PANLIN Capital's Li Yuhui Unveils Refined Investment Logic in Early-Stage Drug Development

Panlin Capital

Technology Innovation-Oriented Early-Stage and Mid-Stage Venture Capital Institutions

Whether starting his career as an elite investment banker, successfully pivoting to become an investor with seven portfolio companies listing on the A-share market, or leading Panlin Capital to build a healthcare investment system centered on new drug R&D, Li Yuhui’s every venture has been the envy of many. Within the investment community, Panlin Capital has rapidly gained prominence in healthcare VC; whenever friends come across healthcare projects, they habitually turn toLi YuhuiPlease review it.

In Shanghai, where autumn was in full swing in November, a small nucleic acid company under Li Yuhui’s early-stage investment portfolio had just closed its C1 financing round. “This marks Panlin Capital’s continued lead investment, following our participation in the A and B rounds,” said Li Yuhui, sharing his insights on healthcare investment with VCBeat from his high-rise office adjacent to the new Shanghai Stock Exchange.

In 2010, after a decade of investment banking services and five years of professional investing, Li Yuhui founded Panlin Capital. At that time, his early-stage investment in Toread (300005), China’s leading outdoor brand, had just completed its listing among the first batch of companies on the ChiNext board. Today, Panlin Capital has invested in nearly 50 companies, eight of which are listed on the A-share market, while many other early-stage portfolio companies have exited through industrial M&A. The firm boasts an exceptionally high project success rate, along with outstanding fund IRR and DPI metrics.

With nearly two decades of investment experience, Li Yuhui is convinced that high-quality investment targets are extremely scarce and must be captured with a sniper’s mindset. Thus, “careful selection of targets and concentrated investment” has become Panlin Capital’s sniper-style investment philosophy. “When encountering promising investment opportunities, one must have the courage to establish significant positions, make accurate judgments in the early stages to secure a strategic foothold, and continuously increase investment as the company grows. Only such targets can deliver excess returns to investors.”

In Li Yuhui’s investment philosophy, verifiability is fundamental. Whether it concerns technology, products, or the founding team, all must withstand market validation. Each successful validation of a project may serve as a trigger for Panlin Capital to make additional investments. “More than half of our portfolio companies have received multiple rounds of follow-on investment. As these companies grow and reach new financing milestones, we may continue to inject capital through different funds.”

Hybribio (300639), which has become a leading enterprise in the field of biological and genetic testing for cervical cancer, and Kangtai Biological (300601), a leading company in China’s vaccine industry, are classic examples of Panlin Capital’s investment strategy. These successes have firmly established Panlin Capital’s foundation in healthcare investment and validated its sniper-style, boutique investment approach.

According to reports, Panlin Capital led the Series B financing of Kangtai Biological Products in 2011 and made two follow-on investments; it also invested in Hybribio during the Series A round and made three follow-on investments. Both companies successfully listed on China’s A-share market in 2017.

Currently, Panlin Capital has invested in nearly 20 healthcare projects through its two specialized medical funds. Under the theme of “technology innovation driving consumption upgrades,” it has established a systematic portfolio in the fields of new drug development and high-end medical devices for major diseases such as cancer, cardiovascular diseases, and metabolic disorders. In addition to the two leading enterprises listed on the A-share market mentioned above, two new drug R&D companies that Panlin invested in at a very early stage have entered the final phase of preparation for listing on the STAR Market.

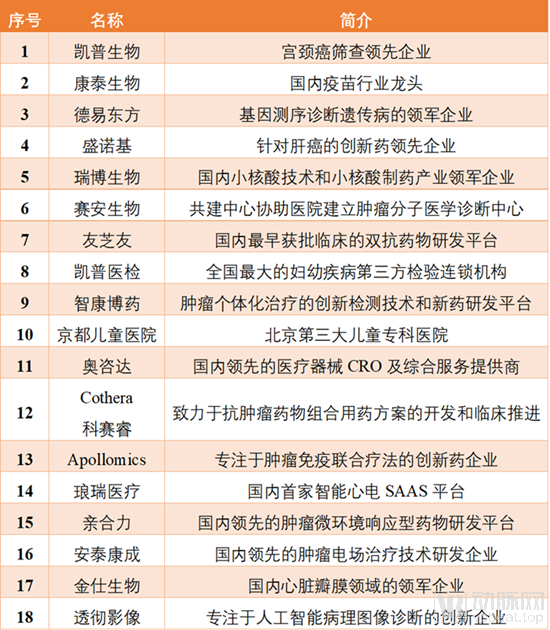

Panlin Capital Healthcare Investment Portfolio

“Consumption Upgrade” is the starting point for Panlin Capital’s understanding of investment opportunities in healthcare. As China’s per capita GDP continues to rise, people’s demands for improved quality of life and extended lifespan have given rise to two categories of medical needs: on one hand, disease prevention, diagnosis, and treatment; on the other, personal physical and mental health management and enhancement of quality of life.

