical and elderly care services is very broad, covering almost all major sectors of the service industry. These include daily living assistance, health services, rehabilitation and wellness, medical care, and hospice care.

① Daily Living Care: Includes day care, home visits, domestic services, meal provision, and daily companionship.

② Health Services: Including health consultation, health management, and prevention and control of chronic diseases.

③ Rehabilitation and Healthcare: Primarily, rehabilitation therapists assist elderly individuals in carrying out corresponding rehabilitation training based on their physical condition and in accordance with tailored rehabilitation plans. This aims to help those recovering from major illnesses, suffering from chronic diseases, or experiencing disability or partial disability to restore their physiological and social functions, including rehabilitative treatment and functional recovery training.

④ Medical Services: Including outpatient care, inpatient care, and emergency medical services

⑤ Hospice Care: Includes palliative care, spiritual care, and psychological support and counseling services for family members.

China has initially established an elderly care service system that is home-based, community-supported, and institutionally underpinned. However, a common issue among elderly care institutions is the lack of medical nursing services, which fails to meet the medical needs of semi-disabled and disabled elderly individuals.

As of the end of 2018, there were 168,000 elderly care institutions and facilities across China, with a total of 7.271 million elderly care beds, representing a 3.3% year-on-year increase. This equated to 29.1 beds per 1,000 elderly individuals. Specifically, there were 29,000 registered elderly care institutions nationwide, a 10.0% year-on-year increase, providing 3.794 million beds, up by 3.9% from the previous year. There were 45,000 community-based elderly care service institutions and facilities, along with 91,000 mutual-aid community elderly care facilities. The number of beds for community residential and day-care services reached 3.478 million. According to general international standards for institutional elderly care, elderly care beds should account for approximately 5% of the elderly population. Currently, China still faces a shortfall of 5.2 million beds, indicating that industrial demand remains far from being met.

Home and Community-Based Elderly Care.Government-funded or subsidized professional elderly care institutions are entrusted to establish and operate home-based elderly care service stations within communities, managing and running these facilities after completion to provide home-based care services for seniors in the jurisdiction. Service offerings include daily living assistance, respite care, psychological support, and cultural activities. Currently, there is an excessive trend toward domestic housekeeping-style services, with a lack of medical care components such as nursing care and emergency response.

Institutional Elderly Care.Refers to elderly care provided within elderly care institutions. These institutions may be affiliated with public institutions, medical facilities, welfare organizations, or operated by individuals and group entities, specializing in providing comprehensive services for the elderly, including dietary and daily living support, hygiene and cleaning, personal care, health management, and cultural, sports, and recreational activities.

Integrated Elderly Care Complex.The sector primarily comprises real estate developers, insurance companies, and specialized elderly care service providers. Representative players include Poly, Vanke, Taikang, and China Life. Elderly care complexes center their value proposition on senior living services, although some still prioritize property sales. Key business models include monthly fee structures, title sales, sale-leaseback arrangements, and membership systems.

To address the lack of medical services in some elderly care institutions, China has encouraged the development of integrated medical and elderly care facilities since 2013 to meet the healthcare needs of disabled and semi-disabled older adults.

As of 2019, there were nearly 4,000 integrated medical and elderly care institutions across China, with over 1 million beds. Among these, more than 2,800 were medical facilities established within elderly care institutions, over 1,000 were elderly care facilities set up by medical institutions, and more than 20,000 pairs of medical and elderly care institutions had established contractual partnerships. From the perspective of basic models, there are four modes of integrated medical and elderly care.

① Medical Care and Elderly Support.This generally refers to a hospital-led model that essentially extends from medical institutions downstream into the elderly care and nursing sector, primarily targeting customers with essential needs. It involves establishing elderly care beds within hospitals and setting up elderly care institutions under the auspices of medical facilities; alternatively, it entails creating specialized departments within medical institutions to provide elderly care services, thereby transforming these facilities into integrated health and nursing institutions capable of delivering both medical and elderly care services. Due to the high market acceptance of medical institutions, this approach facilitates easier entry into the elderly care and nursing sector.

