Medicilon Soars 71.08% on STAR Market Debut as Pharmaron Clears HKEX Hearing, Signaling Peak Opportunities for China's CRO Sector

The keyword for pharmaceutical CROs this year can be summed up in one word: hot!

In January this year, Pharmaron’s successful listing on the A-share market appeared to set the tone for the development of the contract research organization (CRO) sector throughout the year. The newly revised Drug Administration Law, released in late August, incorporated a series of policies that have driven the development of innovative drugs in recent years, naturally drawing significant attention to the CRO industry, which is closely tied to innovative drug R&D. As the year drew to a close, the IPO of Medicilon and Pharmaron’s passing of the Hong Kong Stock Exchange’s listing hearing became the highlight events of the year.

Driven by the innovative drug industry, China’s CRO sector has experienced its best three years. Yet these three years are merely the beginning. Under policy impetus and market self-regulation, the CRO industry will continue to consolidate among leading players. Meanwhile, top-tier companies will extend their business scope across the entire R&D and manufacturing process, striving to provide clients with comprehensive solutions.

Medicilon, newly listed on the STAR Market, initially issued 15.5 million shares at an offering price of RMB 41.5 per share, raising approximately RMB 640 million in total—far exceeding the anticipated RMB 347 million. The proceeds will be used to fund several new projects for its innovative drug research and international registration center, as well as to supplement part of its working capital.

Medicilon opened at 66.66 yuan today, surging 60.6%. By the afternoon close, its real-time share price stood at 71.00 yuan, representing a 71.08% gain. A price-to-earnings ratio exceeding 70x also reflects the STAR Market’s expectations for the future development of the CRO industry.

In February 2004, MediciNova Ltd. was founded by Mr. Chen Chunlin. As the company's founder and lead core technologist, Mr. Chen brings extensive industry experience. He previously served as Chair of the Department of Pharmacy at the Park Hughes Cancer Center in the United States and as Chief Scientist of the Non-Clinical Drug Assessment Division at Vertex Pharmaceuticals in the United States, accumulating rich expertise in the field of pharmaceutical research and development.

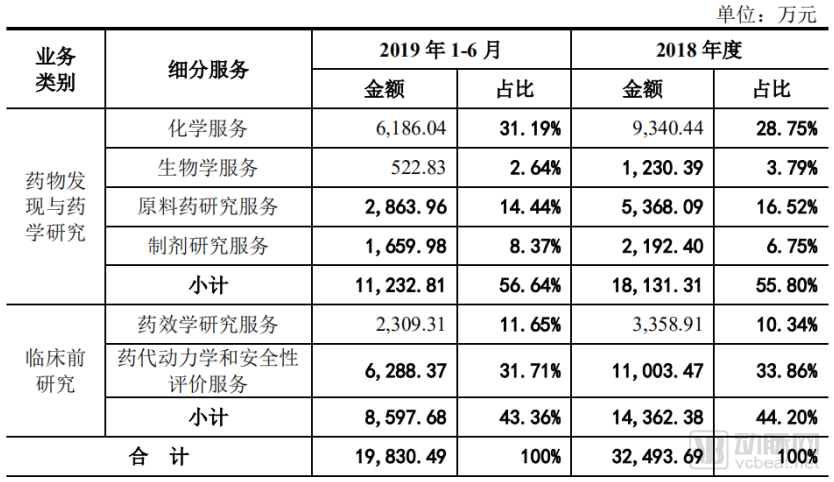

Distribution of Medicilon's Main Business

Medicilon achieved substantial performance growth in 2018, with revenue reaching RMB 320 million, representing a year-on-year increase of 30.4%. The company maintained this rapid growth trajectory in the first half of 2019, with revenue approaching RMB 200 million. Although Medicilon still lags significantly behind domestic CRO industry leaders such as WuXi AppTec and Pharmaron in terms of scale, it has firmly established its market position through its own capabilities.

As the first CRO company listed on the STAR Market, Medicilon’s business layout primarily focuses on preclinical product development. As a professional CRO providing comprehensive preclinical R&D services for biopharmaceuticals, Medicilon covers the entire process of preclinical new drug research, mainly including drug discovery, pharmaceutical studies, and preclinical studies. Among these, drug discovery and pharmaceutical studies for chemical drugs, along with pharmacokinetics and safety evaluation services, constitute Medicilon’s core business directions. Together, these two segments account for more than 60% of Medicilon’s total business.

