How Can Domestic Vascular Interventional Consumables Enhance Market Influence Amid Import Substitution? | 2019 Year-End Review

In 2019, the domestic market for high-value medical consumables underwent significant transformation. From the “Two-Invoice System” to centralized procurement of high-value medical consumables, sales channels and models have fundamentally changed; shifting from imitation products to independent innovation, Chinese-made high-value medical consumables are continuously being optimized; and as the market transitions from import dominance to localization, companies involved in the production of domestic high-value medical consumables are experiencing diverse outcomes...

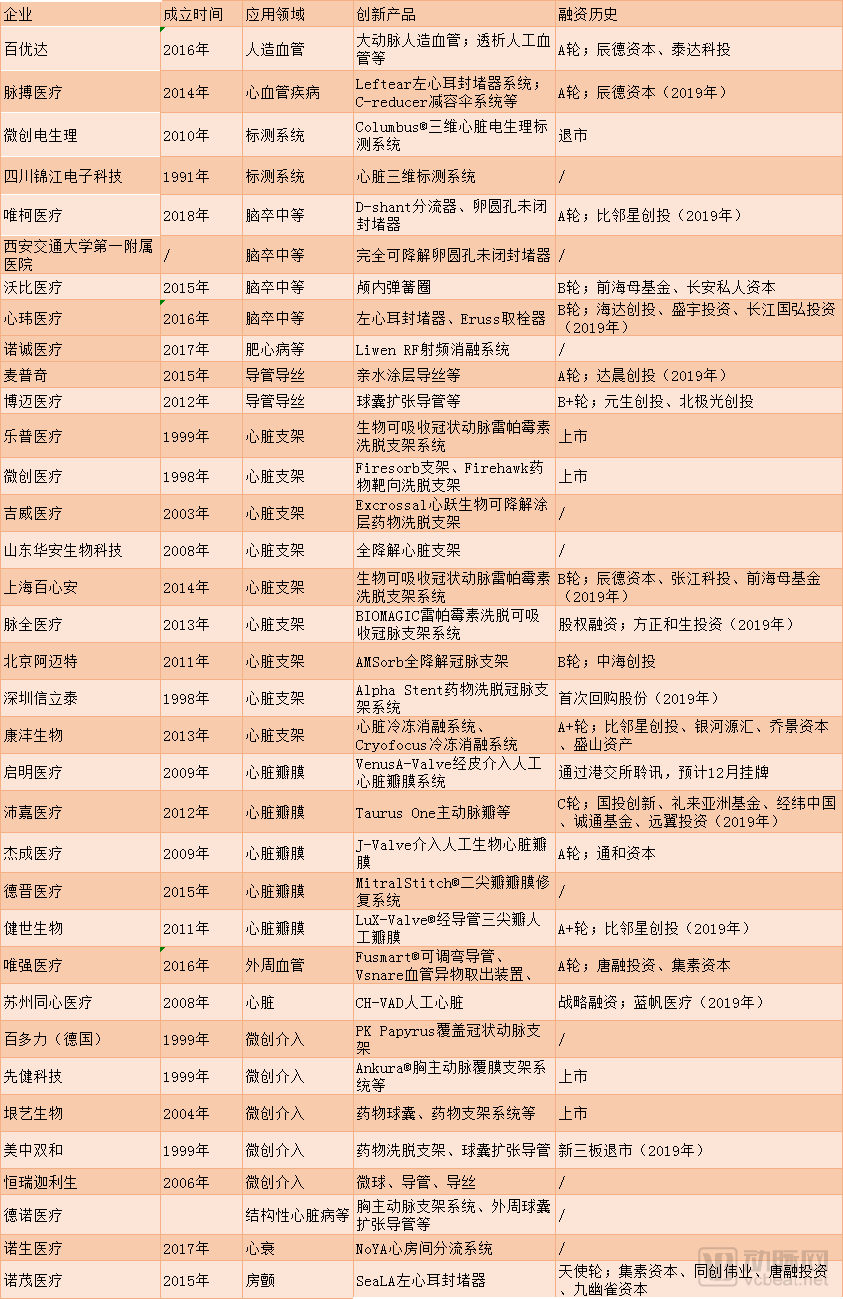

Over the past four months, according to incomplete statistics, VCBeat has reported on 32 related companies. Numerous cardiac surgery experts, in collaboration with the Cardiac Surgery Professional Committee of the China Medical Education Association and the Cardiovascular Surgery Technology and Engineering Branch of the China Medical Biotechnology Association, launched the “Starting from the Heart—2019 Top Ten Cardiovascular Technology Innovation Cases in China” call for submissions, and organized the “FTC 2019 China Frontier Technologies in Cardiac Surgery Forum.”