② Medical care integrated with elderly care.This generally refers to large-scale elderly care institutions allocating certain buildings or areas to establish medical service facilities such as nursing hospitals, outpatient clinics, or even primary or secondary general hospitals. This is the most common model of hospital-integrated care, which involves setting up medical institutions within elderly care facilities, including geriatric hospitals, rehabilitation hospitals, medical offices, and nursing homes. Examples include the Beijing No. 1 Social Welfare Institute and the Cuncao Chunhui Nursing Home in Chaoyang District, Beijing. At present, standalone elderly care projects face challenges such as low profitability and long payback periods. By integrating medical facilities, these projects can not only enhance health protection for seniors but also diversify revenue streams, thereby alleviating operational pressures.

③ Integration of Medical and Elderly Care.“Integrated Medical and Elderly Care,” as the name suggests, refers to the provision of medical and health services to the elderly through collaborative efforts between elderly care and healthcare sectors. Currently, there are numerous traditional contracted cooperation models in the market, wherein elderly care institutions sign cooperation agreements with medical institutions. Under such arrangements, medical institutions regularly dispatch medical personnel to conduct ward rounds and provide medical services at elderly care facilities, while the elderly care institutions assume responsibility for post-treatment rehabilitation and nursing care during the recovery period; a case in point is the collaboration between Beijing No. 2 Hospital and Beijing Jintai Yishouxuan Nursing Home. Another model achieves integration within elderly care communities by establishing comprehensive medical facilities through various means to ensure effective medical coverage for residents. For instance, Hunan Kangnaixin Elderly City has established the Kangnaixin Geriatric Hospital, an Elderly Care Center, and Nursing Workstations. The development of newly built integrated elderly care and medical institutions represents an emerging model of such integration, exemplified by projects such as the Balizhuang Yingzhi Health and Elderly Care Complex and Shuangjing Gongheyuan in Beijing.

④ Regional Coverage of Care.Community-based inclusive care is the integrated medical and long-term care system that the Japanese government is currently striving to establish. Its fundamental approach involves coordinating various elderly service providers—including hospitals, clinics, home-visit nursing agencies, pharmacies, and long-term care service agencies—under a established government service platform. Through home-based services, this model delivers integrated medical and long-term care tailored to the needs of older adults requiring both medical and nursing support.

⑤ Other New Models.By leveraging mobile internet and telemedicine technologies, the concept of elderly care has been digitized and virtualized. Through the establishment of a regional cloud-based information service platform for elderly care, seniors can communicate their service needs to the platform via telephone or the internet. The platform then dispatches enterprise staff to provide in-home services according to these needs, while also monitoring service quality. Taking Youhu Wanjia as an example, the company provides training for multi-skilled professionals with expertise in both medical nursing and elderly care, operates elderly care centers, and offers in-home services. Notably, 80% of its medical and nursing resources are sourced from major Grade A tertiary hospitals in Beijing.

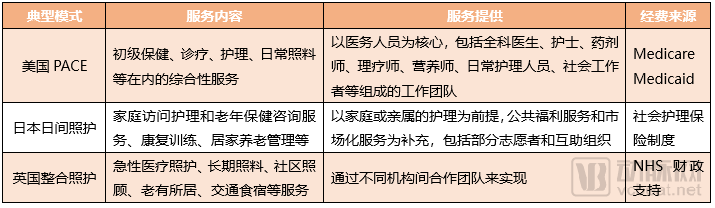

The U.S. model of integrated medical and elderly care primarily includes three categories of service programs.

The first category is the Program of All-Inclusive Care for the Elderly (PACE). PACE targets low-income individuals aged 55 and older who require nursing care but wish to remain living in the community. It provides a comprehensive range of social services, including daily personal care and medical services. By integrating community-based care with medical care, this model ensures that the long-term care needs of participants are met while they continue to live in their communities or homes.

The second category is the Congregate Housing Services Program (CHSP). This program primarily serves low-income elderly individuals who are unable to care for themselves, providing them with basic daily living services and other supportive services.

The third category is Home and Community-based Services (HCBS). HCBS serves elderly individuals living at home, providing them with daily living assistance and medical care. Compared with PACE, HCBS is more suitable for relatively younger and healthier older adults, while PACE is better suited for those with more severe functional impairments. The integrated medical and elderly care model in the United States is generally established through diverse state-specific aging programs, with long-term care policies consistently integrated throughout. State governments fully respect the physical and psychological needs of the elderly and continuously promote the development of home- and community-based care models to meet the growing demands of the aging population. Meanwhile, the U.S. integrated medical and elderly care model imposes high professional requirements on caregivers.

