Impact of DRGs on Payers, Hospitals, Physicians, Patients, and MedTech Companies: A Comprehensive Analysis

DRGs (Diagnosis Related Groups) is a management system that categorizes patients into several diagnostic groups (DRG groups) based on factors such as age, disease diagnosis, comorbidities, complications, treatment methods, severity of illness, and outcomes.

Health insurance payers will establish payment standards based on diagnosis-related groups (DRGs) and settle payments directly with hospitals. Meanwhile, patients’ existing payment methods and reimbursement ratios will remain unchanged.

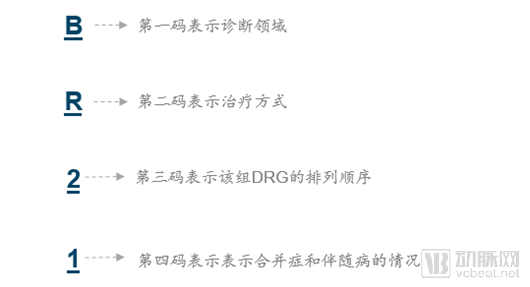

Presentation Formats of DRGs

Each patient's DRG diagnostic group code consists of four characters (e.g., BR21).

The core objectives of DRGs are threefold. First, to control healthcare costs. By shifting the payment standard from individual drugs or tests to diagnosis-related groups, excessive medical treatment is avoided, thereby saving health insurance funds. Second, to enhance healthcare service capabilities and increase the Case-Mix Index (CMI) of medical institutions. A higher CMI indicates stronger diagnostic and treatment capabilities, enabling hospitals to manage more complex diseases. Third, to improve healthcare service efficiency and reduce patients’ average length of stay.

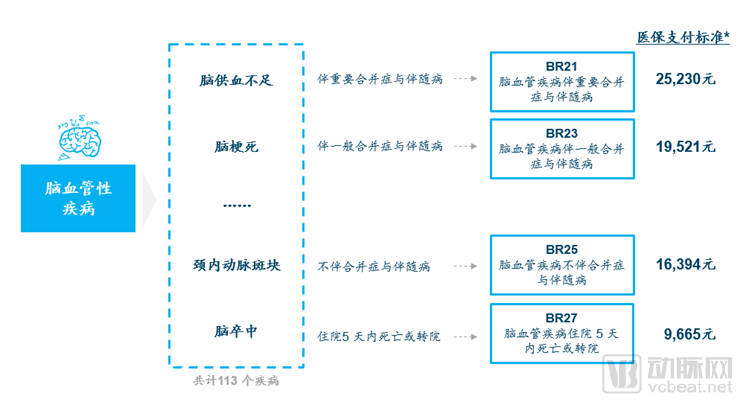

For example, patients with the same type of disease can be assigned different health insurance payment standards based on their specific comorbidities or concomitant conditions. Compared to other mainstream global payment models, Diagnosis-Related Groups (DRGs) are more precise and scientific; however, they also impose higher requirements on hospital management and government oversight.

Global Development History of DRGs

Source: “Application of DRG in Taiwan’s Medical Payment Reform”

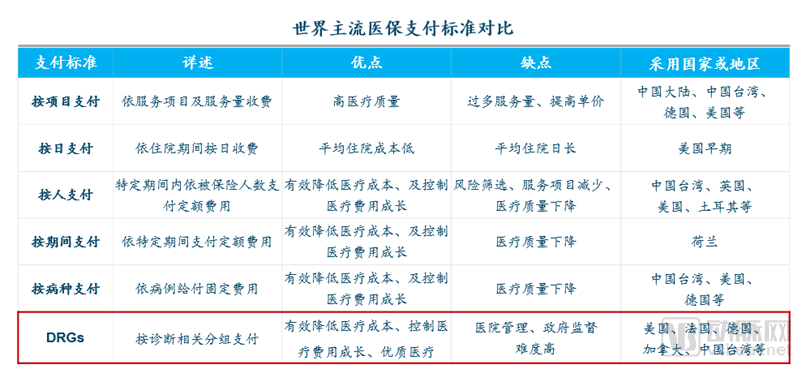

Unlike per-disease payment, Diagnosis-Related Groups (DRGs) account for individual patient variations within the same disease category, including different complications and comorbidities, treatment modalities, and diagnostic complexities, thereby establishing differentiated payment standards. Consequently, DRGs enable more personalized reimbursement than per-disease payment, thus ensuring healthcare quality. However, due to the large number and complexity of diagnostic groups in DRGs, they pose significant challenges to hospital diagnostic management and government oversight.