In this process, we observed the following changes in the high-value medical consumables sector in 2019:

1. Capital is generally cooling down, but remains keen on healthcare enterprises with core competitiveness;

2. The market for high-value consumables continues to expand;

3. The sales models of high-value medical consumable companies are undergoing a transformation, posing challenges for distributors;

4. Domestic manufacturers of high-value medical consumables are continuously innovating, with their products successively gaining approval or entering fast-track review channels, thereby posing a challenge to international brands;

5. Innovative enterprises will seize development opportunities, while homogeneous competitors will be gradually phased out;

6. An increasing number of companies in the high-value medical consumables sector are beginning to explore the path toward domestic production.

Given the significant attention paid to how high-value consumables can enhance market influence, VCBeat examines the development of enterprises in the vascular intervention sector and the evolution of policies in 2019 to address this question.

In the field of high-value medical consumables, the major capital market event of 2019 was Venus Medtech’s listing in Hong Kong. (On November 10, the Hong Kong Stock Exchange disclosed Venus Medtech’s post-hearing prospectus.)). Other innovative enterprises have also secured financing. In 2019, companies such as Pulse Medical, Weike Medical, Xinwei Medical, Mapuqi Medical, Shanghai Baixinan, Maiquan Medical, Peijia Medical, Jian Shi Biotech, and Suzhou Tongxin Medical completed new rounds of financing, with amounts ranging from tens of millions to hundreds of millions of yuan.

In fact, although the capital market cooled down this year (2019) and investment institutions became more cautious with their funds, capital investment in the healthcare industry remained enthusiastic. This was driven by factors such as favorable policy shifts and corporate innovation.

(Incomplete statistics: overview of companies in the cardiovascular interventional consumables sector)

Under this procedure, for the registration of innovative medical devices, the provincial medical products administration conducts a preliminary review within 20 working days, after which the National Medical Products Administration (NMPA) must issue its review opinion within 40 working days. If all goes smoothly, innovative products can enter the public notice period in just 60 working days, with the public notice period lasting no less than 10 working days. Overall, the entire process from application to completed registration may take approximately 15 weeks, representing a significant reduction compared to previous approval timelines. This is particularly beneficial for Class III domestically produced devices that require NMPA approval, enabling manufacturers to obtain market authorization more rapidly.

Since the implementation of the Special Approval Procedure for Innovative Medical Devices, the market launch of medical device products characterized by high innovation, advanced technology, and urgent clinical needs has been accelerated, while also speeding up the domestic substitution of high-end medical devices. According to available data, as of August 30, 2019, a total of 233 product applications had been approved to enter the special approval procedure. Among these, 28 were approved in 2019, with vascular intervention devices accounting for five items (excluding diagnostic products).

(As of now, in the field of vascular intervention in 2019Products Under the Special Approval Procedure for Innovative Medical Devices)

Among approved products, high-value consumables—particularly implantable and interventional devices—account for the largest proportion by product type, with vascular stents within the vascular intervention category being especially prominent. To date, four vascular stents have been marketed through the Special Approval Procedure for Innovative Medical Devices: MicroPort’s branched aortic stent graft and delivery system, Huamai Taike’s abdominal aortic stent graft system, Lepu Medical’s bioresorbable sirolimus-eluting coronary stent system, and MicroPort Endovascular’s abdominal aortic stent graft and delivery system.

In 2017, the bioresorbable sirolimus-eluting coronary stent systems developed by Biocartesia, Amate, Salubris, and Maiquan were also included in the special approval procedure.

In addition, numerous innovative domestic products have entered clinical trials, such as patent foramen ovale (PFO) occluders. These favorable factors have bolstered investor confidence in the healthcare sector, sustaining investment levels.

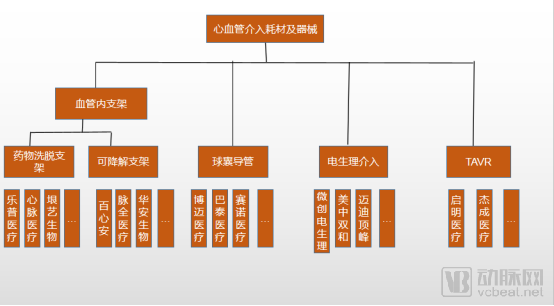

High-value medical consumables refer to disposable medical devices that feature high technical requirements, are subject to strict regulation, are limited to use in specific specialties, and command relatively high prices. These include products for cardiology, orthopedics, ophthalmology, and dentistry. Among them, vascular interventional consumables encompass coronary stents, guidewires, catheters, and the like.

Leading domestic companies in this field include Lepu Medical and MicroPort, while outstanding innovative enterprises such as Biomime Medical are also gaining increasing recognition.

(Partial Vascular Interventional Products and Related Enterprises)

High-value consumables account for a significant proportion of the global medical market. According to statistics, in 2017, cardiovascular high-value consumables ranked as the second-largest device segment globally. In contrast, high-value consumables represent a smaller share of China’s medical device market, with cardiovascular products accounting for only 6%, indicating substantial growth potential.

