Will the Gene Testing Industry Rebound in 2020? | 2019 Annual Review: MGI Drives Upstream Acceleration and Pathogen Detection Emerges

For the NGS industry, 2019 was a long-awaited winter. Compared with $1 billion in 2017 and $986 million in 2018, the total financing amount this year has seen a precipitous decline. Investment enthusiasm has cooled rapidly; compared to the fiercely competitive landscape of a few years ago, the current NGS market has become more subdued. Companies are no longer rushing to enter the saturated “red ocean” market but are instead taking a more rational approach to identifying remaining market spaces and new opportunities.

As per our longstanding tradition, we will conduct a comprehensive review of the genetic testing sector, analyzing industry trends and future trajectories by integrating investment and financing data with major industry developments.

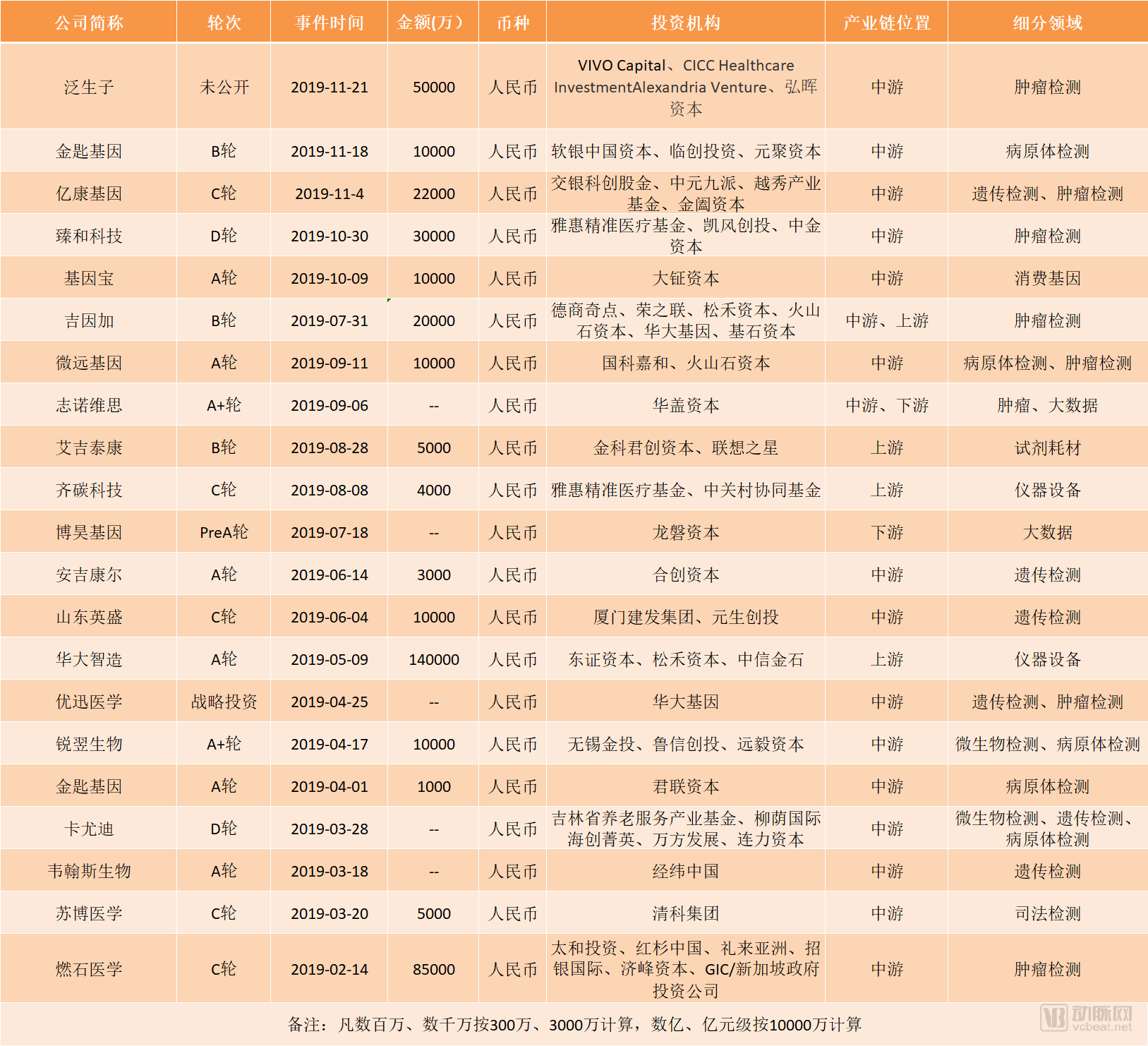

First, let’s take a look at this year’s financing details:

Data sourced from the VCBeat Knowledge Base

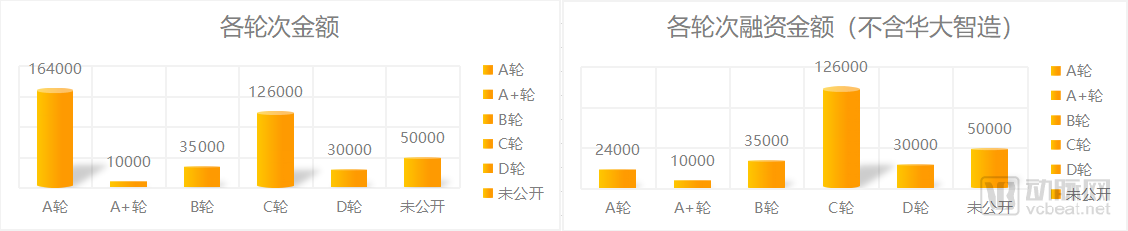

Similar to the overall trend last year, most of this year’s financing was concentrated in companies at relatively early to mid-stages, with only one company raising funds prior to Series A. The majority of capital flowed into Series A rounds, with these companies collectively raising RMB 1.64 billion; Series C followed, with these companies raising a total of RMB 1.26 billion; while companies at Series B, Series D, and later stages raised RMB 350 million and RMB 300 million, respectively.