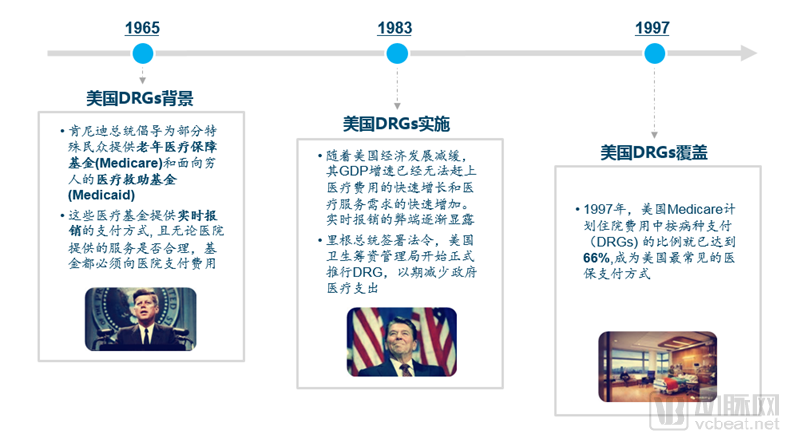

DRGs have been in operation in the United States for nearly 40 years, with relatively mature experience.

Source: “Implications of the Development of American DRGs for Controlling Medical Costs in China”

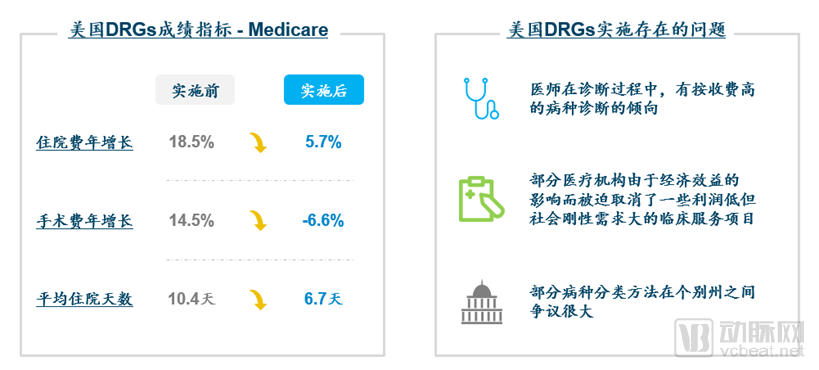

Although the implementation of Diagnosis-Related Groups (DRGs) in the United States has exposed certain issues, its achievements have been more significant. The annual growth rate of hospitalization costs decreased from 18.5% to 5.7% post-implementation. The average growth rate of surgical fees dropped from 14.5% to -6.6%, and the average length of stay was also substantially reduced. Nevertheless, the implementation of DRGs has led to some problems, including the forced discontinuation of certain medical services that are low-profit but in high demand.

Source: "Implications of the Development of American DRGs for Controlling Medical Costs in China"

Given the dominance of public health insurance in China, the financial pressure on China’s healthcare insurance fund is even greater than that in the United States. The effectiveness of DRG implementation in the U.S. has served as both a driving force and a valuable reference for China’s adoption of this policy. Meanwhile, key challenges inevitably facing the domestic implementation of DRGs include how to prevent physicians and hospitals from upcoding or misclassifying DRG groups, and how to mitigate regional disparities in DRG classification.

Current Status of DRG Development in China and Related Policy Overview

China has been exploring reforms in medical insurance payment for many years. Since the establishment of the National Healthcare Security Administration, the pace of reform has significantly accelerated, with the launch of pilot programs for Diagnosis-Related Groups (DRGs).

In 2004, the Ministry of Health issued the "Notice on Launching Pilot Programs for Diagnosis-Related Group (DRG) Payment Management," proposing to carry out pilot programs for DRG-based payment management for 30 diseases in seven provinces and municipalities.