Currently, the clinical management of cardiovascular diseases primarily relies on three approaches: pharmacological therapy, surgical intervention, and interventional procedures. Due to advantages such as minimal invasiveness, rapid recovery, and shorter hospital stays, interventional therapy has become the preferred option for indicated conditions. This trend has also spurred the rapid development of vascular interventional consumables.

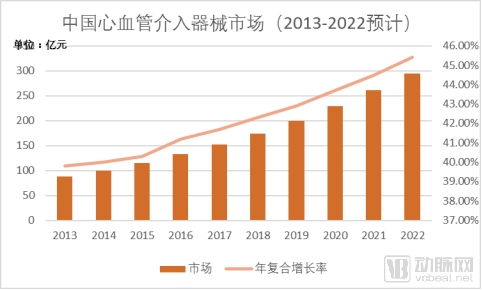

It is estimated that the market size of China's medical device industry grew from RMB 43.4 billion in 2006 to RMB 530.4 billion in 2018, with a compound annual growth rate (CAGR) of approximately 25.55%. Among these, the market size of high-value medical consumables reached approximately RMB 104.6 billion, representing a year-on-year growth of 20.37%, making it the segment with the highest growth rate within the medical device industry.

Meanwhile, China currently has 290 million patients with cardiovascular diseases. As the population ages, both the prevalence and mortality rates of cardiovascular diseases in China are expected to continue rising. In addition, the actual reimbursement rate under the New Rural Cooperative Medical Scheme is steadily increasing, and primary care capabilities are continuously improving, which will unleash the demand for percutaneous coronary intervention (PCI) procedures at the grassroots level. These factors will enableChina's market for high-value cardiovascular consumables continues to experience rapid growth, with the growth rate projected to remain at approximately 20%.

(Compiled by VCBeat based on relevant data)

From a market perspective, in the high-value medical consumables sector, foreign manufacturers such as Johnson & Johnson and Medtronic face intense competition in the mid-to-high-end product segment. Meanwhile, domestic manufacturers are continuously enhancing their innovation capabilities and launching innovative products amid national efforts to promote import substitution, resulting in a gradual increase in their market share.

Major domestic companies with a presence in the vascular interventional device market include Lepu Medical, MicroPort Medical, Lifetech Scientific, Yinyi Biological, Meizhong Shuanghe, and MicroPort EP. These companies possess strong R&D capabilities, and the vascular stents they have developed are among the few high-end medical devices in China that have basically achieved import substitution with domestically produced alternatives.

Among these companies, LifeTech Scientific, Yinyi Biomedical, Medtronic Shuanghe, and MicroPort EP focus on the field of cardiovascular intervention. LifeTech Scientific’s occluders and MicroPort EP’s 3D mapping systems and radiofrequency ablation catheters are leading products both in China and globally. In addition, innovative companies have also made breakthrough progress. Examples include Venus Medtech in the field of heart valves, Suzhou Tongxin in the field of artificial hearts, and Suzhou Jialisheng (acquired by Hengrui Medicine in 2015) in the field of drug-eluting microspheres.

In terms of innovative products, LifeTech Scientific and MicroPort Medical have had multiple products included in the Special Approval List for Innovative Medical Devices. Among these, LifeTech Scientific has obtained approval for one occluder product and one pacemaker product, while MicroPort Medical, including its subsidiary MicroPort EP MedTech, has secured approval for three products. Other domestic companies, such as Weike Medical and Weiqiang Medical, are also conducting innovative research, with a batch of innovative products expected to launch within the next two years.

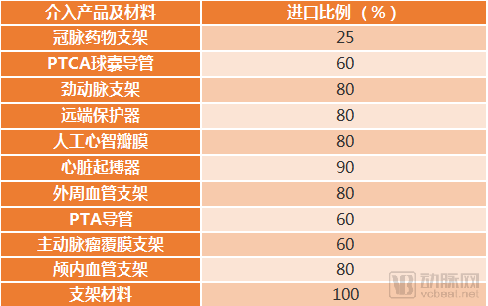

However, at present, import substitution has only been achieved for coronary drug-eluting stents among vascular interventional consumables. The import share for other interventional products and materials—such as carotid artery stents, distal protection devices, cardiac pacemakers, peripheral vascular stents, and stent materials—remains as high as 80%–100%.

(Compiled by VCBeat based on relevant data)

The deepening aging of the population, continuous improvement in national living standards, and expanded coverage and depth of medical insurance have driven up the demand for interventional procedures, leading to a sustained increase in demand for high-value medical consumables in China. On the policy front, incentives for medical device innovation and technological upgrading have established a “green channel” for domestically produced innovative medical devices. The combined forces of demand-side growth and supportive policies are accelerating the rapid development of China’s high-value medical consumables market.

Import substitution refers to the replacement of imported products with domestically produced ones. According to data from Qianzhan Industry Research Institute, China’s total import and export volume of medical devices reached $42.06 billion in 2017. In terms of import structure, mid-to-high-end medical devices accounted for approximately 44.3% of all imported medical devices. The top three categories by import value were optical and radiation instruments, high-end interventional materials, and medical X-ray diagnostic equipment.