If judged solely by funding rounds, capital appears to prioritize emerging companies with preliminary validation of their business logic or technology and rapid growth. However, we note that among companies completing Series A financing, MGI Tech announced in May the completion of a $200 million round (approximately RMB 1.4 billion). MGI Tech has already launched several sequencer products, delivered its initial orders, and media had previously speculated that the company might be planning an IPO on the Hong Kong Stock Exchange. Therefore, despite being at the Series A stage, MGI Tech is not a company in the early R&D phase. Only by removing this “top-scoring” outlier can we perhaps discern the true direction of this year’s investment and financing market.

Financing Amounts by Round (Unit: 10,000 Yuan)

After excluding MGI Tech’s financing data, the total amount of Series A funding in the gene industry reached RMB 240 million. In November, Genetron Health announced the completion of a new round of financing worth RMB 500 million. Although the specific round was not disclosed, it is certain that this financing occurred after its Series C round. Capital markets grew more conservative throughout the year, with funds flowing toward mature, late-stage companies that had already achieved partial success.

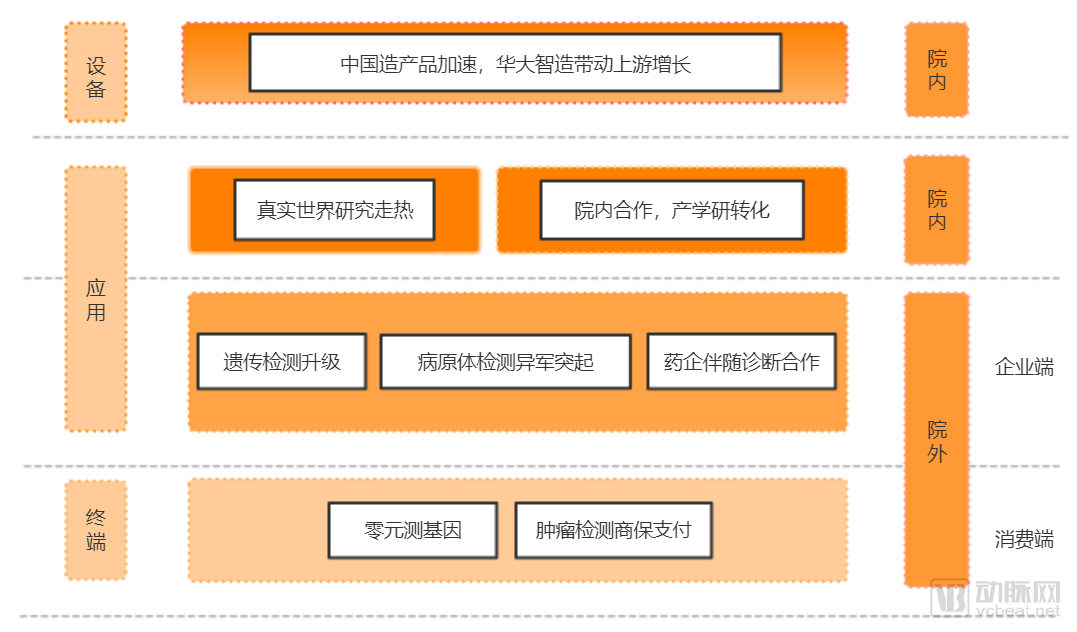

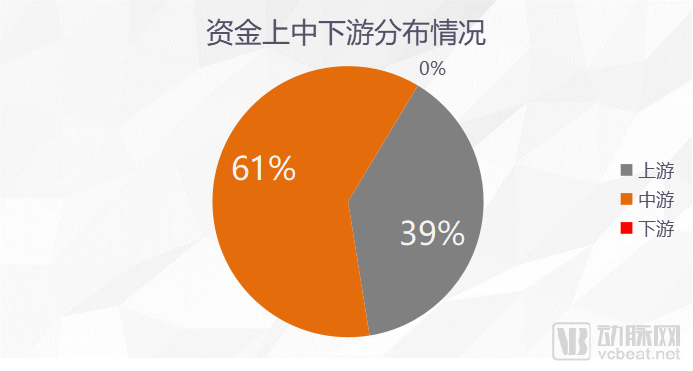

A closer look at capital flows reveals that, compared to the concentration of funds in midstream application segments, the share of financing in upstream sectors has increased this year.

The financing ratio between the upstream and midstream segments of the industrial chain stands at 6:4, while the downstream segment accounts for 0%. This is attributable to the rise of domestic manufacturers of instruments, equipment, and consumables, represented by MGI Tech.

In May 2019, MGI Tech completed a $200 million Series A financing round provided by CITIC, Goldstone Investment, Pinehe Capital, and Dongzheng Capital, setting this year’s transaction record in China’s genetic testing sector.