In 2011, the General Office of the State Council issued the “Notice on the Arrangement of Pilot Work for the Reform of Public Hospitals in 2011,” requiring that by the end of the year, the number of clinical pathways formulated and issued be increased to 300; furthermore, 50% of Grade III Class A hospitals and 20% of Grade II Class A hospitals were to implement clinical pathway management for no fewer than 10 and 5 disease entities per hospital, respectively.

On July 6, 2016, the National Development and Reform Commission, together with the National Health and Family Planning Commission, the Ministry of Human Resources and Social Security, and the Ministry of Finance, issued the “Opinions on Advancing the Reform of Medical Service Pricing,” which stated that “by the end of 2016, pilot regions for comprehensive reform of urban public hospitals shall implement diagnosis-related group (DRG) or case-based payment for no fewer than 100 disease entities.”

In January 2017, the National Development and Reform Commission, the National Health and Family Planning Commission, and the Ministry of Human Resources and Social Security jointly issued the “Notice on Promoting Diagnosis-Related Group (DRG) Payment Reform,” to comprehensively advance the reform of payment by disease type. The notice published a catalog of 320 diseases for localities to select from when implementing diagnosis-related group payment.

In 2019, the National Healthcare Security Administration and three other departments issued the "Notice on Printing and Distributing the List of National Pilot Cities for Diagnosis-Related Groups (DRG) Payment." The National Working Group on DRG Payment Pilots designated 30 cities, including Beijing and Tianjin, as national pilot cities for DRG payment. Simulated operation of this payment model was conducted in 2020, with actual implementation launched in 2021.

Led by Beijing, some domestic cities have already gained experience and achieved results in the implementation of DRGs.

A summary of the effectiveness evaluation of pilot hospitals in Beijing from 2014 to 2016 showed that the three-year differential surplus rate was 9.95%. There were six DRG groups with a three-year surplus rate exceeding 50%, and seven DRG groups with a three-year deficit rate exceeding 10%. The final results indicated that the pilot hospitals outperformed the control hospitals in controlling the growth rate of medical expenses, as well as in medical efficiency and treatment outcomes.

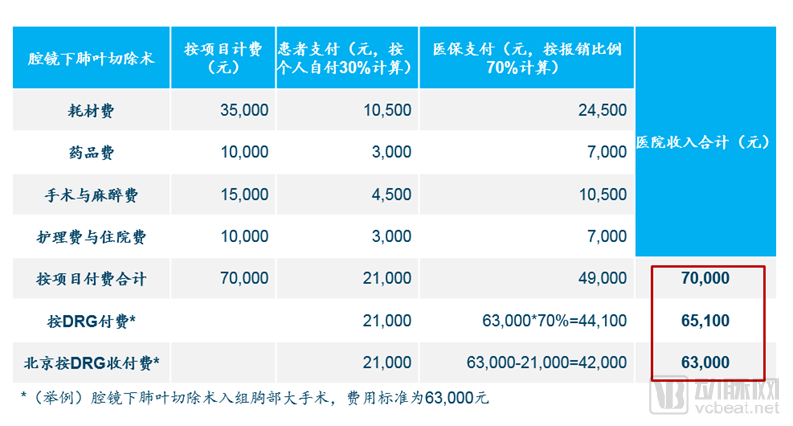

Compared with the current fee-for-service model in China, Beijing’s DRG system has effectively curbed unnecessary medical expenditures by linking hospital profitability to medical bills.

The “DRG Lufeng Model” from Lufeng County, Chuxiong Yi Autonomous Prefecture, Yunnan Province, was selected as one of the Top Ten National Healthcare Reform Experiences and hailed as the “Chinese Rural Version of DRG.” In 2013, under the guidance of national and provincial expert teams, Lufeng County pioneered the reform of Diagnosis-Related Groups (DRGs) payment system in secondary hospitals in China and achieved success, establishing a localized DRGs payment system for county-level hospitals that aligned with local conditions and was replicable. By the end of 2016, the DRGs payment system had covered all 18 public county-level hospitals across the prefecture.

As a national benchmark for DRG-based healthcare reform, the “Lufeng Model” has, to some extent, demonstrated that DRGs can deliver benefits to multiple stakeholder groups.

First, there was a decline in the utilization rate of the medical insurance fund. The utilization rate of the New Rural Cooperative Medical Scheme (NRCMS) fund in Lufeng County decreased from 100.39% in 2012 (pre-reform) to 88.54% in 2016.