Among high-end interventional consumables, domestic cardiac stents have captured 80% of the Chinese market since 2010, successfully achieving import substitution. However, other niche segments remain dominated by imported products. How domestic enterprises can increase the market share of locally produced products has become a critical issue, drawing significant attention from industry practitioners.

In response to widespread public interest, VCBeat used vascular interventional consumables as a case study and interviewed Professor Pan Junjie from the Department of Cardiology at Huashan Hospital, Mr. Zhao Yiwei, CEO of Deno Medical, Mr. Li Bin, CEO of Biomer Medical, as well as distributors, to explore and analyze how Chinese-made high-value medical consumables can enhance their market influence against the backdrop of import substitution.

Professor Pan Junjie has been working on the clinical frontline since 2000, possessing extensive experience in the diagnosis and treatment of cardiovascular diseases, with unique expertise in the emergency management of critical conditions in cardiology. He has a profound understanding and mastery of stent implantation for complex coronary artery lesions, independently performing over 300 emergency and elective procedures annually.

Denuo Medical is a professional enterprise specializing in investment, incubation, and operations within the innovative life sciences industry, with R&D centers established in both China and the United States. Its portfolio includes innovative companies such as Venus Medtech, Broncus Medical, Venustech Medical, Nuomao Medical, Dejin Medical, and Deko Medical.

Guangdong Biomed Medical Device Co., Ltd. is a medical device manufacturer specializing in the design, production, sales, and service of high-value consumables for vascular intervention, with products marketed in more than 40 countries and regions, including Europe, the United States, and Japan.

Policies that hinder fair competition between high-quality domestically produced products and imported ones

When domestic products were once technologically inferior, government tenders deliberately separated imported and domestically produced items into distinct bidding categories. While this approach previously safeguarded market opportunities for the domestic industry, it has now become a significant barrier preventing high-quality Chinese vascular interventional consumables from competing on an equal footing with international brands.

In fact, China’s medical device industry has advanced rapidly, with many domestically produced products now surpassing those of ordinary foreign manufacturers in quality. However, domestic companies remain at a competitive disadvantage because Chinese-made products are unable to compete with imported brands during bidding processes, as domestic policies favor imported products.

Taking Bomai Medical as an example, its products have been registered in China, the United States, the European Union, Japan, and other regions, and are sold at scale in more than 40 countries and territories, competing directly with top-tier international brands in many developed nations. However, while Bomai Medical’s balloon catheters can outperform numerous leading international products in global markets, they face price-driven competition confined to domestically produced alternatives upon returning to the Chinese market, with their market share restricted to a narrow segment.

If policies can keep pace with the times and be adjusted in a timely manner after significant progress has been made in the technology and quality of domestic products, it will certainly provide substantial support for accelerating the scale and speed of import substitution for vascular interventional medical devices.

Domestic innovative products not only meet quality standards but are also more aligned with Chinese clinical practice, enabling a faster response to the needs of the local clinical community. Nevertheless, imported products remain dominant in the market. This necessitates timely policy adjustments to effect change as soon as possible.

Few high-quality products; overall quality is generally inferior to imported products.

In recent years, the quality of domestically produced vascular interventional consumables has improved significantly. For instance, some domestic coronary stents are comparable to imported products, with follow-up data showing similar clinical outcomes. However, objectively speaking, many domestic products still lag behind their imported counterparts in terms of precision and refinement.

For accessories such as guidewires and catheters, there is essentially no difference between domestic and international brands for products with simple manufacturing processes. However, for products designed to treat complex lesions, domestically produced items lag behind imported ones in terms of quality.

Guidewires, among the consumables used in vascular interventional procedures, have extremely small diameters and demand exceptionally high manufacturing precision. China has not yet accumulated sufficient experience in precision manufacturing and needs to continue refining its processes or achieve technological breakthroughs. In the guidewire market, Japanese products have reached the global pinnacle. Why are Japanese products so highly favored?

Professor Pan Junjie from Huashan Hospital stated, “Because Japanese physicians continuously provided feedback on clinical outcomes, the corporate engineering team consistently refined the product, creating a closed-loop system that facilitated the upgrading and iteration of guidewires. Meanwhile, Japan’s precision manufacturing industry developed early and boasts strong capabilities; its relentless pursuit of craftsmanship is well worth our emulation.”

In addition to a lack of experience in precision manufacturing, the slightly inferior quality of domestically produced guidewires may also be related to insufficient investment in research and development (R&D) and production. Guidewires are characterized by low market prices yet high technical content, resulting in an unfavorable return on investment. Consequently, manufacturers may be reluctant to develop high-quality products due to concerns over substantial upfront costs and insufficiently visible returns.

An anonymous distributor stated, “Whether for imported or domestically produced products, the sole criterion physicians use in selecting products is quality. Domestic companies collaborate with physicians during product development; however, physicians are not developers and cannot precisely articulate their requirements. For example, a physician may comment that a product feels somewhat stiff during use, but engineers cannot fully grasp the specific quantitative data implied by such feedback.”

