Zelgen Biopharmaceuticals Submits Hong Kong IPO Prospectus Following Historic Approval Under STAR Market's Fifth Listing Standard

By Jin Meina (Healthcare Team at AnJie Law Firm)

On October 30, 2019, Suzhou Zelgen Biopharmaceuticals Co., Ltd. (“Zelgen Pharmaceuticals”) passed the listing review by the Listing Review Committee of the Shanghai Stock Exchange’s STAR Market, drawing widespread attention from China’s capital markets.

The launch of the STAR Market represents a fundamental reform of China’s A-share market. It has truly eliminated profitability requirements for prospective listed companies, introduced the concept of market capitalization, and established five sets of financial listing criteria for applicants to choose from. Among these, the fifth set of criteria is widely regarded as being “tailor-made” for biotechnology enterprises, aligning with their characteristics of long R&D cycles, substantial capital investment, and lack of early-stage profitability. As an innovative pharmaceutical company with no commercialized products, no revenue, and yet to achieve profitability, Zeltex Pharmaceuticals was the first enterprise in the entire market to apply for listing under the fifth set of criteria. Following Zeltex, several other companies, including Bio-Thera Solutions and Frontier Biotechnologies, have also applied using this standard. If Zeltex ultimately secures registration approval and successfully lists, it will mark one of the most significant milestones in the development of China’s capital market in recent years.

I. Main Content and Profound Implications of the Fifth Set of Listing Criteria on the STAR Market

The STAR Market holds a significant historical position, requiring companies seeking listing to align with the global technological frontier, the main arena of economic development, and major national needs. It prioritizes support for high-tech and strategic emerging industries—including next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, and biomedicine—while promoting the deep integration of the internet, big data, cloud computing, and artificial intelligence with the manufacturing sector.

Compared with the Main Board, the SME Board, and the ChiNext Board, the STAR Market no longer sets single, rigid profitability and revenue indicators. Instead, it introduces the concept of market capitalization and innovatively establishes diversified financial criteria by integrating factors such as market capitalization, net profit, operating revenue, and cash flow. According to its listing rules, prospective listed companies need only meet one of the following financial standards:

(1) The estimated market value is no less than RMB 1 billion, with positive net profits in each of the last two years and cumulative net profits of no less than RMB 50 million; or the estimated market value is no less than RMB 1 billion, with a positive net profit in the most recent year and operating revenue of no less than RMB 100 million;

(2) The projected market capitalization is no less than RMB 1.5 billion, the operating revenue for the most recent year is no less than RMB 200 million, and the cumulative R&D investment over the past three years accounts for no less than 15% of the cumulative operating revenue over the same period;

(3) The projected market capitalization shall be no less than RMB 2 billion, the operating revenue for the most recent year shall be no less than RMB 300 million, and the cumulative net cash flow from operating activities over the past three years shall be no less than RMB 100 million;

(4) The projected market capitalization is no less than RMB 3 billion, and the operating revenue for the most recent year is no less than RMB 300 million;

(5) The projected market capitalization is no less than RMB 4 billion. The main business or products must be approved by relevant national authorities, possess significant market potential, and have already achieved phased results. Pharmaceutical companies must have at least one core product approved to commence Phase II clinical trials, while other enterprises aligning with the positioning of the STAR Market must demonstrate clear technological advantages and meet corresponding requirements.

The aforementioned Item (5) constitutes the fifth set of listing criteria for the STAR Market. This framework is characterized by waiving rigid requirements for operating revenue, net profit, and cash flow, in favor of more flexible criteria such as “an estimated market capitalization of no less than RMB 4 billion, approval of core business or products by relevant national authorities, substantial market potential, achievement of interim milestones (e.g., Phase II clinical trials), and significant technological advantages.” In effect, this substantially lowers the bar for companies seeking an initial public offering.

It is well known that the first decade after establishment is particularly challenging for innovative drug companies. A drug must undergo drug discovery, preclinical research, and Phase I, II, and III clinical trials before it can be approved by regulatory authorities and marketed. The cycle from research and development to market launch typically spans 7–10 years, with investments generally ranging from RMB 100 million to RMB 1 billion. Therefore, innovative drug companies need strong financing capabilities to survive. However, the A-share market has long had explicit profitability requirements for initial public offerings (IPOs), preventing start-up innovative drug companies from accessing the domestic capital market before they mature into established enterprises. As a result, these companies have primarily relied on financing from private equity/venture capital (PE/VC) firms and overseas capital markets. Given the significant uncertainty surrounding listings in this sector, PE/VC firms’ overall level of investment has been relatively low. Compared with the substantial venture capital allocated to other sectors, investment in innovative drug companies has been merely a drop in the bucket.