Secondly, the average cost per hospitalization decreased. In 2016, the average cost per county-level hospitalization in Lufeng County was RMB 3,308, which was RMB 446 lower than the provincial average. In the same year, the average cost per county-level hospitalization in Chuxiong Yi Autonomous Prefecture was RMB 3,324, also below the provincial average; compared with 2014, the year prior to DRG implementation, the annualized growth rate was only 5.6%. Among the nine county- and district-level people’s hospitals in Yuxi City, the average cost per hospitalization dropped from RMB 4,131 in 2015 to RMB 3,630 in 2016.

Hospital Staff Incomes Rise. Taking the People’s Hospital of Lufeng County as an example, from 2012 to 2016, the average annual growth rate of per capita annual income for staff reached 33.64%. Meanwhile, in 2016, the compensation for medical and nursing staff at the People’s Hospital of Yuxi City increased by 27.2% year-on-year, both figures being significantly better than those at hospitals in the same province that had not implemented Diagnosis-Related Groups (DRGs).

However, as an innovative medical insurance payment method, DRGs still have a long way to go in their development within China.

Sources: MHRSS Social Security Center

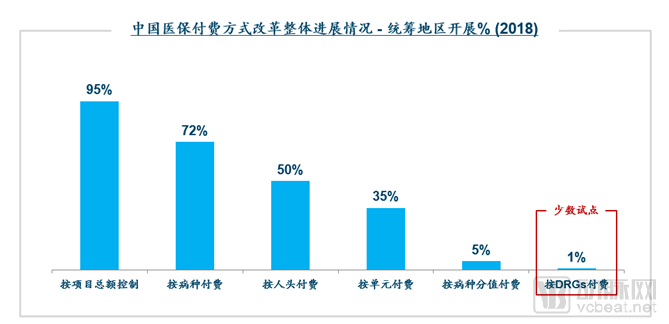

The drawbacks of mainstream health insurance payment methods have become fully apparent. The global budget payment system completely disregards differences in disease conditions, leaving physicians constrained in their prescribing practices while simultaneously compromising the quality of care. Although diagnosis-related group (DRG)-based payment accounts for variations among diseases, it overlooks individual patient circumstances. These issues have created opportunities for the development and adoption of DRGs.

The goal of the new 2019 policy was to further expand the experience from small-scale DRG pilots to more cities.

Sources: “Notice on Issuing the List of National Pilot Cities for Diagnosis-Related Group (DRG) Payment”

This pilot program covered cities of all tiers, making it more instructive for subsequent nationwide rollout. According to policy requirements, the DRG pilot was scheduled to operate in simulation mode in 2020 and to initiate actual payment in 2021. Therefore, Ryan Partners believes that the impact of DRGs on various dimensions at the national level will not truly become apparent until 2022 at the earliest.

What Are the Future Impacts of DRGs?

The implementation of DRGs will have varying impacts on payers, hospitals, patients, and pharmaceutical and medical device companies. We summarize these effects from the perspectives of different stakeholders as follows.

Payers: Alleviating the Financial Pressure on Medical Insurance Funds

For payers, the government expects that the implementation of Diagnosis-Related Groups (DRGs) will alleviate the financial pressure on health insurance funds to some extent. Taking the United States as an example, after the implementation of DRGs in 1983, the growth rate of total Medicare inpatient expenditures decreased from 18.5% in 1983 to 5.7% in 1990, and the growth rate of surgical fees dropped from 14.5% in 1984 to -6.6% in 1992, significantly easing the strain on health insurance funds. Similarly, Germany and Canada have also effectively controlled the growth of healthcare costs after implementing DRGs, stabilizing their share relative to GDP.

Furthermore, the implementation of Diagnosis-Related Groups (DRGs) facilitates health insurance settlement between payers and hospitals. Previously, such settlements required itemized accounting based on detailed diagnoses, medications, medical devices, and consumables. Under the DRG system, payers can settle payments uniformly according to classification codes, significantly improving the settlement efficiency for relevant departments.

Meanwhile, DRGs can generate systematic disease data, facilitating public health management. The implementation of DRGs is based on coding systems and information processing platforms. It is foreseeable that information systems will be able to record and collect more comprehensive epidemiological, surgical, and other data, thereby improving the efficiency of disease management for both governments and hospitals.