Japan’s integrated medical and elderly care model is categorized based on needs, with the main types being Day Care Centers, Senior Apartments, Nursing Homes (also known as Special Nursing Homes), and Elderly Welfare Centers. Day Care Centers provide daytime care for seniors who age in place; Senior Apartments are generally intended for healthy older adults; Nursing Homes primarily accommodate elderly individuals requiring specialized nursing care; and Elderly Welfare Centers mainly offer health check-ups and healthcare services to the elderly. The characteristics of Japan’s integrated medical and elderly care model are fully reflected in the establishment and operation of elderly care institutions. The setup of these institutions adopts an operational mechanism led by the government, with multi-party social participation and market competition. In terms of operations, most elderly care institutions have established long-term cooperative relationships with nearby hospitals to ensure the needs of elderly patients with illnesses are met. Medical and nursing staff within these institutions can diagnose and treat common daily ailments among the elderly.

The UK’s “Integrated Care” Model“Integrated care,” as defined by Henk N. and Philip C. B., refers to “a comprehensive, multi-faceted set of carefully planned and implemented services and care tailored to groups with similar needs or problems.” Specifically for older adults, integrated care should include at least the following elements: medical care, long-term care, social support, age-friendly housing, and transportation and meal services. In the United Kingdom, the integration of healthcare and social service resources is mandated by law. As a paradigmatic high-welfare state, the UK also relies on community-based elderly care to address population aging.

Table 2 International Models of Integrated Medical and Elderly Care, Service Contents, and Service Providers

Everjoy HEALTH Group Co., Ltd.

Our business operations encompass the general health sector, architectural ceramics, and eco-friendly healthy building materials. Within the general health sector, we plan to invest in and construct “Regional Health Complexes.” These complexes will operate at the county level, aiming to promote the health of urban and rural residents. Centered on secondary general hospitals, they will extend services downward to primary care facilities (community hospitals and health clinics), forward into health promotion, and backward into rehabilitation, elderly care, and hospice care, all supported by financial insurance services. In addition, Everjoy HEALTH will introduce chains of specialized hospitals (or outpatient clinics) as needed for its development, with a particular focus on assisted reproduction, dentistry, and rehabilitation. Furthermore, by leveraging overseas resources, we will develop high-end medical services.

YIHUA HEALTH CARE

Established two core business pillars: medical institution operations and services, and senior living community operations and services. The medical institution operations and services segment includes hospital trusteeship, hospital investment and operations, and cooperative diagnostic and treatment centers. The company engages in the investment and operation of membership-based senior living communities and provides elderly care services to resident members. Its subsidiary, Qinhuyuan, currently operates multiple senior living communities across cities including Shanghai, Hangzhou, Jiaxing, Ningbo, Qingdao, and Sanya.

Taikang Community

Taikang Community has introduced the CCRC (Continuing Care Retirement Community) model, providing residents with four distinct living service areas: independent living, assisted living, memory care, and skilled nursing. This offers a one-stop retirement living solution with varying levels of daily care and nursing services. The community features its own secondary-level rehabilitation hospital, with exclusive green channels for residents to ensure seamless access to professional and considerate rehabilitation and medical services. Taikang Community has established a presence in 15 key cities, including Beijing, Shanghai, Guangzhou, Chengdu, Suzhou, Wuhan, Hangzhou, Sanya, Nanchang, Xiamen, Shenyang, Changsha, Nanning, Ningbo, and Hefei. Currently, Taikang Community Yan Garden in Beijing, Shen Garden in Shanghai, Yue Garden in Guangzhou, and Shu Garden in Chengdu are fully operational.The 100-bed Taikang Yan Garden Rehabilitation Hospital in Beijing houses departments such as the Geriatrics Center, Rehabilitation Center, Internal Medicine, Surgery, Gynecology, Ophthalmology, Otolaryngology, Stomatology, Traditional Chinese Medicine, General Practice, Pharmacy, Laboratory Medicine, Radiology, and Psychiatry, and is accredited for medical insurance coverage. The retirement community offers three types of apartments: independent living apartments, disability care apartments, and dementia care apartments.