One month later, MGI Tech unveiled its “high-definition” assembled genome solutions and standards based on its proprietary DNBSEQ™ sequencing technology and stLF at the European Human Genetics Conference, truly ushering genomic sequencing into the “Full HD” era.

On September 9, the DNBSEQ-T7 (hereinafter referred to as T7), an ultra-high-throughput gene sequencer independently developed by MGI Tech, was officially delivered for commercial use. It is reported that the first batch of sequencers has arrived at the laboratories of companies such as BGI Genomics and WeGene. This commercial delivery marks the first step in the marketization of domestically produced sequencers. It is revealed that this move will help China’s gene sequencing industry further break through the technological barriers imposed by overseas companies, achieving leadership in both sequencing equipment technology and cost-effectiveness. MGI Tech stated that with the commercial deployment of the T7, the cost of personal whole-genome sequencing is expected to drop further to below $500.

In addition to MGI Tech, several other domestic manufacturers of sequencing instruments have also achieved gains this year. Since 2016, Genetron Health has implemented a strategy of securing all three certifications—for sequencers, reagents, and software—and leveraged more than 100,000 tumor genomic data sets, aiming to make significant strides in the high-throughput tumor sequencing sector. In September 2019, Genetron Health’s two sequencer models, Gene+Seq-200 and Gene+Seq-2000, received approval from the National Medical Products Administration (NMPA) for market launch.

Geneplus officially launched the Gene+Seq-200/2000 sequencing platforms during the CSCO conference on September 20. Unlike other sequencers, the Gene+Seq-200/2000 was specifically developed for oncology applications. Based on the DNB (DNA Nanoball) sequencing technology and equipped with proprietary X-shaped adapters, these instruments meet the highest standards for sequencing technologies, particularly in liquid biopsy.

Currently, the Gene+Seq-200/2000 platform has achieved stable operation with large sample volumes in the laboratory. Based on this platform, Genetron Health has achieved perfect scores in multiple authoritative quality assessment programs both domestically and internationally.

Qitan Technology, a player in the nanopore single-molecule sequencing sector, also completed its RMB 40 million Series C financing round this year. The investors in this round include the Zhongguancun Collaborative Innovation Fund and the Yahui Precision Medicine Fund. Prior to this round, Qitan Technology had cumulatively raised RMB 23 million from investors such as angel investment firm Heli Investment, Huakong Cornerstone Fund, and venture capital firms including Baidu Ventures.

In 2018, Qitan Technology began filing domestic patent applications for proprietary intellectual property rights, including speed-control proteins. Meanwhile, the company continued to iterate on its proof-of-concept prototype, expanding the channel count from 16 to 64 and improving the accuracy of its sequencing data analysis algorithms from 80% to 90%. As of August 2019, Qitan Technology had completed the development of the engineering prototype for QNOME-6410, its first nanopore sequencer with independent intellectual property rights, and planned to launch a minimum viable product in early 2020.

Some Companies Venturing into the Upstream Sequencer Market

However, these sequencers are still in the early stages of commercialization or R&D, and the market is currently dominated by products from Illumina and Life Technologies. In clinical practice, the applications of most sequencers remain limited to non-invasive prenatal testing (NIPT), leaving significant market potential yet to be explored.

In July 2019, Berry Genomics announced that the intended use of the NextSeq CN500 gene sequencer, co-developed with Illumina, had been updated. The revised intended use is stated as: “For sequencing human deoxyribonucleic acid (DNA). Clinically, this instrument may be used in conjunction with in vitro diagnostic reagents approved by China’s National Medical Products Administration and the accompanying random-access software provided with the instrument, and it is not intended for whole-genome sequencing or de novo sequencing of humans.” This means that the NextSeq CN500 has become the first general-purpose next-generation sequencing (NGS) platform currently available for immediate large-scale clinical genetic testing.

This expansion of the applicable scope has been hailed as a milestone by China’s gene sequencing industry, signifying that NGS has moved beyond NIPT in clinical practice to encompass a broader range of diseases.

On November 13, Genetron Health also announced that its developed sequencer, “GENETRON S5,” had officially received market approval from the National Medical Products Administration (NMPA), securing entry into the upstream market.

In the reagents and consumables segment, AgiTech completed a RMB 50 million Series B financing round in May this year. Furthermore, China released its first national standard for gene capture this year, titled “GB/T 37872-2019 General Principles for Quality Evaluation of Target Gene Region Capture.” As a representative enterprise of “Made-in-China” gene capture technologies, AgiTech participated jointly in the drafting of this standard. The General Principles specify methods and requirements for evaluating the quality of target gene region capture. Serving as the national-level basis for assessing applications of target gene region capture technology, it provides framework guidance for quality evaluation in the genetic testing industry.

In the financing rounds of previous years, the vast majority of capital was concentrated in midstream application segments, making domestically produced sequencers a scarce commodity. However, with the rise of Chinese brands such as MGI Tech and AgiBio, we are witnessing Chinese ingenuity at the upstream end of the industry chain. This also signals that the NGS industry is shifting from technology application to the research, development, and optimization of foundational technologies, with the most critical upstream technologies increasingly transferring to China.

Furthermore, we can observe that the application scope of sequencers is shifting toward tumor detection. The expansion of the intended use for Berry Genomics’ sequencers signifies that oncology is being positioned as the next core area of development; meanwhile, the sequencer approved for Gene+ was specifically developed for tumor detection. Coupled with the sequential approval of multiple clinically applicable tumor detection kits, we can predict that a battle for market dominance in tumor detection is imminent in the next phase.