Japanese companies pursue excellence in manufacturing, with physicians continuously providing feedback on clinical outcomes and engineers iteratively optimizing and improving products. This solid, collaborative approach ensures high-quality products. As a result, Japanese vascular interventional consumables are highly popular in the global market.

Imitative Technologies Abound, Innovative Technologies Are Scarce

There is still significant potential for the domestic production of vascular interventional consumables. Just as other industries, such as high-speed rail and telecommunications, have achieved world-leading status, the medical industry certainly has the potential to reach the same level of global leadership.

Vascular interventional consumables present significant technical barriers, making technology the decisive factor in this field. The medical industry is constantly refining new technologies, while companies continuously iterate and upgrade their products. If domestic enterprises merely follow others by imitating existing technologies, they will struggle to achieve substantial growth.

Although imitating foreign technologies in the early stages can yield quick profits, in the long run, such imitation fails to establish a company’s core competitiveness. Moreover, the medical industry differs from general industries; generic products face slow market entry and may encounter issues such as patent litigation.

Mr. Zhao Yiwei, CEO of Deno Medical, stated: “The healthcare industry enforces stricter patent protection. Bringing a product to market requires multiple steps, including R&D, clinical trials, and regulatory approval, all of which involve lengthy review processes. By the time generic products enter the market, original manufacturers have already captured the majority of the market share and may even have launched their second-generation products. Patients have also established trust in these brands, making it difficult for generic alternatives to gain traction.”

For clinicians using original products, training is typically provided by technological pioneers. Consequently, after being trained by originator companies, these clinicians have already established habits regarding disease understanding, treatment solutions, and surgical procedures. When generic technologies emerge, clinicians lack sufficient motivation to learn them.

The cumulative effect of these factors has resulted in proprietary technologies overwhelmingly outperforming imitative products. Therefore, the level of localization in the healthcare industry still needs to be further enhanced, with continued focus on developing innovative technologies.

Late Market Entry Makes It Difficult to Challenge Imported Brands

In addition to quality, tactile feel is also a crucial factor. Since medical products are largely manipulated by hand, manufacturers must take into account the tactile experience and habits of physicians. Unlike driving, where the average person may not discern significant differences between premium brands such as BMW and Mercedes-Benz, physicians who frequently use interventional products are highly sensitive to product handling. For example, with a catheter, maneuvers performed at the proximal end by the physician should elicit precise, corresponding responses from the distal tip within the patient’s vasculature. If a product fails to deliver accurate, responsive control (“point-and-shoot” precision), it will not be favored by clinicians.

Some products are not substandard in quality; rather, many doctors have become accustomed to specific brands. A sudden switch to a different product could adversely affect their performance during surgery. Even a slight deviation may lead to surgical failure. Therefore, physicians generally do not change brands arbitrarily.

Li Bin, CEO of Bomai Medical, believes that the biggest challenge to the localization of vascular interventional consumables is mindset. He argues that a deep-seated perception persists among both clinicians and regulatory authorities: imported products are inherently superior, while domestically produced ones are invariably inferior. “In fact, looking back over the 40 years of reform and opening-up, this pattern has been common across most of China’s industrial sectors. Take the mobile phone industry as an example: before Huawei phones emerged with brilliance after multiple generations of evolution, few people would have believed that Chinese smartphones could become more popular than those from Samsung or Apple. However, because medical and health products directly impact patient safety, shifts in such perceptions are even more cautious and slow.”

In fact, this is also the result of years of brand promotion by imported products to users. This concept was cultivated from a time when the quality of domestic products was generally poor or there were no domestic products on the market. Imported products entered the market earlier and first nurtured users, making them believe that the quality of imported products is always superior to others, which has made it difficult for domestically produced products with gradually improving quality in recent years to shake the market.

Clinicians Are Concerned About the Safety and Efficacy of Domestically Produced Products

In fact, the hospitals that use imported products the most are well-known large domestic hospitals. Doctors in these major Chinese hospitals encounter more challenging diseases and more complex pathological changes; if domestically produced products were used, issues such as restenosis might arise, or the therapeutic outcomes might fail to meet physicians’ expectations. Patients seeking care at these major hospitals have largely moved beyond price considerations, with patients’ families placing greater emphasis on treatment efficacy. Therefore, the use of imported products by these leading hospitals is an inevitable choice.

For example, during interventional procedures, physicians need to deliver products such as stents to the lesion site; however, if the catheter wall is too thick or the lumen is too small, it becomes difficult for these products to pass through.

If the aforementioned issues arise, patients’ lives will be at risk, surgical procedures will become difficult to complete, and physicians will find themselves in a dilemma. In the event of surgical failure, doctors will face inquiries from patients’ families and need to handle various disputes. Consequently, it becomes challenging for physicians to focus on their professional duties, which significantly impacts their practice. Therefore, with patients’ best interests as the paramount objective, physicians select specific products to optimize surgical outcomes (or therapeutic efficacy). From both the patient’s and the physician’s perspectives, there is a shared preference for using higher-quality products.