Poly

In 2012, Poly Group proposed a development strategy of “cultivating the entire industrial chain of the elderly care sector,” achieving diversified layout in institutional elderly care, home-based care, community-based care, age-friendly products, community healthcare, and exhibitions for the senior industry. As its high-end elderly care brand, Poly Hexi Club is committed to building “medical-care integrated” centers, providing seniors with affectionate, professional, and personalized full-process services. In 2017, it upgraded its community-embedded small-scale institution brand—Poly Heyue Club—which offers home-based elderly care services, community-based elderly care services, specialized medical-care services, and extended elderly care services, exploring a neighborhood-style healthy aging model with a three-dimensional honeycomb structure. Poly Heping focuses on the design, R&D, and overall configuration of age-appropriate products, providing age-friendly space renovation and product configuration services for various elderly care institutions, communities, and households. By hosting multiple sessions of the China International Senior Industry Expo and establishing the China Senior Industry Alliance, Poly has promoted the transformation and upgrading of China’s elderly care industry.

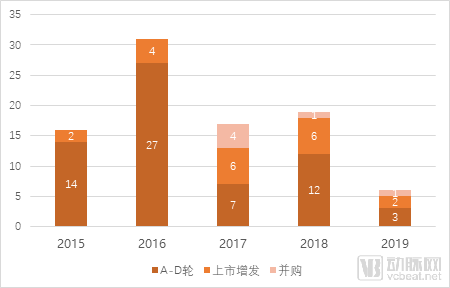

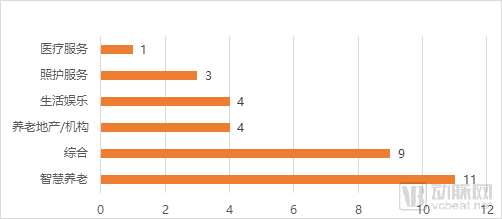

The elderly care industry comprises several specialized segments, including senior housing, elderly care products, pension finance, smart elderly care, and daily life and medical caregiving, as well as cultural and entertainment services. An analysis of the number of investments and financings in elderly care enterprises and their respective segments on VCBeat reveals that the current investment and financing market is becoming more rational. The segment attracting the most funding is smart elderly care, which includes institutional information systems, followed by segments related to elderly care institutions and daily living assistance. In contrast to the investment and financing market’s preference for smart elderly care, many large enterprises—such as insurance companies, real estate developers, and state-owned enterprises—are entering the market through institutional elderly care, with a greater emphasis on developing the entire industrial chain. This comprehensive approach encompasses elderly care products, home-based caregiving, medical services, and operational management.

Figure 1. Number of Investments and Financings in the Elderly Care Industry, 2015–2019

Figure 2 Investment Subsectors in the Elderly Care Industry, 2016–2019 (Incomplete Statistics)

The goal of integrating medical care with elderly care is to achieve an integrated model encompassing medical treatment, nursing, rehabilitation, and eldercare. This approach better meets the medical needs of older adults by providing medical services, rehabilitative nursing, and health management, thereby helping them maintain a healthy status. It also better addresses their eldercare needs through dedicated elderly care services, thus alleviating the burden on families and society. Medical services include professional offerings such as disease diagnosis and treatment, and emergency care; medical technology supports telemedicine and remote diagnostic services via internet-based platforms. Rehabilitative nursing provides long-term, continuous professional nursing services, including medical nursing, rehabilitation promotion, and hospice care. Health management offers services such as health check-ups, chronic disease management, and health consultation. Elderly care services provide daily living assistance, psychological and emotional support, and cultural and recreational activities. Through the integration of services, resources, and information, this model achieves online-to-offline connectivity across medical treatment, nursing, rehabilitation, and eldercare.

Policies and evaluation standards for the integrated medical and elderly care industry are being further implemented and refined. The current difficulties in implementing institutional elderly care policies stem from several factors: excessively low fee schedules for many medical services provided by primary healthcare institutions, imperfect medical insurance payment policies, and a lack of incentive mechanisms for caregivers in elderly care facilities, all of which have become bottlenecks restricting the development of integrated medical and elderly care. Fragmented management further complicates coordination; nursing homes are overseen by the Ministry of Civil Affairs, medical and health institutions by health authorities, medical insurance reimbursement by social security departments, and community-based home care services by aging affairs offices, making it difficult to align interests. Policy trends are moving toward deregulating administrative controls over the medical health and elderly care sectors to break down industry monopolies. Simultaneously, reforms in payment systems, including the exploration of a long-term care insurance system, are being pursued to promote the development of integrated medical and elderly care.