Corresponding to its revenue is the compensation level of its staff. In terms of management personnel, the average annual compensation for Pharmaron’s management in 2018 was RMB 164,900, whereas MediciNova’s was only RMB 113,800 during the same period. Regarding sales personnel, the average annual compensation for Pharmaron’s sales staff in 2018 was RMB 804,900, while MediciNova’s sales personnel earned only RMB 159,700. MediciNova itself has highlighted personnel issues in its risk disclosures: during each period of the reporting period, the company’s employee turnover rates were 27.03%, 33.74%, 24.40%, and 11.43%, respectively, which are relatively high. Since 2017, several vice president-level employees from various departments have successively resigned from the company for personal reasons. Therefore, controlling employee attrition in the rapidly growing CRO industry may be a key issue that MediciNova needs to address.

Pharmaron, which listed on the A-share market earlier this year, passed the hearing of the Hong Kong Stock Exchange yesterday and is set to become another A+H listed company in the CRO sector, following WuXi AppTec.

According to its prospectus, the funds raised by Pharmaron through its Hong Kong listing will be primarily used for: expanding the capacity and capabilities of its laboratory and manufacturing facilities in China (30%); further expanding its overseas business (10%); establishing a pharmaceutical R&D service platform focused on biologic drug development (20%); enhancing its clinical development service capabilities (15%); acquiring other CRO companies globally (15%); and supplementing working capital (10%).

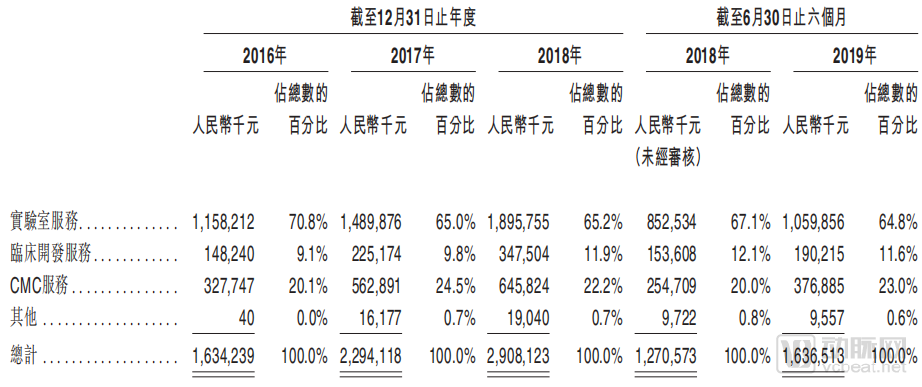

Pharmaron's Business Distribution

Pharmaron has maintained rapid growth in recent years, with a compound annual growth rate (CAGR) of nearly 33.4% from 2016 to 2018, and revenue reaching RMB 2.9 billion in 2018. Furthermore, based on the revenue data for the first half of 2019 (2019H1), Pharmaron continued to exhibit strong growth momentum in 2019.

As the third-largest global pharmaceutical CRO company by market share in the drug discovery segment, Pharmaron continuously expands its service offerings to raise its growth ceiling. Given the strong sustainability of its laboratory services, Pharmaron’s revenue from this segment is expected to continue rising. The CMC/CMO business is key to demonstrating the company’s scale. Unlike preclinical services, this segment requires substantial investment in fixed assets; therefore, as production capacity increases, it is likely to become Pharmaron’s most scalable business line.

The allocation of funds also reveals that Pharmaron, like WuXi AppTec, which also started with small-molecule drug R&D, is striving to integrate the entire value chain from research and development to manufacturing. The proportion of clinical development services and chemistry, manufacturing, and controls (CMC) services in its business has been continuously increasing, and a significant portion of the funds raised in this offering has been allocated to these two segments. Vertical integration has become the dominant trend in the CRO industry, and Pharmaron is advancing further along this path of vertical integration.