Why Is It Difficult to Promote Domestic Brands? Vascular interventional consumables are life-saving products and rank among the highest-risk and most strictly regulated medical products worldwide. Consequently, the market for vascular interventional consumables does not segment into high-, mid-, and low-tier categories. While consumers may opt for lower-tier alternatives in other product categories, vascular interventional consumables must deliver superior efficacy and high quality. Physicians do not choose these products based solely on low price, and patients’ families likewise prioritize optimal therapeutic outcomes and the highest quality standards.

If a more advanced product emerges in the market, it will be difficult for inferior products to gain market acceptance, resulting in a winner-takes-all scenario. Fundamentally, the market will not tolerate medical products that compromise safety and efficacy for the sake of lower prices.

Policy Support for the Healthcare Industry and Domestically Produced Products

Domestic coronary stents are priced lower than imported ones, with imported stents costing approximately RMB 15,000 per unit, while domestic stents range from RMB 7,000 to 8,000 per unit. In contrast, other vascular interventional consumables are not priced lower than their imported counterparts and thus lack a price advantage. If the government could reform and optimize medical insurance reimbursement policies to achieve both cost reduction and support for high-quality domestic medical devices, it would constitute a significant benefit for domestic brands.

In industrial policy, if the government increases support for the healthcare industry, domestic enterprises are likely to increase R&D investment in high-end medical products, improve the quality and performance of domestically produced products, and enable Chinese brands to gain a certain degree of influence in the domestic market.

In the United States, the pharmaceutical industry accounts for 20% of GDP, whereas in China, it constitutes only 5%. As a sunrise industry, the pharmaceutical sector warrants greater national attention. With policy support, Chinese technology-driven and innovative enterprises can flourish, making the localization of medical products an imminent reality.

Fortunately, over the past six months, the Chinese government has successively introduced policies related to the governance of high-value medical consumables. For instance, policy documents such as the Reform Plan for the Governance of High-Value Medical Consumables, the Pilot Work Plan for the Unique Device Identification (UDI) System for Medical Devices, and the Reform Plan for the Governance of High-Value Medical Consumables have been released in succession. Jiangsu Province took the lead in launching provincial alliance-based centralized procurement of high-value medical consumables. On November 6, the National Development and Reform Commission published the Catalogue for Guiding Industry Restructuring (2019 Edition).

Under Jiangsu’s centralized procurement rules, the products eligible to participate in this volume-based procurement are all those that have been shortlisted in the provincial-level review for centralized procurement of medical consumables in Jiangsu Province over the past five years. Having undergone years of clinical validation, their safety is assured. The alliance also has a withdrawal mechanism for shortlisted products with recurrent quality issues.

Unlike pharmaceuticals, medical devices are difficult to subject to consistency evaluations. However, the requirement that only products with years of clinical validation are eligible to participate in volume-based procurement poses a significant blow to innovative and start-up enterprises.

The Guidance Catalogue released on November 6 pointed out that the research, development, and manufacturing of high-end equipment are encouraged in the pharmaceutical sector, includingHigh-end implantable and interventional devices and materials, such as novel stents and prostheses.The “Industrial Catalog” consists of three categories: encouraged, restricted, and phased-out. Specifically in the pharmaceutical sector, it includes 8 encouraged items, 6 restricted items, and 13 phased-out items.

Encouraged categories primarily refer to technologies, equipment, products, and industries that play a significant role in promoting economic and social development, help meet the people’s needs for a better life, and facilitate high-quality development;

Restricted categories primarily refer to production capacities, technologies, equipment, and products that are characterized by outdated technological processes, fail to meet industry access conditions and relevant regulations, and are therefore prohibited from new construction or expansion, while existing ones require mandated upgrades.

Eliminated Category mainly refers to outdated processes, technologies, equipment, and products that do not comply with relevant laws and regulations, lack safe production conditions, seriously waste resources, pollute the environment, and need to be eliminated.

The “Industrial Catalogue” explicitly came into effect on January 1, 2020. This represents a significant boon for innovative enterprises. As some experts have stated, “In the face of the industry’s painful adjustment period, innovation is the only way to break through.”

Technological Innovation Continues

As medical technology continues to innovate, if domestic enterprises can seize the trends amid technological shifts, devote substantial effort to technological advancement, and persistently pursue breakthroughs, the industry will have the opportunity for leapfrog development, enabling Chinese brands to join the global first tier.

Currently, the quality of domestically produced products has improved, and technological advancements have reached a level where they can replace imported alternatives. However, Chinese enterprises still need to increase their investment in the research and development of innovative technologies to enhance their core competitiveness, thereby keeping pace with international standards in the future.