In the prevention, diagnosis, and treatment of diseases, technology-driven approaches are continuously optimized and diversified, making it possible to address complex medical challenges. This represents the unmet needs that medical technologies aim to fulfill. This is also the entry point for Panlin Capital’s early-stage investments in the healthcare sector, with a focus on the driving role of biotechnology in the research and development of new drugs and medical devices, as well as in their manufacturing, organization, and services.

Li Yuhui believes that for both R&D-driven and manufacturing enterprises, demand is the root of their growth. “Accurately grasping market demand, combined with the current inflection point of domestic technological innovation, constitutes the core focus of healthcare investment. Panlin Capital analyzes healthcare investment from three perspectives: population aging, technological iteration, and medical insurance cost containment.”

Rigid demand creates ample market space for products and services. Meanwhile, the accelerated application of new biotechnologies in novel drug development will significantly drive the emergence and clinical approval of products or services that meet the needs for prevention, diagnosis, and treatment of major diseases. The R&D cycle establishes phased barriers for products, thereby ensuring longer-term product gross margins. This constitutes the logic of healthcare investment. Clinical R&D requires regulatory approval, and the phased nature of clinical progress forms the most critical industry characteristic of healthcare investment. “While mastery of technology is crucial in healthcare investment, the timing and pacing of investment and exit strategies will ultimately determine the success and outcomes of such investments.”

New drug development is the top priority of Panlin Capital’s healthcare investments and has become a distinctive hallmark of the firm. Although this sector entails extremely high risks for investors, Panlin Capital had already established its presence in new drug R&D investment as early as 2015.

For new drug R&D companies, Panlin Capital’s investment scope covers the stage from the completion of cell and animal studies to the acquisition of Phase II clinical trial data, with a primary focus on the period following the identification of a Preclinical Candidate (PCC) up to the initial entry into clinical trials. “We bypass the early-stage product development phase and seek to mitigate the risks associated with the development of individual drug candidates.” From an investment perspective, entering clinical trials represents a significant milestone in new drug development, making it easier to gauge the company’s future growth trajectory.

Li Yuhui provided a detailed interpretation of this investment logic. Typically, Phase I clinical trials primarily focus on drug safety; given solid preliminary research, advancing to Phase II is relatively straightforward. New drug development companies with platform-based technological characteristics often see other projects in their pipeline enter clinical trial stages simultaneously as their lead candidates advance to Phase II clinical trials, thereby creating strong support for valuation growth. At that point, their strategic M&A value to large pharmaceutical companies or research institutes also begins to emerge. In other words, the investment becomes viable for exit.

For medical device companies, Panlin Capital chooses to intervene at the stage when prototypes have been developed and type testing is nearing completion. Li Yuhui stated that for medical devices with a large market potential, Panlin Capital will hold its investment until the product is launched and generates sales revenue and profits, then exit through capital market channels; for medical devices with a smaller market potential, it adopts an industrial M&A approach for exit.

Therefore, another distinctive feature of Panlin Capital’s investment logic is its emphasis on the feasibility of project exit from the outset. Li Yuhui pointed out that, given the inherently long R&D cycles in the healthcare sector, which make exit timing difficult to control, Panlin Capital manages project risk by investing in platform-based technologies and designs exit pacing through careful timing of investments. “When making investment decisions, we often concurrently develop preliminary plans for subsequent exit channels.”

“Final investment decisions are made based on rational and rigorous analysis, but emotional factors play a crucial role in initially bringing a project to the attention of the investment team.” Li Yuhui strongly endorses the straightforward investment philosophy that “investing is about investing in people.” Drawing on its experience with 47 prior investments, Panlin Capital has developed an investment approach focused on identifying “entrepreneurs among scientists.”

However, assessing individuals is the most challenging task.

In Li Yuhui’s view, even when evaluating technical talent, it is necessary to take into account factors such as educational background, work experience, and life experiences. Moreover, the personality traits of technical professionals often play a pivotal role in shaping the future trajectory of projects.

For issues that defy quantitative resolution through rational analysis, Li Yuhui opts for qualitative judgment via intuitive analysis. In healthcare investments, Panlin Capital selects suitable startup teams based on two dimensions: the influence of technical resources and the capability to integrate business resources.

On the one hand, for R&D-driven enterprises, once the potential market for a product is clearly defined, the effective advancement of product development becomes the most critical measure of team capability. During the R&D process, a collaborative division of labor should be established within the team, where founders integrate resources while senior technical personnel handle specific implementation. On the other hand, scientist-entrepreneurs need to complete the design of technical frameworks and even product architectures, and possess a certain degree of academic or commercial influence in their entrepreneurial fields to attract talent.