During the process of vertical integration, Pharmaron has completed its layout across the entire end-to-end R&D and manufacturing workflow through acquisitions. Its earlier acquisitions of Quotient and Xceleron were primarily aimed at enhancing its preclinical CRO service capabilities. In contrast, its strategic moves in the past two years, particularly the acquisitions of SNBL Clinical and Nanjing Sirui, mark Pharmaron’s significant entry into the clinical CRO sector.

SNBL Clinical is capable of providing comprehensive clinical CRO services, including medical collaboration, patient/volunteer recruitment, clinical trial execution, regulatory submissions, and data management. Nanjing Sirui’s core business is primarily concentrated in its subsidiary, Nanjing Ximaidi, a domestic clinical CRO enterprise that offers a high-quality one-stop clinical CRO service platform. These two acquisitions demonstrate that Pharmaron places significant emphasis on its strategic layout in the clinical CRO sector, which will be a key focus area in the near future.

CRO (Contract Research Organization) is an organization or institution that provides specialized outsourcing services to pharmaceutical companies and other pharmaceutical R&D institutions during the research and development process through contractual agreements, with its primary clients being innovative drug companies. Therefore, under the continuous support of domestic policies for the innovative drug industry in the past two years, the CRO industry has ushered in unprecedented prosperity.

Medicilon and Pharmaron have successively entered the secondary market, significantly boosting investor attention toward the CRO sector. In fact, the CRO industry has experienced rapid growth in the Chinese domestic market over the past three years.

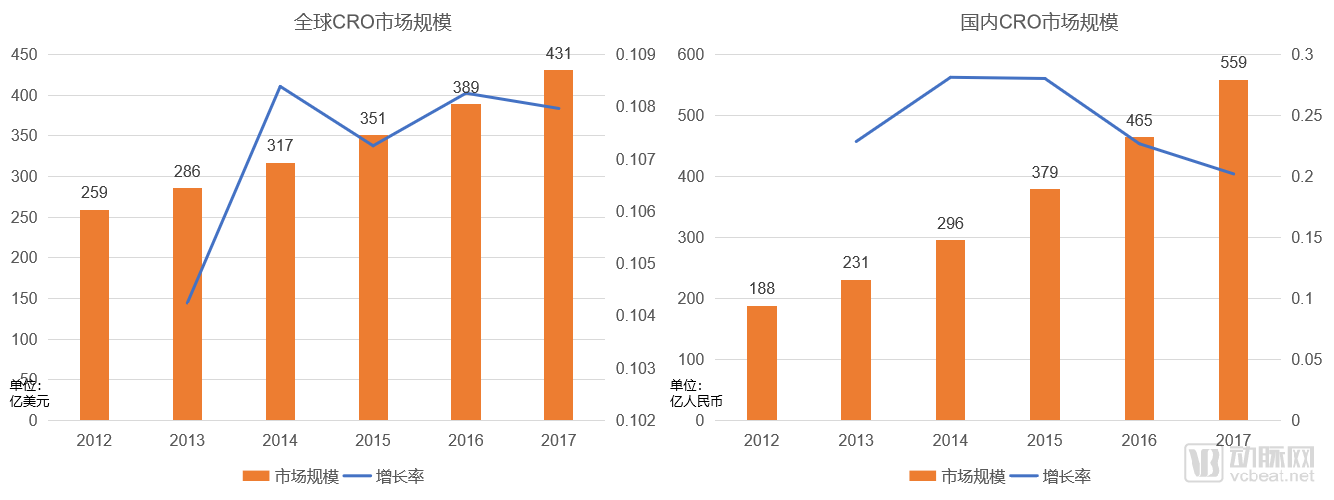

Global CRO Market Size (Data Sources: Frost & Sullivan, Nanfang Economic Research Institute, VCBeat)

According to prior market estimates by Frost & Sullivan, the global CRO market size exceeded $40 billion in 2017, with an annual growth rate consistently maintained at approximately 10%. Meanwhile, based on market size assessments of China’s CRO sector by the Southern Institute, the domestic CRO industry reached a market size of RMB 55.9 billion in 2017, with an annual growth rate of around 20%. Based on this, the domestic CRO market size in 2018 is estimated to be approximately RMB 65 billion.