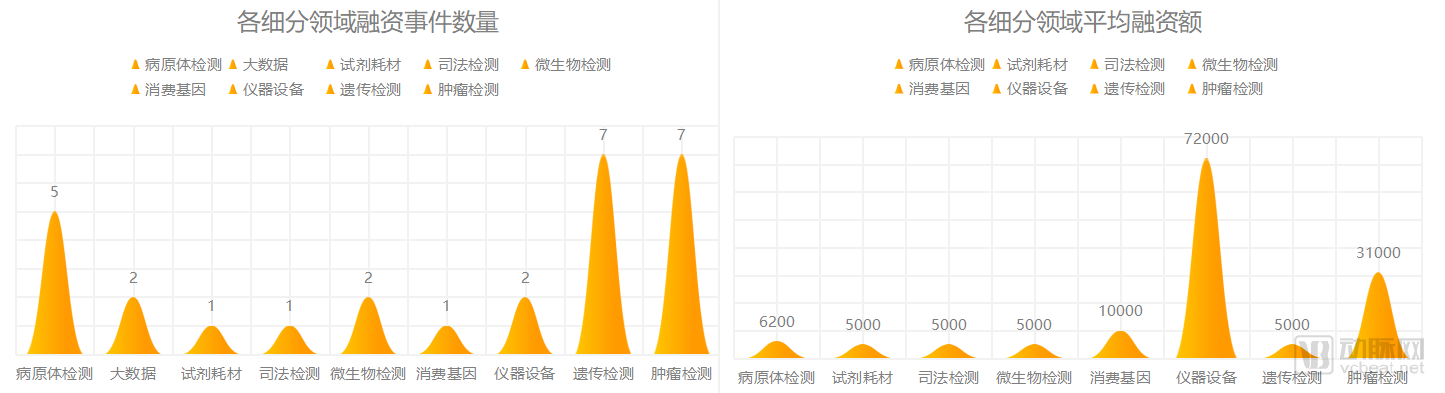

In addition to the upstream segment of instruments and equipment, another area worthy of attention is cancer detection. Among 20 financing rounds, four were related to cancer detection, with both the average financing amount and total financing volume ranking among the highest.

Number of Financing Deals and Amount Raised by Sector (Amount in RMB 10,000)

Tumor testing is a relatively active niche within the current NGS landscape, with multiple companies having established partnerships with upstream instrument manufacturer Illumina. This trend may indirectly indicate that the market size for tumor testing is expanding. Furthermore, this year, as the concept of precision therapy continues to gain traction, we have observed a marked increase in interactions between tumor testing companies and oncology pharmaceutical firms.

On June 24, AmoyDx announced that it had entered into a clinical research collaboration agreement with LOXO ONCOLOGY, a subsidiary of Eli Lilly and Company, for marketed drugs. According to the announcement, AmoyDx’s independently developed “AmoyDx® EGFR/KRAS/ALK Fusion Gene Mutation Detection Kit (PCR-Fluorescence Probing)” (“AiHuiJian”) and “AmoyDx® Pan-Cancer Gene Mutation Detection Kit (NGS)” (“WeiHuiJian”) will serve as companion diagnostics for LOXO ONCOLOGY’s cross-indication RET inhibitor, LOXO-292, in clinical trials across Asia. The products covered by the agreement include “AiHuiJian,” a multi-gene combined detection assay based on the PCR platform, and “WeiHuiJian,” a genetic testing product based on the NGS platform. Both products received market approval in August and November of last year, respectively.

On July 8, KingMed Diagnostics entered into a strategic cooperation agreement with Merck regarding genetic testing for colorectal cancer. Both parties will jointly focus on precision diagnosis and precision treatment of colorectal cancer in China, and work together to promote the standardization and normalization of molecular biomarker testing (including RAS/BRAF) for colorectal cancer, thereby helping physicians and patients select optimal treatment regimens.

In this regard, AstraZeneca has made the most significant investment among pharmaceutical companies. On August 20, the global leading biopharmaceutical company announced that it had signed a strategic cooperation agreement with Merger Diagnostics in Shanghai, aiming to leverage their respective advantages in treatment and diagnosis to establish a sustainable clinical diagnostic therapy ecosystem. Under this agreement, AstraZeneca formed alliances with nine companies, including KingMed Diagnostics, Dian Diagnostics, Kunyuan Genomics, Zhenhe Technology, Herui Genetics, GenePlus, AmoyDx, Ruidiagene, and the Zhiai Huhe Online Testing Platform.

It is understood that this collaboration aims to enhance China’s technical capabilities in genetic testing and precision diagnostics, while improving awareness among physicians and the public regarding standardized practices for the diagnosis and treatment of cancers caused by genetic mutations.

On October 9, Novogene and Chipscreen Biosciences successfully signed a collaborative agreement for the development of companion diagnostic products for novel oncology drugs. Novogene will develop detection assays based on the list of genes and loci provided by Chipscreen Biosciences, and construct positive and negative reference standards to validate the analytical performance of these assays. If the performance targets are met, Chipscreen Biosciences will utilize this assay to screen and stratify patients in its Phase II clinical trial of Chidamide (also known as CS055 or Tucidinostat) for small cell lung cancer, and to investigate whether the covered genes and loci can predict the therapeutic efficacy of Chidamide.