The Most Suitable Elderly Care Model for China: The Home- and Community-Based Care ModelChina’s elderly care system follows a “9073” structure, with 90% of seniors receiving home-based care, 7% relying on community-based services, and 3% residing in institutional facilities. From a socioeconomic perspective, given China’s large population base, adopting a home- and community-based care model can rapidly alleviate the shortage of nursing beds and institutional resources. For investment institutions in the elderly care sector, this model primarily involves service provision, requiring lower capital investment and yielding quicker returns. From the seniors’ perspective, most prefer aging in place, living in familiar surroundings, maintaining regular communication with family members, and receiving emotional support.Currently, unresolved challenges in home- and community-based elderly care include access to medical services, nursing, and rehabilitation for older adults. To address these issues, it is essential to establish close collaborations with community health service centers, create expedited green channels for medical consultations, and have family doctors regularly visit seniors’ homes to provide health consultations, physical examinations, and other services. To leverage the critical role of communities in elderly care, greater investment in community-based elderly care services is required. Communities should be encouraged to establish diverse social organizations dedicated to elderly care services, supported by preferential policy measures. Furthermore, promoting and fostering a “culture of community mutual aid” is vital. By encouraging family self-care, neighborly assistance, and broader social关怀 (care), societal forces can be guided and integrated into the development of the elderly medical and care service system.

For home- and community-based elderly care, the core impact of advancements in digital technologies and equipment lies in the construction of regionalized information cloud platforms and the widespread adoption of electronic health records for the elderly. For institutional operators, it is crucial to integrate and interconnect medical information systems with elderly care information systems. In addition to existing elderly care management systems, integrated care facilities should incorporate information systems that provide functionalities such as electronic medical record (EMR) management, physical examination management, pharmacy management, physiotherapy and rehabilitation management, and nursing workstation management. Furthermore, the application and upgrading of telemedicine and remote nursing technologies are vital for both institutional operators and providers of home- and community-based elderly care services. Leveraging technologies such as the Internet of Things (IoT), medical image transmission, wearable devices, and bedside nursing enables significant advancements in remote health monitoring, teleconsultation, and remote nursing care for the elderly.

Traditional Chinese Medicine Plays Its Due Role in the Integration of Medical Care and Elderly CareThe core theory of Traditional Chinese Medicine (TCM) regarding “preventive treatment of disease”—which emphasizes “prevention before illness, early treatment upon onset, and prevention of progression during illness”—is highly consistent with the philosophy of “promoting medical care through wellness support and enhancing wellness through medical assistance.” TCM-based health and elderly care services represent a unique advantage and characteristic of China’s integrated model of medical and elderly care. TCM offers numerous advantageous interventions for elderly care models, including Tai Chi, Baduanjin Qigong, massage, acupuncture, cupping, gua sha, and medicinal baths. Tailored TCM-based regimens for health preservation, conditioning, and rehabilitation can be designed according to the varying conditions of elderly individuals. TCM therapies are characterized by their simplicity, convenience, efficacy, and affordability, enjoying strong public acceptance and medical advantages in primary healthcare settings, making them the most preferred medical services among the elderly. In the practice of integrating medical care with elderly care, it is essential to conduct in-depth research and exploration of the theories and practices of TCM health preservation and “preventive treatment of disease,” striving to establish an integrated service system model that reflects Chinese characteristics.

Author: Li Ying

References

1. "Expert Consensus on the Integration of Medical and Elderly Care in China (2019)"

2. Exploring the “Last Mile” of Healthy Aging, Deloitte

3. Special Analysis of China’s Integrated Medical and Elderly Care Market, Analysys

4. Exploring a New Model of Medical-Nursing Integration: “Nurturing Health to Support Medicine, and Medicine to Aid Nursing”—Reflections on the Integration of Medical Care and Elderly Care in China’s Aging Society

5. Research on Population Aging and Healthcare Expenditures among the Elderly in China

6. Statistical Bulletin on the Development of Civil Affairs in 2018 - Ministry of Civil Affairs