Meanwhile, according to relevant statistics, the domestic CRO penetration rate in China was 31% in 2017, compared with 42% abroad, indicating substantial room for growth. Therefore, this growth rate is unlikely to encounter a bottleneck in the coming years.

CROs can help pharmaceutical companies shorten R&D cycles, reduce R&D costs, and mitigate risks.As an external resource that pharmaceutical companies can leverage, CROs can rapidly assemble a highly specialized and experienced research team in a short period, thereby shortening the new drug development cycle and reducing R&D costs. According to data from the Tufts Center for the Study of Drug Development, the involvement of CROs can reduce the duration of each stage of drug development by 25–40%, with an average reduction of 34.43%.

Currently, more than 50% of pharmaceutical companies worldwide engage CROs to assist in new drug development, aiming to reduce R&D costs and mitigate risks. Major global pharmaceutical companies are progressively deconstructing their internal R&D processes, leading to a continuous decline in the proportion of in-house developed drug pipelines. For non-in-house components, besides acquiring high-quality pipelines from biopharmaceutical companies, another major source is collaboration with preclinical CROs.

China’s pharmaceutical industry is undergoing a strategic transition from “generic drugs” to “innovative drugs.”China’s pharmaceutical industry is undergoing a period of transformation. The rapid growth of the domestic CRO sector has been driven by the boom in the innovative drug industry over the past two years, which has generated substantial demand for CRO services from innovative pharmaceutical companies.

Key Policy Initiatives Driving the Development of the Innovative Drug Industry in China in Recent Years

In August 2015, the State Council issued Document No. 44 [2015], titled “Opinions on Reforming the Review and Approval System for Drugs and Medical Devices” (hereinafter referred to as “Document No. 44”), officially ushering in a new era of regulatory reform for innovative drugs in China. Following Document No. 44, Document No. 42 [2017] of the General Office of the CPC Central Committee and the General Office of the State Council, titled “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices” (hereinafter referred to as “Document No. 42”), further emphasized the provisions outlined in Document No. 44, with particular focus on key areas such as “promoting drug innovation and the development of generic drugs,” “reforming clinical trial management,” “accelerating market approval review and processes,” and “strengthening lifecycle management of drugs and medical devices.” These four critical aspects are closely intertwined with the CRO industry.

In the following years, the efficiency of drug-related approvals improved rapidly. First, the application process for clinical trials under the registration system was changed to a filing-based system, reducing the approval time from 18 months to just 2 months. Second, the backlog of pending approvals was quickly cleared, and a priority review mechanism was established. The number of drug registration applications pending at the Center for Drug Evaluation (CDE) dropped sharply from 22,000 in September 2015 to 4,000 by the end of 2017, while the median review time for New Drug Applications (NDAs) decreased from over 400 days in 2013 to around 180 days in 2017.

Strictly controlled approval timelines have further boosted the enthusiasm of innovative drug companies for domestic filings in China. Many drugs originally planned for initial clinical trial applications abroad have adjusted their strategies to include China in global multi-center clinical trials. The number of clinical trials assigned a Clinical Trial Registration (CTR) number surged rapidly from 887 in 2015 to 2,570 in 2018, with the expanding market driving growing demand for Contract Research Organization (CRO) services.

The innovative drug industry is the primary downstream client base for the CRO industry.Long before the release of Document No. 44, numerous Chinese companies had already begun to establish their presence in the innovative drug sector. Representative domestic innovators currently at the forefront of the industry—such as Innovent Biologics, Junshi Biosciences, BeiGene, and Henlius Biotech—were all founded around 2010. Subsequently, driven by policy support, the innovative drug industry has continued to gain momentum, bringing unprecedented prosperity to the CRO (Contract Research Organization) sector.

Innovative pharmaceutical companies inevitably need to invest substantial R&D funding across multiple drug pipelines. While they possess well-established internal R&D processes, they typically outsource different stages of the R&D workflow to Contract Research Organizations (CROs) to enhance efficiency and reduce costs, thereby maximizing overall R&D productivity. In China, traditional generic drug manufacturers, driven by the requirements for consistency evaluation of generic drugs, also need to collaborate with clinical institutions on Bioequivalence (BE) studies, thus creating market opportunities for CROs. Furthermore, under the impact of Volume-Based Procurement (VBP), pharmaceutical companies are compelled to undergo business transformation; lacking sufficient in-house R&D capabilities, they increasingly rely on the support of CROs.