The establishment of the fifth listing standard on the STAR Market has made it possible for start-up innovative drug companies to access China’s capital markets at an early stage of their development. Once this pathway is proven viable, it will significantly stimulate investment enthusiasm among private equity (PE) and venture capital (VC) firms in this sector. In effect, the fifth listing standard has substantially broadened financing channels for innovative drug companies and improved their funding landscape.

Although listing on capital markets in regions such as Hong Kong, China, and the United States offers an alternative pathway for innovative drug companies, the STAR Market possesses significant inherent advantages. First, its more market-oriented price-to-earnings (P/E) ratio for initial public offerings enables these companies to raise ample capital. Second, the A-share market’s characteristics of high valuations and high liquidity facilitate growth in corporate market capitalization. Third, listing on the STAR Market enhances the visibility of innovative drug companies, thereby supporting the subsequent launch and promotion of their products.

II. Unprofitable Innovative Drug Companies Must Meet Multiple Regulatory Requirements of the STAR Market

Given the potential risks that unprofitable companies may face in their subsequent development, the STAR Market has adopted a regulatory approach that balances flexibility with strictness for such enterprises. On one hand, it has relaxed the profitability requirements for listing; on the other hand, it has imposed targeted requirements on unprofitable companies in various aspects, including information disclosure, the proportion of offline placements, restrictions on share reductions, and delisting mechanisms.

Based on our review, these requirements include:

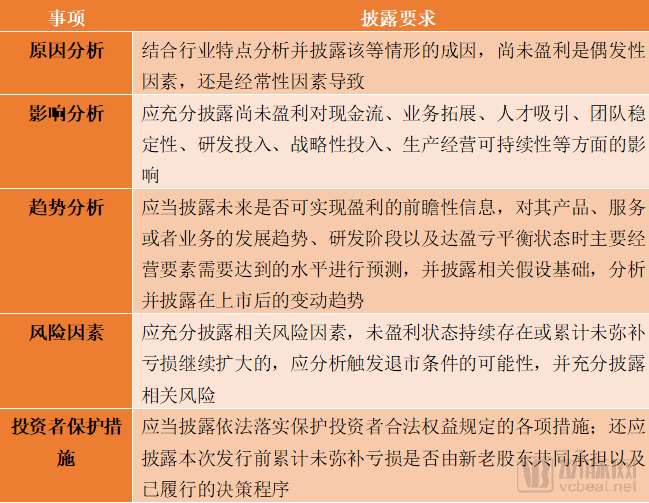

1. Strengthening Information Disclosure Requirements

During the listing review phase, the STAR Market requires pre-profit companies to provide more detailed information disclosure:

Unprofitable enterprises, after their initial public offering, shall continue to disclose the risks, causes, and impacts of their unprofitability in accordance with the requirements of the STAR Market. They are required to prominently disclose in their annual reports their core competitiveness and the significant risks facing their business operations.

2. Increase the Proportion Requirement for Offline Issuance

The STAR Market has increased the proportion of initial public offerings (IPOs) allocated to offline placement for unprofitable companies, requiring that no less than 80% of the total offering be placed offline. Compared with the 70% requirement for other companies whose total share capital after public offering does not exceed 400 million shares, the STAR Market mandates a greater allocation to institutional investors in the offline tranche for unprofitable issuers’ IPOs, thereby reducing the subscription proportion available to retail investors in the online tranche, who typically have lower risk tolerance.

3. Extension of the Lock-up Period for Share Reduction by Special Shareholders

The STAR Market has extended the lock-up period for share reductions by special shareholders of unprofitable companies after their listing. It requires that, for unprofitable companies, controlling shareholders, actual controllers, directors, supervisors, senior management personnel, and core technical staff shall not reduce their pre-IPO shares within three full fiscal years from the date of the company’s stock listing until profitability is achieved. During the fourth and fifth fiscal years following the listing date, controlling shareholders and actual controllers may not reduce more than 2% of the company’s total shares per year from their pre-IPO holdings.