For example, Venus Medtech began its strategic expansion into the emerging field of structural heart disease a decade ago. At that time, this sector was still in its nascent stage both domestically and internationally. Starting from the same baseline, Venus Medtech has continuously developed new products, leveraging its highly skilled team. It is precisely due to its innovative technologies that Venus Medtech’s products have successfully captured market share and gained recognition from experts, physicians, and patients alike.

For precision products such as guidewires, the quality of domestically manufactured alternatives is continuously improving alongside advancements in domestic processing technologies. Currently, national policies support the adoption of domestic products, and physicians are increasingly inclined to use Chinese brands whenever feasible, leading to a steady rise in the utilization of these domestically produced devices.

Emphasize Industry Promotion

A distributor stated, “Promotional efforts for vascular interventional consumables have limited impact.” When domestic companies market their products, they often claim that their offerings are no inferior to a specific competitor’s product, which implicitly acknowledges that they do not surpass it. With no technological breakthroughs and no significant price advantage, physicians are reluctant to adopt the promoted product. Only when a product demonstrates superior quality and more robust technology will physicians choose to use it.

An international medical device manufacturer once produced a guidewire, promoting it with the slogan that it was “no inferior to” a certain Japanese brand. However, to date, few physicians in the market have adopted this product.

Some domestic companies choose to highlight certain advanced technologies in their promotional campaigns; however, the true quality of a product becomes evident only after actual clinical use. Unlike other consumer goods, medical products can lead to complications and other issues when used in patients. Direct feedback obtained during clinical application or follow-up visits clearly reveals the product’s effectiveness.

In fact, many imported products do not rely on promotional campaigns but instead drive sales through word-of-mouth and industry advocacy. There are similar cases among domestically produced products; for instance, MicroPort’s stents have won market share due to their high quality and endorsement by physicians. Therefore, physicians place greater emphasis on peer-to-peer promotion and value the opinions of their colleagues regarding specific products.

To promote the localization of vascular interventional consumables, domestic enterprises need to improve product quality and collaborate with physicians to continuously optimize the handling experience. Once physicians endorse domestically produced products, sales will naturally increase, making localization an inevitable outcome.

Clinical Trials of Domestically Developed Innovative Products

For simple lesions, clinicians may opt for domestically produced products; however, for complex lesions where manipulation is more challenging, imported products or outstanding innovative domestic products with higher precision can be selected.

Taking Huashan Hospital as an example, the proportion of domestically produced cardiac stents used is higher because their quality is comparable to that of imported products. For delicate devices such as guidewires, domestic products are trialed for simple lesions. If the trial yields favorable outcomes, physicians will continue to use them; if any defects arise during use, physicians provide feedback to manufacturers to help optimize and improve their products. This practice contributes to the advancement of import substitution for domestic medical devices.

China is home to a cohort of innovative enterprises and a portfolio of high-quality products. Their performance has been validated by international regulatory systems and global markets, proving not only comparable to but in some cases superior to imported alternatives. Notable examples include MicroPort Medical, Lepu Medical, and Venus Medtech.

Therefore, clinical practice in China should provide domestic enterprises with opportunities to allow more high-quality products to replace imported ones for complex lesions, while standard products are used for simple lesions. In this way, the market share, quality, and clinical efficacy of domestically produced products will continue to improve, creating a virtuous cycle.

Venus Medtech’s Strategic Layout in TAVR Technology

Transcatheter Aortic Valve Replacement (TAVR) refers to the procedure in which a pre-assembled aortic valve is delivered via catheter to the aortic root to replace the native valve and restore its function. Compared with surgical valve replacement, TAVR offers advantages such as minimal invasiveness and faster recovery. With continuous improvements in valve technology and the accumulation of clinical experience among physicians, TAVR is expected to become the mainstream approach for aortic valve replacement in the future.

Globally, two international giants, Edwards and Medtronic, have captured 65% and 30% of the global TAVR market, respectively. However, VenusA-Valve, a transcatheter heart valve replacement system independently developed by Venus Medtech, was approved for market launch in 2017. To date, Venus Medtech has implanted 2,600 valves via the transfemoral approach, presenting an optimistic outlook for import substitution.

In China, besides Venus Medtech, companies deploying TAVR technology include Jiecheng Medical and MicroPort, among others. Although China started later, it is making significant strides forward with the support of national policies, entrepreneurs, and capital.

As TAVR technology gradually becomes widespread in top-tier hospitals, the latent demand for heart valves is also emerging. Data from Huatai Securities shows that by the end of 2018, more than 80 hospitals had experience performing TAVR procedures. As this technology expands to more hospitals, the domestic market is projected to exceed RMB 10 billion by 2029. In addition to transcatheter aortic valve products, Venus Medtech has also expanded its portfolio to include transcatheter pulmonary valve products.

Deno Medical Expands into Structural Heart Disease and Peripheral Vascular Fields

Deno Medical began its strategic expansion into the emerging field of structural heart disease a decade ago. At that time, this sector was still in its nascent stages both domestically and internationally. Starting from the same baseline, Deno Medical has continuously developed new products thanks to its outstanding team. It is precisely due to its innovative technologies that Deno Medical’s products have been able to capture market share and gain patient recognition.