Novogene will develop detection methods based on the list of genes and loci provided by Chipscreen Biosciences, and construct positive and negative reference standards to validate their analytical performance. If the product meets the performance targets, Chipscreen Biosciences will use this assay to screen and stratify patients in the Phase II clinical trial of Theanorine for small cell lung cancer. Meanwhile, studies will also be conducted to determine whether the covered genes and loci can be used to predict the efficacy of Theanorine.

Microchip Biotech shall pay Novogene outsourcing service fees on a per-test basis for services included in the collaboration, such as R&D of testing methods and clinical trial sample testing. Upon verification of relevant phased results in subsequent cooperation, Microchip Biotech shall pay Novogene corresponding milestone payments. For the aforementioned service fees and milestone payments, both parties will negotiate and enter into contracts at appropriate times based on project progress.

Pharmaceutical companies began venturing into the genomics sector as early as 2014. However, in those earlier years, their involvement primarily took the form of equity investments, acquisitions, joint ventures, or establishing in-house capabilities, with participants largely consisting of large-cap listed companies and traditional pharmaceutical firms. Notable examples include Beilu Pharmaceutical’s investment in Geneseeq, Double-Crane Pharmaceutical’s equity stakes in FanShengZi and Annoroad Gene Technology, Kangmei Pharmaceutical’s establishment of Kangmei Biotechnology, and WuXi AppTec’s creation of its subsidiary, BGI Tech Solutions (formerly NextCODE Health). These engagements were predominantly capital-driven, with limited substantive business collaboration between pharmaceutical companies and genomics firms. Significant discrepancies existed between the two parties in terms of market objectives and strategic approaches.

This year, these interactions have seen greater participation from multinational pharmaceutical companies, with collaboration models shifting from mere capital investment to substantive business partnerships. This trend not only reflects multinational pharma’s recognition of the technological prowess of domestic NGS companies but also underscores their growing emphasis on genetic testing technologies, as diagnosis and treatment in precision medicine begin to truly converge. These developments are the fruit of years of diligent efforts by NGS enterprises.

In addition to pharmaceutical companies, hospitals are also deepening their collaborations with testing firms. Notably, Berry Genomics’ subsidiary, Herui Gene, has established a joint research center with Shanghai Chest Hospital.

On September 6, Huirui Gene and Shanghai Chest Hospital announced the establishment of the “Shanghai Chest–Huirui Gene Precision Medicine Research Center.” The center will leverage their respective strengths in clinical resources, genetic testing, and big data analytics. By effectively integrating accurate clinical information with genomic data, it will conduct clinical research on precision oncology therapy and cutting-edge scientific studies. This initiative aims to drive clinical translation and technology implementation through research, enabling cancer patients to benefit from personalized precision medical services at an earlier stage. Reportedly, this will be the first precision medicine research center for thoracic cancers in China.

Of course, co-establishing research centers imposes extremely high requirements on a testing company’s technological and financial capabilities. In contrast, more companies are currently choosing to collaborate with Principal Investigators (PIs) at hospitals to facilitate product translation and validation. As predicted in our 2018 review, real-world studies have rapidly gained momentum this year.

Since 2017, Burning Rock Biotech has initiated five prospective real-world study projects. At this year’s CSCO conference, real-world studies accounted for a significant proportion of the satellite symposium presentations; indeed, they took center stage at the satellite symposia hosted by multiple companies, including Burning Rock, Novogene, and Genetron Health.

Real-world studies are typically led by hospitals, with multiple centers often participating simultaneously in a single project. This presents an excellent opportunity for companies to understand clinical needs, accumulate clinical resources, and validate product performance. However, coordination and communication among the various centers become crucial, posing a major challenge at present. Furthermore, clinical researchers need to conduct more extensive data analyses to enhance the significance of these studies. In this process, genetic testing technologies are bound to drive the development of clinical research, steering it toward greater precision and depth.

The sudden surge in interest in real-world evidence (RWE) stems from the emerging limitations of randomized controlled trials (RCTs) as disease research deepens. RCTs impose stringent criteria for indication selection and participant enrollment, yet clinical drug use involves greater variability than observed in RCTs, both in terms of patient conditions and adherence. Particularly in complex diseases such as cancer, it is essential to monitor therapeutic efficacy during actual drug administration and to validate the practical utility of biomarkers in companion diagnostic products. As next-generation sequencing (NGS)-based tumor testing becomes more widely adopted in hospitals and the concept of precision medicine gains deeper traction, research based on real-world data will inevitably become a prevailing trend.

In May 2019, the Center for Drug Evaluation (CDE) released the “Basic Considerations on Using Real-World Evidence to Support Drug Development (Draft for Comment)” (hereinafter referred to as the “Basic Considerations”). This represented a key policy signal in China, indicating that the CDE had provided clear definitions for concepts related to real-world studies. In fact, both China and the global community had already taken significant steps forward in the field of real-world research. As of September 2019, according to incomplete statistics, more than 1,700 studies registered on ClinicalTrials.gov included keywords related to “Real World,” with over 180 registrations originating from China. These studies covered multiple therapeutic areas, including oncology, cardiovascular diseases, endocrinology, liver diseases, and adverse drug events.

Within hospitals, clinical institutions are also exploring the integration of genetic technologies with clinical testing. The First Hospital of China Medical University spearheaded the launch of the Liaoning Provincial Clinical Diagnosis and Treatment Integration Center this year, under which patients at the initial 23 participating hospitals will receive standardized, unified multidisciplinary care. According to reports, under the medical model of the Lung Cancer Diagnosis and Treatment Integration Center, genetic testing is incorporated alongside routinely applied clinical methods such as thoracic CT scans, biopsies, and pathological examinations.