China’s accession to the ICH has brought more overseas business opportunities to domestic CRO companies.China formally joined the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) in June 2017, and subsequently issued guidelines in October 2017 and July 2018 to facilitate international multi-center clinical trials and accept overseas clinical data, marking a progressive alignment of China’s drug quality regulatory system with international standards.

Foreign pharmaceutical companies conducting clinical trials in China benefit from patient diversity and cost advantages. Under ICH standards, domestic clinical trial data are recognized by foreign regulatory authorities. Coupled with accelerated clinical trial approvals, this has led to a significant influx of international multi-center trials into China’s clinical CRO market.

In summary, the domestic CRO industry is experiencing rapid growth, particularly in the clinical CRO sector.Tigermed, the leading clinical CRO company listed on China’s A-share market, saw its revenue surge rapidly from RMB 1.17 billion in 2016 to RMB 2.3 billion in 2018. This growth has prompted companies such as WuXi AppTec and Pharmaron, which primarily focused on preclinical CRO services, to expand their operations downstream into the clinical sector.

Drawing on the development trajectory of the overseas CRO industry: In 1984, the United States enacted the Hatch-Waxman Act, which significantly streamlined the approval process for generic drugs. In the subsequent years, a large volume of generic drugs entered the market, leading to a substantial decline in revenues for originator pharmaceutical companies. Meanwhile, as the costs of new drug R&D continued to rise, pharmaceutical companies urgently needed to improve the efficiency of new drug development. This demand drove the rapid emergence of the overseas CRO industry in the 1990s. Quintiles (one of the predecessors of IQVIA), Covance, PPD, and Parexel were all established in the 1980s and rose to become global top-tier CRO enterprises during this wave.

Looking at the domestic landscape, the consistency evaluation of generic drugs and volume-based procurement are being vigorously implemented, compressing profit margins for generics to international levels. Consequently, Chinese generic drug manufacturers have a strong imperative to control R&D costs. Furthermore, the rapid internationalization of China’s pharmaceutical market has intensified R&D pressures on domestic pharmaceutical companies. Driven by this robust demand, China’s CRO industry is poised for rapid development.

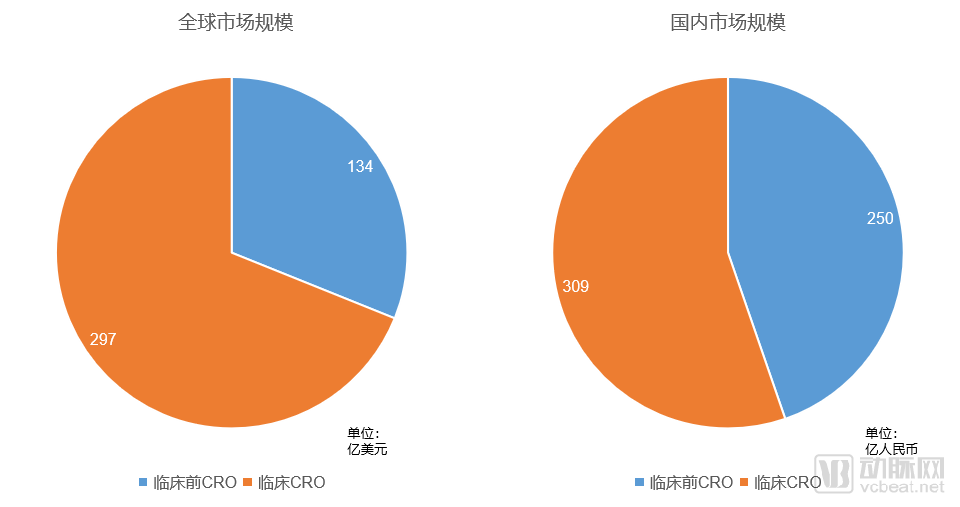

Distribution Ratio of Preclinical and Clinical CROs

Market Composition.In 2017, the global CRO market was valued at $43.1 billion, with the preclinical and clinical CRO segments accounting for approximately a 3:7 ratio. In contrast, the corresponding ratio in China’s domestic market was about 5:6, indicating a higher share for preclinical CROs. This disparity is partly attributable to the nascent stage of China’s innovative drug industry, which has driven strong demand for preclinical services, and partly reflects the significant untapped market potential remaining in China’s clinical CRO sector.