4. Delisting Mechanism

For unprofitable companies, the STAR Market does not solely use consecutive losses as a delisting criterion. Instead, a company will be subject to a delisting risk warning if its audited net profit (before or after deducting non-recurring gains and losses) for the most recent fiscal year is negative, and its audited operating revenue for that same period is less than RMB 100 million, or if its audited net assets are negative.

In particular, the STAR Market has established special provisions for R&D-focused listed companies applying under Listing Standard V, granting them a three-year development period and requiring such companies to comply with the aforementioned regulations starting from the fourth full fiscal year after their listing date. Meanwhile, in view of the unique characteristics of R&D-focused listed companies, the STAR Market mandates that if their core business, products, or underlying foundational technologies fail in development or are prohibited from use, and no other businesses or products meet the criteria of Listing Standard V, these companies shall be subject to a delisting risk warning.

III. Review Dynamics for Innovative Drug Companies Applying under the Fifth Set of Listing Criteria and Key Focus Areas of the Shanghai Stock Exchange

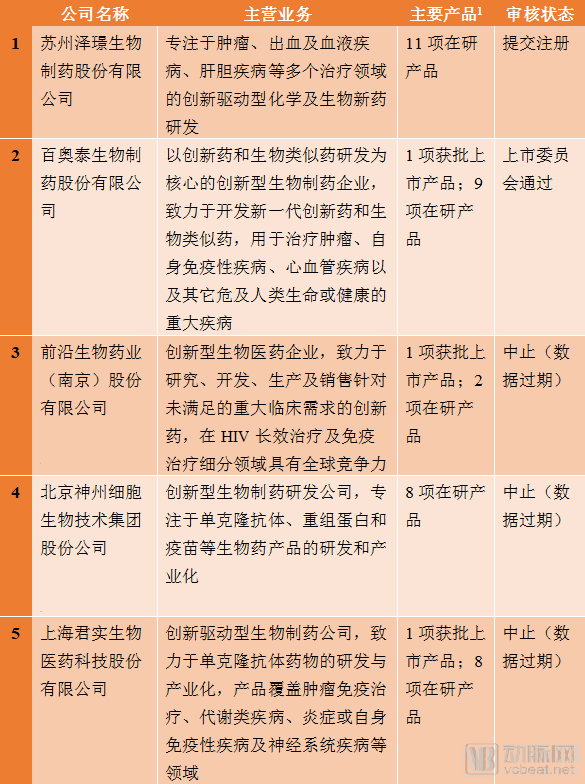

As of November 25, 2019, a total of 31 biopharmaceutical companies had applied for listing on the STAR Market [1]. Among them, 11 were primarily engaged in the research and development and production of innovative drugs, and 5 unprofitable innovative drug companies all adopted the fifth set of listing criteria. Based on the information disclosed in the prospectuses of these innovative drug companies, their main profiles are as follows:

Data Source: iFinDiFinD。

We have compiled and analyzed the inquiry letters issued by the Shanghai Stock Exchange (SSE) to these five companies. In addition to focusing on routine matters such as actual controllers, clarity of equity structure, related-party transactions, share-based payments, and accounting treatment of R&D expenditures, the SSE placed greater emphasis on the companies’ business operations, technologies, and innovativeness. Through its inquiries, the SSE sought to assess the competitive advantages and future development trends of these pre-profit innovative drug companies, and required them to enhance risk disclosures regarding their unprofitable status and products under development, primarily covering the following aspects:

1. Advancement and Origin of Core Technologies

Companies planning to go public are required to fully disclose the advancement of their existing core technologies and their position relative to domestic and international development levels. They must also explain whether there is a risk that their core technologies could be replaced or phased out by other technologies in the international and domestic markets in recent years, and whether these core technologies can support the smooth progress of all products in the research and development pipeline as well as the development of future products. Meanwhile, companies planning to go public need to fully disclose the source of their core technologies—whether they are independently developed, jointly developed, or externally procured—and clarify whether the process of formation or acquisition was legal and compliant.

2. R&D Strength

Companies planning to go public are required to fully disclose their R&D capabilities, clarify whether core products and pipeline drugs are independently developed or in-licensed from external parties, and detail their collaborations with CROs (including specific procurement amounts, any dependency issues, the extent of the CROs’ contributions to the development of pipeline products, and ownership of intellectual property rights).