Hospital: Increased Revenue, Improved Service Efficiency

For hospitals, based on domestic and international experience, DRGs will enhance management efficiency and increase hospital revenue.

First, it will drive hospitals to improve management efficiency and optimize diagnosis and treatment protocols. Since the insurance payment standards for each DRG group are fixed, hospitals must optimize their clinical pathways and strictly adhere to standardized treatment protocols to ensure effective patient care within limited healthcare expenditures. Taking the United States as an example, after implementing DRGs, the average length of hospital stay decreased from 10.4 days to 6.7 days. Similarly, at a pilot hospital in Beijing implementing DRGs, the average length of stay gradually declined from 8.75 days before implementation to 6.62 days afterward, demonstrating that the hospital’s diagnosis and treatment protocols have been optimized.

Secondly, it can help improve the utilization rate of health resources and enable hospitals to admit more patients. The reduction in patients’ length of stay further enhances the patient admission capacity of hospitals, especially large tertiary hospitals, thereby improving the utilization of high-quality medical resources. At Lufeng County People’s Hospital, the largest public hospital in Lufeng County, the number of discharges increased from 25,000 before DRG implementation to 31,000 afterward. Other pilot hospitals also saw significant increases in their average annual patient visits.

Finally, physicians’ compensation and income were increased. Seeing more patients led to higher medical revenue for hospitals and increased earnings for healthcare staff. Taking Lufeng County People’s Hospital as an example, its annual medical service revenue rose rapidly from RMB 92 million before DRG implementation to RMB 159 million afterward. Employee benefits also improved, with average annual per-capita income growing by approximately 33.64%, outperforming control hospitals that had not implemented DRGs.

DRGs incentivize hospitals to reduce individual patient medical bills by shortening the average length of stay, thereby increasing overall healthcare revenue.

Additionally, the real-time implementation of DRGs can enhance the efficiency of healthcare services. Strict adherence to clinical pathways can reduce unnecessary preoperative tests and their frequency, thereby shortening preoperative preparation time. Mutual recognition of test results among hospitals reduces time wasted on redundant examinations and improves diagnostic efficiency. Meanwhile, measures such as day-case surgery and transfer to rehabilitation facilities help shorten patients’ hospital stays.

Patients: Reduce Costs, Improve Healthcare Quality

For patients, the expectation is that Diagnosis-Related Groups (DRGs) will not only reduce medical expenses but also improve the quality of care. The implementation of DRGs encourages hospitals and physicians to deliver optimal clinical outcomes using the most efficient and cost-effective resources, thereby avoiding unnecessary overprescribing and excessive testing. Taking Lufeng County in Yunnan Province, a pilot site for DRGs, as an example, the average hospitalization cost per discharge at county-level hospitals in 2016 was RMB 3,308 after DRG implementation, which was RMB 446 lower than the provincial average for hospitals at the same level.

To a certain extent, it alleviates the problem of “difficulty in accessing medical care.” DRGs encourage hospitals to optimize diagnosis and treatment protocols and shorten patients’ length of stay, thereby increasing patient admission capacity and enabling more patients to access high-quality medical resources. At Lufeng County People’s Hospital, the number of discharged patients increased from 25,000 before DRG implementation to 31,000 afterward. This rise in patient admissions was achieved without any increase in the number of hospital beds.

Optimized diagnosis and treatment protocols, strictly adhering to clinical pathways, have further enhanced the quality of care for patients. Following the implementation of Diagnosis-Related Groups (DRGs), Lufeng County People's Hospital achieved a concordance rate of 97.14% between outpatient and discharge diagnoses, and a cure/improvement rate of 99.03%, both significantly higher than pre-implementation levels.

Pharmaceutical and Medical Device Companies: Bringing a Series of Potential Challenges

For foreign pharmaceutical companies and manufacturers of medical devices and consumables, DRGs are expected to bring a series of potential challenges.

1. Reduction in overall medication and consumable usage

To comply with national payment standards, public medical institutions may reduce unnecessary medications and tests for individual patients. Meanwhile, hospitals will also favor prescribing low-cost generic drugs that have passed the consistency evaluation. Taking France as an example, the prescription share of generic drugs was less than 20% before the implementation of Diagnosis-Related Groups (DRGs), but rose to over 60% afterward.