“We hope that after securing sufficient funding, he can successfully transition from a scientist to an entrepreneur.” Li Yuhui pointed out that since every project is unique—even those with strong technical foundations—their technological characteristics, indications, business models, and founders all differ. Therefore, the human element is a critical factor in investment decisions.

Leading the initial round, participating in the second round with anti-dilution follow-on investment, and then making a substantial additional investment upon significant R&D milestones—this is Li Yuhui’s standard strategy for specific healthcare project investments.

Hybribio.Panlin Capital completed its first investment in Hybribio (300639) in 2011, marking Li Yuhui’s debut deal in healthcare investing. At the outset of his foray into healthcare investments, Li focused primarily on two key areas: major diseases and in vitro diagnostics. Hybribio’s HPV testing products for cervical cancer aligned perfectly with both of his strategic priorities.

Consequently, Li Yuhui personally led the team to conduct due diligence on Hybribio. He observed that, although Hybribio’s net profit was still under RMB 5 million at the time, the company had already established a market presence in more than 600 hospitals across China. The hospital-side distribution network had accumulated to form a business inflection point, indicating that net profit would grow rapidly thereafter. Subsequent developments at Hybribio validated Li Yuhui’s judgment. Four years after Panlin Capital invested in Hybribio, the latter’s net profit rose to over RMB 60 million, reaching RMB 118 million in 2018—a nearly 30-fold year-on-year increase in profitability. During this period, Panlin Capital made three additional rounds of investment.

The initial success of investing in Hybribio bolstered Li Yuhui’s conviction that, even in early-stage healthcare investments, a thorough understanding of investment principles is just as critical as technical expertise. “The subject of healthcare investment should be ‘investment’ itself—it is a financial activity, fundamentally distinct from supporting a medical research project.”

Li Yuhui pointed out that aligning a company’s development stage with the investment pace is highly beneficial to both parties, “however, project inflection points are rare and serendipitous in investment.”

Ribo Life Science.Ribo Life Science has always been a source of pride for Li Yuhui, having just completed its C1 round of financing. It is worth noting that when Panlin Capital invested in Ribo Life Science during its Series A round in 2015, the field of small nucleic acid drugs was still in a dormant phase, with no such therapies yet approved globally.

“Although small nucleic acid technology has gone from its initial prominence to a period of stagnation, we remained confident in this field during the Series A investment round,” Li Yuhui told reporters. He noted that the key technological breakthrough in this area lies in accurately targeting RNA interference therapeutics to lesion sites and ensuring their efficacy, and Ribo Life Science’s delivery platform system can be considered relatively leading.

In 2017, with continuous breakthroughs in highly efficient and safe drug delivery systems, small nucleic acid drugs gradually achieved commercial viability internationally, reigniting global investment interest and drawing the attention of major biopharmaceutical companies.

Based on its accurate assessment of this field, Panlin Capital successfully secured an early strategic position in the small nucleic acid drug sector. Ribo Life Science has also experienced rapid growth amid favorable industry conditions, significantly enriching its product pipeline. Collaborative products have already entered Phase II clinical trials in China, with some even completing enrollment for Phase III clinical trials. Self-developed follow-on products, including those targeting metabolic indications, are scheduled to submit clinical trial applications over the next two years.

As Ribo Life Science’s product pipeline continues to expand, Panlin Capital has steadily increased its investment: it made an additional investment in the Series B round in 2017 and once again led the Series C1 round in November 2019. Li Yuhui believes that the small nucleic acid drug market holds immense potential, and Ribo Life Science’s platform-based technology is critical for developing a serialized portfolio of products. This constitutes one of the core investment rationales Panlin Capital applies when investing in innovative drug R&D companies. Moreover, Ribo Life Science’s outstanding R&D and business development (BD) teams have been the fundamental reason why Panlin Capital had the confidence to make an initial investment and continue to increase its stake from the outset.

High technical barriers characterize healthcare investment; mastering this domain enables firms to build a formidable moat in the competitive investment landscape. As the interview drew to a close, Li Yuhui told VCBeat that excelling in healthcare investment demands exceptional professionalism, and Panlin Capital has deliberately cultivated a robust talent pipeline. Currently, Panlin’s healthcare investment team is built on a foundation of professional and industry expertise, supplemented by internal investors and external advisors. Through years of refinement, the team has matured, establishing a replicable healthcare investment framework, while maintaining regular weekly learning and exchange sessions. The firm’s investment focus has also evolved from its initial emphasis on innovative medical devices and healthcare services to a more concentrated strategy targeting new drug development for major diseases and high-end medical devices.