Denovo Medical’s Nuocheng Medical Liwen RF Radiofrequency Ablation System, Venus Medtech’s transcatheter aortic valve product Venus A-Valve, Weiqiang Medical’s modular endograft for the aortic arch, Nuosheng Medical’s NoYA Adjustable Interatrial Shunt System, and Nuomao Medical’s SeaLA Left Atrial Appendage Occluder each offer distinct advantages.

For example, Weiqiang Medical’s modular endograft for the aortic arch is designed to treat aortic arch pathologies. The incidence of aortic arch diseases is relatively high, and the anatomical structure of the aortic arch is complex. A key challenge in thoracic endovascular aortic repair (TEVAR) for aortic arch diseases is to ensure the patency of the supra-aortic branch vessels while excluding the diseased segment. Prolonged cerebral ischemia due to compromised blood supply can lead to fatal outcomes. This stent-graft system comprises multiple modular components, and its implantation process does not compromise blood flow to the main vessel or branch vessels, thereby significantly reducing surgical risk.

Bomai Medical Deploys Advanced Manufacturing Processes

Bomai Medical is committed to achieving a competitive advantage for its domestic brand in the global high-end medical device consumables market by integrating internationally leading product technologies and manufacturing processes with an innovative, open business model.

Its developed coronary balloon dilation catheter features the smallest outer diameter globally for crossing stenotic lesions, enabling it to navigate complex chronic total occlusion (CTO) lesions. Furthermore, its developed triple-wire scoring balloon dilation catheter demonstrates superior capabilities in both lesion dilation and lesion crossing.

Bomai Medical’s independently developed Artimes and Apollo balloon dilation catheters are at the international forefront in terms of design, quality, and performance. These two products are primarily used in percutaneous transluminal coronary angioplasty (PTCA) procedures aimed at improving myocardial blood flow at sites of focal stenosis in the coronary arteries.

To date, Biomer Medical’s coronary balloon dilation catheters have achieved large-scale sales in over 40 countries and regions, including China, the United States, the European Union, and Japan. The company competes directly with leading international brands in many developed countries, and in some markets, Biomer Medical’s products have even surpassed certain top-tier international competitors in market share. In addition to these products, Biomer Medical has developed a diverse portfolio of devices in the fields of cardiovascular intervention, peripheral vascular intervention, and vascular access.

In China, in addition to innovative products from emerging enterprises, well-established companies such as Lepu Medical, MicroPort Medical, Jiwei Medical, HeartCare Medical, Lifetech Scientific, and Perimedic are competing with international brands. In the long run, the localization of vascular interventional consumables is an inevitable trend.

Based on exchanges with clinical experts, enterprises, and distributors, VCBeat believes that the following measures can serve as references for the localization of vascular interventional consumables:

1. The company chose to begin its promotion at primary care hospitals and invited physicians to conduct industry-wide advocacy;

2. Companies may invite experts to trial high-quality products, optimize them based on feedback, and replace imported alternatives;

3. Clinicians predominantly use high-quality domestically produced products, thereby providing Chinese manufacturers with certain opportunities;

4. The state supports the healthcare industry to promote its development;

5. Centralized procurement policies for medical devices should be innovated to select lower-priced products while ensuring quality. Consideration may be given to having an expert committee evaluate bid products through trial use, followed by price negotiations. The procurement protection period may be extended to two years.

6. The state may encourage the trial use of innovative products to protect the development of start-ups.

Currently, China’s manufacturing capabilities are continuously strengthening, and the quality of domestically produced products is steadily improving. Chinese products have also been exported to countries in Africa, Southeast Asia, and other regions. Under policy guidance, the proportion of domestically produced products in use is rising, a trend already reflected in current data. The localization of vascular interventional consumables is gradually yielding results, driven by the continuous implementation of multiple measures.

"New Growth in Life": The 2019 Future Healthcare 100 Conference

December 20-22, the 2019 Future Healthcare 100 Conference, hosted by VCBeat and Eggshell Research Institute, will be grandly held at Jiuhua Resort in Beijing.

The theme of this conference is “New Growth in Life,” which will comprehensively showcase the innovation ecosystem in China’s healthcare sector by focusing on factors such as the policy environment, technological landscape, and demand potential.

The conference features the Future Healthcare Main Forum, Future Healthcare Top 100 Summit, Future Healthcare Leaders Summit, Future Healthcare Cross-Industry Summit, Health and Medical Fund Partners Summit, China-Japan Health Industry Development Forum, Healthy City Development Forum, Innovative Health Insurance Forum, Digital Pathology and Precision Diagnostics Forum, Health Management Forum, Consumer Healthcare Forum, Internet Hospital Forum, Smart Hospital Construction Forum, Pharmaceutical Digital Marketing Forum, Biotechnology Forum, Medical AI Forum, and Medical Devices Forum. Additionally, it includes the release of over ten reports and the Future Healthcare Top 100 List.