Strategies for Foreign Enterprises: Accelerating the Launch of Innovative Drugs in China.

2. Shifts in the Competitive Landscape Necessitate an Urgent Strategic Pivot

Taking originator drugs as an example, competitors have expanded from domestically produced generic drugs to other cost entities within the same DRG group, including diagnostics, consumables, hospitalization, surgery, and rehabilitation.

Strategies for Foreign-Funded Enterprises: Design Promotion Strategies Based on DRG Groups or Clinical Pathways as a Whole.

3. Changes in End Customers (Primarily Medical Devices)

Diagnostic constraints imposed by DRGs increase the cost risks for hospitals in updating diagnostic equipment, potentially leading to reluctance in such upgrades and resulting in the outsourcing of certain diagnostic tests to third-party laboratories.

Strategies for Foreign Enterprises: Medical device companies need to adjust their channel coverage and sales efforts toward third-party laboratories.

On the other hand, DRGs will also bring some opportunities to foreign pharmaceutical companies and medical device manufacturers.

1. Increased Importance of Compliant Promotion

“The drug-revenue-dependent healthcare model” will become increasingly unsustainable. Physicians’ prescribing decisions will refocus on the clinical value of medications (efficacy and safety) and the necessity of diagnosis. Consequently, compliant promotional practices will gain greater importance, representing a competitive advantage for multinational pharmaceutical companies.

Strategies for Foreign-Funded Enterprises: Challenging the Efficacy and Safety Deficiencies of Competing Products.

2. Created more opportunities for hospital-enterprise collaboration

The successful implementation of Diagnosis-Related Groups (DRGs) requires, first, a robust coding system and, second, supporting hospital information systems. Given that most hospitals are currently unfamiliar with the development of such information systems, this situation creates opportunities for enterprises to collaborate with hospitals—a domain in which foreign companies possess greater expertise.

Strategies for Foreign-Invested Enterprises: Establish Internal Working Groups to Assist Hospitals in Building DRG Information Technology Platforms.

3. Development of Emerging Channels Such as Retail and Internet Hospitals

To control medical billing costs, hospitals are increasingly likely to shift more prescriptions to out-of-hospital pharmacies, thereby reducing in-house medical bills. Through new channels such as internet hospitals, they aim to move prescriptions for patients with chronic diseases out of the hospital setting, alleviating the pressure on in-hospital medical billing.

Strategies for Foreign Enterprises: Establish Pharmacies and Online Healthcare Teams, and Proactively Layout New Channels.

The next two to three years will be a critical period for enterprises to prepare for and respond to DRGs. Proactive engagement is essential, as the execution of strategic initiatives will largely determine their development performance over the subsequent five to ten years.

Recommendations for Pharmaceutical and Medical Device Companies

For pharmaceutical and medical device companies, we recommend adopting flexible pricing strategies for originator products that already have generic equivalents which have passed the consistency evaluation, while accelerating the R&D and registration of innovative products that are not yet on the market.

In terms of team building, the importance of corporate medical teams has increased, requiring them to assist hospitals and physicians in optimizing diagnosis and treatment plans and providing recommendations on clinical pathways. Meanwhile, the development of retail teams is also critical. International case studies have demonstrated that the implementation of Diagnosis-Related Groups (DRGs) drives prescription outflow as a measure to reduce healthcare costs.

In terms of product promotion strategy, while the clinical team focuses on promoting clinical value, it must also emphasize economic benefits by conducting relevant prescription economics studies to convey key messages to physicians. Centered on physicians’ future needs, this approach aims to assist them in achieving their performance targets.

Finally, healthcare enterprises need to strengthen hospital-enterprise collaboration related to DRGs, such as information system development and optimization of clinical treatment protocols.

Author: Ryan Partners

Ryan Partners provides clients with comprehensive solutions, including global market research, market access strategies, and market potential assessments, among other business intelligence services. We help clients address various challenges encountered at different stages of the business cycle, enabling them to evaluate and understand market environments and potential opportunities, thereby enhancing their competitiveness in the global marketplace.

URL: http://www.ryan-partners.com/

WeChat Official Account: ruianshangwu