3. Product Pipeline Progress and Competitive Landscape

Prospective listed companies are required to fully disclose the approval progress of each pipeline under development, explain the domestic and overseas competitive landscape of key products entering clinical trial phases, as well as their post-launch market potential, competitive advantages, development prospects, and revenue outlook, and comprehensively disclose risks associated with each product under development.

4. Commercialization Expectations for Products Under Development

Prospective listed companies are required to fully disclose the average time required and validity period for inclusion of new drugs in the national and provincial medical insurance catalogs following successful R&D; post-launch business and operating models, marketing plans, sales team size and experience, and sales strategies; the costs and projected timeline for commercialization of core products; and potential commercialization risks that may arise after the new drug is launched.

5. Risks Exist in the R&D and Commercialization of the Pipeline Under Development

Companies planning to go public are required to fully disclose the risks associated with the research, development, and commercialization of their pipeline products, including: risks in drug candidate selection; clinical development risks; risks associated with collaborative R&D; regulatory review and approval risks; the risk that projects not yet entered into clinical trials may fail to obtain clinical trial approvals or be rendered obsolete by technological advancements; and the risk that investigational drugs may ultimately fail to obtain marketing authorization.

6. Risks Faced by Biopharmaceutical Companies Applying Standard Five

Prospective listing companies must fully disclose, in light of the characteristics that their products are not yet marketed and that substantial subsequent R&D investment is required, that: (i) the Company’s products have not yet been launched for commercial sale, the Company is not currently profitable and expects to continue incurring losses; (ii) the Company has an extensive product pipeline and anticipates sustaining significant R&D expenditures in the future; (iii) the Company cannot guarantee obtaining regulatory approval for new drug launches, and there is uncertainty regarding the commercialization of its core investigational drugs; and (iv) the Company cannot assure profitability within the next several years and may face delisting risks after its initial public offering.

7. Risk of Accumulated Uncovered Losses and Continued Losses

Companies planning to go public are required to disclose that, due to their ongoing losses, they may be unable to achieve profitability or distribute profits within a certain future period. Such circumstances may impose restrictions or have adverse effects on the company’s financial position, R&D investment, business expansion, talent acquisition, and team stability. The company’s revenue may fail to grow as planned, it may face the risk of triggering delisting criteria after its listing, and its losses may continue to widen.

IV. Conclusions and Recommendations

Zelgen Pharmaceuticals’ successful passage through the listing review also signifies that the STAR Market has truly entered the competition with the Hong Kong Stock Exchange and NASDAQ for high-quality biopharmaceutical companies. However, it should be noted that the STAR Market’s de-emphasis on profitability requirements does not imply a disregard for corporate development prospects. Through its inquiries directed at currently unprofitable innovative drug companies, the Shanghai Stock Exchange (SSE) places greater emphasis on these enterprises’ business operations, technology, and innovativeness, requiring prospective listed companies to fully disclose their development trends, competitive advantages, and potential risks. This approach further enables the market to assess the value of unprofitable enterprises. We look forward to more high-quality Chinese pharmaceutical companies listing on the STAR Market, collectively establishing an advanced capital market segment that prioritizes technology, innovation, and the future.

Author: Anjie Health Team

Contact WeChat ID: zjqc111111

Lead Counsel of the Team: Lawyer Cai Hang

Introduction to Cai Hang: With over a decade of focus on investment and financing services in the healthcare, TMT, and artificial intelligence sectors, he has exerted significant influence in the field of venture capital legal services in China. *China Business Law Journal* has named him one of the “Top 100 Legal Elite in China,” recognizing him as one of the country’s most outstanding commercial lawyers. He has also been repeatedly recommended by leading legal ranking agencies such as The Legal 500 and Legalband in the fields of TMT and venture capital. In addition to venture capital practice, he is highly proficient in mergers and acquisitions and capital markets. Mr. Cai Hang serves as the Managing Partner of AnJie Broader’s Shanghai office.

Author

Jin Meina

Jin Meina: Primarily engaged in advisory services for domestic and overseas listings, private equity financing and investment, and mergers, acquisitions, and restructuring. She has provided consulting to numerous renowned investment institutions on domestic and cross-border private equity investments, and offered services to corporate groups for M&A transactions and public listings. Additionally, she possesses extensive experience in fund establishment and fundraising, registration of fund managers, and regulatory compliance for funds.