Overall, the concept of precision medicine, exemplified by genetic technologies, has brought revolutionary changes to clinical diagnosis and treatment, thereby increasing the acceptance of emerging technologies in clinical practice. However, it is undeniable that interaction between clinical research and industry remains fragmented, with silos persisting across various stages. Institutions with clinical resources lack technological platforms, while enterprises with technological platforms lack access to clinical resources and high-quality clinical data. The polarization between resources and technology has become increasingly pronounced, making collaborative exploration perhaps the only viable solution currently imaginable.

“Previously, clinical institutions and enterprises operated in silos without integration. Now, we aim to collaborate closely, leveraging clinical data and technological advantages to conduct in-depth exploration, extract valuable insights, validate them in clinical practice, and then promote industrialization to benefit more patients,” said Pan Changqing, President of Shanghai Chest Hospital.

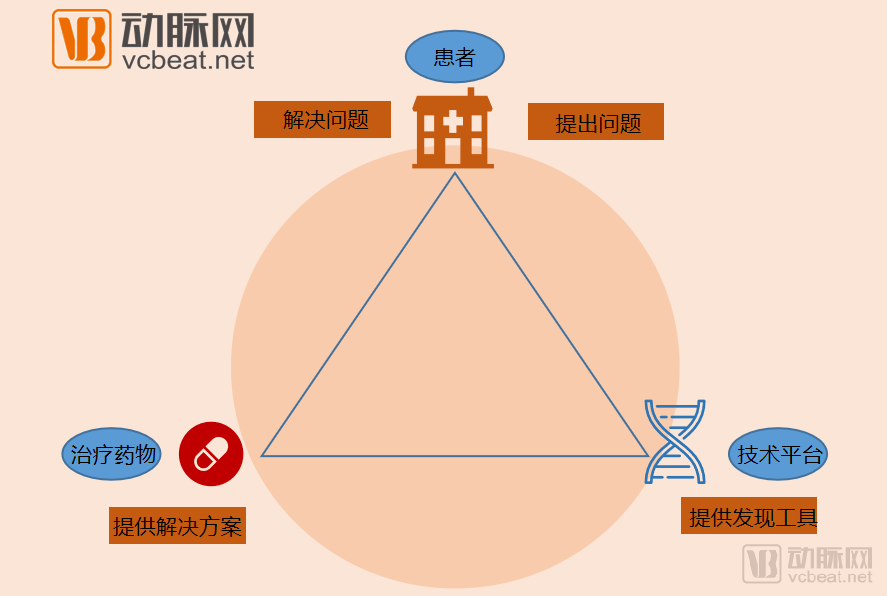

In the process of precision medicine, genetic testing companies, hospitals, and pharmaceutical companies are all indispensable for detection, diagnosis, treatment, and medication. In this triangle, genetic testing technology plays a connecting role. As the connection between technology and clinical practice, as well as disease treatment, becomes more precise, this triangular relationship will become even stronger, and there may be more opportunities for interaction and cooperation among these three parties in the future.

The "impossible trinity" in healthcare posits that as product quality and service delivery channels improve, the growth rate of healthcare costs rises in tandem. This phenomenon is particularly pronounced in the field of oncology testing. However, genetic testing is fundamentally a probabilistic prediction based on big data analytics. If high-cost tests, priced at tens of thousands of yuan, fail to guarantee 100% accuracy and efficacy, users’ willingness to pay will inevitably decline.

At this juncture, companies have made substantial investments in market and user education, which inevitably drives up product costs. Breaking the “impossible triangle” of healthcare requires introducing new incremental value, whether through technological breakthroughs or innovative service models. This year, the entry of insurance payers has stirred some ripples in the industry.

Genetic testing is, in essence, a form of risk selection. Based on this characteristic, there is room for insurance payment to intervene. Since 2016, the industry has been exploring ways for insurance to get involved. The products launched at that time were mostly consumer-oriented tests, with genetic testing companies primarily providing the testing products, while insurers held greater control. Due to the loose connection between biotechnology and insurance payment, this initial attempt ultimately came to nothing.

This year, two oncology testing companies successively reached collaborations with commercial insurance providers, marking the first integration of commercial insurance into the genetic testing and payment processes. In February, Geneseeq partnered with Beijing Jianyibao and Shanghai Nuohui Medical to launch China’s first innovative payment insurance plan targeting oncology testing and therapeutic medication, titled “Oncology Testing and Combination Therapy Insurance.” The initial phase of this insurance coverage includes gene mutations in ERBB2 (HER2), BRCA1/2, EGFR, ALK, and ROS1. In July, Geneseeq further announced a collaboration with Yuanxin Huibao Network Technology, with both parties joining forces to develop an innovative service model combining “NGS Oncology Testing + Disease & Medication Management.”

Also in July, Zhenhe Technology announced strategic partnerships with Nuohui Medical and Beijing Jianyibao, launching the “Lung Cancer NGS Testing and Combination Therapy Coverage Plan.” The initial phase of the plan will provide coverage for lung cancer patients with EGFR, ALK, or ROS1 gene mutations.

In this collaboration, product sales are no longer driven by insurance companies; instead, insurance products are bundled as complimentary offerings within testing service packages. If a patient does not respond to medication guided by the test results, the insurer will provide compensation. This model alleviates patients’ concerns about undergoing pharmacogenetic testing, while the insurer’s involvement serves as an endorsement of the test’s accuracy.