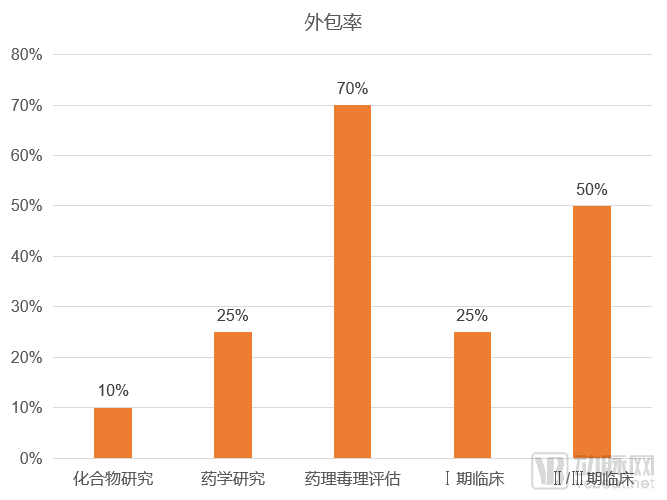

Outsourcing Rate Across All Stages of Drug Development

Outsourcing Rate in R&D.Among the various stages, outsourcing rates tend to be higher in the later phases, particularly in pharmacology and toxicology assessments and Phase II/III clinical trials. Earlier R&D processes are often closely tied to core patent protection, so companies generally keep these activities in-house. Additionally, pharmacology and toxicology assessments require specialized animal facilities; since most companies do not maintain dedicated animal housing, this segment has the highest outsourcing rate.

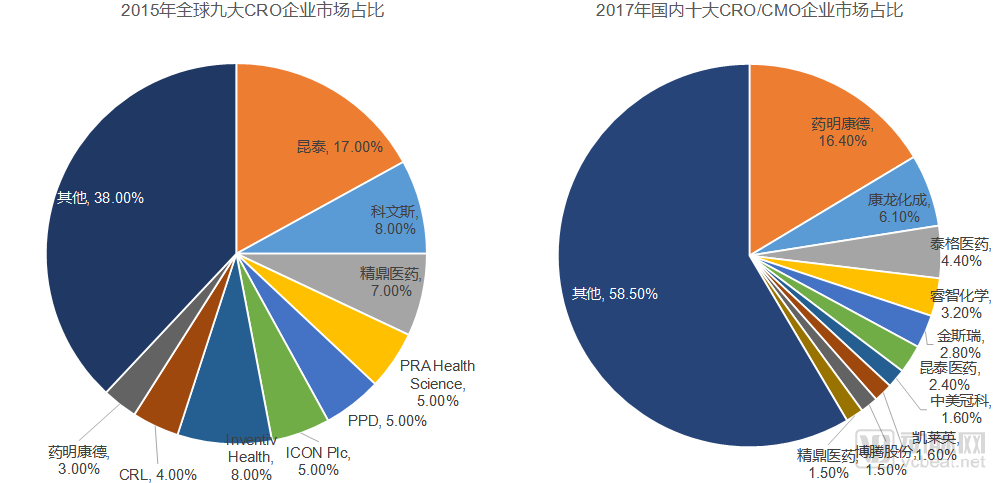

According to incomplete statistics, there are 525 CRO companies in China, primarily distributed in provinces and municipalities with relatively developed biopharmaceutical industries, such as Beijing, Shanghai, and Jiangsu. The top ten companies account for approximately 40% of the market share, compared to 60% globally, indicating that China’s CRO industry currently exhibits a relatively fragmented market structure.

China's CRO industry exhibits a clearly stratified competitive landscape, characterized by the prominence of leading firms and a large number of smaller players. Leading companies primarily undertake high-margin innovative drug projects, whereas smaller enterprises rely on cost advantages to handle lower-technology generic drug projects.

Market Share Comparison of Leading Domestic and International Enterprises (Data Sources: Frost & Sullivan, PharmCube, VCBeat)

Amid the intensifying volume-based procurement (VBP) in China, profit margins for generic drugs have been significantly compressed. Due to these market conditions, small contract research organizations (CROs) primarily engaged in generic drug services will face substantial setbacks. Consequently, resources within the CRO industry are expected to continue consolidating among leading enterprises, gradually reducing industry fragmentation.

Due to the strong economies of scale in the CRO industry, the market position of leading companies is highly solidified. In the preclinical CRO segment, competitiveness hinges on assets such as compound libraries and animal models, which require substantial accumulation over time and rely on experienced, high-caliber talent. For clinical CRO services, effective oversight of overall clinical trials demands extensive experience from clinical teams, while hospital resources necessitate long-term cultivation and maintenance by enterprises.

Meanwhile, the CRO industry exhibits extremely high customer stickiness. Large pharmaceutical companies are often very cautious in their selection of CROs; once a deep collaboration is established, a highly stable partnership is formed, and they are unlikely to change partners easily.

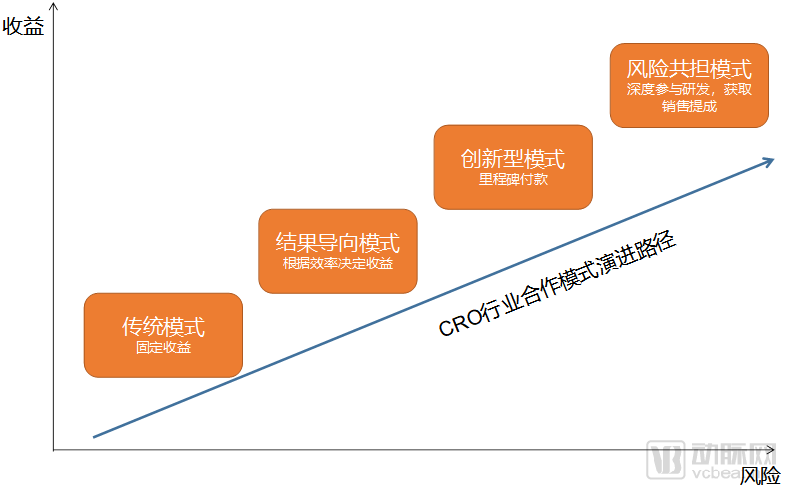

Evolutionary Path of Collaboration Models Between CROs and Pharmaceutical Companies

In the course of their development, collaboration models between CROs and pharmaceutical companies have been gradually evolving from traditional low-risk, low-return fixed-fee arrangements toward high-risk, high-return risk-sharing models. Initially, CROs collaborated with pharmaceutical companies on a simple “payment upon delivery” basis. Over time, outcome-based models emerged, wherein both parties set timelines and determined compensation based on the CRO’s completion efficiency. Milestone-based payments are currently the most common collaboration model between CROs and pharmaceutical companies. This shift implies longer project cycles, greater resource commitments from CROs, and increased risk exposure. Nevertheless, compared with innovative biopharma companies that generate revenue only after successful product commercialization, milestone payments enable CROs to secure short-term revenue streams.

The emerging risk-sharing model requires contract research organizations (CROs) to proactively assume risks in drug development. By providing pharmaceutical companies with support in funding, technology, and commercialization, CROs take on these risks in exchange for a share of post-launch sales revenues. This arrangement enables pharmaceutical companies to reduce R&D costs and mitigate the risk of potential development failures. Such a collaborative model necessitates that CROs provide more comprehensive coverage of the drug development process and engage more deeply in R&D activities.

In 2002, Eli Lilly and Quintiles collaborated to develop the antidepressant drug Cymbalta. Quintiles made a cash investment of $110 million before and after the drug’s launch and provided a sales team of more than 500 people. In return, Quintiles received 8.25% of Cymbalta’s annual U.S. sales revenue for the first five years and 3% annually for the subsequent three years. During the first eight years on the U.S. market, Cymbalta generated $14.474 billion in sales, yielding approximately $748 million in sales-based returns for Quintiles.