Although the product offerings remain relatively limited, this marks the beginning of explorations into oncology testing and commercial insurance payment models. If this model is validated, a broader range of oncology-related products may gradually emerge in the future; the current “medication insurance” products are merely the prelude to a larger narrative. The industry has taken its first step toward exploring new business models for oncology testing and innovative payment mechanisms for oncology diagnosis and treatment.

The data from the genetic testing sector this year is also surprising. Although the total financing amount was not the highest, it recorded the largest number of financing deals among all sectors. The genetic testing market has been dominated by several major companies, including BGI Genomics, Berry Genomics, CapitalBio, and Da An Gene. What entry points remain for emerging startups in this field?

We examined seven genetic testing companies that secured financing this year and identified the following characteristics:

1. Avoid the NIPT market and focus on the field of genetic disorders;

2. Break through market scenarios, covering pre-conception, newborns, and healthy populations;

3. Focus on genetic diseases with high severity and incidence rates.

All companies have chosen to avoid direct competition in the NIPT market, with most opting for application scenarios such as preconception screening and newborn screening, which cover a broader population than the prenatal screening market. These companies’ applied research continues to focus on reproductive health, and the market development efforts for NIPT in recent years have effectively provided preliminary market education for them. However, since BGI Genomics and Berry Genomics have both entered fields such as monogenic genetic testing, these companies will inevitably compete head-to-head with these industry giants.

The consumer testing market has undergone significant changes this year, with several new companies backed by major corporations making a strong entry.

In February 2019, Berry Genomics and Prenetics Limited jointly announced that Circle Gene, a consumer genetic testing company in which they had made a joint investment, had completed the formation of its core management team and would commence operations by the end of the second quarter.

Shanghai Jiexi Biology launched the consumer genetic testing brand Anwo Gene in 2018. According to Qichacha, the ultimate controlling shareholder of Jiexi Biology is Yuan Jianzhong; it remains unclear whether this is the same person as Yuan Jianzhong, the former General Manager for China at BGI (formerly known as Mingma Biology), a subsidiary of WuXi AppTec.

Shenzhen-based Genebox has also been shortlisted this year. Since its establishment in April 2018, the company has completed two rounds of financing totaling nearly RMB 140 million. During its angel round, Genebox brought in Dashenlin, one of China’s four largest chain retail pharmacies, as a strategic investor.

Like a few sudden disruptors, the entry of these companies has driven pricing in the already price-war-ridden consumer-grade genetic testing market to rock-bottom levels. At the start of 2019, Genebox entered the market with genetic testing services priced at just RMB 9.9, while its routine testing panels were offered at three price tiers: RMB 38, RMB 68, and RMB 88. 23Mofang and Yuan Gene successively partnered with JD.com to launch limited-quantity “Zero-Cost Genetic Testing” promotions, with the former even introducing a long-term free testing product.

23Mofang responded that “zero-cost genetic testing” represents a shift in its marketing strategy, moving from past reliance on key opinion leader (KOL) promotions to current user education efforts. “23Mofang has long adhered to a sales model driven by KOL placements, but in recent years we have gradually come to believe that the era of KOLs has passed,” said a relevant company representative. “The cost of such placements is high, yet their effectiveness has declined compared to previous years. We believe it is necessary to adjust our corresponding business model.”

Whether leveraging key opinion leaders (KOLs) or offering “zero-cost screenings,” new products require substantial investment in market education to gain traction. A review of rapidly emerging brands in recent years, such as Didi, Ele.me, and Luckin Coffee, reveals that they all secured market share and educated consumers through extensive discounts and promotional offers.

In terms of distribution channels, 23Mofang and WeGene primarily rely on online sales, while new market entrants have introduced some novel elements to the sales channel landscape.

Leveraging Dashenlin’s chain store network, Genebox has implemented a dual-channel “online + offline” operational model; Anwo Genomics conducts targeted promotions through channels such as Babytree, Suning, JD.com, and Kidswant; Yuan Gene focuses on e-commerce platforms, leveraging traffic from celebrity key opinion leaders (KOLs), and has established an offline presence in Watsons stores...

Whether through internet channels, e-commerce, or offline platforms, these companies have invested substantial resources in marketing. However, market competition is not solely driven by price. Currently, none of these companies have established particularly clear monetization pathways. The competition for traffic is essentially a competition for data, yet the practical utility of this data remains unclear—no one has found a definitive answer. Should they seek payment from pharmaceutical manufacturers, or partner with health management enterprises? How can this data be effectively leveraged? Whoever first identifies a viable path forward may well hold the key to success.

Historically, the applications of genetic testing have been primarily confined to hereditary diseases, oncology, forensics, gut microbiota analysis, and consumer-grade testing. Due to a lack of new exploratory directions, homogenized competition at the application level has been severe. This year, however, the industry appears to have made new discoveries in exploring novel applications. We have taken note of an emerging player.

The company, named Jinshi Genomics, was established in 2017 but made its public debut in 2019. Jinshi Genomics primarily focuses on medical diagnostics related to pathogen detection and is led by Dr. Jiang Zhi, founder of Novogene. Additionally, we have engaged with another enterprise, Jieyi Biotechnology, which is also exploring pathogen detection; however, its technological approach combines next-generation sequencing (NGS) with gene editing.