On the other hand, large pharmaceutical companies and small-to-medium-sized biopharmaceutical enterprises exhibit different demands for the CRO industry. Large pharmaceutical companies have comprehensive business layouts, and their needs for CRO firms are more focused on small, segmented outsourcing services. In contrast, most small-to-medium-sized biopharmaceutical enterprises mainly possess core technologies and do not conduct in-depth research on R&D and production processes outside of their core competencies. These companies prefer CRO firms to provide comprehensive solutions.

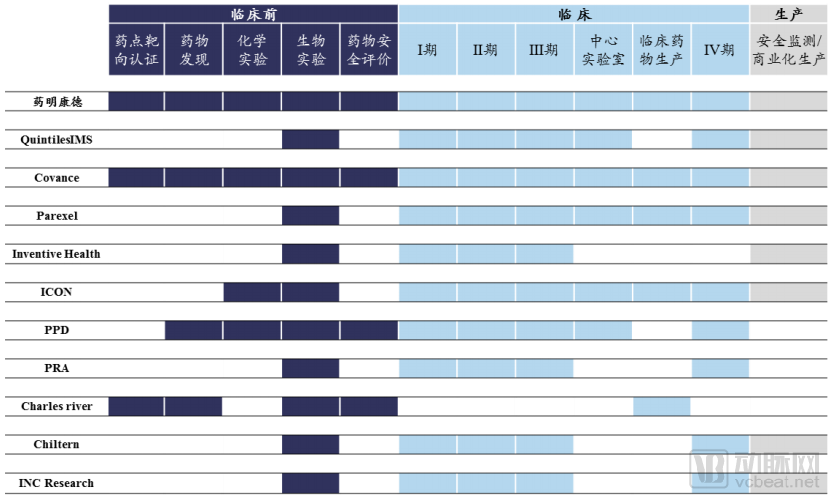

Global Leading CRO Companies’ Layout (Source: WuXi AppTec Prospectus, VCBeat)

Whether it is the new risk-sharing collaboration model or the emerging biopharmaceutical companies, both require CROs to possess the capability to provide comprehensive solutions. Leading global CROs are actively strategizing in this direction, and vertical integration across the R&D-to-manufacturing workflow will undoubtedly define the domestic CRO industry in China in the near future. This is precisely the path being pursued by leading Chinese CROs such as WuXi AppTec and Pharmaron.

Taking Pharmaron as an example, its original business was primarily focused on preclinical CRO services, and it later expanded into the CMO sector. By strengthening its clinical CRO capabilities, Pharmaron can integrate its preclinical CRO and CMO operations to provide customers with a one-stop R&D and manufacturing solution. Consequently, Pharmaron has been actively expanding in the clinical CRO field over the past two years. Revenue generated from its clinical CRO business reached RMB 80 million in 2018 and is likely to surpass the RMB 100 million mark in 2019.

CROs help pharmaceutical companies shorten drug development cycles, reduce R&D costs, and mitigate risks, becoming a critical component of the new drug development process. As a result, an increasing number of pharmaceutical companies are partnering with CROs for drug development. Offshore outsourcing demands from foreign pharmaceutical companies spurred the emergence of China’s CRO industry and drove its initial phase of rapid growth. Against the backdrop of the significant expansion of innovative drugs in China, the domestic CRO market is poised for a new round of sustained growth, making it the first subsector within the innovative drug landscape to reap substantial benefits.

References:

1. Medicilon's Prospectus for the STAR Market IPO;

2. Pharmaron’s Post-Hearing Information Pack for the HKEX Listing;

3. Prospectus for WuXi AppTec's Initial Public Offering;

4. China’s pharmaceutical industry undergoes radical restructuring, ushering in a golden age of growth for the CRO sector: Everbright Securities;

5. Supply-demand balance and efficiency gains sustain high industry prosperity, China Merchants Securities;

6. Three Questions and Answers on the CRO Industry, BOC International Securities;

7. A global CRO company with expanding capabilities and gradually realized scale, Minsheng Securities.