Meanwhile, microbiology research firm RayBiotech, medical testing company Kayou Diagnostics, and Weiyuan Genomics have all launched pathogen detection products this year. After Jinshi Genomics was the first to announce its financing, the sector appeared to ignite almost overnight.

Applying high-throughput sequencing technology to pathogen diagnosis to address key challenges in detection rates, timeliness, and accuracy, thereby enabling timely and precise diagnosis for numerous patients with severe infections.

According to statistics from the World Health Organization, three of the top ten leading causes of death worldwide are infection-related diseases. In China, there are over 10 million cases of infections annually, with more than one million deaths attributed to infections, most of which lack a confirmed etiology. Current conventional diagnostic methods for infections, such as microbial culture, PCR, and mass spectrometry, suffer from either low detection rates or low throughput, failing to address the critical challenges in clinical diagnosis.

On the other hand, the genetic testing industry has been highly favored by venture capital firms in recent years, with substantial capital influx into its major sub-sectors and the emergence of a number of star companies. In contrast, the diagnosis of severe infections integrated with genetic testing technology remains a blue-ocean market.

Based on the number of companies entering the pathogen detection market this year and the level of capital attention they have received, it is evident that the market is eagerly anticipating broader applications of NGS technology. But is pathogen detection alone sufficient? Certainly not.

In China, over 1 billion cases of infection occur annually, yet the vast majority of these common infections can be managed through empirical treatment and routine diagnostic methods. Statistics indicate that approximately 20 million people suffer from complex and critical infections each year. Although this figure exceeds both the annual number of new births and the number of newly diagnosed cancer cases in China, the market size for such infections does not surpass the combined market of these two sectors. It is important to recognize that the current capacity of the genetic testing, oncology testing, and consumer health testing markets to accommodate enterprises is also limited.

The rise of pathogen detection has been driven by the decline in sequencing costs in recent years. While empowering pathogen detection, it also holds future potential in other markets. Homogeneous competition is currently a weakness in the NGS industry. To maintain investors’ interest and enthusiasm, the industry needs to periodically introduce innovations and empower more testing and diagnostic processes.

Of course, the decline in sequencing costs extends beyond pathogen detection. The emergence of CRISPR technology in 2013 has made gene editing more commercially accessible. Paired with gene sequencing, this technology has driven the development of cutting-edge fields such as precision drug R&D, cell therapy, gene therapy, microbiome-based therapeutics, and synthetic biology. As a critical enabling technology, gene sequencing is likely to see synchronized growth in demand across these applications, suggesting that the market for sequencing services may experience modest growth.

In consumer- or patient-oriented sequencing applications, whether for non-invasive prenatal testing (NIPT) or whole-exome sequencing, the floor prices in the Chinese market are significantly lower than those in Europe and the United States. The consumer genomics market has even seen the emergence of “zero-cost testing” products. Driven by these price breakthroughs, such applications are poised to reach a broader consumer base. Beyond expanding the existing market, more importantly, these products will help many genomics companies conduct early-stage market education, laying the groundwork for wider market adoption.

In the oncology market, in addition to companion diagnostic products, some companies are engaged in research on early cancer screening. Compared with companion diagnostics, this application has a higher threshold and greater difficulties in approval and implementation. However, we have noticed that after achieving initial success in companion diagnostics, Burning Rock Biotech publicly announced its early cancer screening project this year. Early cancer screening represents a larger market, and as more companion diagnostic products obtain registration certificates, more companies may begin to lay out their strategies in the field of early screening.

It is generally believed that once the crux of a problem is grasped, everything else will fall into place. So, what was the core issue behind the cooling of financing in 2019?

First, there is a capital shortage in the capital markets; investment institutions are facing relatively difficult fundraising conditions and are therefore more cautious and conservative in their selection of investment targets.

Secondly, there are few cases of exit through IPOs; apart from BGI Genomics and Berry Genomics, no other companies in the industry have gone public.

Once again, there is severe homogenized competition. Capital has poured substantial funds into testing fields such as oncology, genetic diseases, and consumer health, with most investors already having established their positions. However, beyond these applications, few new directions have emerged.

Finally, a valuation bubble emerged in tandem with the industry’s surge in popularity, with excessively high valuations for some companies deterring certain investment institutions.

To forecast the investment and financing sentiment for 2020, it is first necessary to review whether the aforementioned issues have been resolved. The volume of capital fundraising and the number of companies filing for IPOs have not changed significantly. However, we note that Novogene updated its prospectus on November 2 (having initially filed on December 24, 2018); Genetron Health, after completing a new round of financing, promptly filed its prospectus with NASDAQ, potentially becoming the first Chinese tumor genetic testing company to list on NASDAQ. If this company successfully goes public, it may well instill confidence and encouragement among investors and entrepreneurs in the industry.

As startups, companies can only focus on the latter two issues. In terms of new application directions, pathogen detection has emerged as a promising area, and single-cell sequencing companies have also begun to appear this year. Although no breakthrough progress has been made, the industry has started to seek change. Regarding valuation bubbles, after the capital winter from 2018 to the present, the industry has cooled down compared to 2016 and 2017, shifting from blindly pursuing valuations back to the essence of entrepreneurship. Moreover, following industry consolidation, a clear divide has emerged. Under these circumstances, capital is able to more clearly evaluate targets.

Therefore, we predict that although it is difficult to return to the peak years of 2016 and 2017, after a year of consolidation and reflection, investment and financing in the gene sector may see some recovery in 2020.

After the dust settles, return to the essence and regroup for a fresh start.